(Cornell) “Debt Dictionaries” aka “Bonds are from Venus, Stocks are from Mars” Disclaimer: The views expressed here are those of the authors, and not the Federal Reserve

segmentation across debt and equity markets • Lead-lag pricing: ◦ Kwan (1996), Addoum and Murfin (2020) • Distinct pricing kernels: ◦ Collin-Dufresne, Goldstein, and Martin (2001) ◦ Choi and Kim (2018) ◦ Van Binsbergen, Nozawa, Schwert (2023)

plus… • Different information? • Different preferences? We propose: same information, • but different models of inference • and associated (risk neutral?) expectations

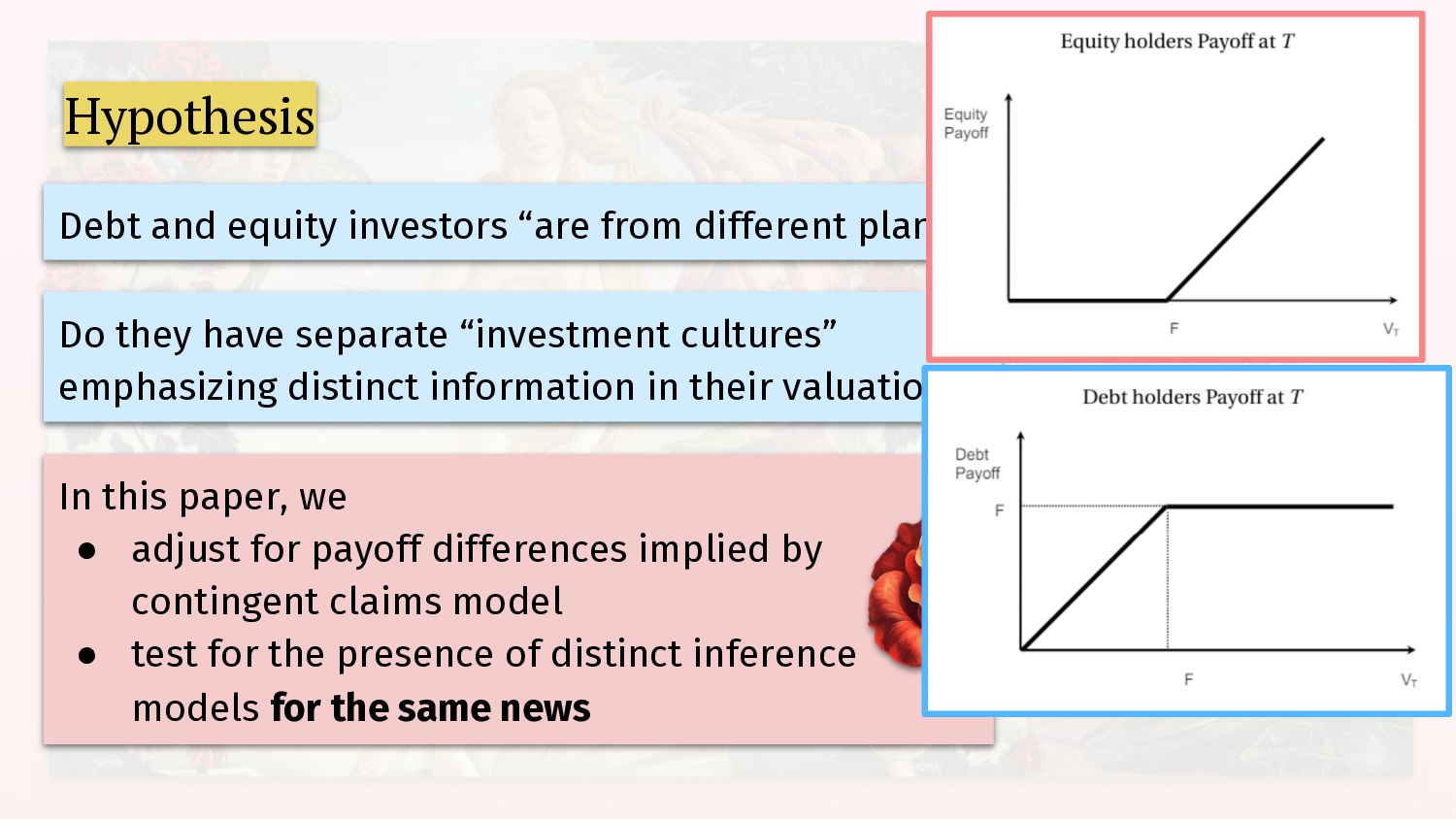

in their valuations? Debt and equity investors “are from different planets!” • Stock and bond investors are segregated across and within institutions • Different training and education background (American Community Survey) • Consume different media (Baron’s vs Euromoney) • Perhaps even social networks? Even the same investor group may engage in categorical thinking, using different models for bonds and stocks

in their valuations? Debt and equity investors “are from different planets!” In this paper, we • adjust for payoff differences implied by contingent claims model • test for the presence of distinct inference models for the same news

in their valuations? Debt and equity investors “are from different planets!” In this paper, we • adjust for payoff differences implied by contingent claims model • test for the presence of distinct inference models for the same news

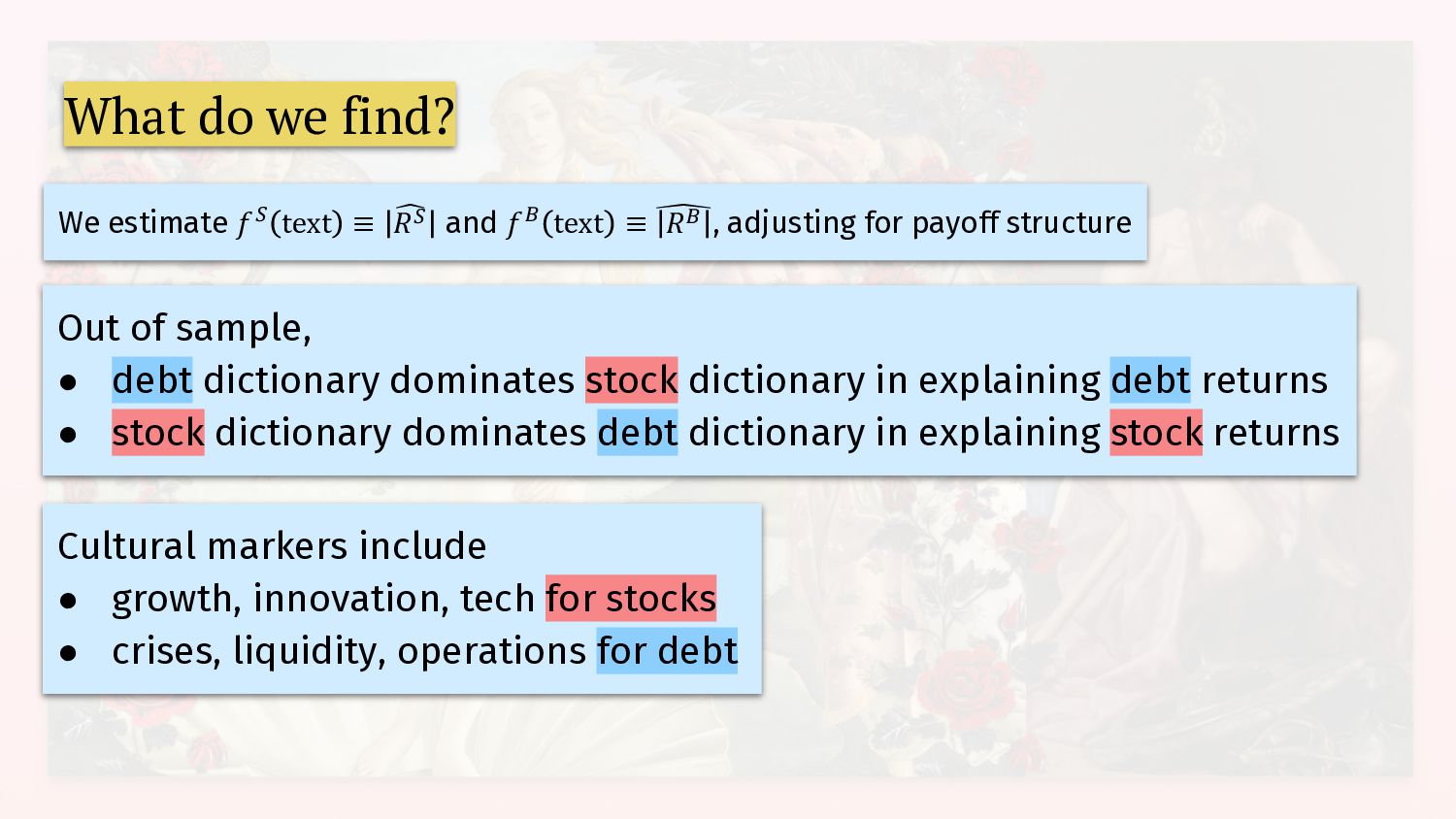

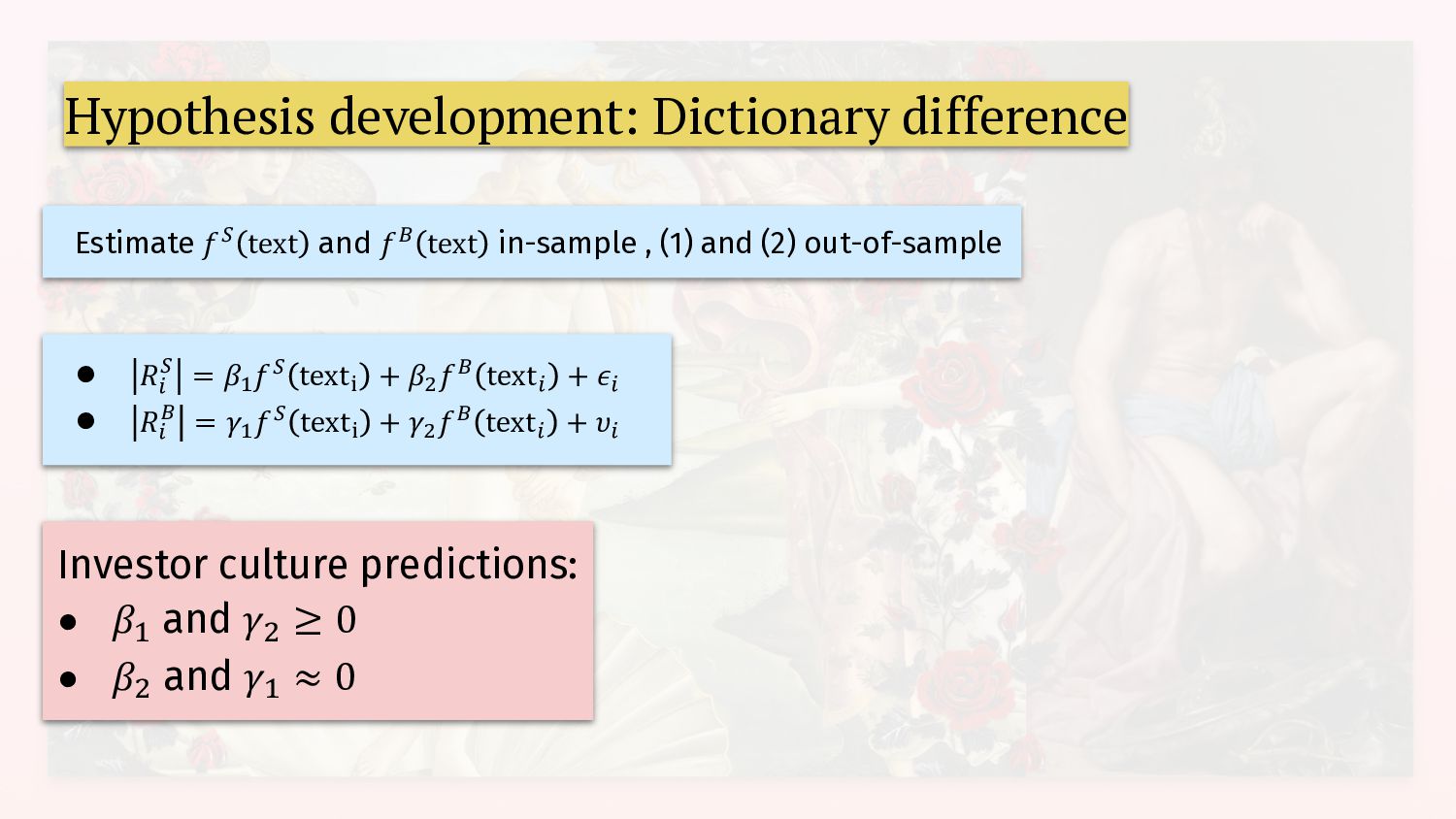

≡ ( 𝑅" Formally, to identify investment culture, we establish a mapping of textual information to value (we call it dictionary) Examine R# and R$ (adjusted for payoff differences) around earnings calls • Information is fixed • Investor cohorts and interpretation can vary • Loosely, 𝐻% : 𝑓! text = 𝑓"(text)

evidence on cultural variation in word meaning (Thompson, Roberts, Lupyan, 2020) Corporate culture comes from “implicature”– a mapping between utterances and interpretation based on shared experience or norms (Gorton and Zentefis, 2018) Resulting dictionaries are observable and interpretable

