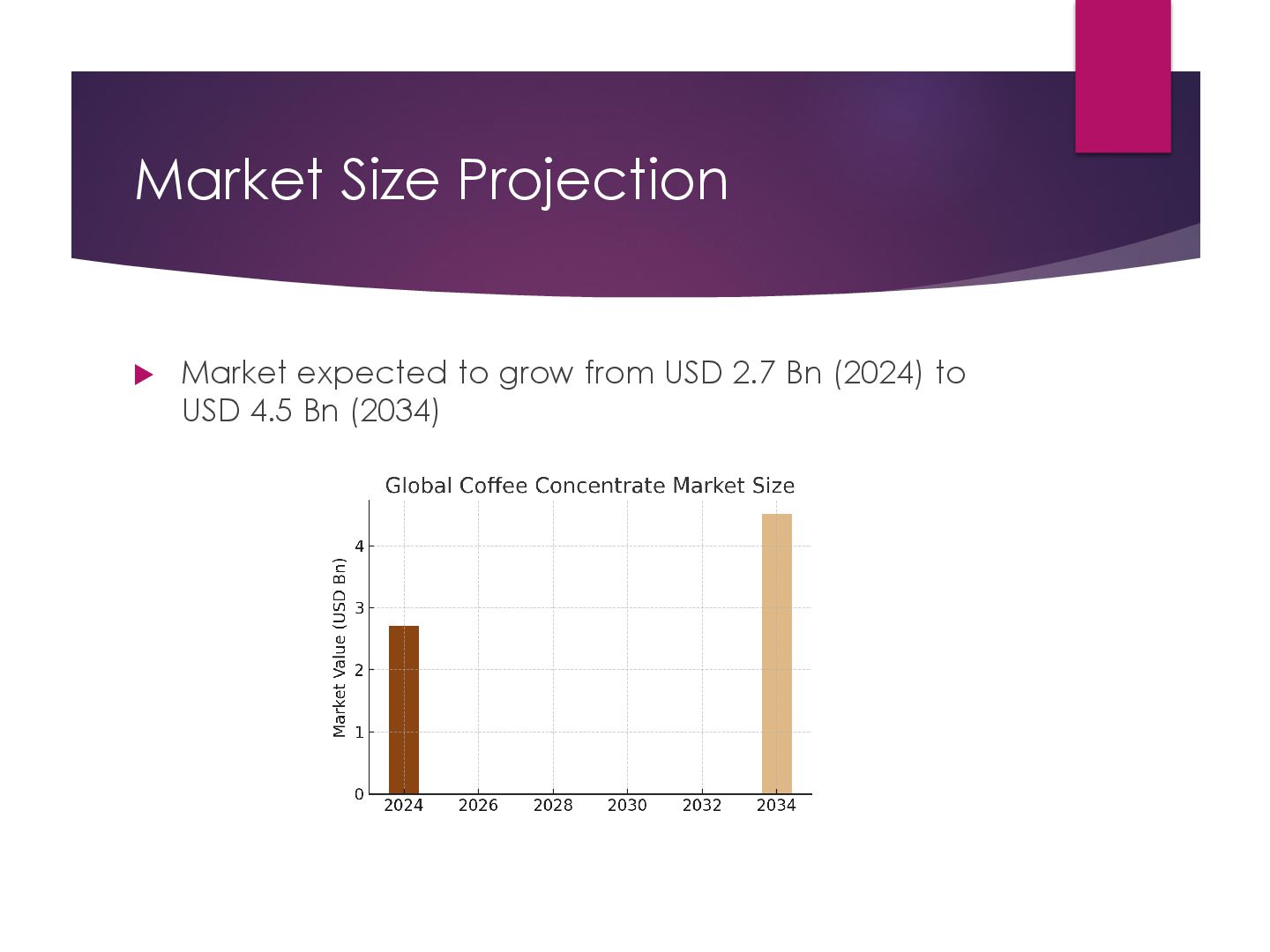

In 2024, the global coffee concentrate market is valued at approximately USD 2.7 billion, and projections indicate it will climb to USD 4.5 billion by 2034, sustaining a compound annual growth rate of 5.4% from 2025 to 2034.A remarkable highlight is the preeminence of caffeinated concentrates, accounting for 86.4% of global sales in 2024, underscoring consumer preference for traditional, high-energy coffee options.

