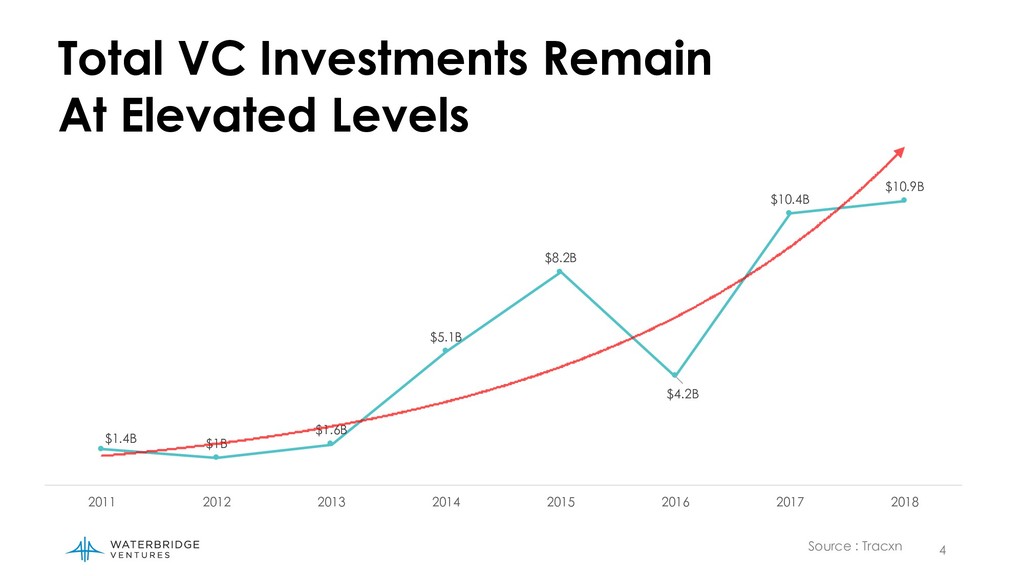

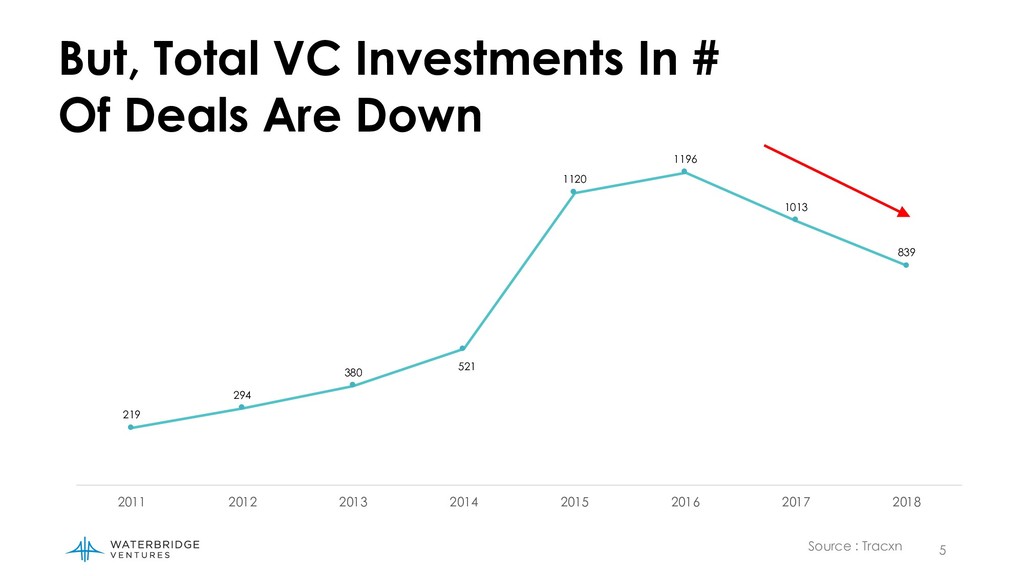

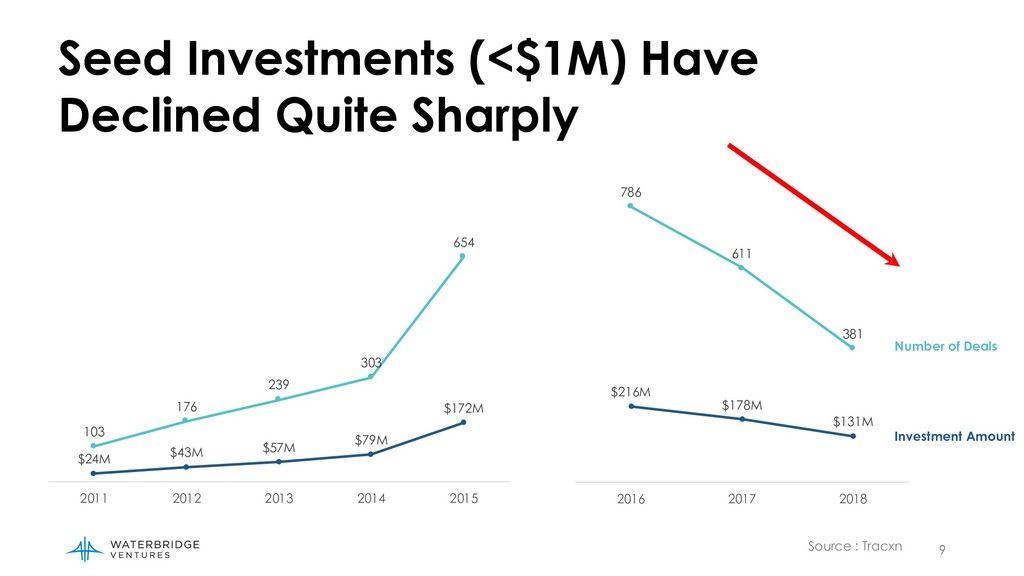

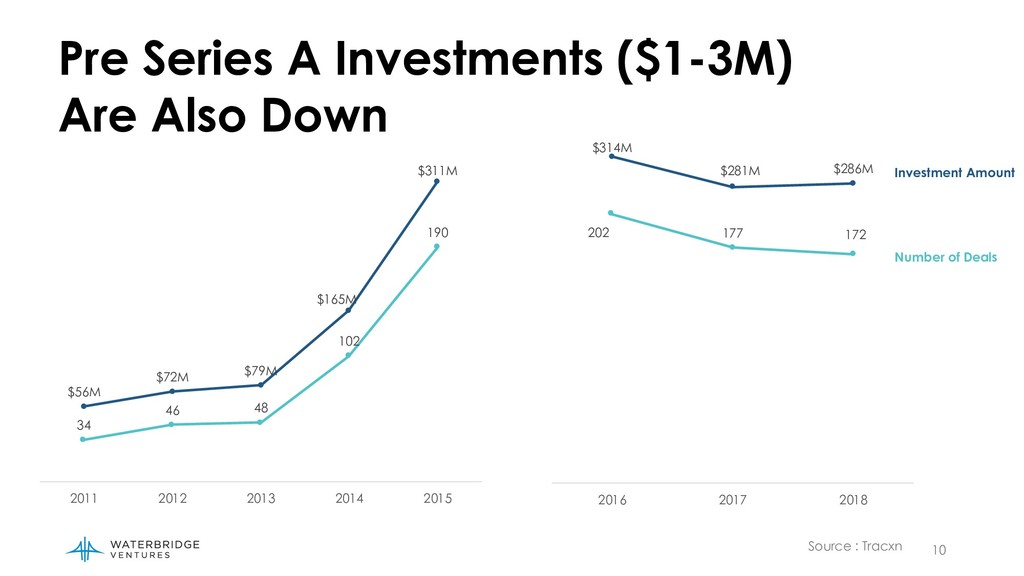

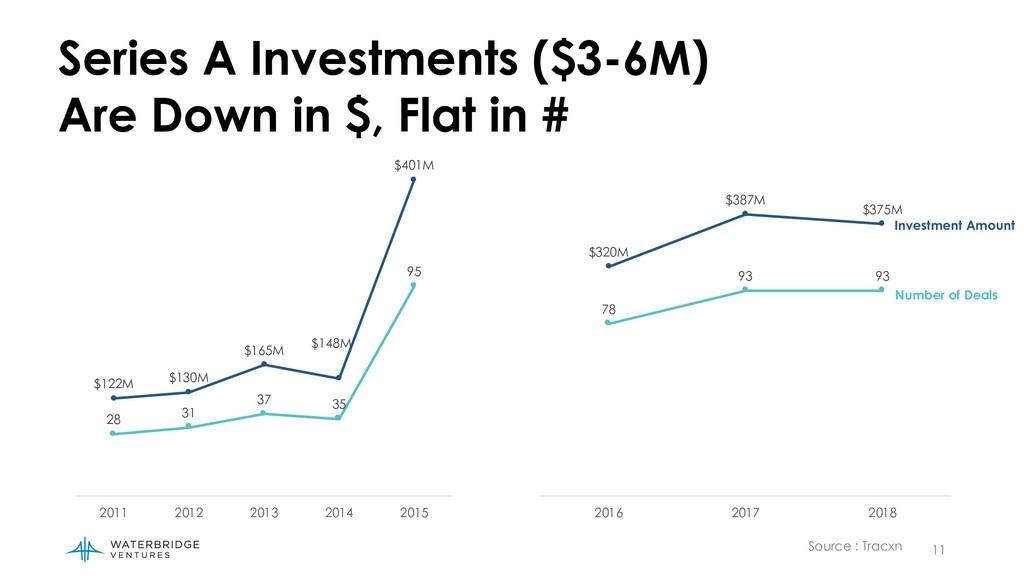

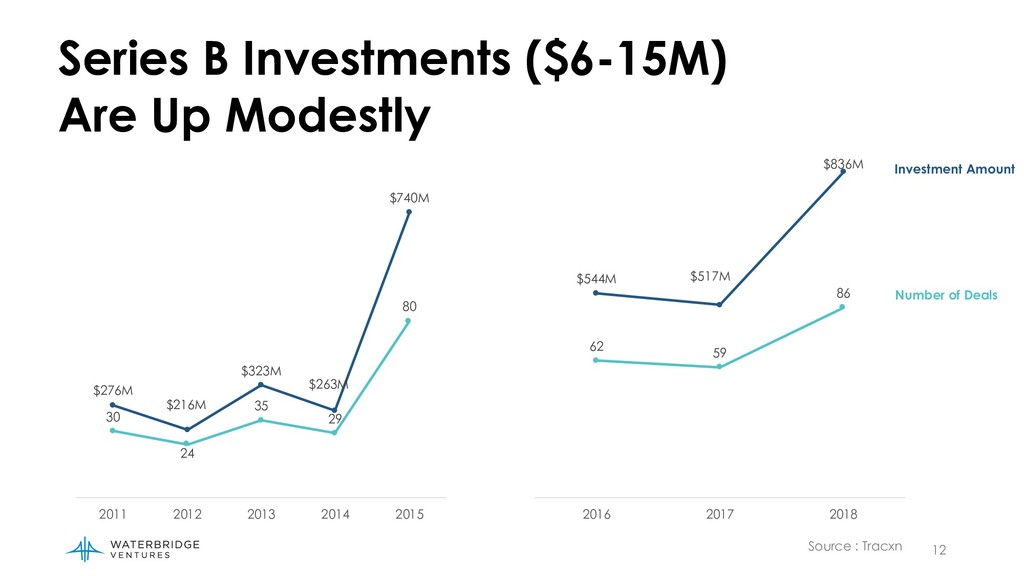

Venture Capital is coming of age in India with a second successive year of $10Bn+ in investments. There is much talk of Unicorns and multi $100 million funding rounds with the occasional flourish of even a $1 Bn+ round. Everyone is in on the action – government, media and general citizens. However, there are a few whispers of discontent. A feeling that perhaps all is not as real as it is made out to be. Some of it tinged by envy of those who missed out, some from the not so hot sectors who feel left out and some from the general it cant be so easy gang. More importantly, even within the eco system, there is a feeling of inequality, a lot of concern around the difficulty of raising money, a feeling that only the big are getting bigger and no one cares about the small.

So which of these narratives is true? Are the headline numbers real? Or are the concerns valid? We at WaterBridge Ventures decided to get into the debate starting from first principles. We have looked at data for the last 8 years both in aggregate and in relevant slices to bring to you the reality of the Indian venture capital eco system.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}