owners of land, property and businesses in rural England and Wales • 35,000 members own or manage around half the rural land in England & Wales • CLA lobby on behalf of members at EU, national and regional level • Provide independent advice on a wide range of policy issues • Access to member benefits

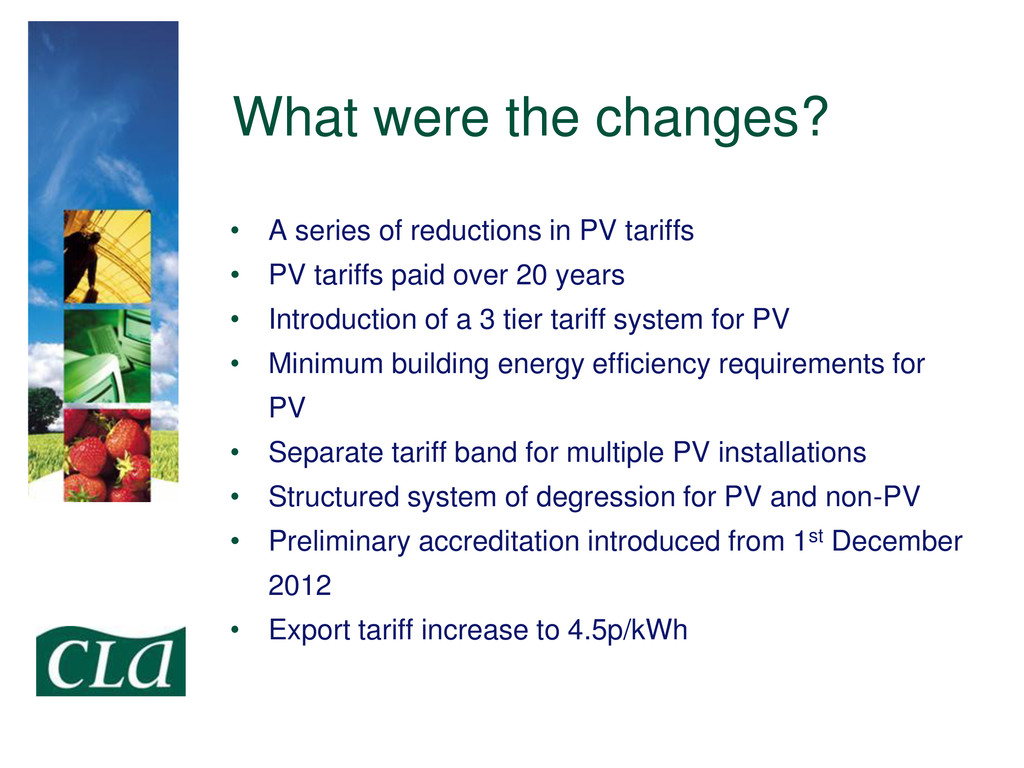

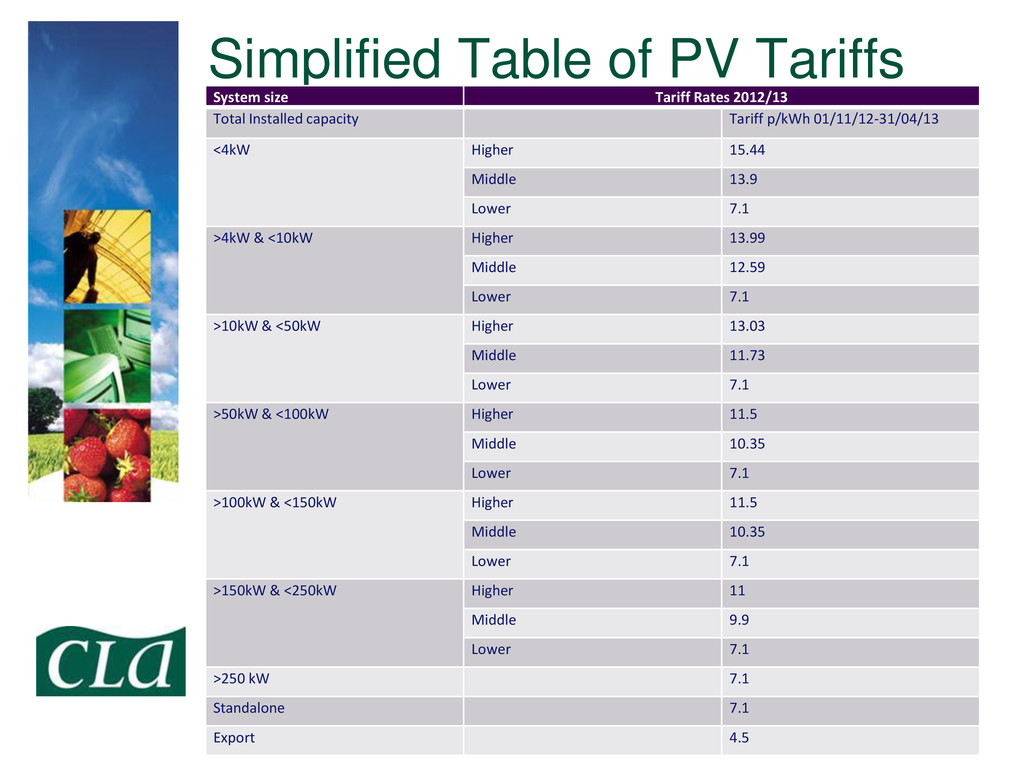

PV tariffs • PV tariffs paid over 20 years • Introduction of a 3 tier tariff system for PV • Minimum building energy efficiency requirements for PV • Separate tariff band for