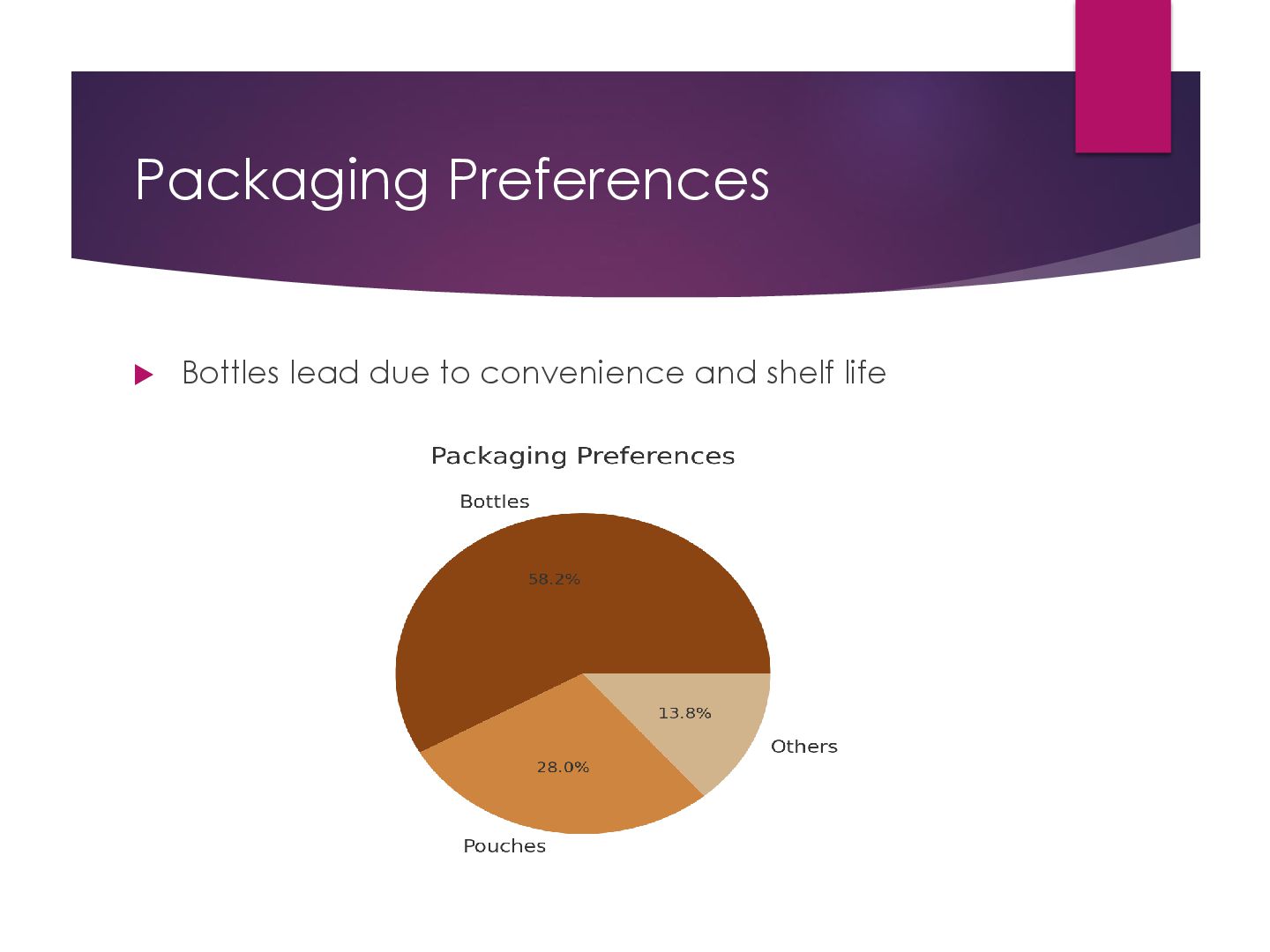

Delving into production sources, Arabica beans dominate with a 63.3% share, favored for their smooth flavor and quality profile.Among packaging formats, bottles lead with 58.2% of the market, reflecting consumer demand for freshness, portability, and premium presentation.

