– No transparency – Lack of community • Excel, Matlab, etc – Transaction costs – Availability of stock (do we find buyers/sellers?) – Market impact of own orders

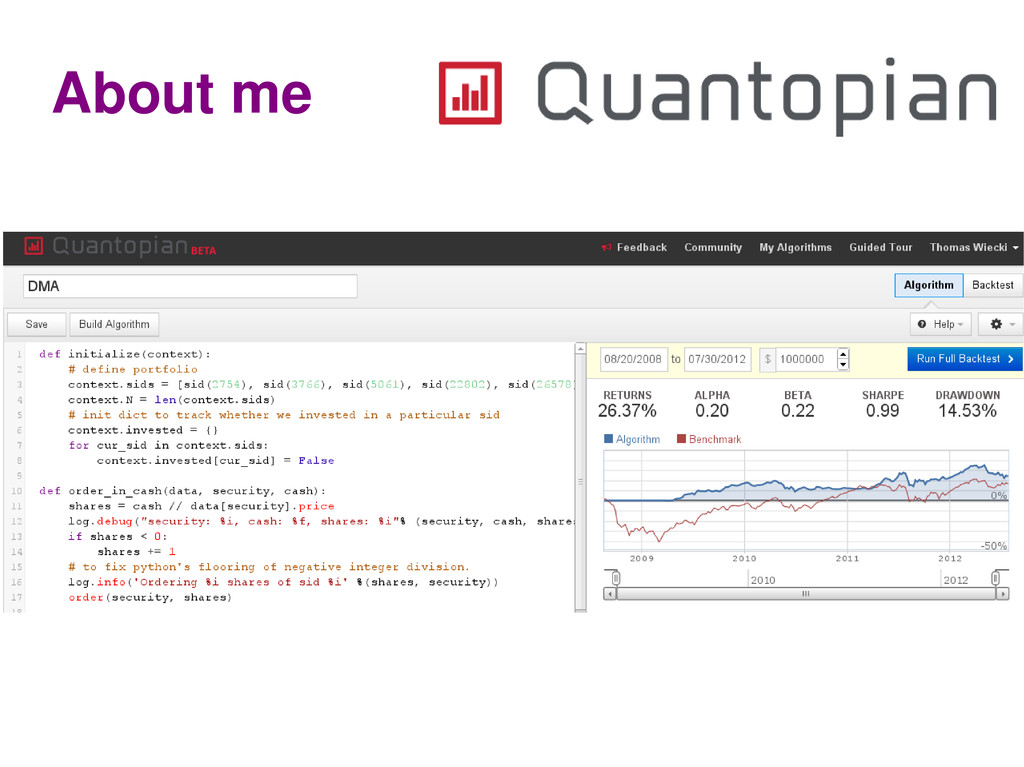

Event-driven • Batteries included – Moving average, Sharpe, alpha, beta... • Used in production on Quantopian.com – Contribute back to community – Linus' law: "given enough eyeballs, all bugs are shallow" • http://github.com/quantopian/zipline

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}