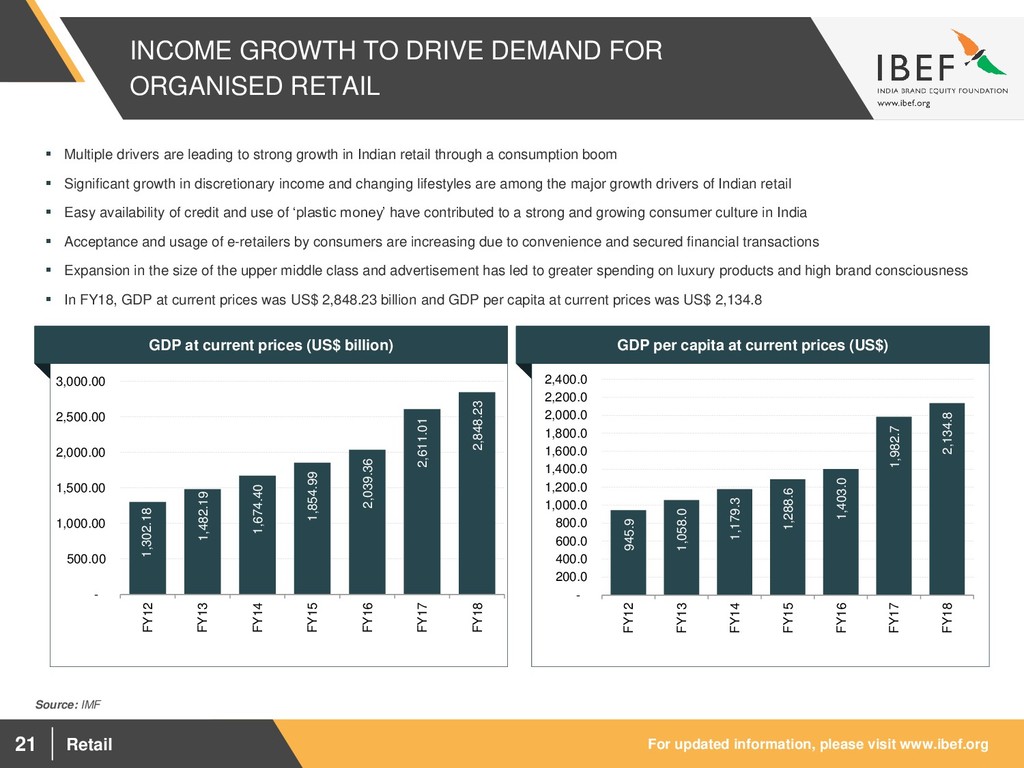

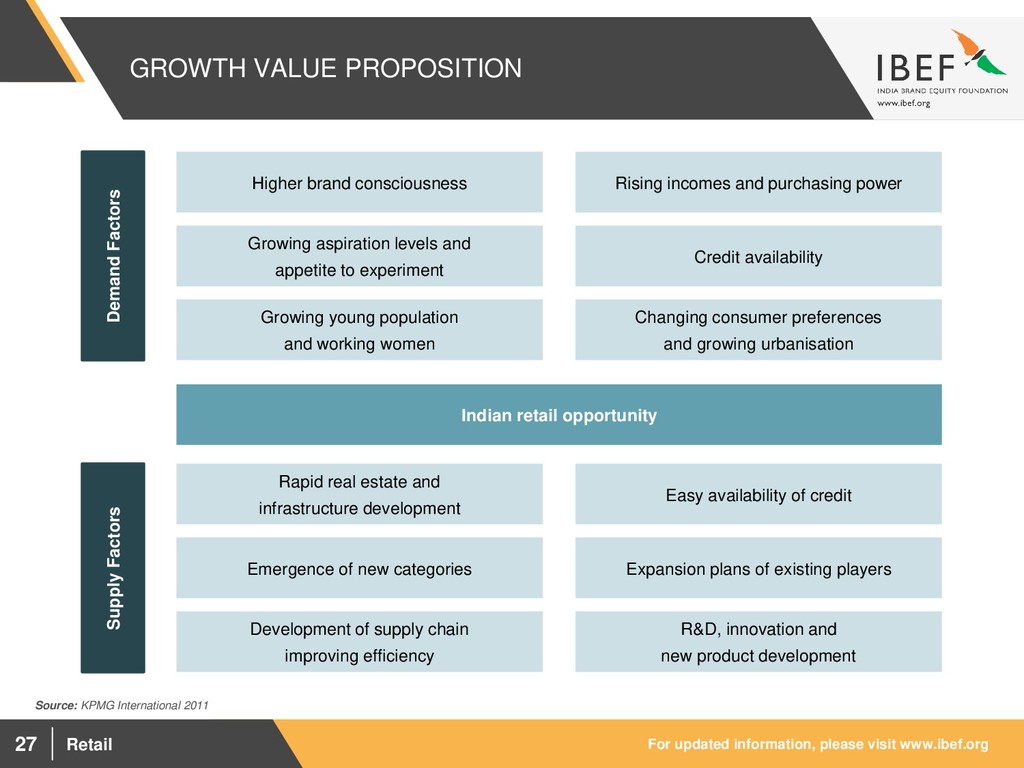

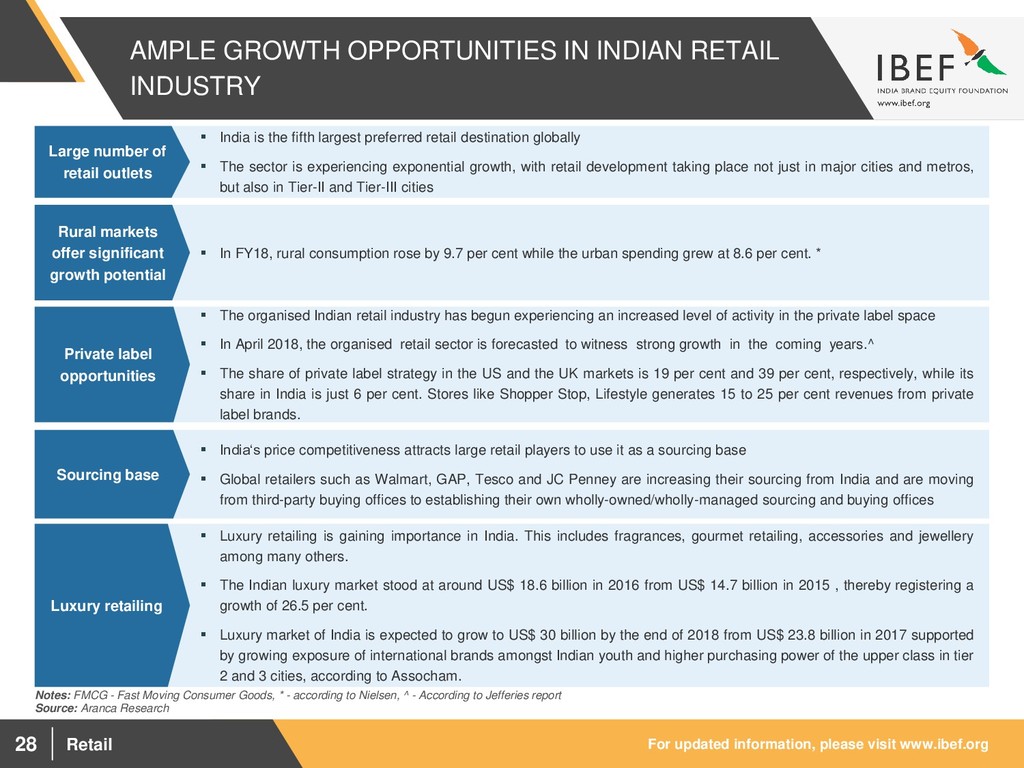

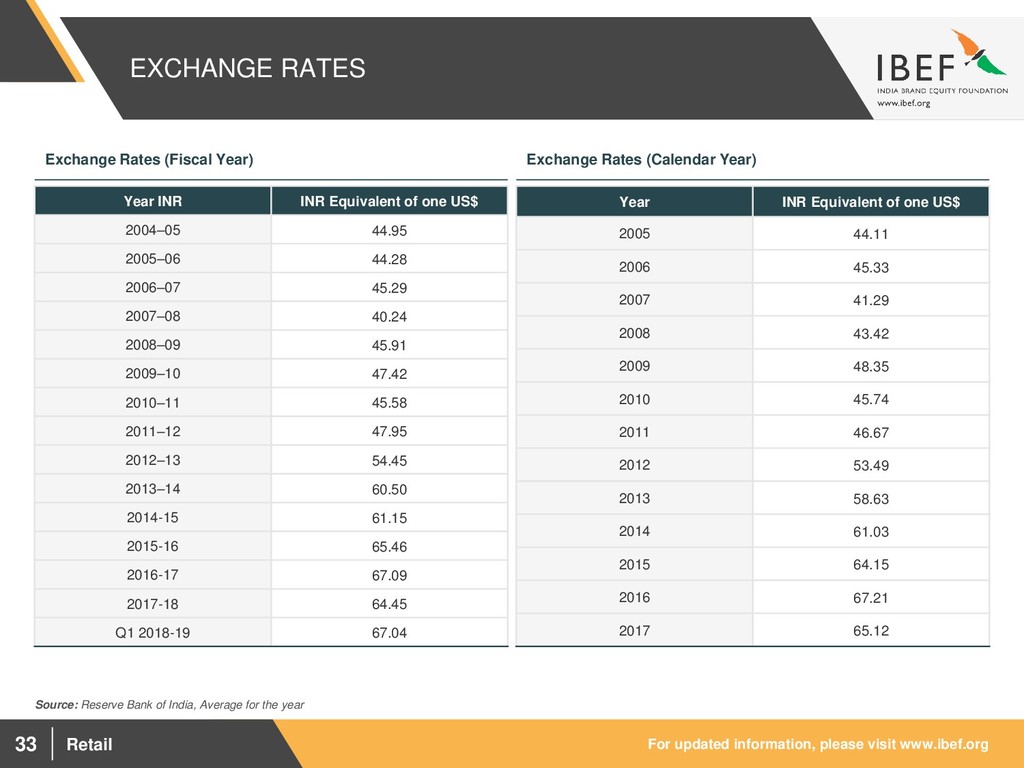

1,674.40 1,854.99 2,039.36 2,611.01 2,848.23 - 500.00 1,000.00 1,500.00 2,000.00 2,500.00 3,000.00 FY12 FY13 FY14 FY15 FY16 FY17 FY18 945.9 1,058.0 1,179.3 1,288.6 1,403.0 1,982.7 2,134.8 - 200.0 400.0 600.0 800.0 1,000.0 1,200.0 1,400.0 1,600.0 1,800.0 2,000.0 2,200.0 2,400.0 FY12 FY13 FY14 FY15 FY16 FY17 FY18 INCOME GROWTH TO DRIVE DEMAND FOR ORGANISED RETAIL Source: IMF Visakhapatnam port traffic (million tonnes) GDP at current prices (US$ billion) Visakhapatnam port traffic (million tonnes) GDP per capita at current prices (US$) Multiple drivers are leading to strong growth in Indian retail through a consumption boom Significant growth in discretionary income and changing lifestyles are among the major growth drivers of Indian retail Easy availability of credit and use of ‘plastic money’ have contributed to a strong and growing consumer culture in India Acceptance and usage of e-retailers by consumers are increasing due to convenience and secured financial transactions Expansion in the size of the upper middle class and advertisement has led to greater spending on luxury products and high brand consciousness In FY18, GDP at current prices was US$ 2,848.23 billion and GDP per capita at current prices was US$ 2,134.8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}