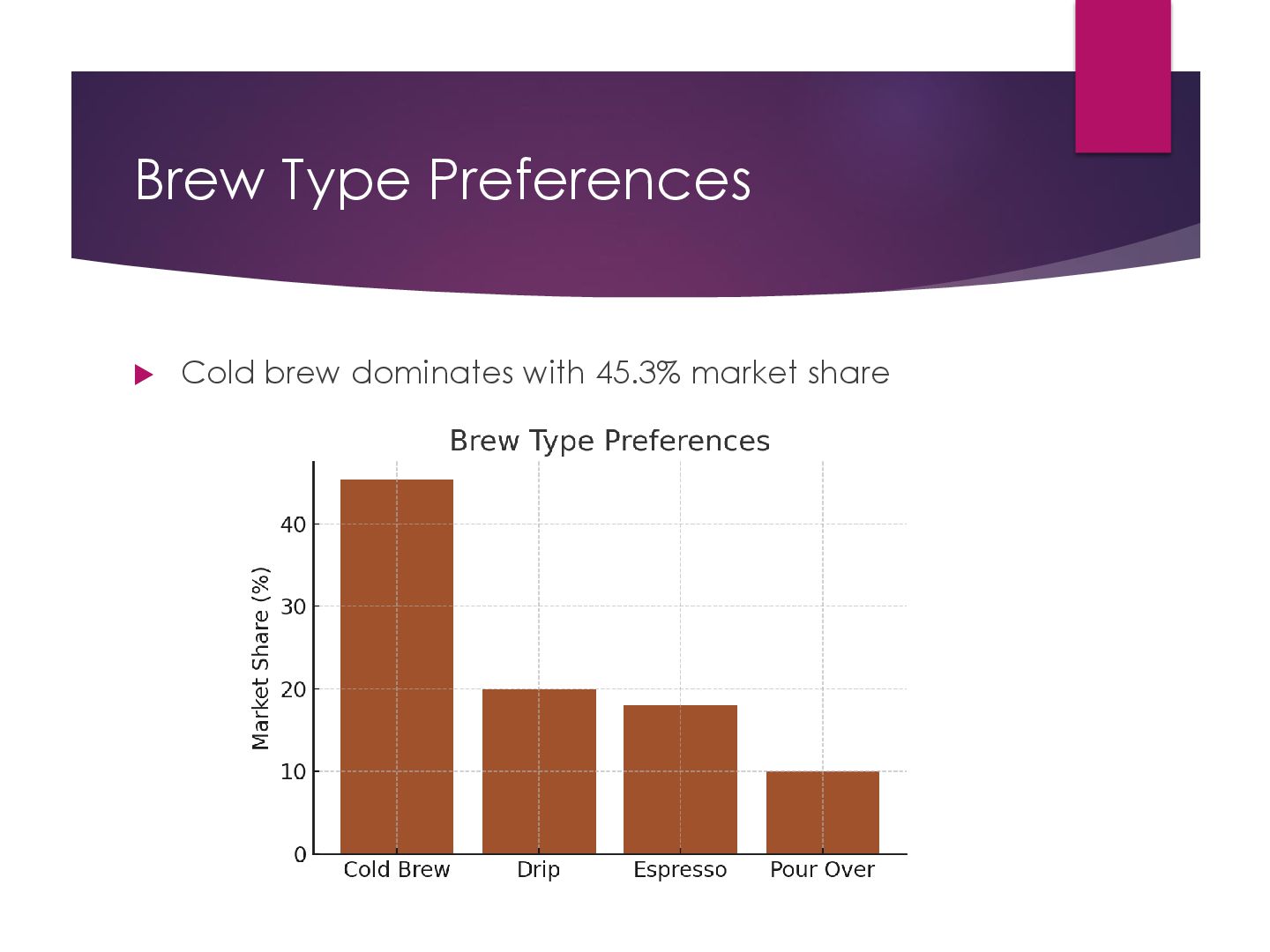

Analyzing consumption styles, cold brew concentrates claim 45.3% of the market in 2024, reflecting the growing global trend toward chilled, low-acid coffee beverages.Equally, original flavor captures 61.2% of sales, suggesting a strong preference for classic, unflavored coffee experience .

