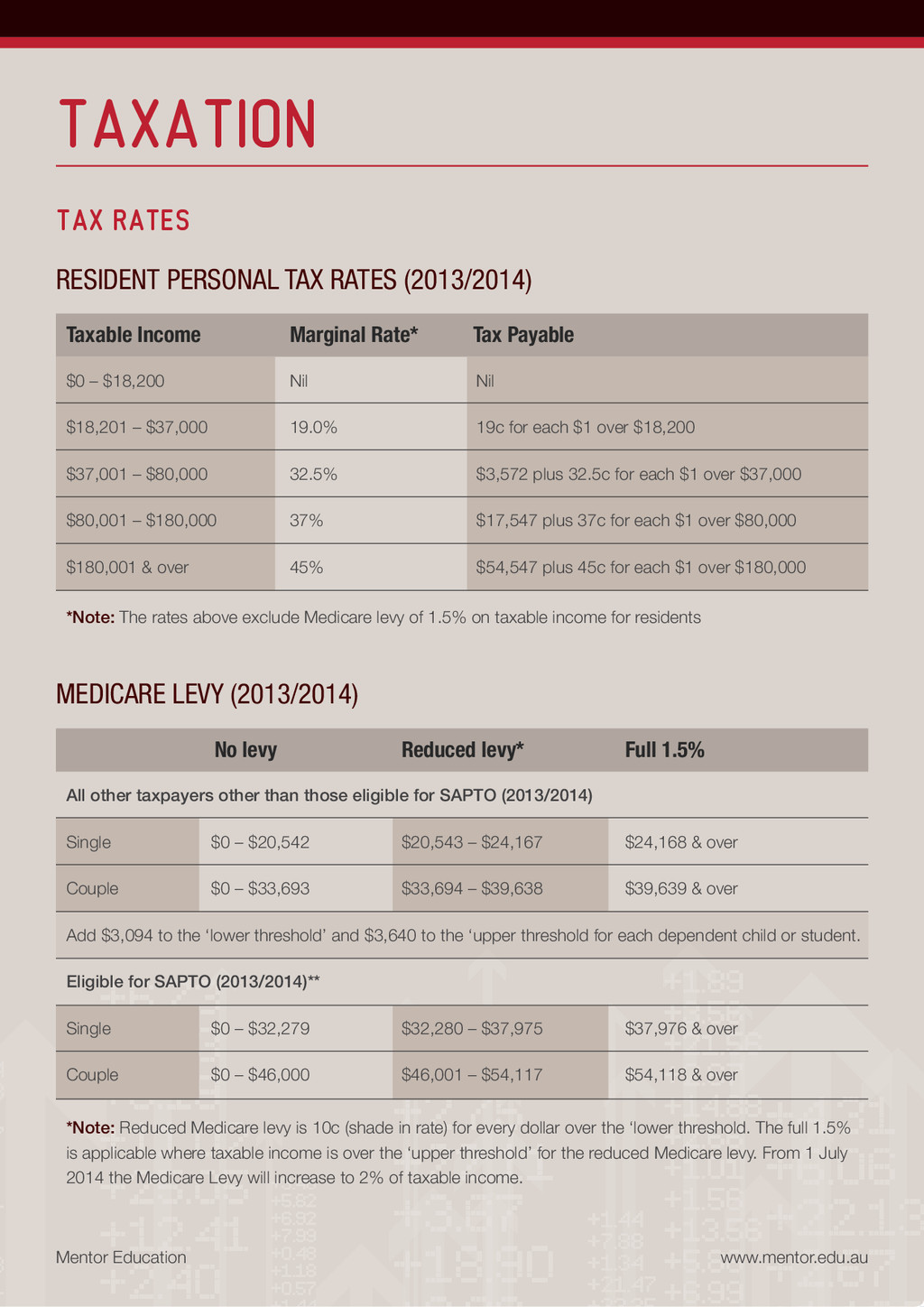

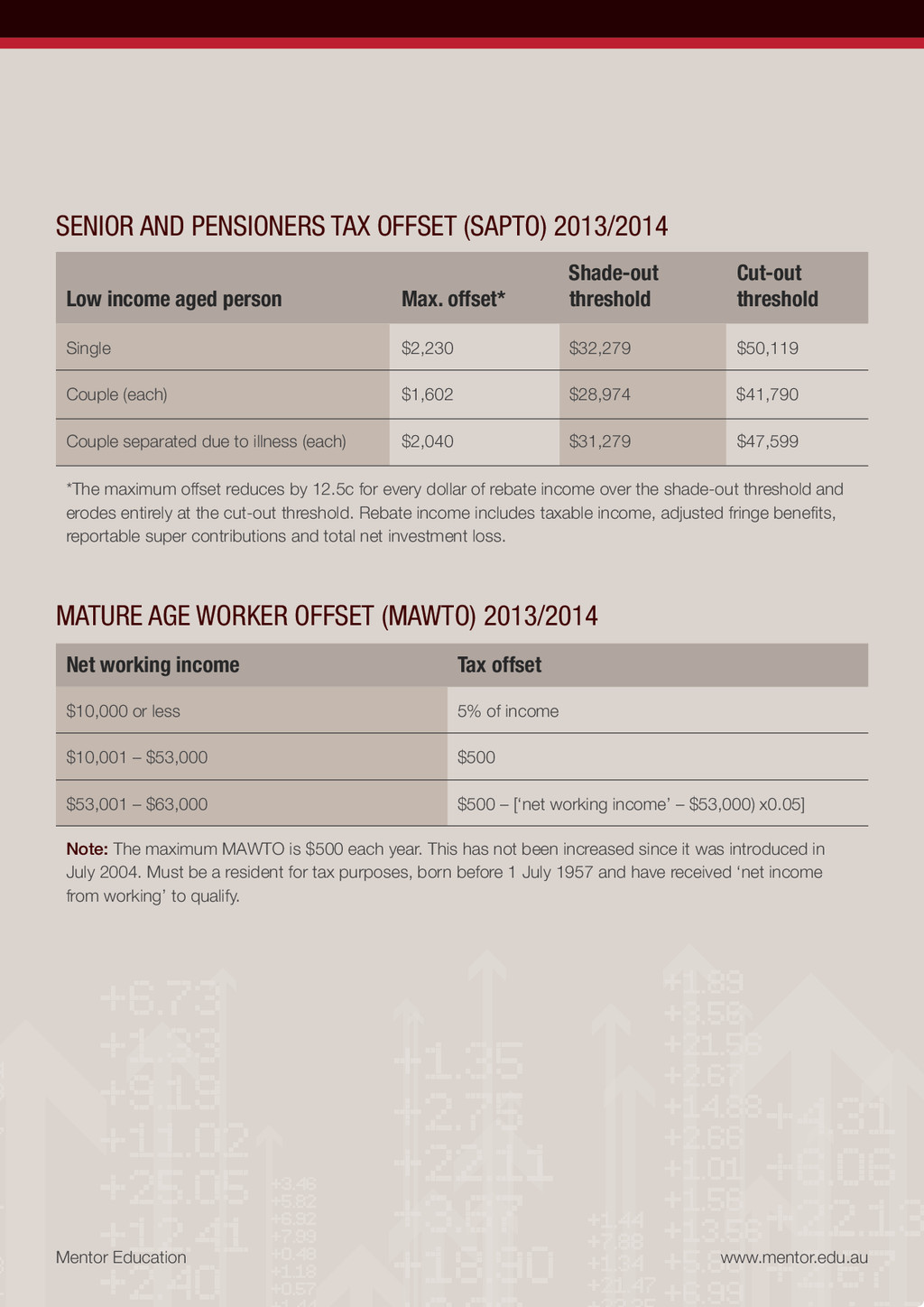

(2013/2014) Taxable Income Marginal Rate* Tax Payable No levy Reduced levy* Full 1.5% $0 – $18,200 Nil Nil $18,201 – $37,000 19.0% 19c for each $1 over $18,200 $37,001 – $80,000 32.5% $3,572 plus 32.5c for each $1 over $37,000 $80,001 – $180,000 37% $17,547 plus 37c for each $1 over $80,000 $180,001 & over 45% $54,547 plus 45c for each $1 over $180,000 All other taxpayers other than those eligible for SAPTO (2013/2014) Single $0 – $20,542 $20,543 – $24,167 $24,168 & over Couple $0 – $33,693 $33,694 – $39,638 $39,639 & over Add $3,094 to the ‘lower threshold’ and $3,640 to the ‘upper threshold for each dependent child or student. Eligible for SAPTO (2013/2014)** Single $0 – $32,279 $32,280 – $37,975 $37,976 & over Couple $0 – $46,000 $46,001 – $54,117 $54,118 & over *Note: The rates above exclude Medicare levy of 1.5% on taxable income for residents *Note: Reduced Medicare levy is 10c (shade in rate) for every dollar over the ‘lower threshold. The full 1.5% is applicable where taxable income is over the ‘upper threshold’ for the reduced Medicare levy. From 1 July 2014 the Medicare Levy will increase to 2% of taxable income. Mentor Education www.mentor.edu.au

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}