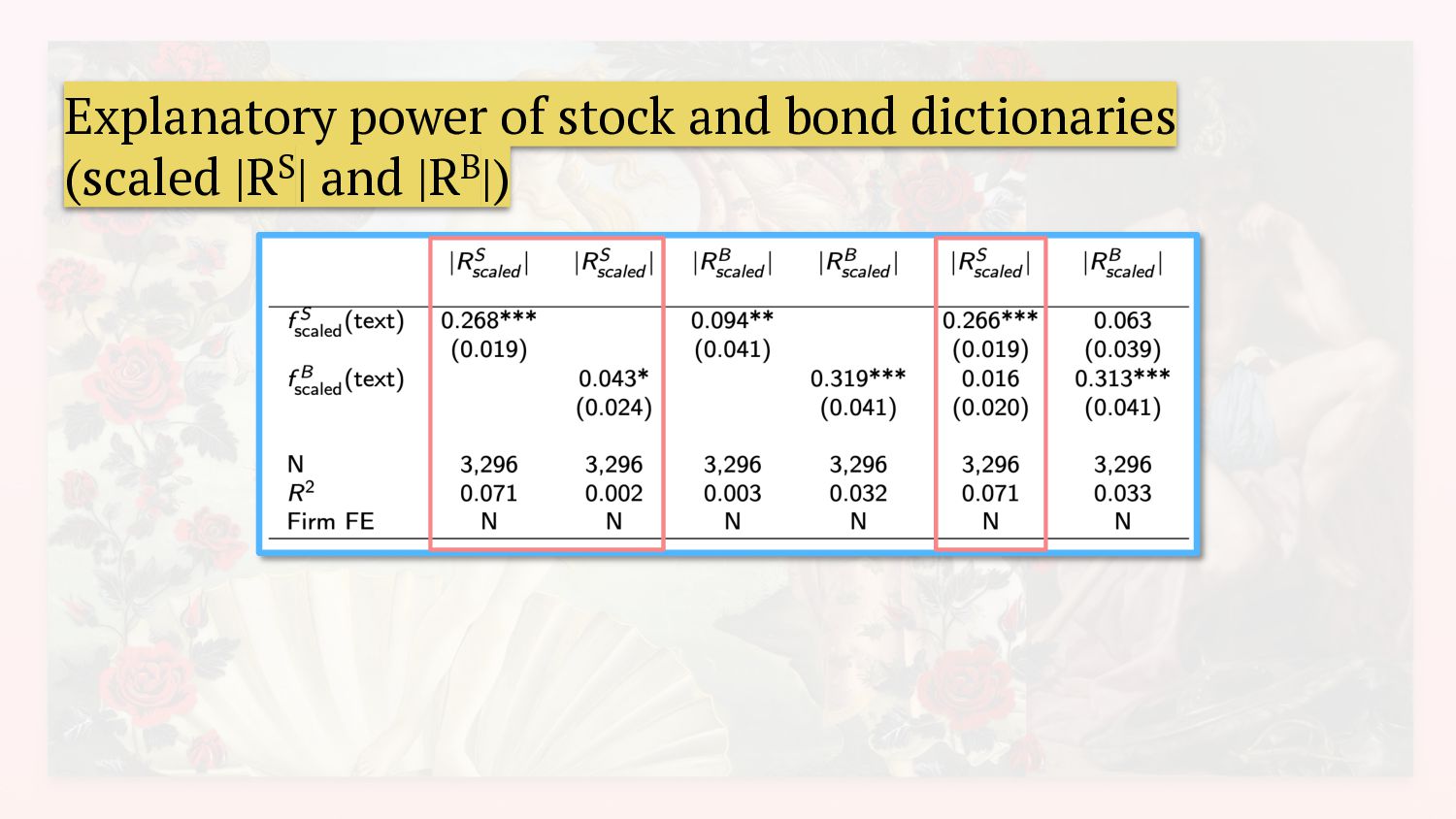

𝑅! and 𝑓" text ≡ ( 𝑅" , adjusting for payoff structure Out of sample, • debt dictionary dominates stock dictionary in explaining debt returns • stock dictionary dominates debt dictionary in explaining stock returns Cultural markers include • growth, innovation, tech for stocks • crises, liquidity, operations for debt

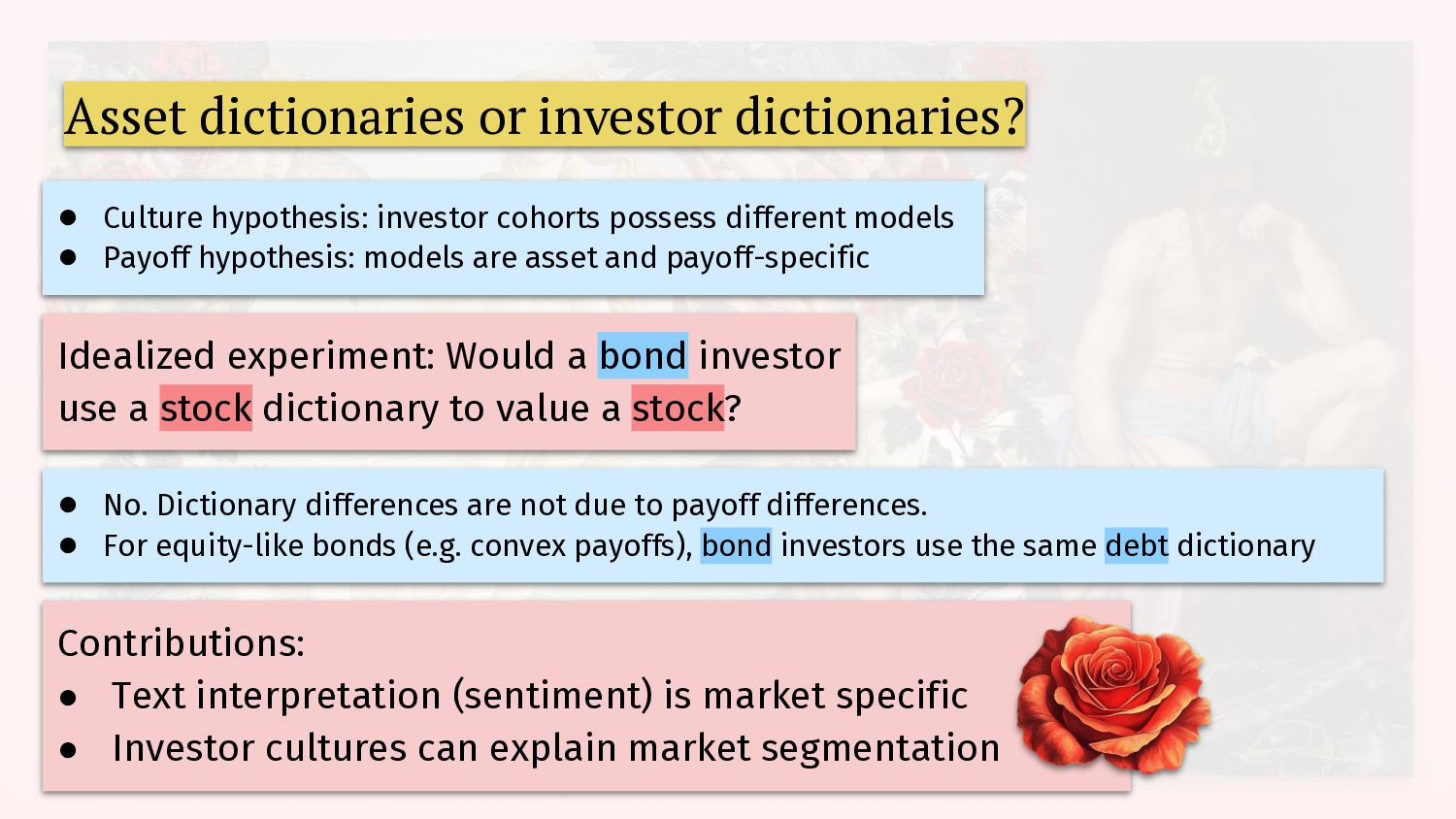

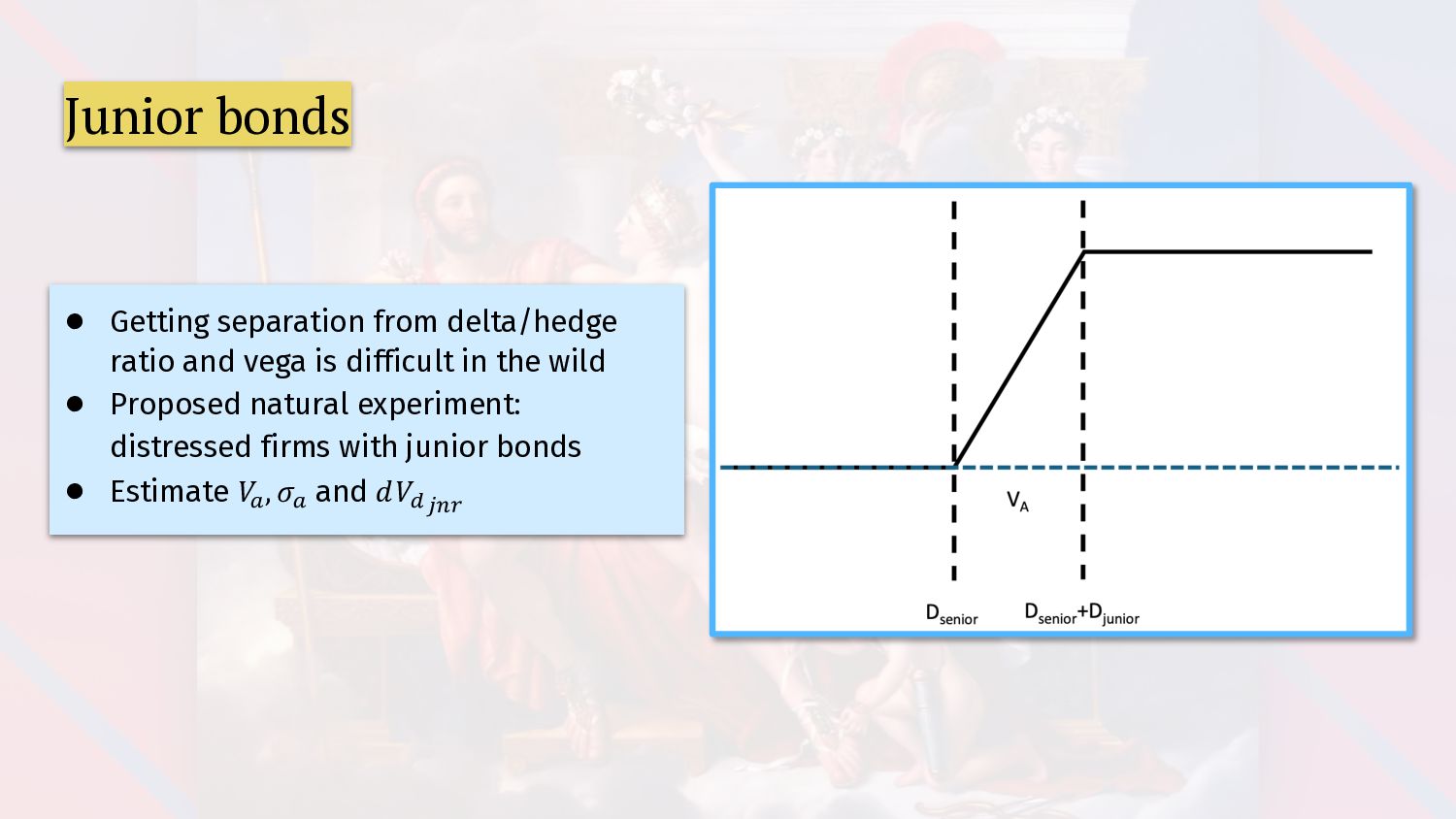

possess different models • Payoff hypothesis: models are asset and payoff-specific Idealized experiment: Would a bond investor use a stock dictionary to value a stock? • No. Dictionary differences are not due to payoff differences. • For equity-like bonds (e.g. convex payoffs), bond investors use the same debt dictionary Contributions: • Text interpretation (sentiment) is market specific • Investor cultures can explain market segmentation