multiple PV installations • Structured system of degression for PV and non-PV • Preliminary accreditation introduced from 1st December 2012 • Export tariff increase to 4.5p/kWh

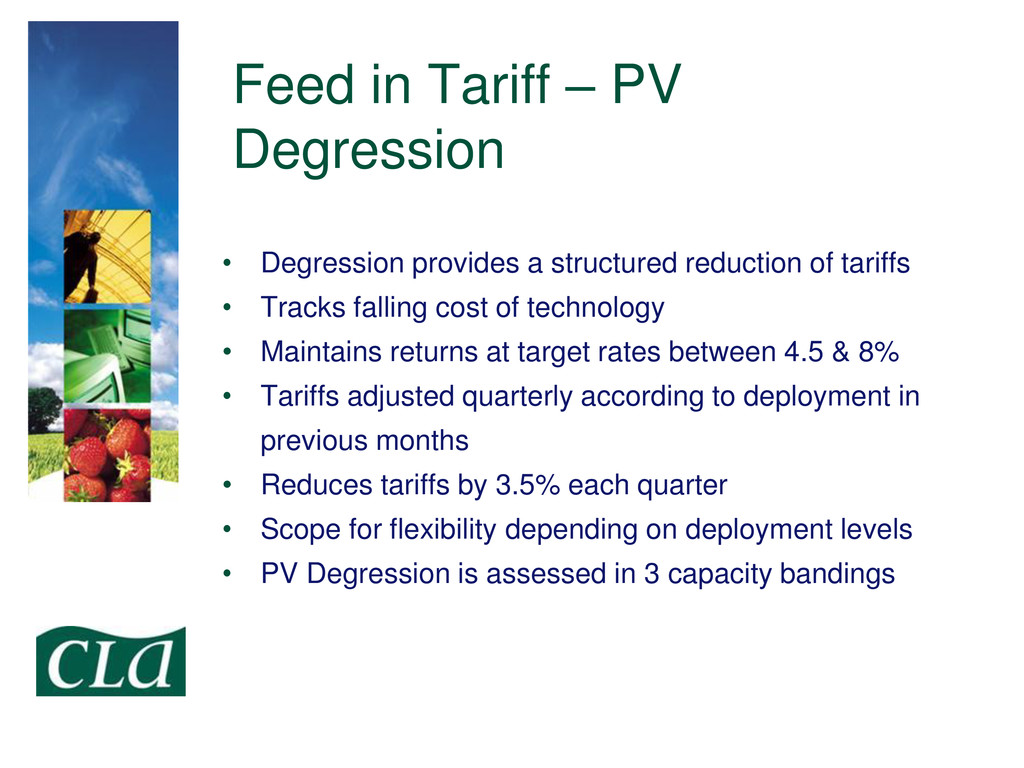

structured reduction of tariffs • Tracks falling cost of technology • Maintains returns at target rates between 4.5 & 8% • Tariffs adjusted quarterly according to deployment in previous months • Reduces tariffs by 3.5% each quarter • Scope for flexibility depending on deployment levels • PV Degression is assessed in 3 capacity bandings

