Sarah Rotman of CGAP was kind enough to present her fantastic slide deck on the basics of branchless banking to NetHope's Payment Innovations Working Group in March 2012.

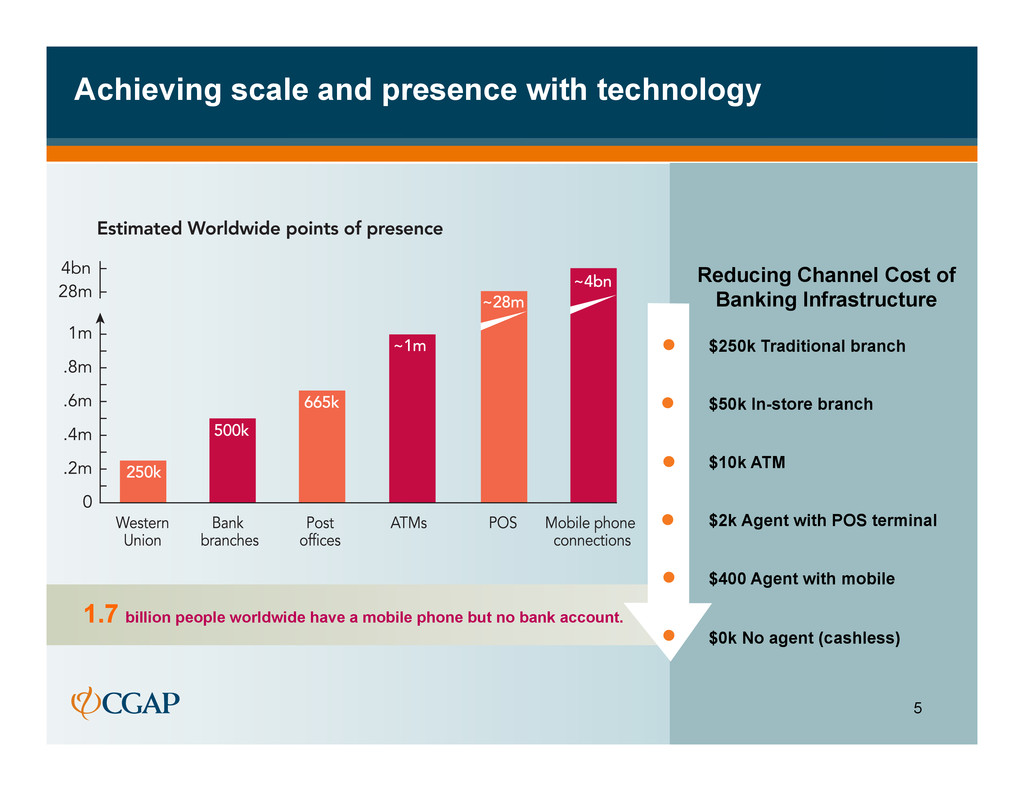

In-store branch $10k ATM $2k Agent with POS terminal $400 Agent with mobile $0k No agent (cashless) 1.7 billion people worldwide have a mobile phone but no bank account. Achieving scale and presence with technology 5