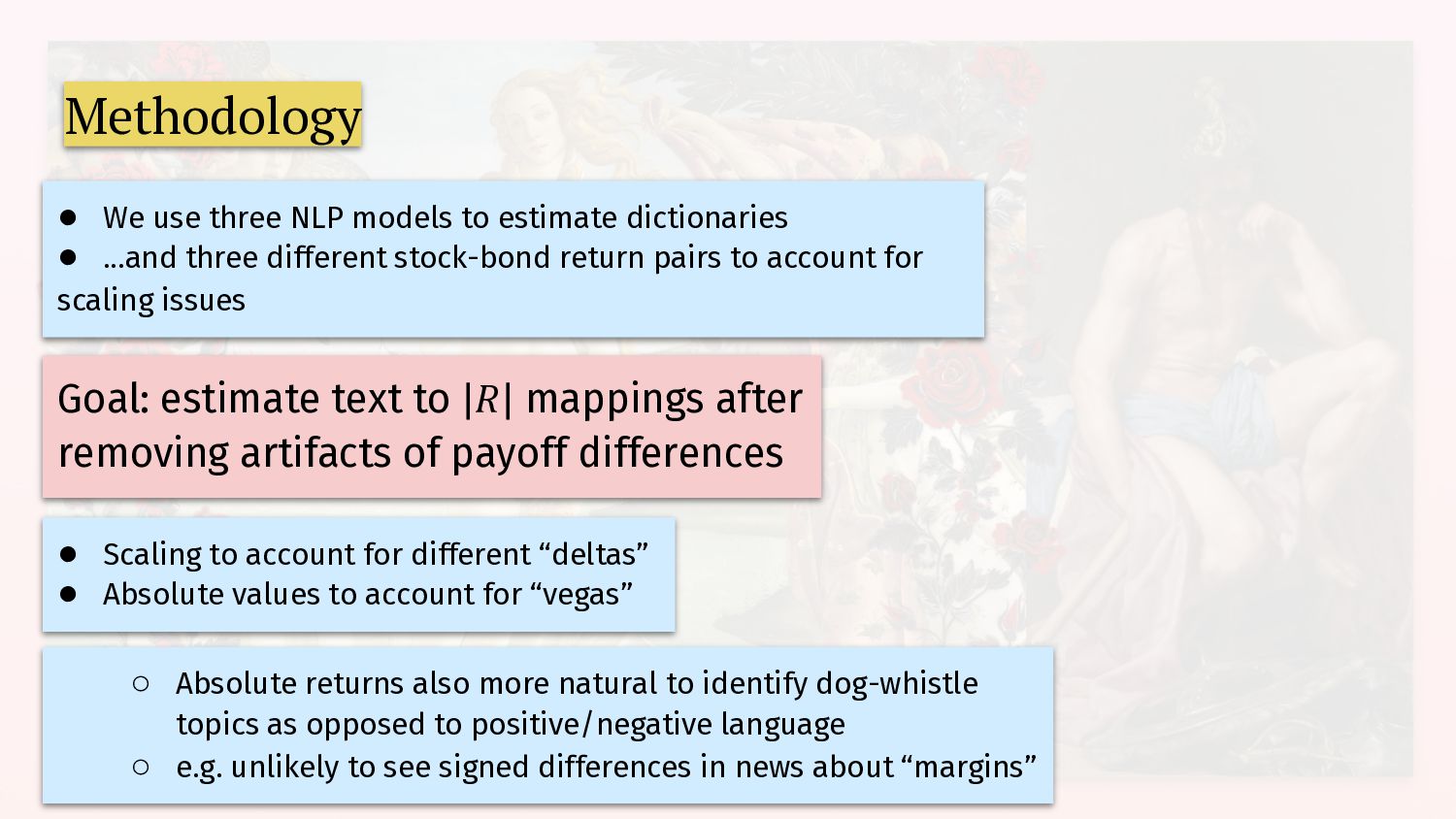

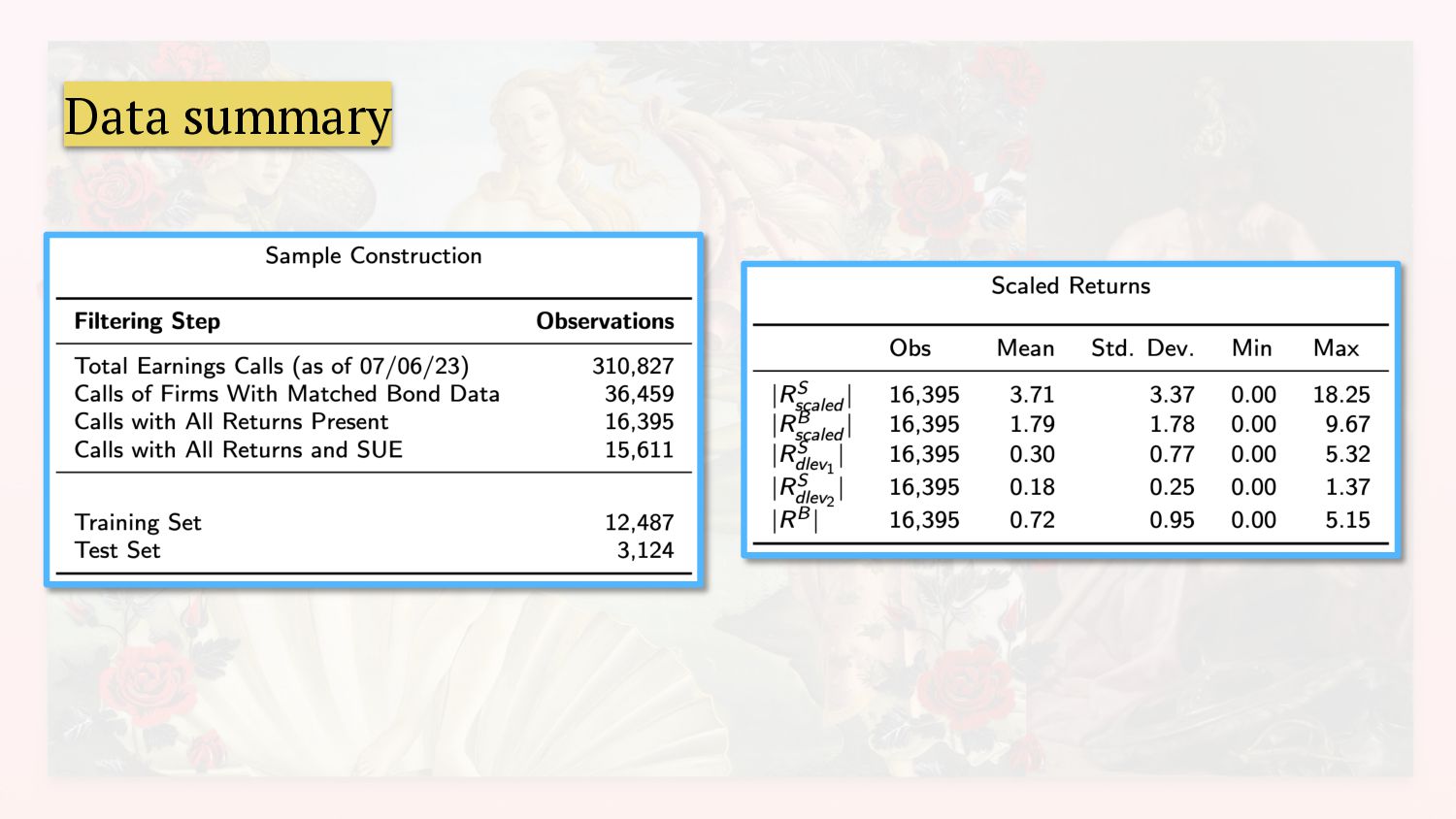

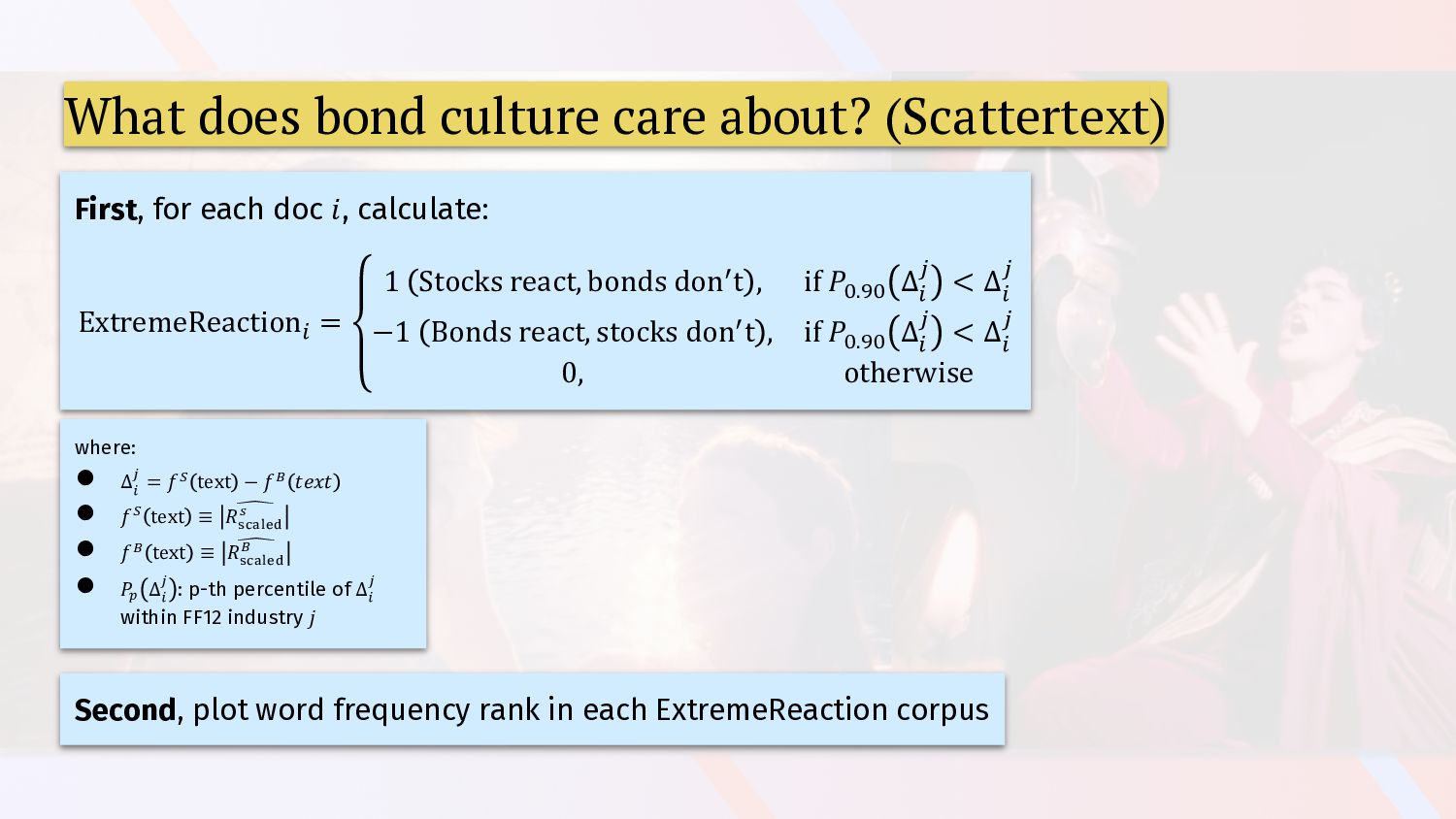

• ...and three different stock-bond return pairs to account for scaling issues • Scaling to account for different “deltas” • Absolute values to account for “vegas” ◦ Absolute returns also more natural to identify dog-whistle topics as opposed to positive/negative language ◦ e.g. unlikely to see signed differences in news about “margins” Goal: estimate text to 𝑅 mappings after removing artifacts of payoff differences