2 months prior to changes • Tariff change dates for PV are 1st Feb, 1st May, 1st August, 1st November • E.g. Tariffs from Feb 2013- May 2013 were announced in December

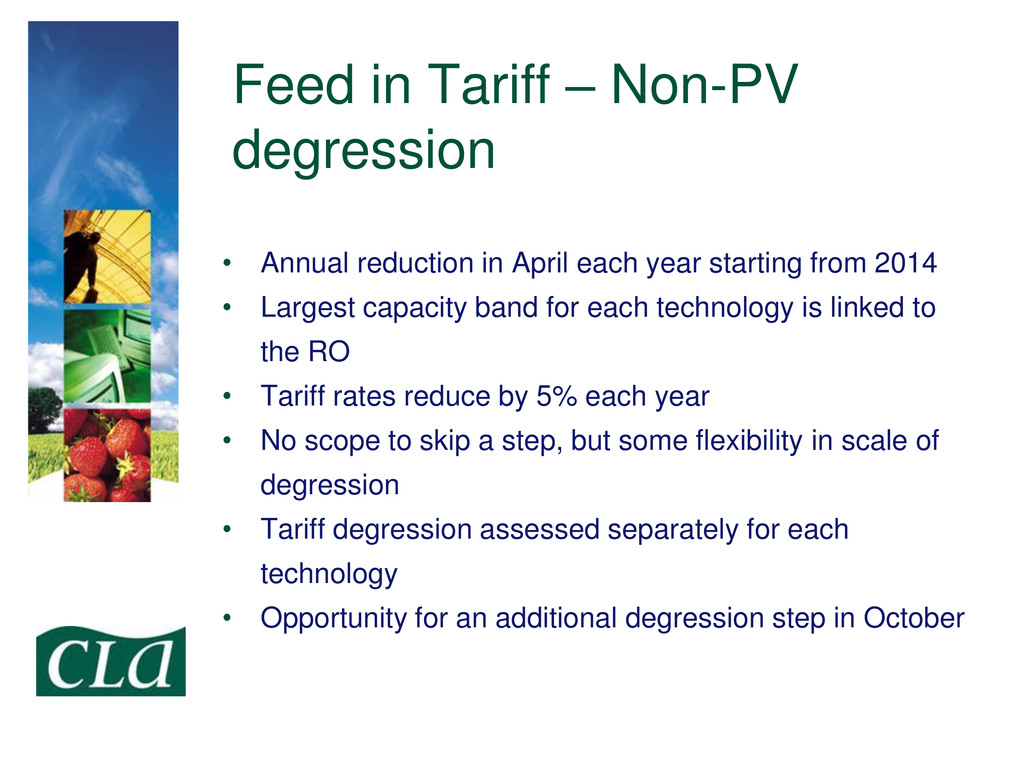

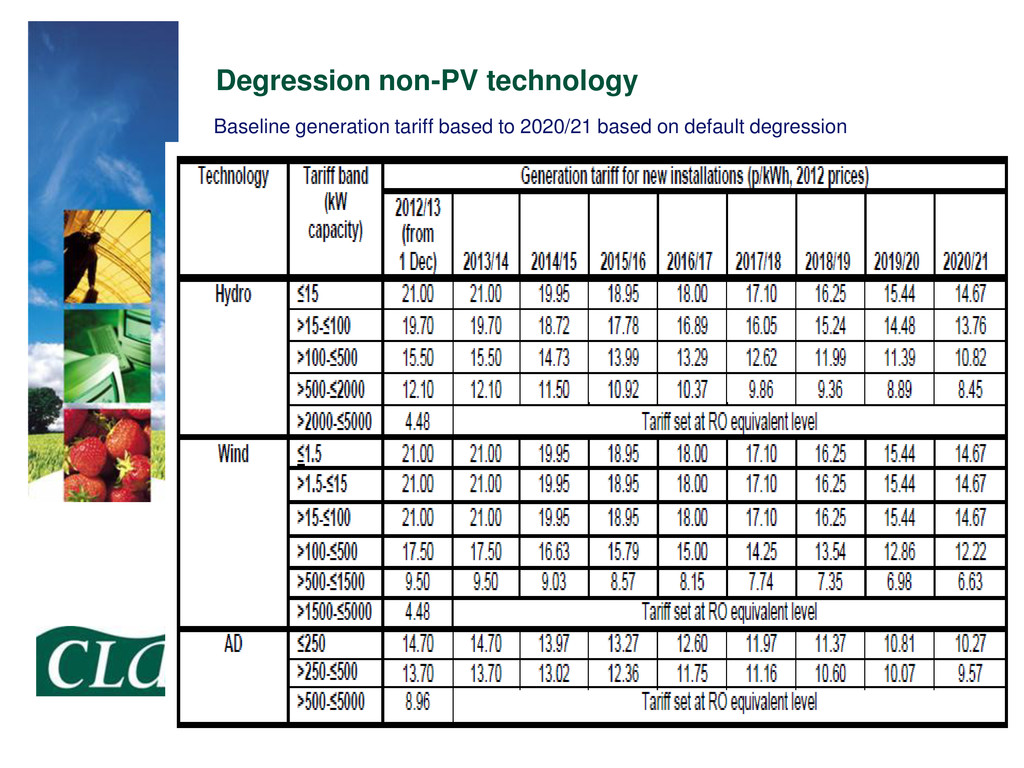

April each year starting from 2014 • Largest capacity band for each technology is linked to the RO • Tariff rates reduce by 5% each year • No scope to skip a step, but some flexibility in scale of degression • Tariff degression assessed separately for each technology • Opportunity for an additional degression step in October