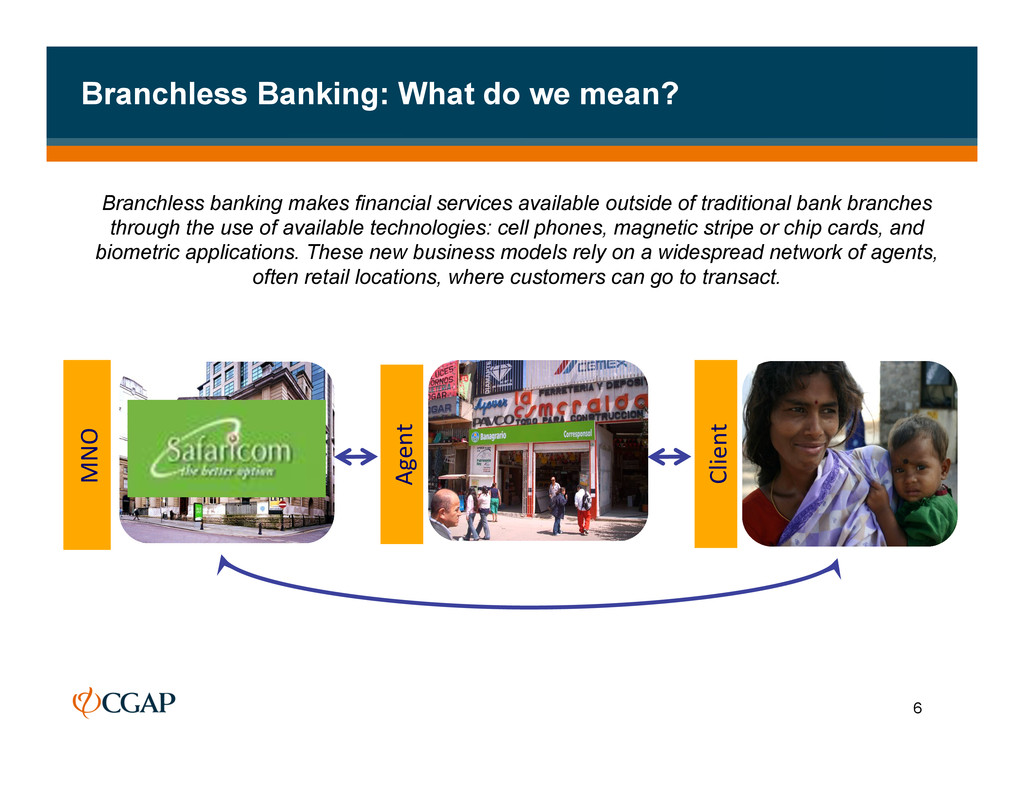

we mean? Branchless banking makes financial services available outside of traditional bank branches through the use of available technologies: cell phones, magnetic stripe or chip cards, and biometric applications. These new business models rely on a widespread network of agents, often retail locations, where customers can go to transact. MNO 6

