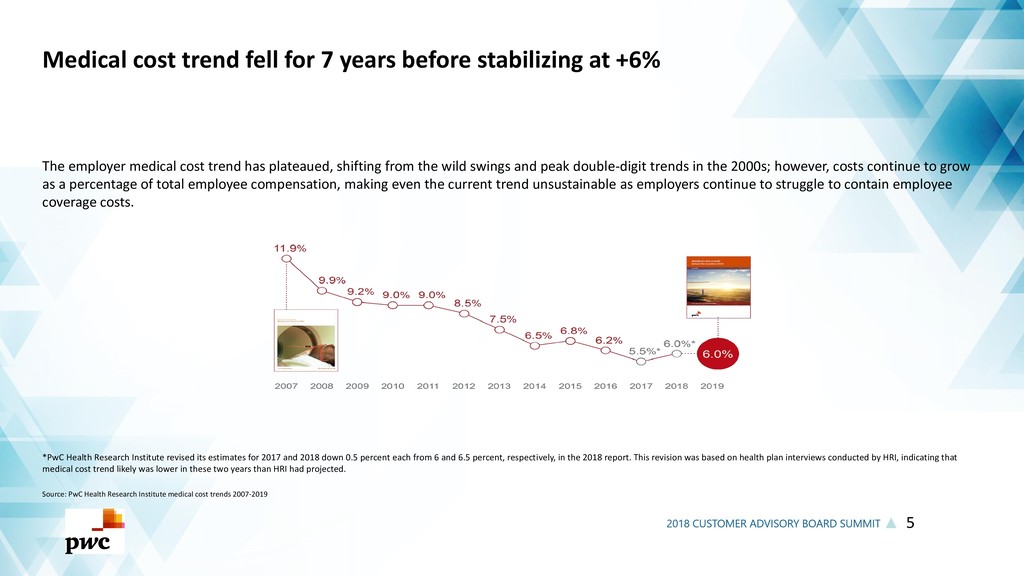

The employer medical cost trend has plateaued. The PwC Health Research Institute’s annual report projects the growth of medical costs in the employer market for 2019 to be 6 percent, the same as they were in 2018. Cost reduction will now start shifting to prices. PwC examines the opportunities and obstacles that will impact the industry and how this can be used as a guide for your business strategies in the coming year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}