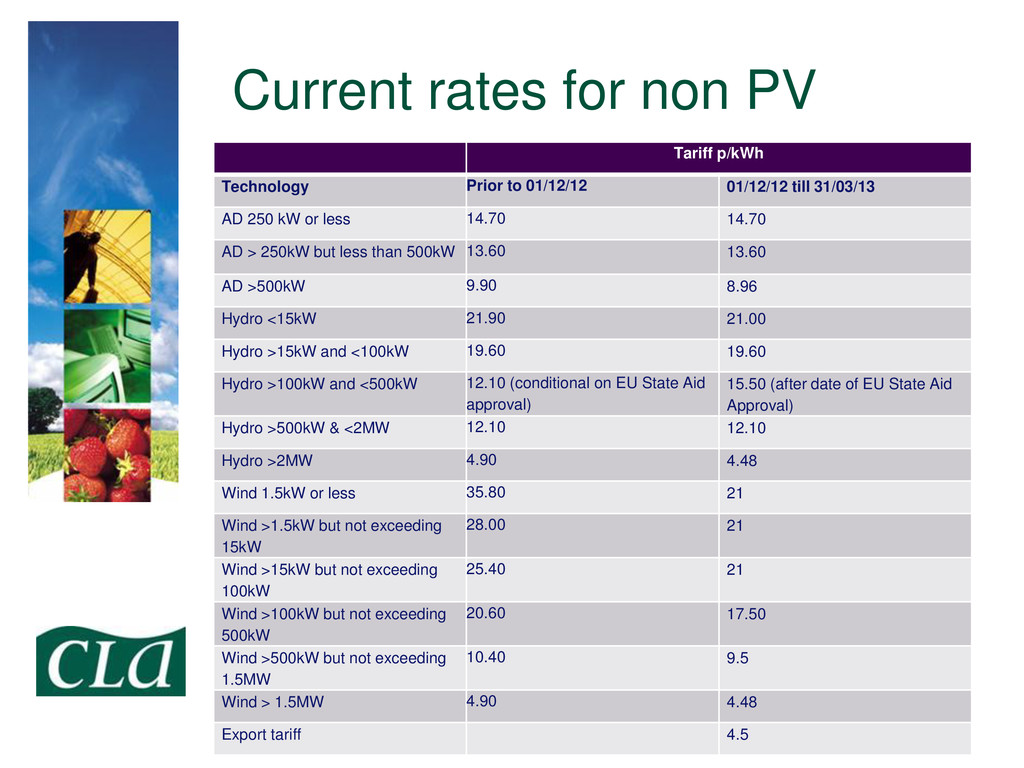

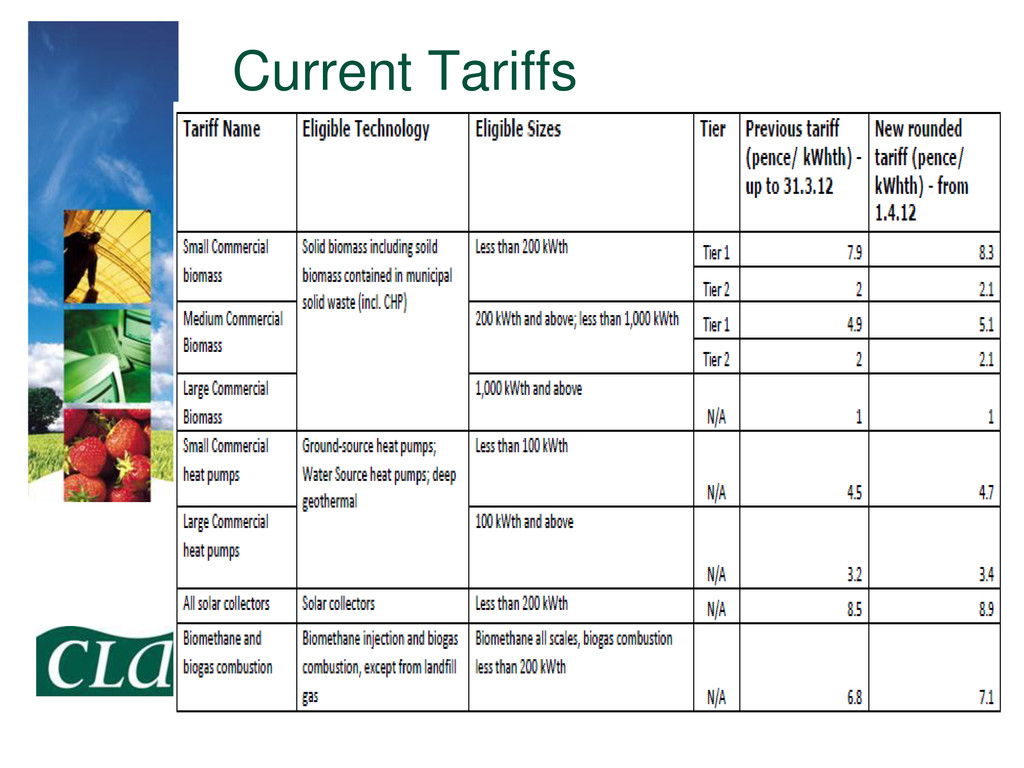

01/12/12 01/12/12 till 31/03/13 AD 250 kW or less 14.70 14.70 AD > 250kW but less than 500kW 13.60 13.60 AD >500kW 9.90 8.96 Hydro <15kW 21.90 21.00 Hydro >15kW and <100kW 19.60 19.60 Hydro >100kW and <500kW 12.10 (conditional on EU State Aid approval) 15.50 (after date of EU State Aid Approval) Hydro >500kW & <2MW 12.10 12.10 Hydro >2MW 4.90 4.48 Wind 1.5kW or less 35.80 21 Wind >1.5kW but not exceeding 15kW 28.00 21 Wind >15kW but not exceeding 100kW 25.40 21 Wind >100kW but not exceeding 500kW 20.60 17.50 Wind >500kW but not exceeding 1.5MW 10.40 9.5 Wind > 1.5MW 4.90 4.48 Export tariff 4.5

