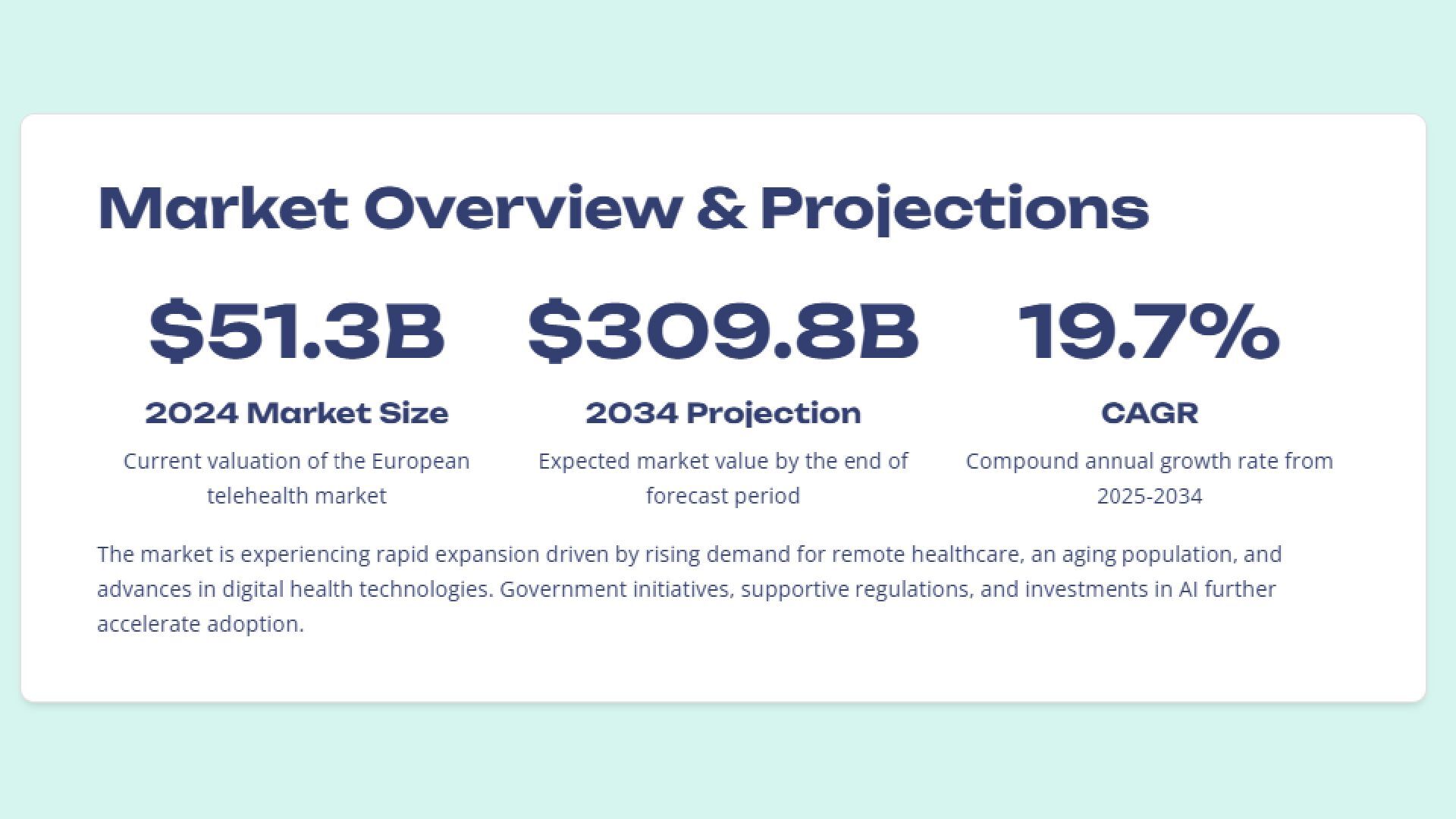

The Europe Telehealth Market is projected to grow significantly, reaching approximately USD 309.8 billion by 2034, up from USD 51.3 billion in 2024. This expansion reflects a strong CAGR of 19.7% from 2025 to 2034. The growth is supported by the increasing demand for remote healthcare services, improved internet connectivity, and favorable regulatory policies. The shift toward digital healthcare is expected to continue as aging populations and chronic disease prevalence drive the adoption of virtual care across the region’s healthcare systems.

Based on service type, Teleconsultation is anticipated to hold the largest market share at 40.8%. This dominance is due to the wide acceptance of virtual doctor-patient interactions in both primary and specialist care. Other segments include Remote Patient Monitoring (RPM), Store-and-Forward, Mobile Health Applications, and Tele-ICU services. Teleconsultation is particularly beneficial for timely access to healthcare, reducing wait times, and expanding coverage in remote areas. The COVID-19 pandemic has also accelerated the usage of virtual consultations across Europe.

The deployment mode segment shows a clear preference for Cloud-Based solutions, which command a 65.9% share of the market. Cloud-based platforms support scalability, enhanced accessibility, and secure storage, making them ideal for remote access and data integration. These platforms enable healthcare professionals to deliver services from multiple locations. In contrast, On-Premises deployment offers limited flexibility. As telehealth services continue to evolve, the shift toward cloud-based systems is expected to strengthen due to cost-efficiency and ease of maintenance.

Telepsychiatry leads the distribution channel segment with a 27.5% share, driven by increased mental health awareness and shortages in mental health professionals. Other key segments include Teleradiology, Teledermatology, Teleneurology, and others. The rise in anxiety, depression, and related disorders post-pandemic has significantly boosted telepsychiatry demand. Patients increasingly prefer remote consultations for psychological support, which reduces stigma and enhances access. These trends are expected to continue supporting growth in this segment throughout the forecast period.

Among end users, healthcare providers dominate the market with a 46.2% share. Hospitals, clinics, and individual practitioners are key users of telehealth technologies to extend their services. Patients, payers, and other stakeholders are also adopting these tools, but providers lead in deployment scale and frequency. Regionally, Germany leads the market due to digital health initiatives. France, the UK, Spain, Italy, and the Netherlands also show strong adoption. Each country focuses on different priorities, such as rural access, elderly care, or mental health integration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}