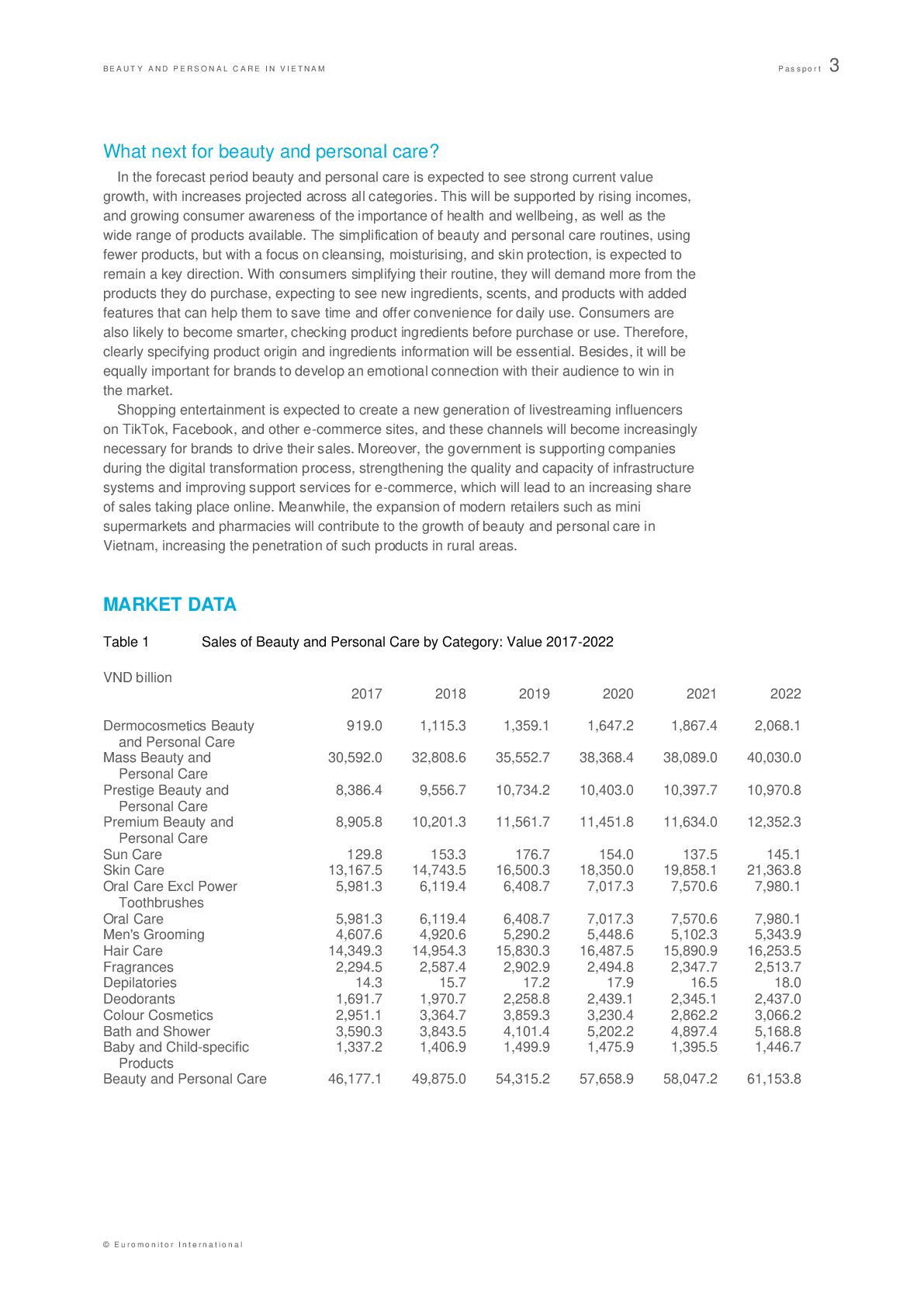

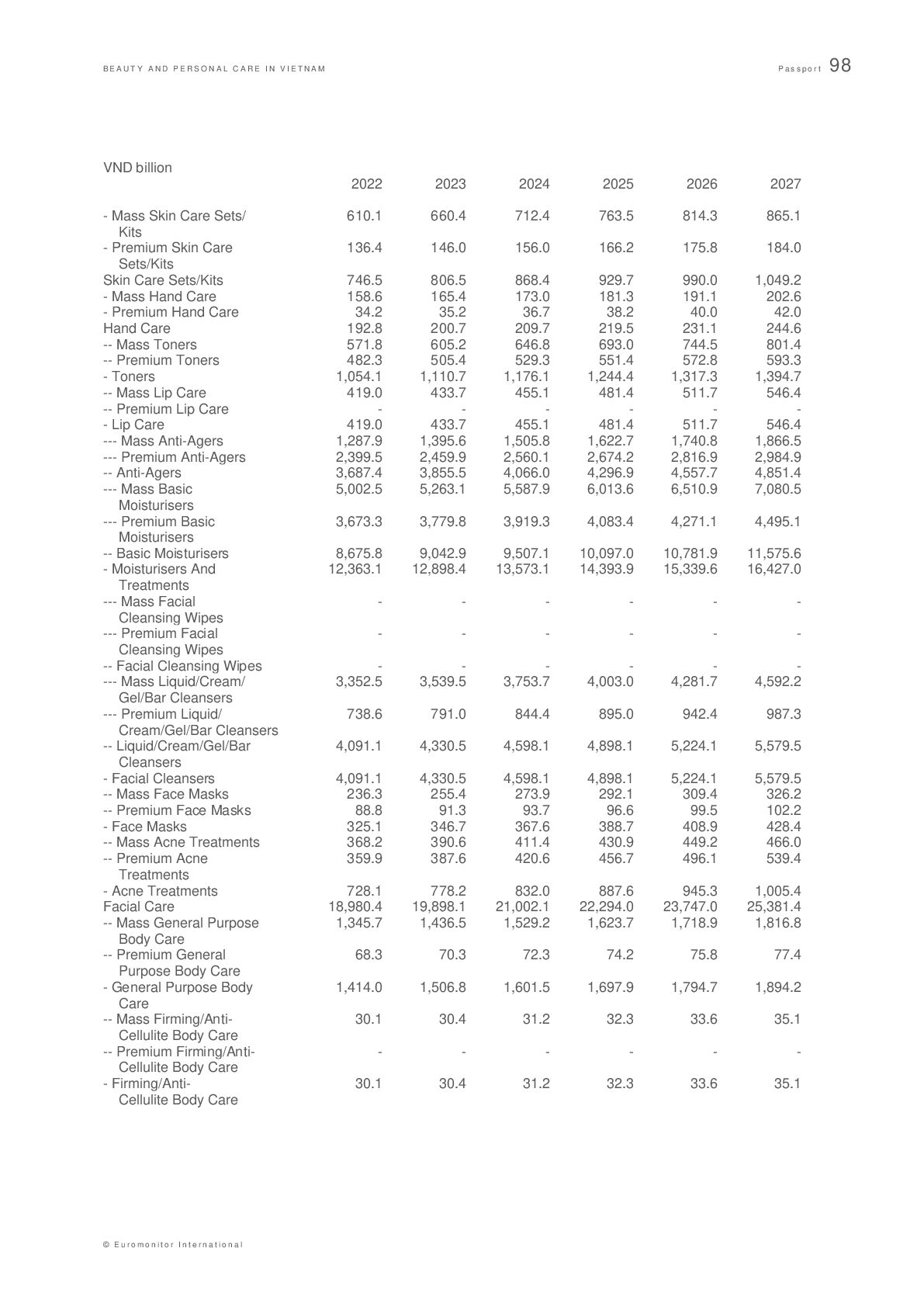

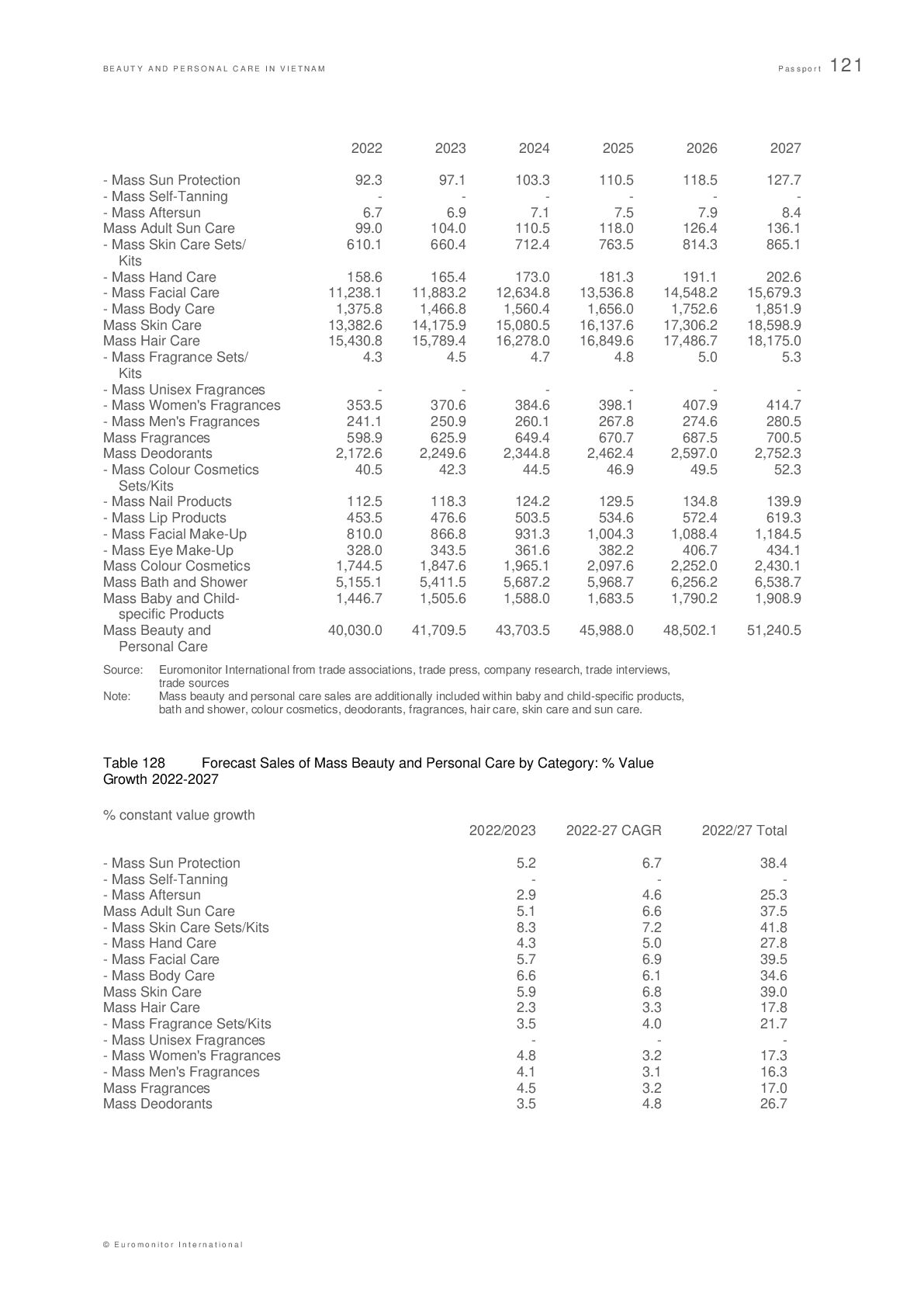

E R S O N A L C A R E I N V I E T N A M P a s s p o r t 3 © E u r o m o n i t o r I n t e r n a t i o n a l What next for beauty and personal care? In the forecast period beauty and personal care is expected to see strong current value growth, with increases projected across all categories. This will be supported by rising incomes, and growing consumer awareness of the importance of health and wellbeing, as well as the wide range of products available. The simplification of beauty and personal care routines, using fewer products, but with a focus on cleansing, moisturising, and skin protection, is expected to remain a key direction. With consumers simplifying their routine, they will demand more from the products they do purchase, expecting to see new ingredients, scents, and products with added features that can help them to save time and offer convenience for daily use. Consumers are also likely to become smarter, checking product ingredients before purchase or use. Therefore, clearly