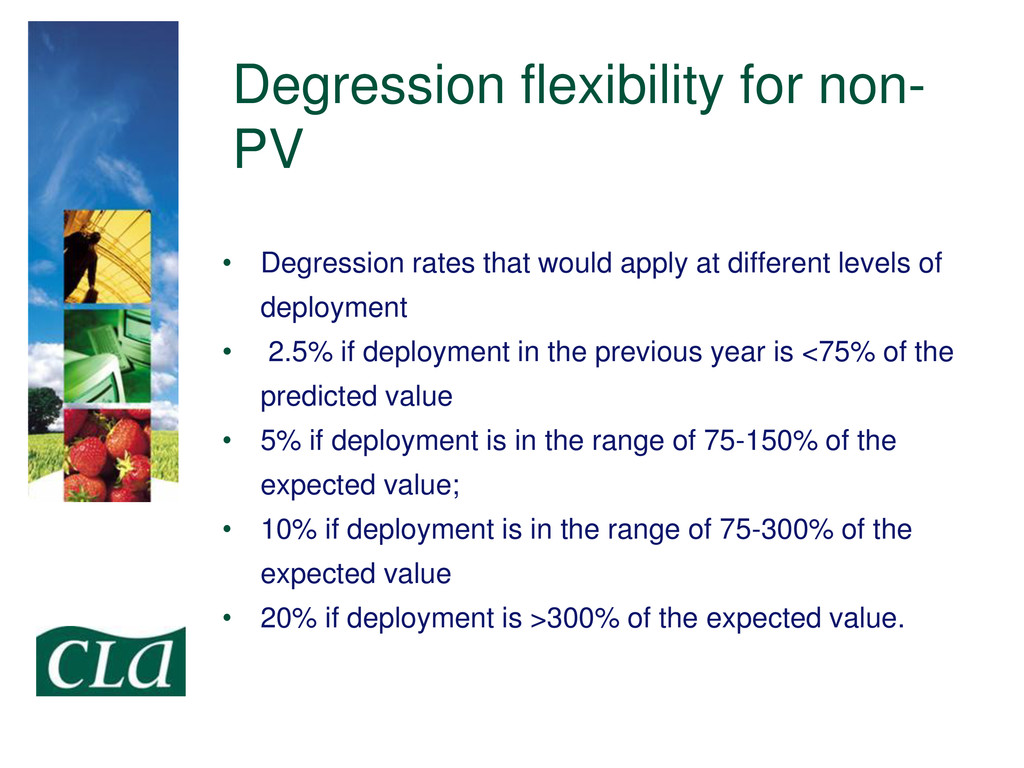

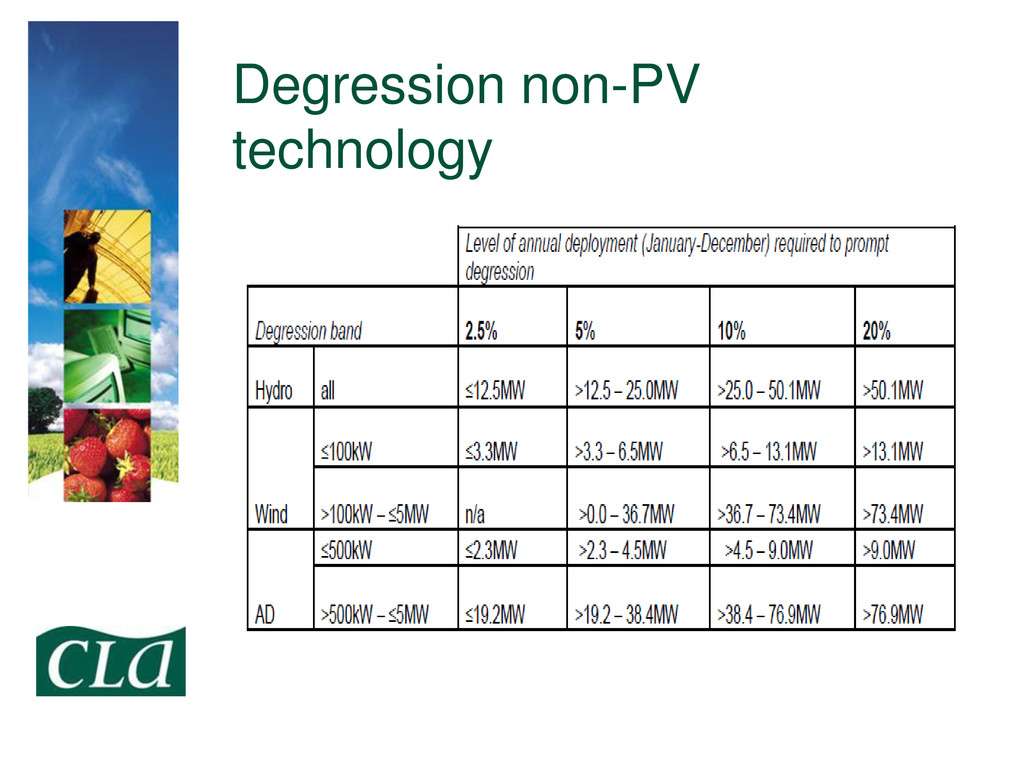

apply at different levels of deployment • 2.5% if deployment in the previous year is <75% of the predicted value • 5% if deployment is in the range of 75-150% of the expected value; • 10% if deployment is in the range of 75-300% of the expected value • 20% if deployment is >300% of the expected value.

• Allows larger projects to ‘lock in’ the level of tariff they will receive • Projects gaining full accreditation receive the tariff appropriate at the date of pre accreditation • Applies to PV and Wind over 50kW & all Hydro and AD projects • Evidence of planning permissions, grid connection agreement & relevant licensing required • Valid for 6 months for PV, 12 months for wind and AD up to 2 years for hydro

March assigned the Tariff available at 1st April that year. • Be aware - For PV EPC requirements are not assessed at preliminary accreditation and changes to installation after accreditation will negate the tariff guarantee

applied retrospectively • Tariff rates for PV have fallen, but so have costs • Export tariff rate increase • Structured degression reduces uncertainty for consumers and industry • Preliminary Accreditation reduces risk for larger projects • Feed in Tariff still a great deal for all technologies, especially when electricity generated utilised on site