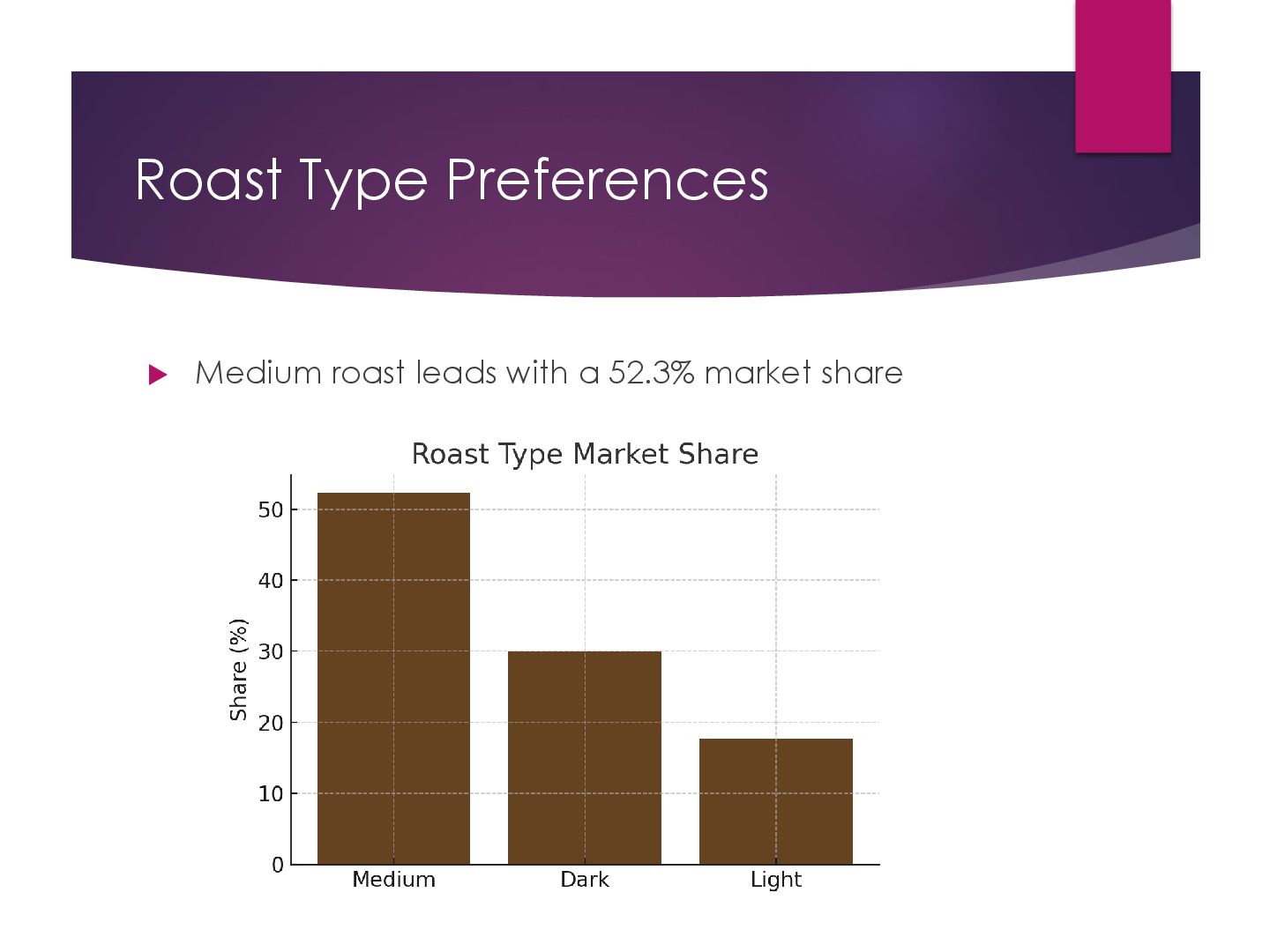

In terms of roast preference, medium roast leads the pack with 52.3% of sales, appealing to a broad audience seeking balance between sweetness and bitterness.Distribution channels show the HoReCa sector (hotels, restaurants, and cafés) dominating with 63.4% of market realisation, driven by efficiency and demand in commercial settings.

