The global digital twin market is expected to grow significantly, projected to reach nearly USD 522.9 billion by 2033, advancing at a compelling CAGR of 46.1% from 2024 to 2033. This accelerated growth is being driven by increasing demand for virtual modeling, real-time monitoring, and predictive analytics across key industrial sectors.

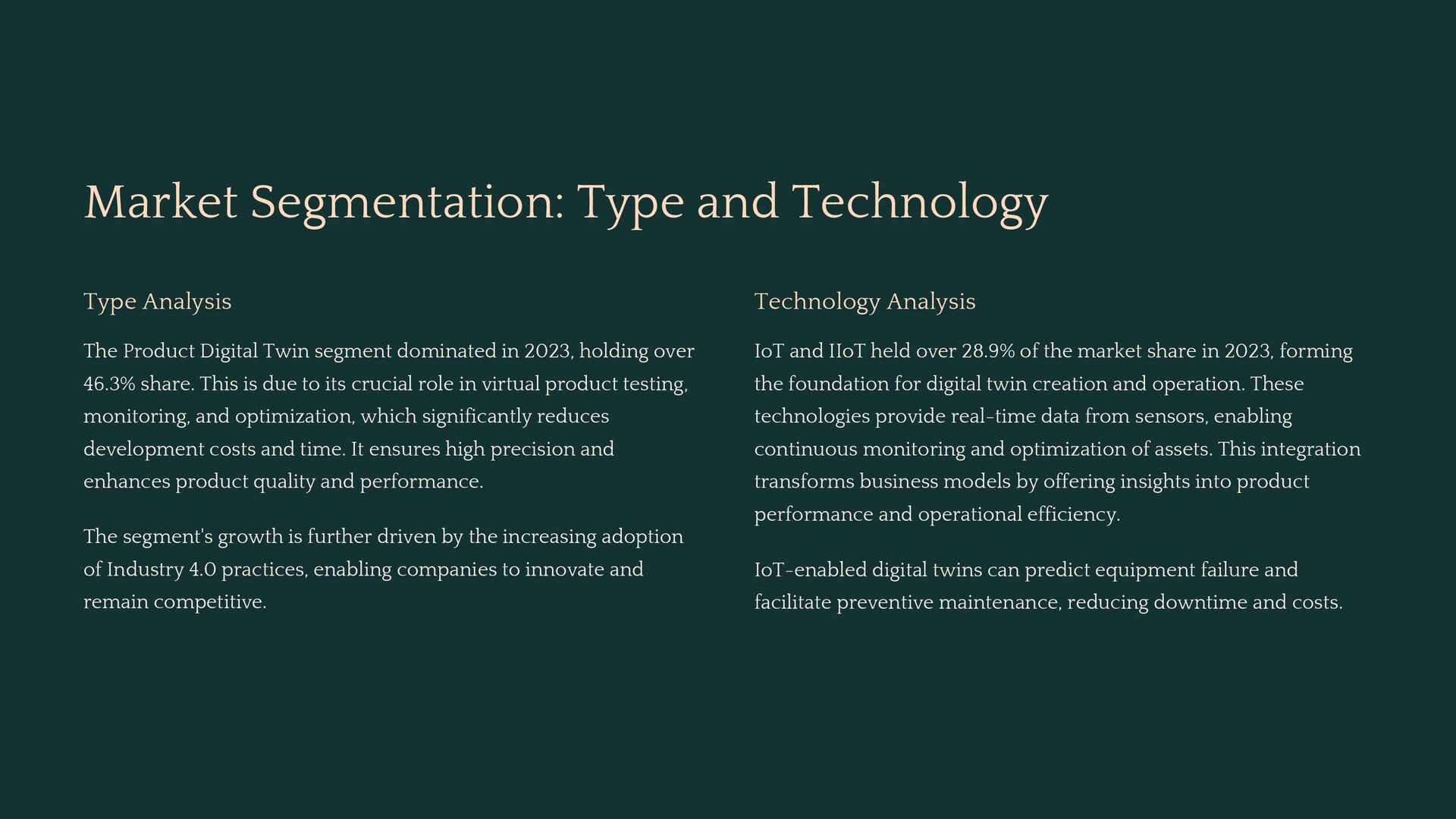

By type, the Product Digital Twin segment emerged as the dominant category in 2023, accounting for a revenue share of 46.3%. Its leadership is attributed to its critical function in product design, simulation, and lifecycle optimization—particularly in sectors where prototype testing is costly or time-sensitive.