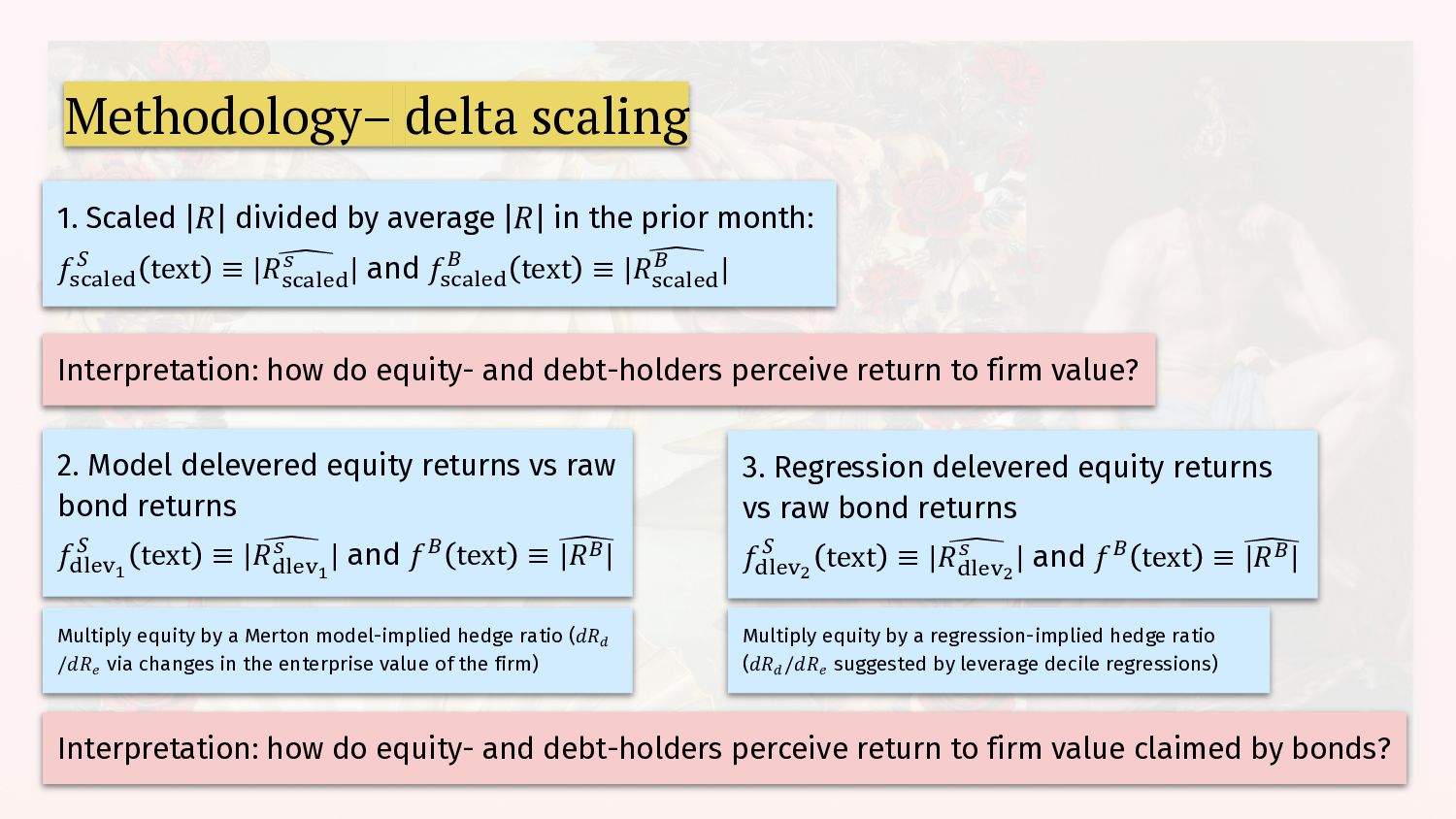

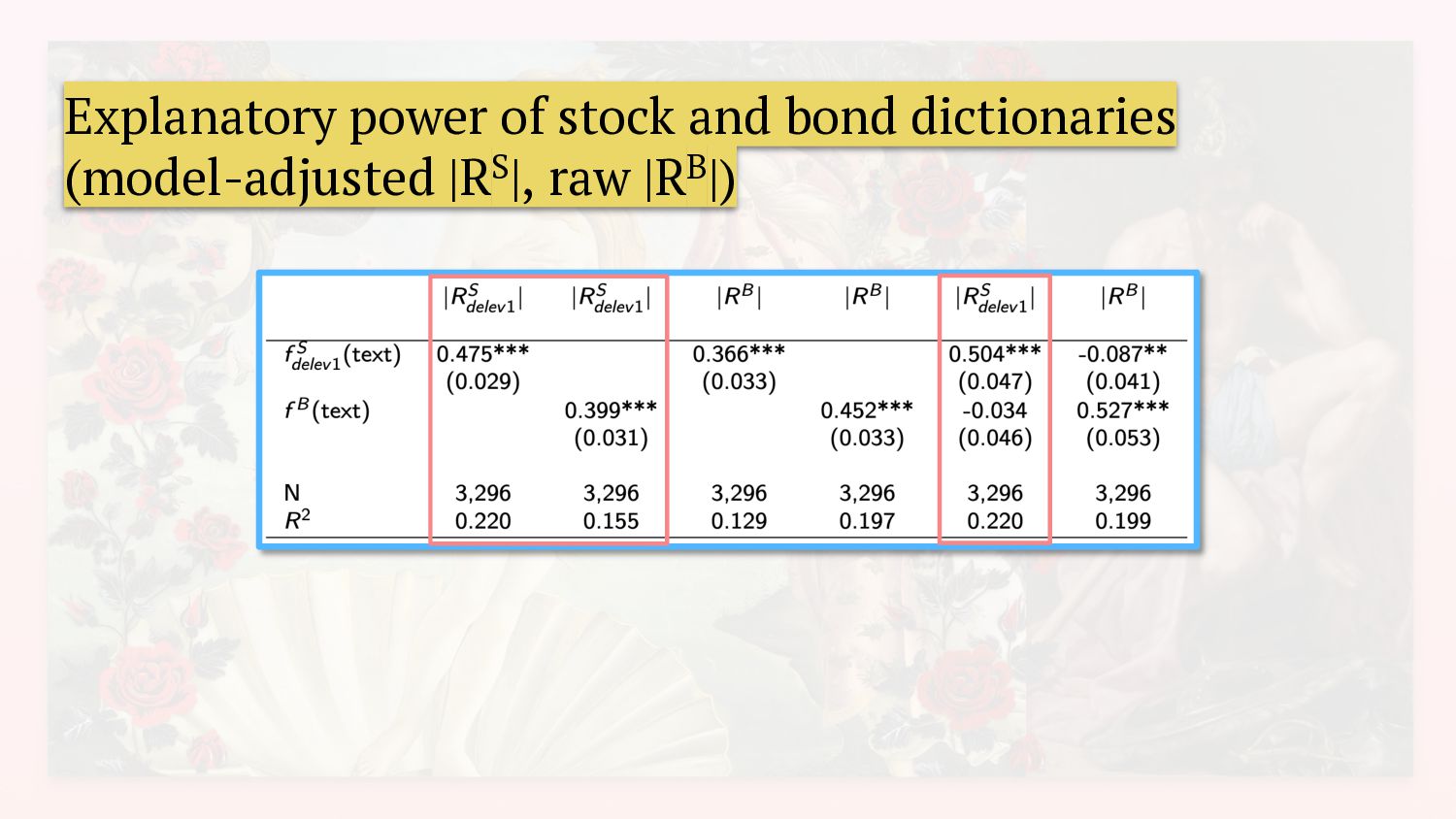

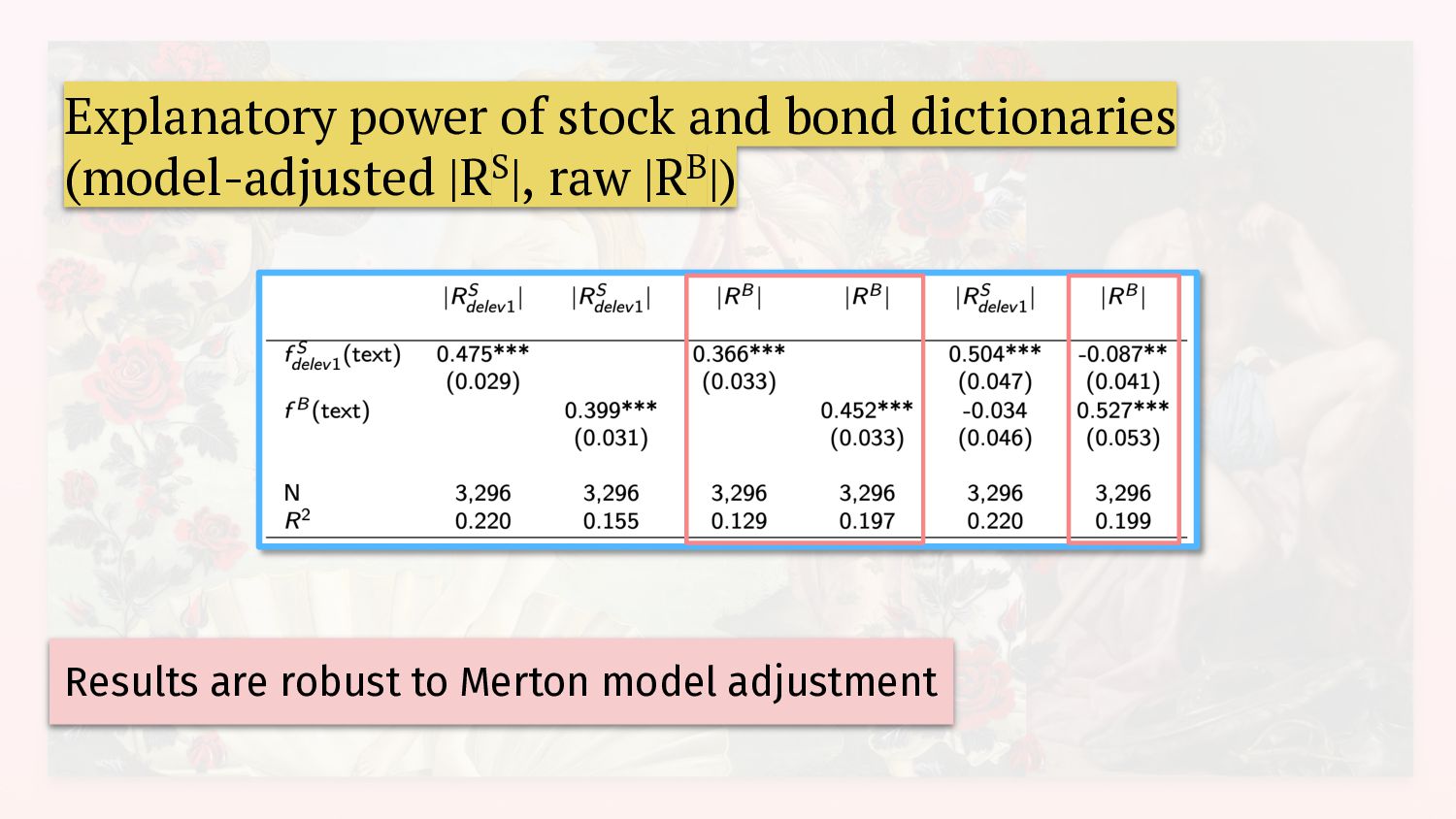

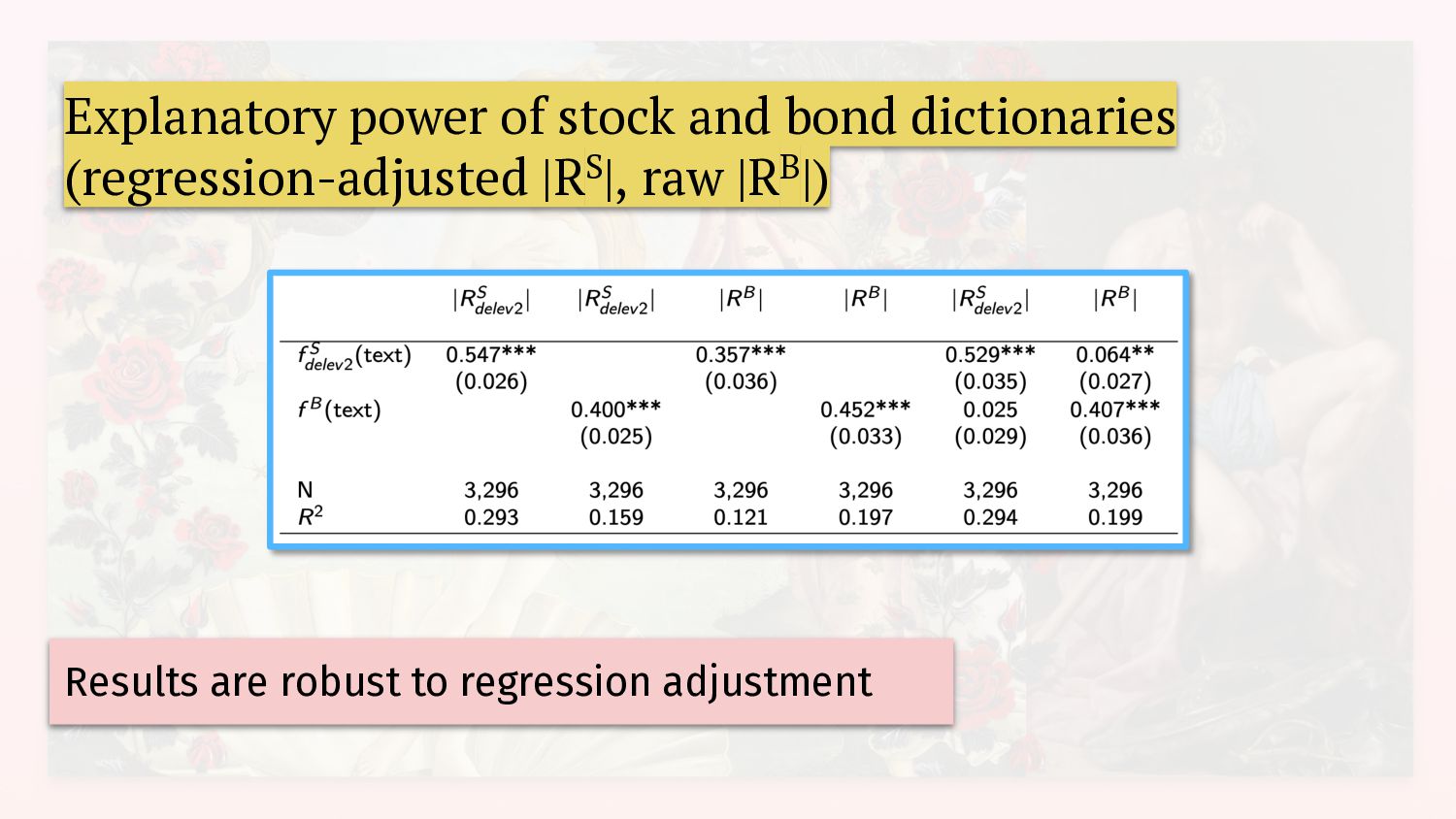

in the prior month: 𝑓#$%&'( ! text ≡ ( |𝑅#$%&'( ) | and 𝑓#$%&'( " text ≡ ( |𝑅#$%&'( " | Interpretation: how do equity- and debt-holders perceive return to firm value? 2. Model delevered equity returns vs raw bond returns 𝑓(&'*! ! text ≡ ( |𝑅(&'*! ) | and 𝑓" text ≡ ( |𝑅"| 3. Regression delevered equity returns vs raw bond returns 𝑓(&'*" ! text ≡ ( |𝑅(&'*" ) | and 𝑓" text ≡ ( |𝑅"| Multiply equity by a Merton model-implied hedge ratio (𝑑𝑅! /𝑑𝑅" via changes in the enterprise value of the firm) Multiply