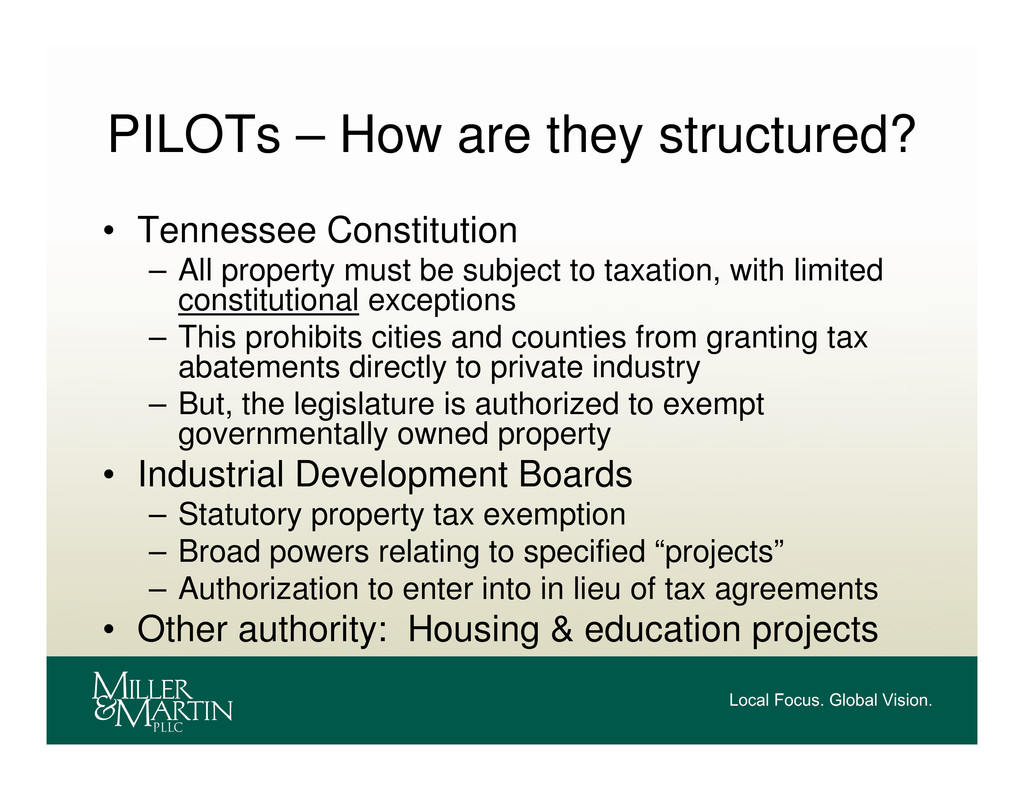

All property must be subject to taxation, with limited constitutional exceptions – This prohibits cities and counties from granting tax abatements directly to private industry – But, the legislature is authorized to exempt governmentally owned property • Industrial Development Boards – Statutory property tax exemption – Broad powers relating to specified “projects” – Authorization to enter into in lieu of tax agreements • Other authority: Housing & education projects

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Questions? Alfred E. Smith, Jr. 423-785-8223 | [email protected] Mark W.](https://files.speakerdeck.com/presentations/508592dd81c995000200baab/slide_21.jpg){kind=link}