In terms of technology, IoT and IIoT played a foundational role, holding a 28.9% share in 2023. These technologies enable seamless data flow from physical assets to their digital replicas, supporting real-time synchronization and advanced analytics that are vital for the operation of digital twin ecosystems.

From an end-user perspective, Automotive & Transportation industries led adoption, representing 22.0% of the market share in 2023. These sectors have embraced digital twins to enhance vehicle design, reduce time-to-market, and improve operational safety through simulation-based testing and monitoring.

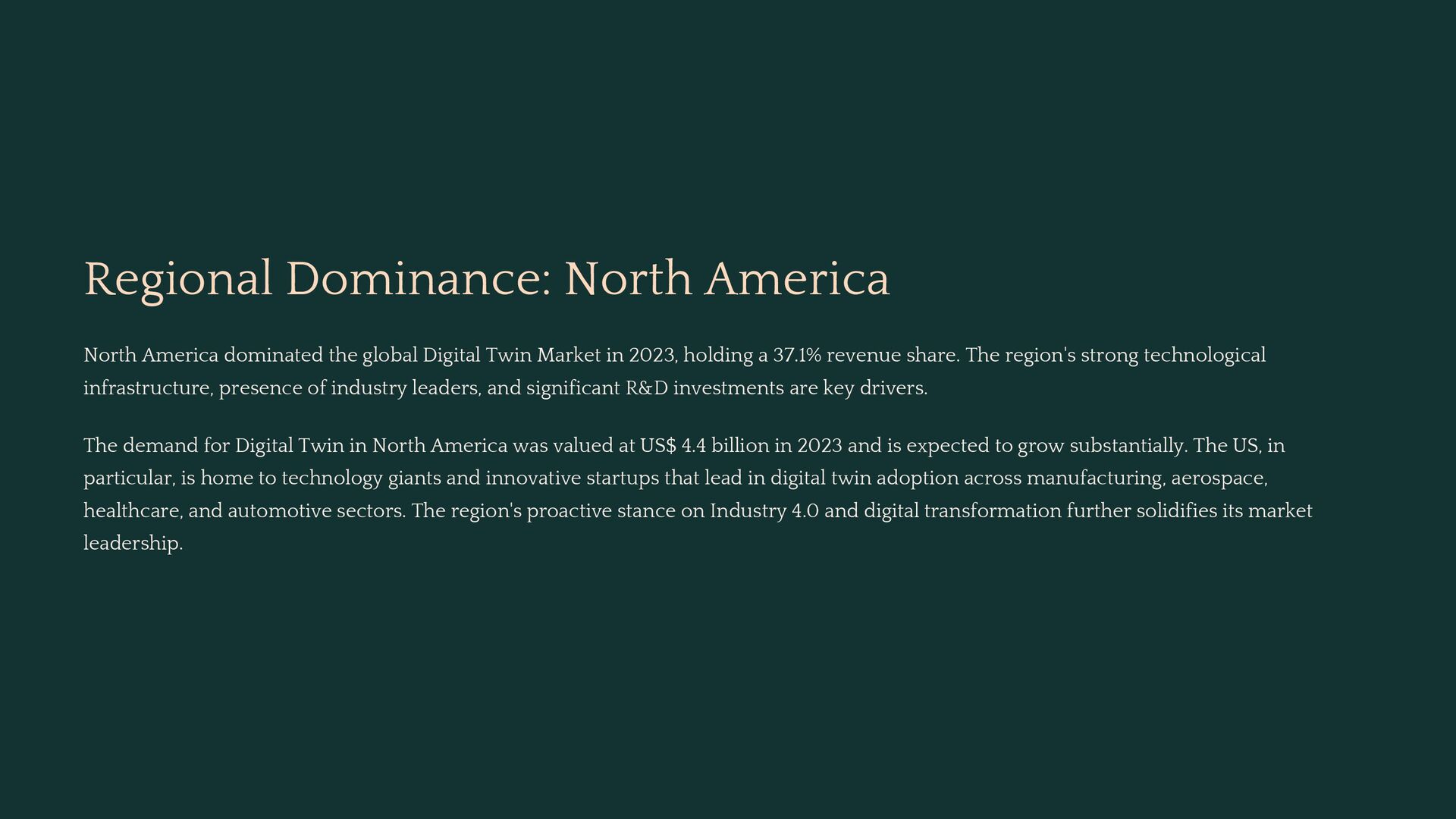

Geographically, North America retained a dominant position in 2023, with a market share of 37.1%. This regional strength is underpinned by its advanced digital infrastructure, early technology integration, and a concentration of leading players actively investing in smart manufacturing and digital transformation initiatives.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}