equity by a regression-implied hedge ratio (𝑑𝑅! /𝑑𝑅" suggested by leverage decile regressions) Interpretation: how do equity- and debt-holders perceive return to firm value claimed by bonds?

+ ridge regression • Multinomial Inverse regression • GTE embeddings + ridge regression Main specification: ensemble model combining three methods 🌹 All three models are consistent about basic facts

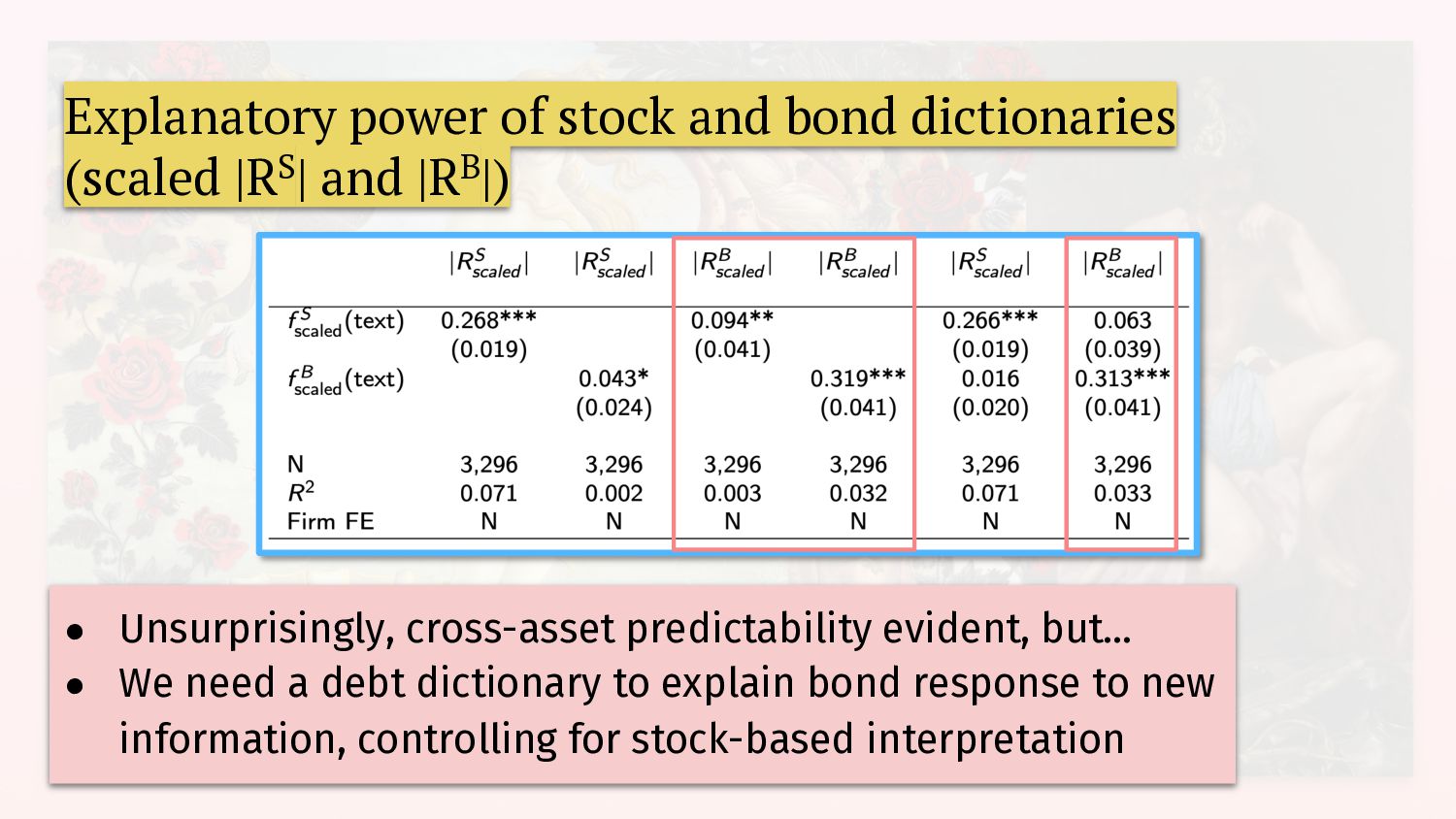

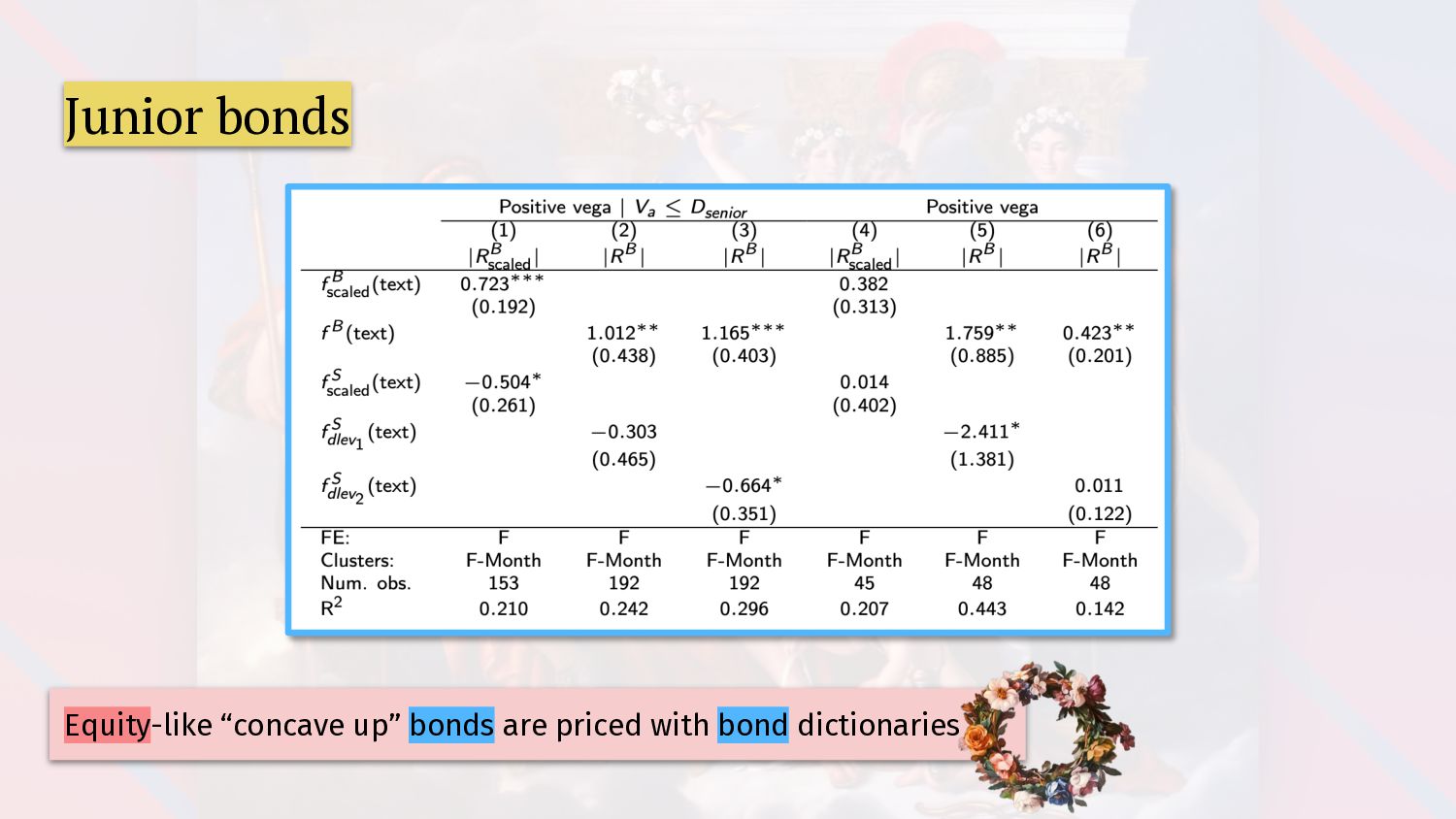

|RB|) • Unsurprisingly, cross-asset predictability evident, but... • We need a debt dictionary to explain bond response to new information, controlling for stock-based interpretation