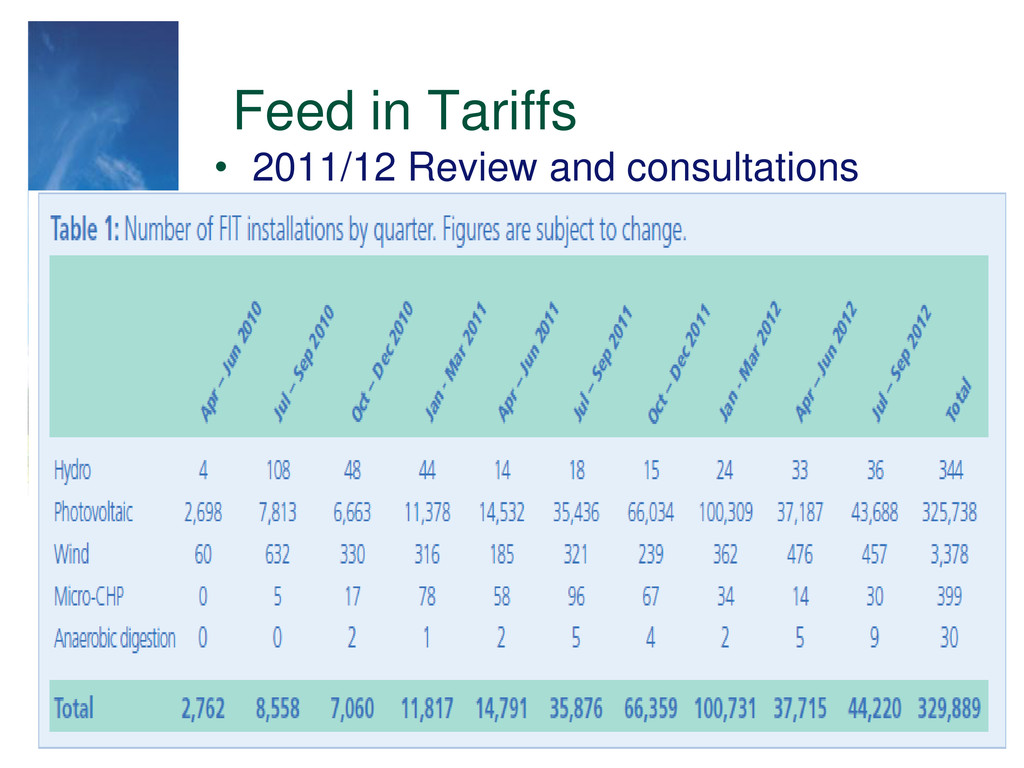

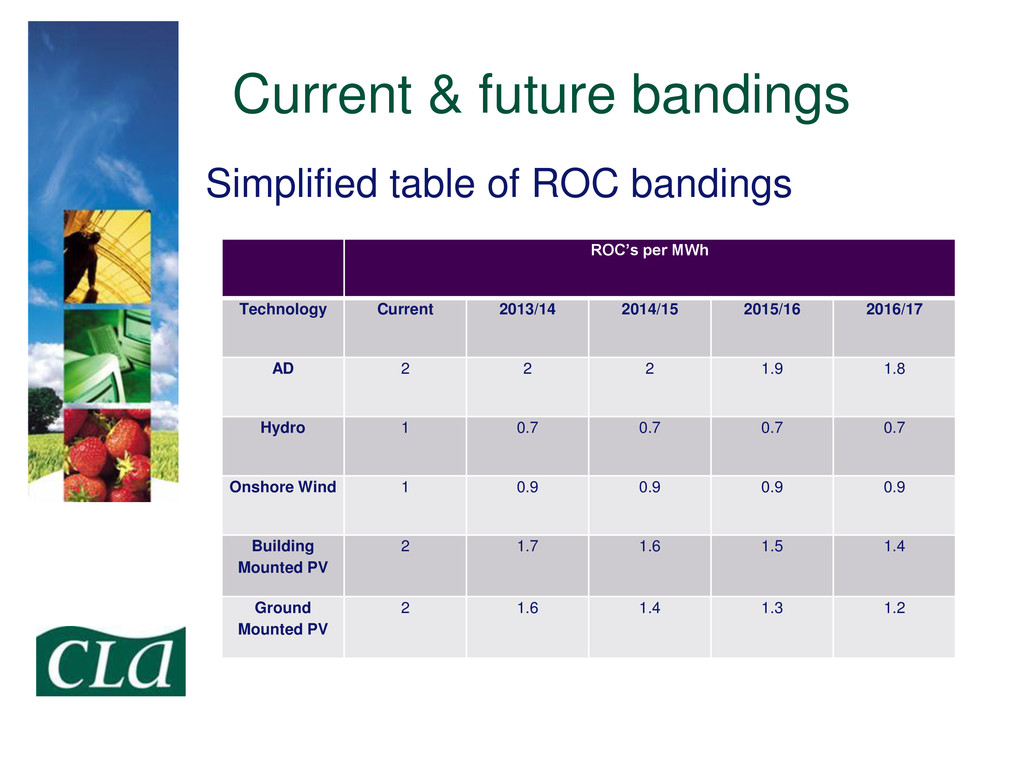

2012 • Number of changes were proposed • Exclusion of installations less than 5MW from RO was proposed • Carried out further consultation on PV banding with response in December 2012

of installations accredited • 90% installations are biomass • Review scheduled for 2014 • Budgetary control mechanism consultation • Two further consultations undertaken to be implemented in Summer 2013

scheme • Inclusion of direct air heating • Extension of support for biogas combustion to include systems over 200 kW • Sustainability requirement from April 2014 • Energy Efficiency Requirement

a surprise • For non domestic buildings minimum level of building efficiency • District heating schemes heating less than 10 properties • District heating schemes heating more than 10 properties

a range of technologies including biomass, GSHP, ASHP, Solar thermal • Final details of scheme not yet available • Opportunity for those off gas grid offers

with heat demand and off the gas grid • Even better if you can provide some of your own feedstock for biomass as a free/ low cost fuel • Get in under the non-domestic scheme currently available if you can. • 2013 is the year for the RHI

diversify income • Protect against future energy price rises • Business sustainability increasingly important • Utilise energy on site for best returns • Don't forget energy efficiency • Range of technologies to select from • 2013 and beyond offers great opportunities for renewable energy

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Any Questions? Tom Beeley, Renewable Energy Adviser [email protected] 0207 4607962](https://files.speakerdeck.com/presentations/bfdbbec05e770130188f22000a1c44c2/slide_31.jpg){kind=link}

{kind=link}