specifying product origin and ingredients information will be essential. Besides, it will be equally important for brands to develop an emotional connection with their audience to win in the market. Shopping entertainment is expected to create a new generation of livestreaming influencers on TikTok, Facebook, and other e-commerce sites, and these channels will become increasingly necessary for brands to drive their sales. Moreover, the government is supporting companies during the digital transformation process, strengthening the quality and capacity of infrastructure systems and improving support services for e-commerce, which will lead to an increasing share of sales taking place online. Meanwhile, the expansion of modern retailers such as mini supermarkets and pharmacies will contribute to the growth of beauty and personal care in Vietnam, increasing the penetration of such products in rural areas. MARKET DATA Table 1 Sales of Beauty and Personal Care by Category: Value 2017-2022 VND billion 2017 2018 2019 2020 2021 2022 Dermocosmetics Beauty 919.0 1,115.3 1,359.1 1,647.2 1,867.4 2,068.1 and Personal Care Mass Beauty and 30,592.0 32,808.6 35,552.7 38,368.4 38,089.0 40,030.0 Personal Care Prestige Beauty and 8,386.4 9,556.7 10,734.2 10,403.0 10,397.7 10,970.8 Personal Care Premium Beauty and 8,905.8 10,201.3 11,561.7 11,451.8 11,634.0 12,352.3 Personal Care Sun Care 129.8 153.3 176.7 154.0 137.5 145.1 Skin Care 13,167.5 14,743.5 16,500.3 18,350.0 19,858.1 21,363.8 Oral Care Excl Power 5,981.3 6,119.4 6,408.7 7,017.3 7,570.6 7,980.1 Toothbrushes Oral Care 5,981.3 6,119.4 6,408.7 7,017.3 7,570.6 7,980.1 Men's Grooming 4,607.6 4,920.6 5,290.2 5,448.6 5,102.3 5,343.9 Hair Care 14,349.3 14,954.3 15,830.3 16,487.5 15,890.9 16,253.5 Fragrances 2,294.5 2,587.4 2,902.9 2,494.8 2,347.7 2,513.7 Depilatories 14.3 15.7 17.2 17.9 16.5 18.0 Deodorants 1,691.7 1,970.7 2,258.8 2,439.1 2,345.1 2,437.0 Colour Cosmetics 2,951.1 3,364.7 3,859.3 3,230.4 2,862.2 3,066.2 Bath and Shower 3,590.3 3,843.5 4,101.4 5,202.2 4,897.4 5,168.8 Baby and Child-specific 1,337.2 1,406.9 1,499.9 1,475.9 1,395.5 1,446.7 Products Beauty and Personal Care 46,177.1 49,875.0 54,315.2 57,658.9 58,047.2 61,153.8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}