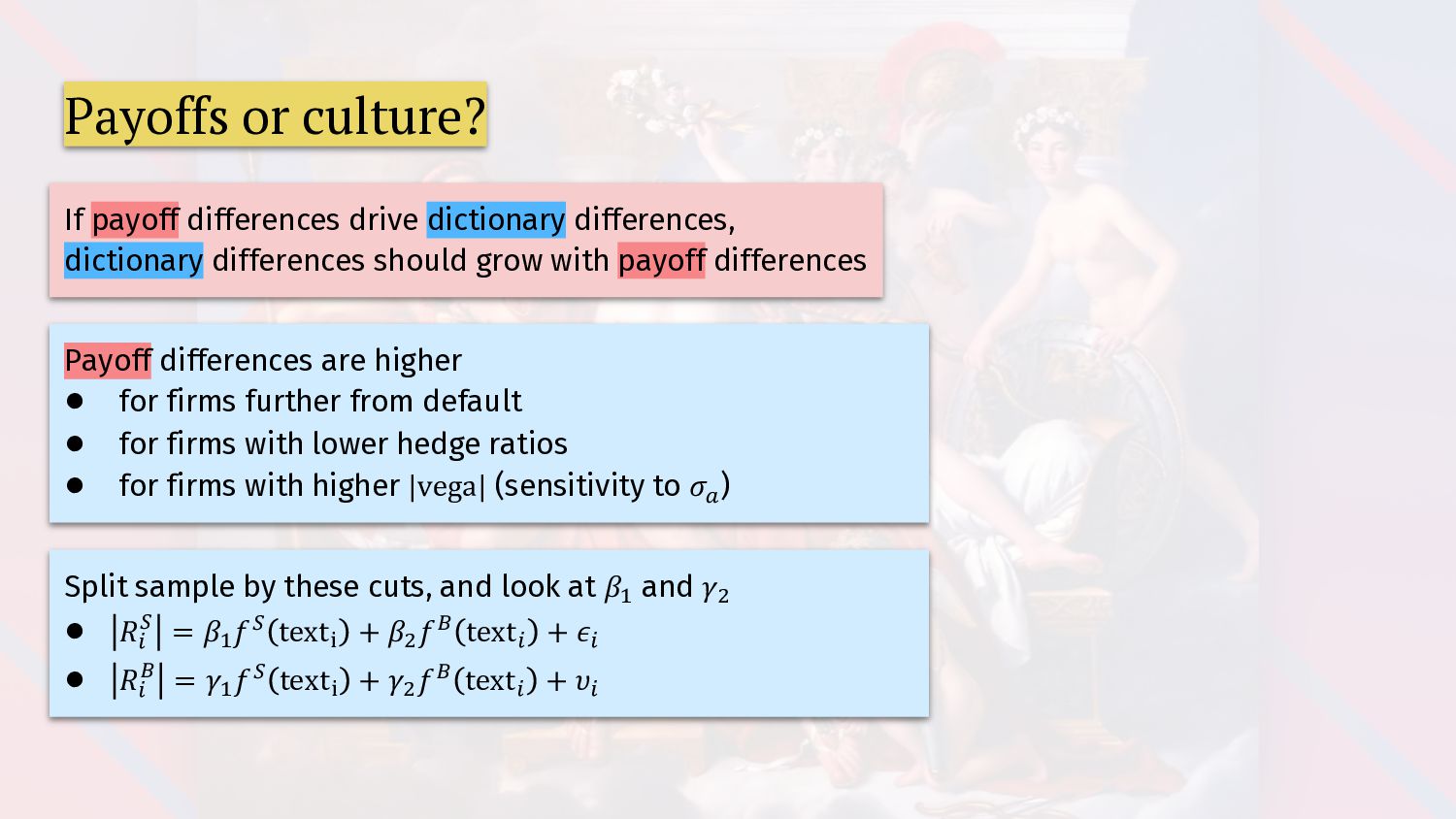

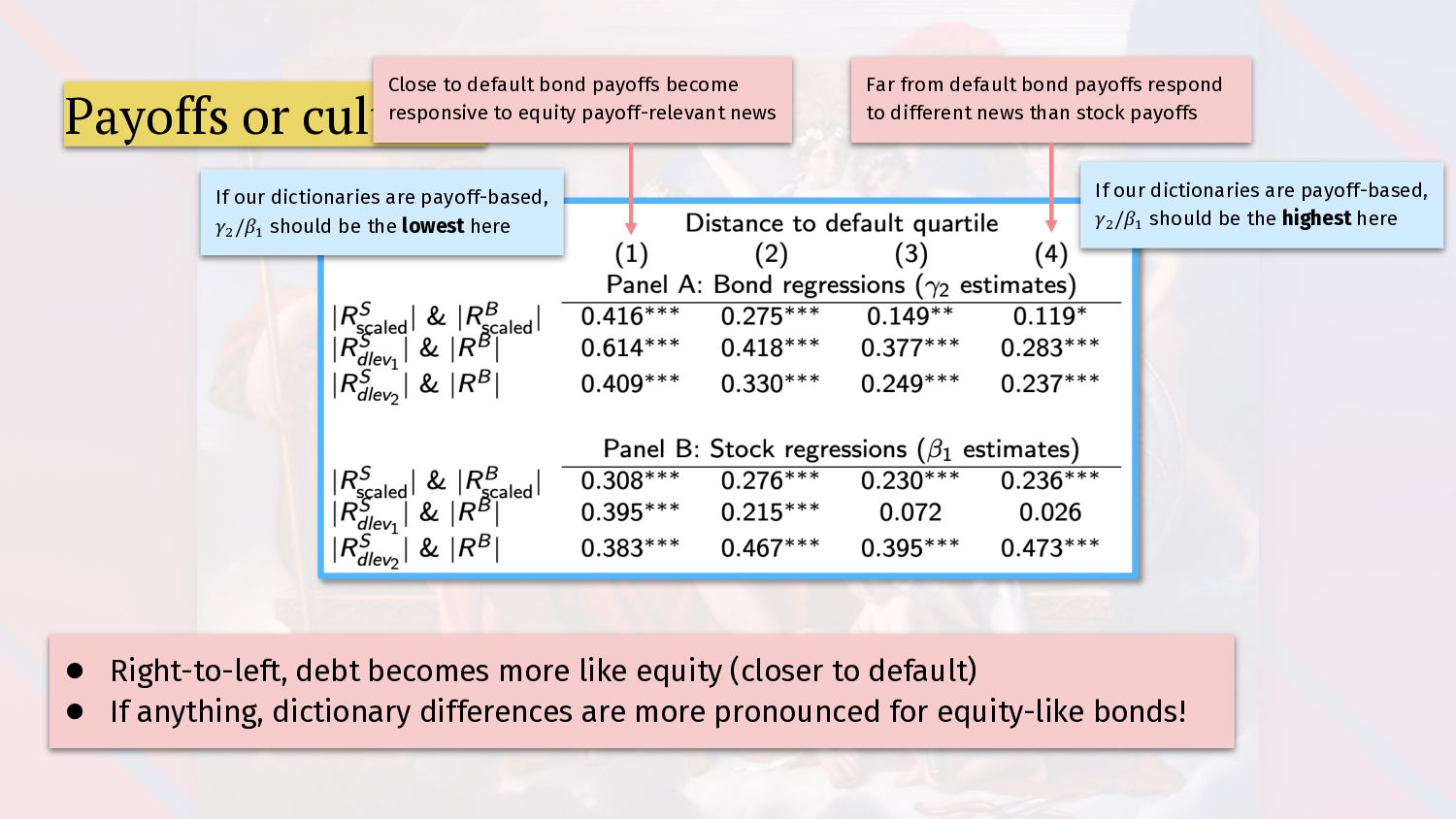

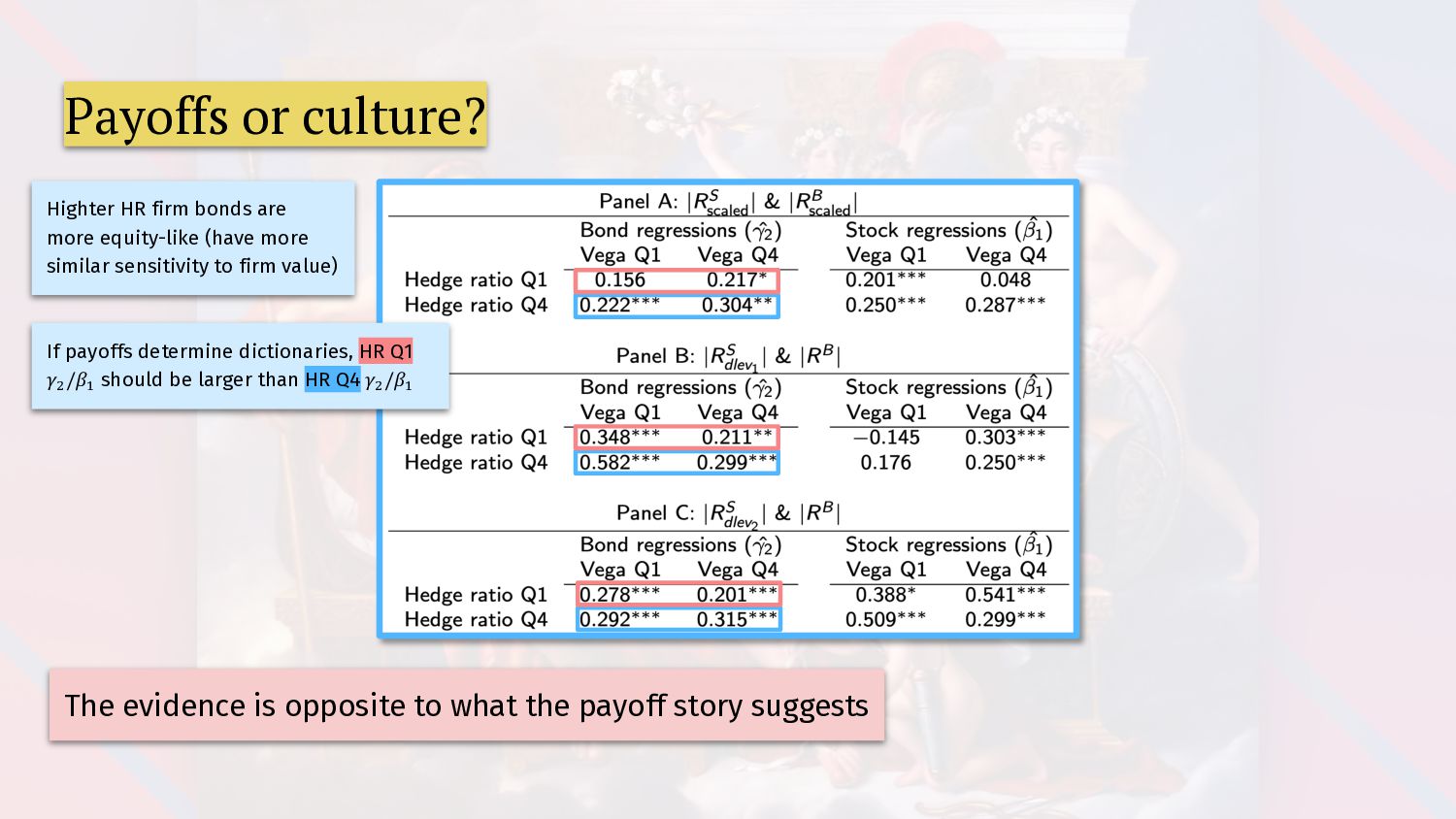

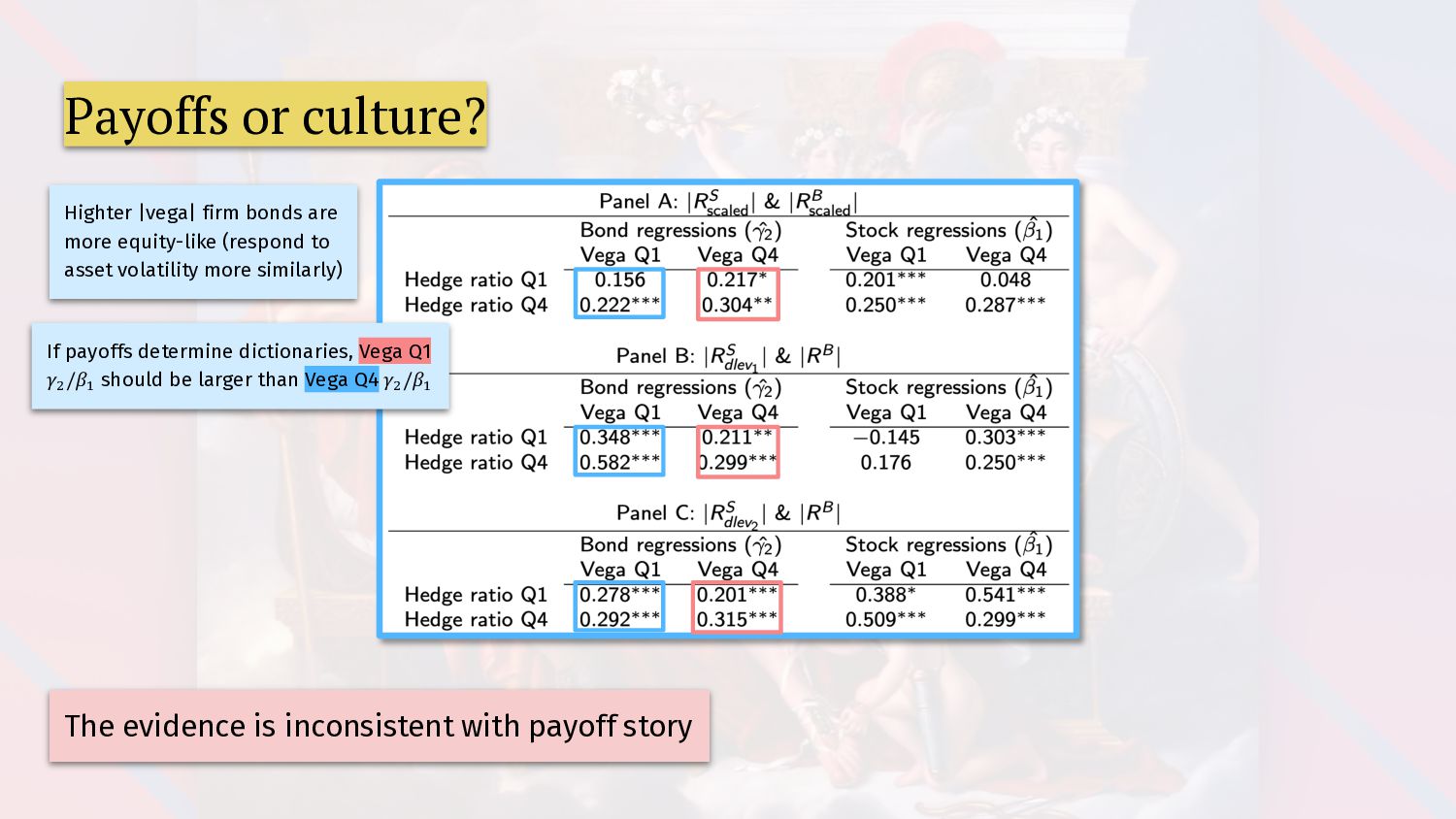

differences should grow with payoff differences Payoff differences are higher • for firms further from default • for firms with lower hedge ratios • for firms with higher |vega| (sensitivity to 𝜎/ ) Split sample by these cuts, and look at 𝛽, and 𝛾. • 𝑅+ ! = 𝛽, 𝑓! text- + 𝛽. 𝑓" text+ + 𝜖+ • 𝑅+ " = 𝛾, 𝑓! text- + 𝛾. 𝑓" text+ + 𝜐+

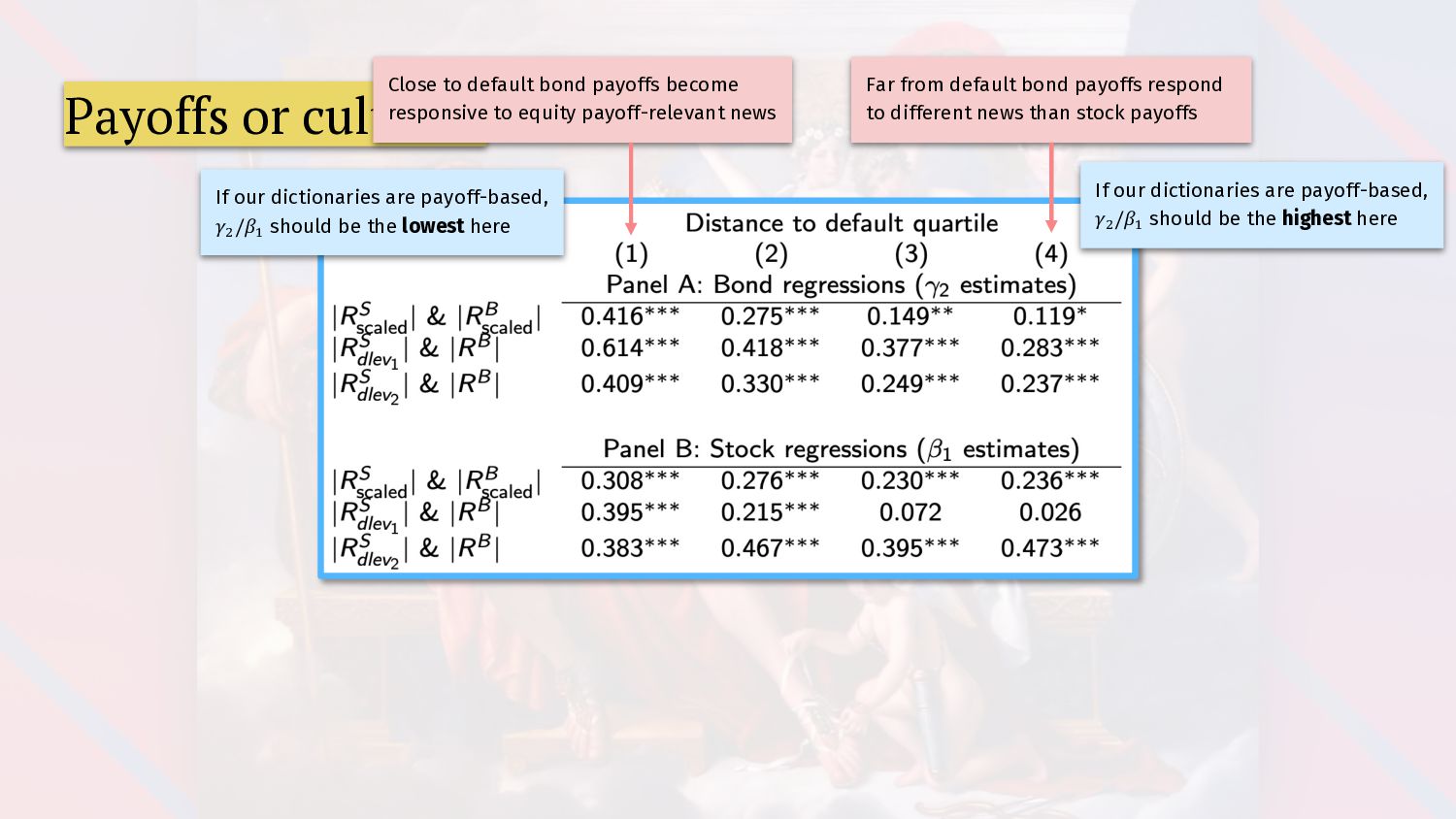

different news than stock payoffs Close to default bond payoffs become responsive to equity payoff-relevant news If our dictionaries are payoff-based, 𝛾# /𝛽$ should be the highest here If our dictionaries are payoff-based, 𝛾# /𝛽$ should be the lowest here

(closer to default) • If anything, dictionary differences are more pronounced for equity-like bonds! Far from default bond payoffs respond to different news than stock payoffs Close to default bond payoffs become responsive to equity payoff-relevant news If our dictionaries are payoff-based, 𝛾# /𝛽$ should be the highest here If our dictionaries are payoff-based, 𝛾# /𝛽$ should be the lowest here

(have more similar sensitivity to firm value) If payoffs determine dictionaries, HR Q1 𝛾# /𝛽$ should be larger than HR Q4 𝛾# /𝛽$ The evidence is opposite to what the payoff story suggests

(respond to asset volatility more similarly) If payoffs determine dictionaries, Vega Q1 𝛾# /𝛽$ should be larger than Vega Q4 𝛾# /𝛽$ The evidence is inconsistent with payoff story