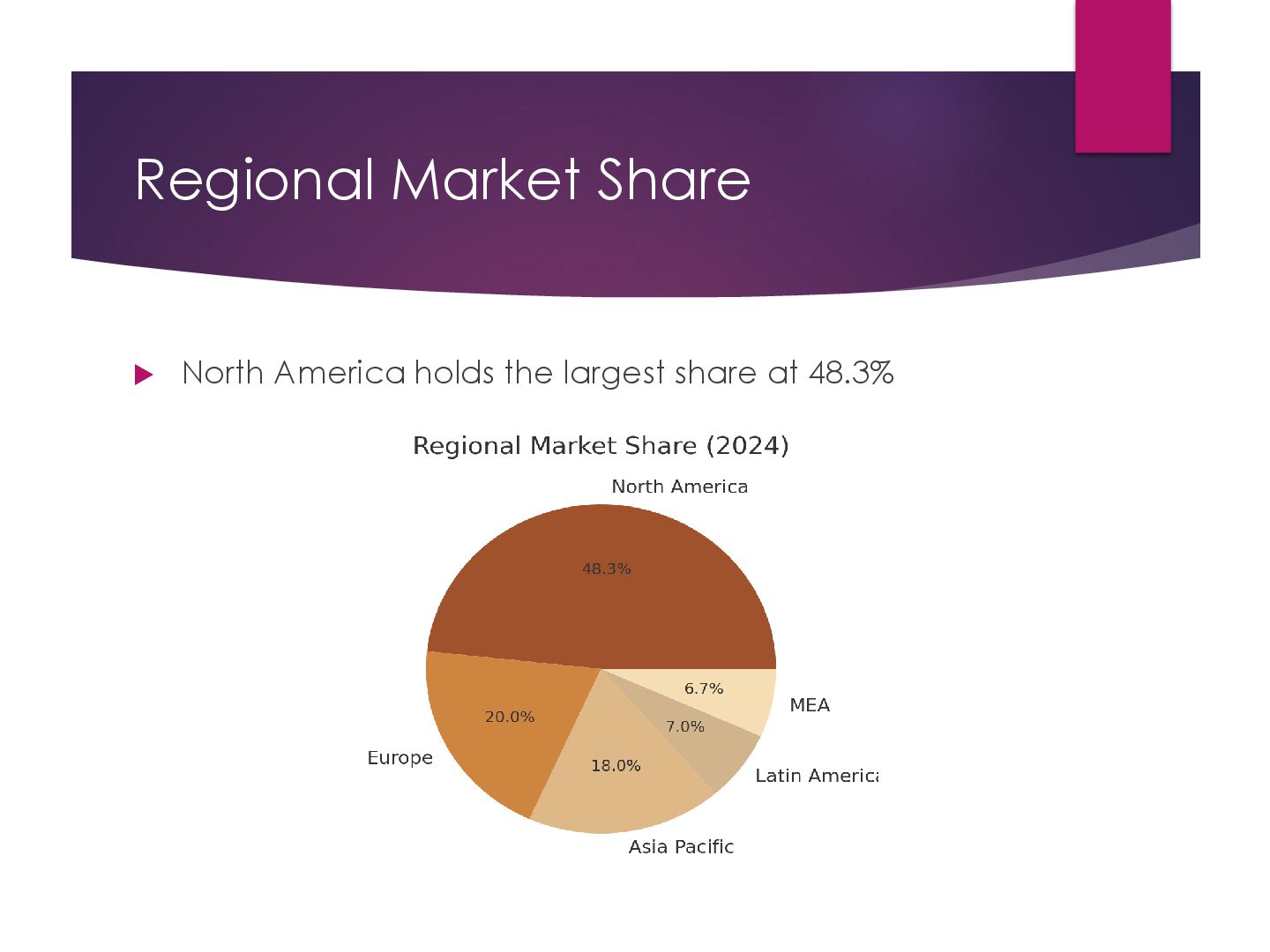

Regionally, North America holds nearly 48.3% of the global market, corresponding to about USD 1.2 billion a clear indicator of strong regional demand and developed infrastructure

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}