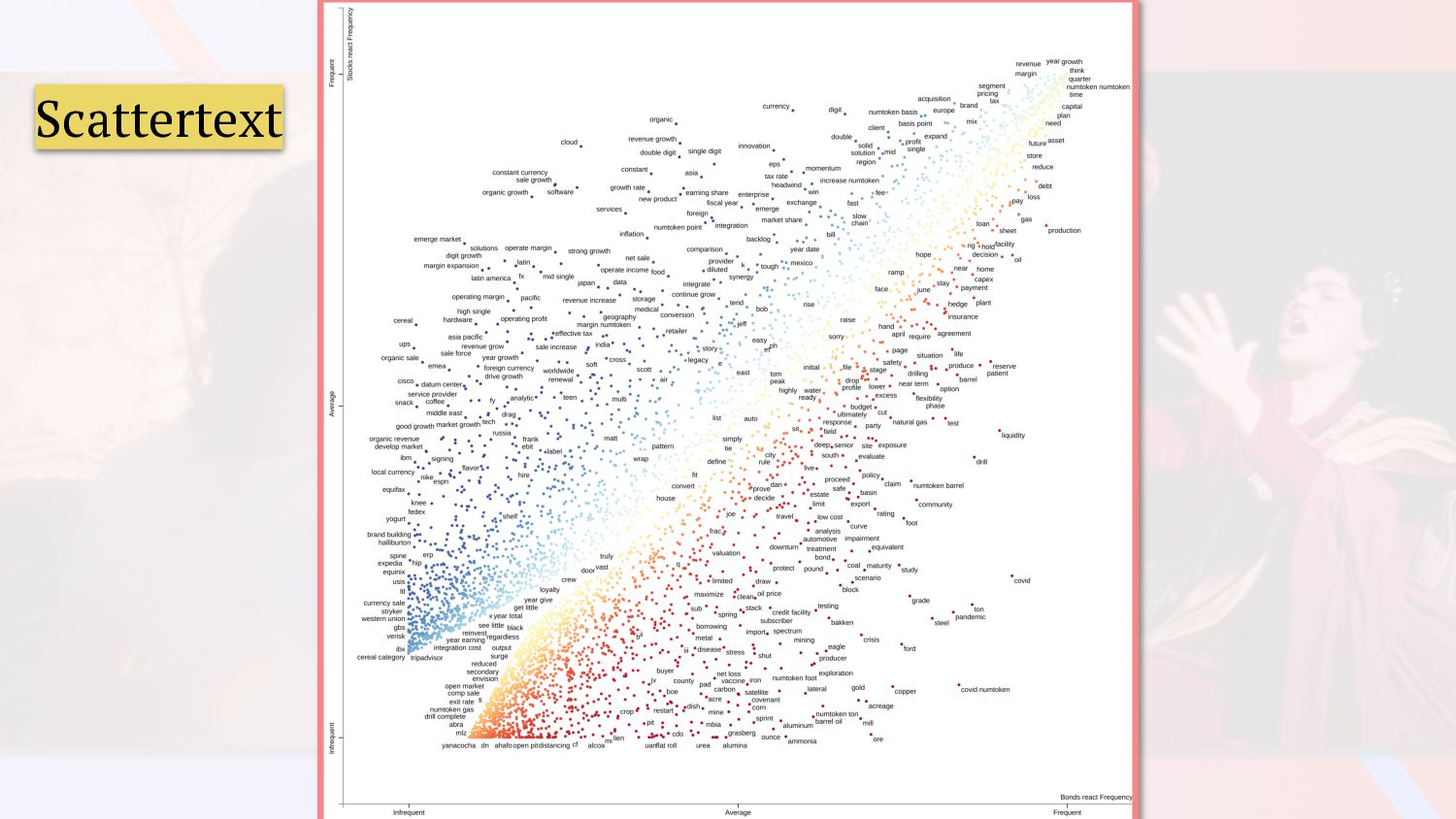

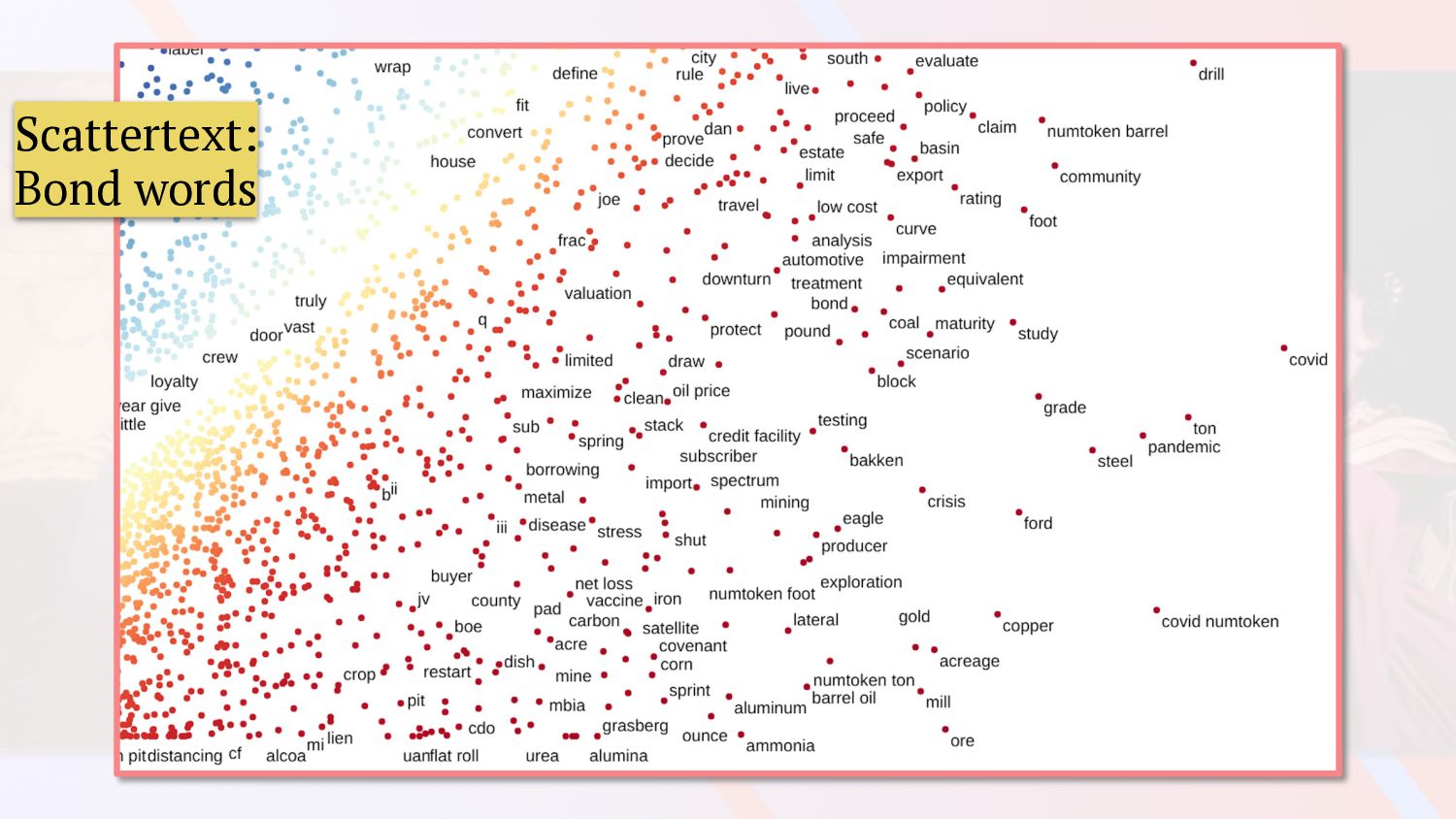

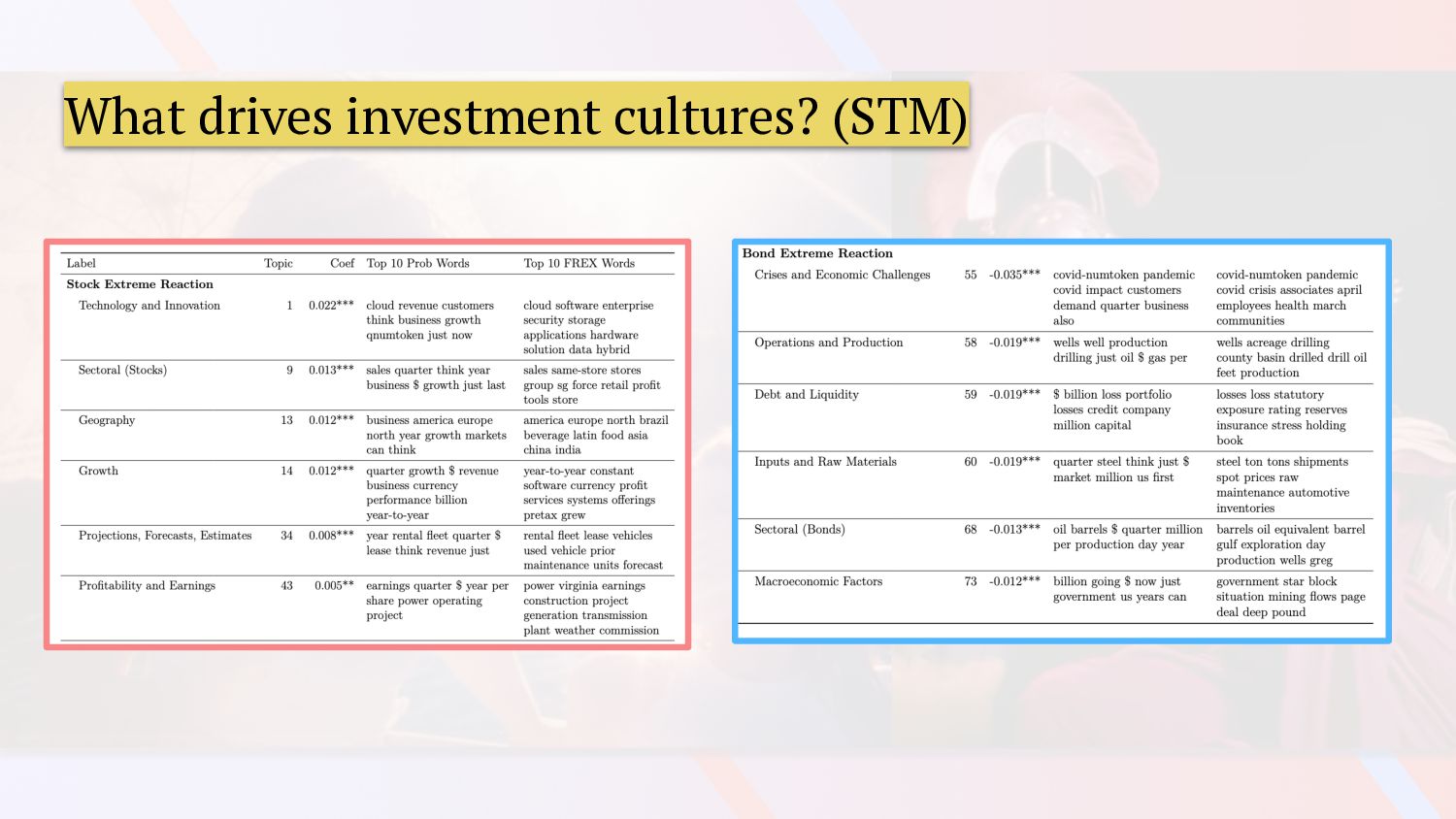

words important to bonds, but not stocks and vice-versa • Structural topic model (STM) – find topics associated with a covariate (reactions by bonds by not stocks) • LLM to summarize topics

topics (probabilities over words) from which documents are built • Structural topic modeling allows covariance of topics with ExtremeReaction ◦ Imbues analysis with opportunity for statistical inference • We identify 100 topics, alongside top words • Of 100, 82 are (statistically) significantly more related to one or the other corpus

the top 10 words for each topic • ...and which ExtremeReaction group the topic was associated with (”1” or ”2”) • ...and 10 themes (Technology and innovation, Profitability, Operations, ...) Ask LLM: What do topics represent thematically, and which themes are most important to each group? ~10,000 unique words -> 100 topics -> 10 themes

dimensions related to Growth, Technology and innovation, Profitability/margins/earnings, Projections/forecasts/estimates, and Geography more extensively.” “Group 2 [bonds] covers dimensions related to Inputs/raw materials, Operations/production, Crises/economic challenges, Debt and liquidity, Macroeconomic factors, and Sectoral topics more extensively.”

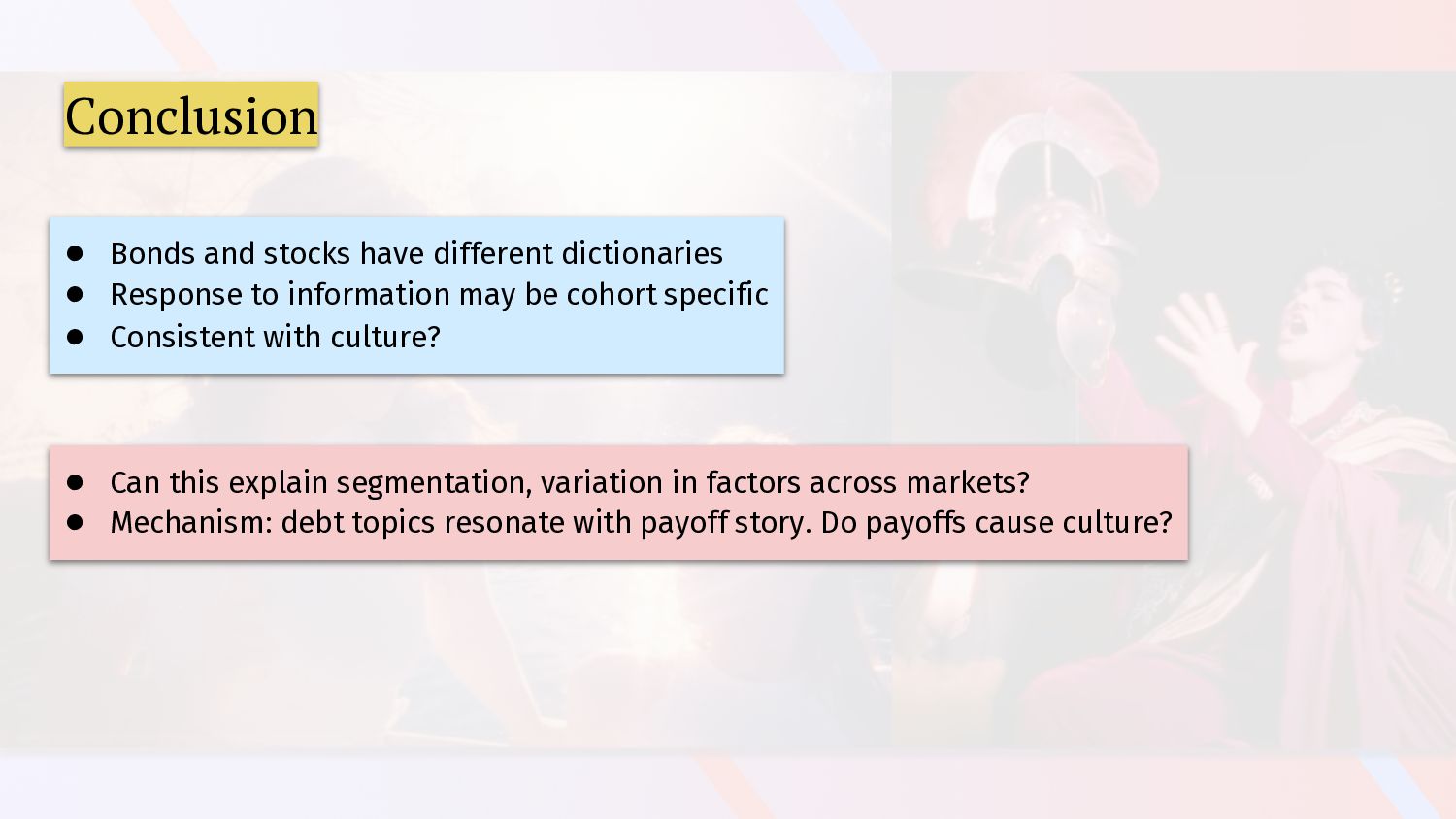

to information may be cohort specific • Consistent with culture? • Can this explain segmentation, variation in factors across markets? • Mechanism: debt topics resonate with payoff story. Do payoffs cause culture?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![What drives investment cultures? (LLM summary) “Group 1 [stocks] covers](https://files.speakerdeck.com/presentations/58abb61d08ba43068cfd32d03dec5b39/slide_42.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}