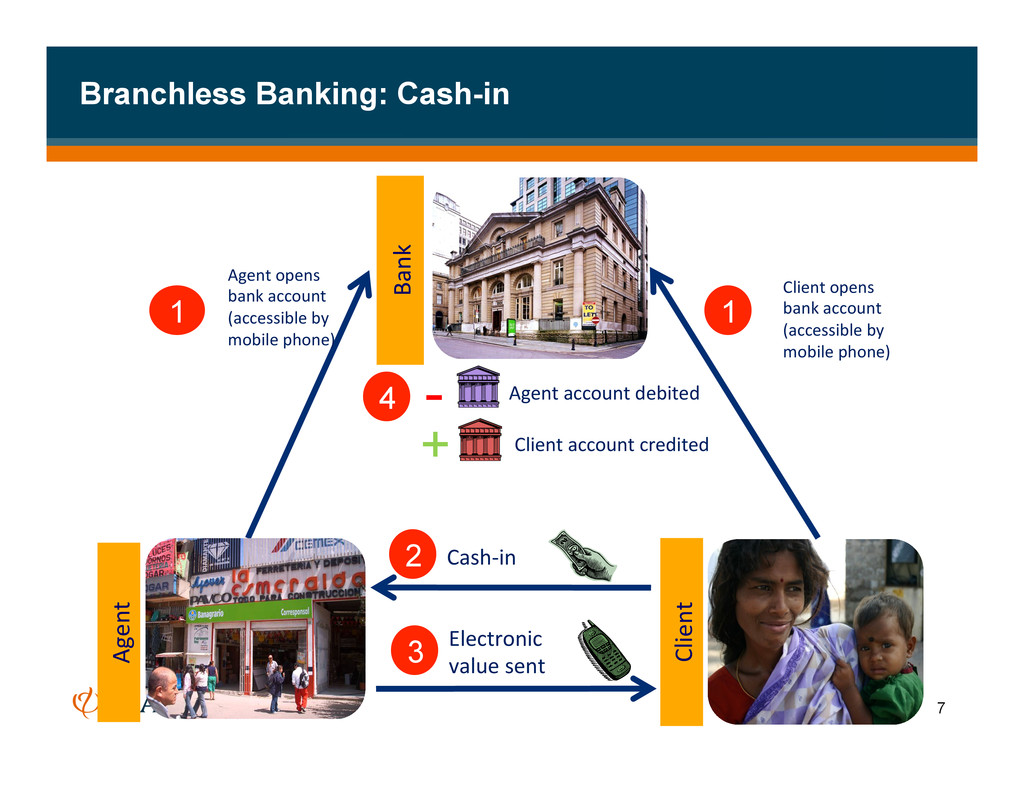

bank account (accessible by mobile phone) Agent opens bank account (accessible by mobile phone) 2 Cash-‐in 3 Electronic value sent 4 Agent account debited Client account credited 1 1 - + Agent 7

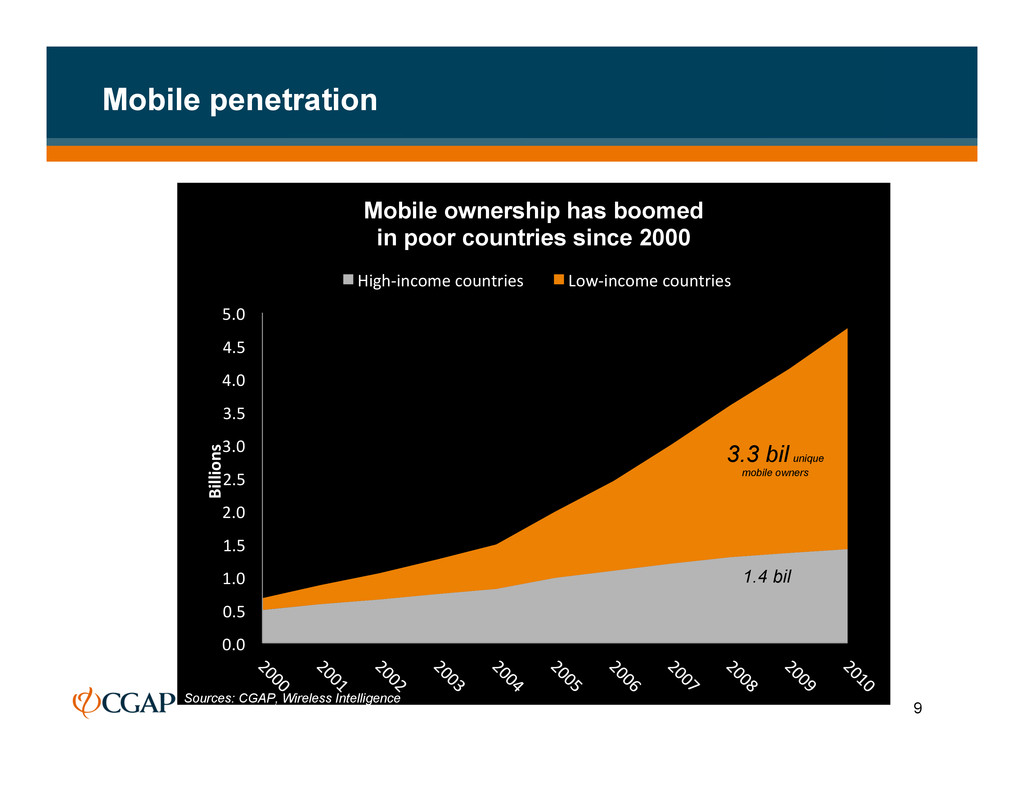

2.0 2.5 3.0 3.5 4.0 4.5 5.0 Billions Mobile ownership has boomed in poor countries since 2000 High-‐income countries Low-‐income countries Sources: CGAP, Wireless Intelligence 3.3 bil unique mobile owners 1.4 bil 9

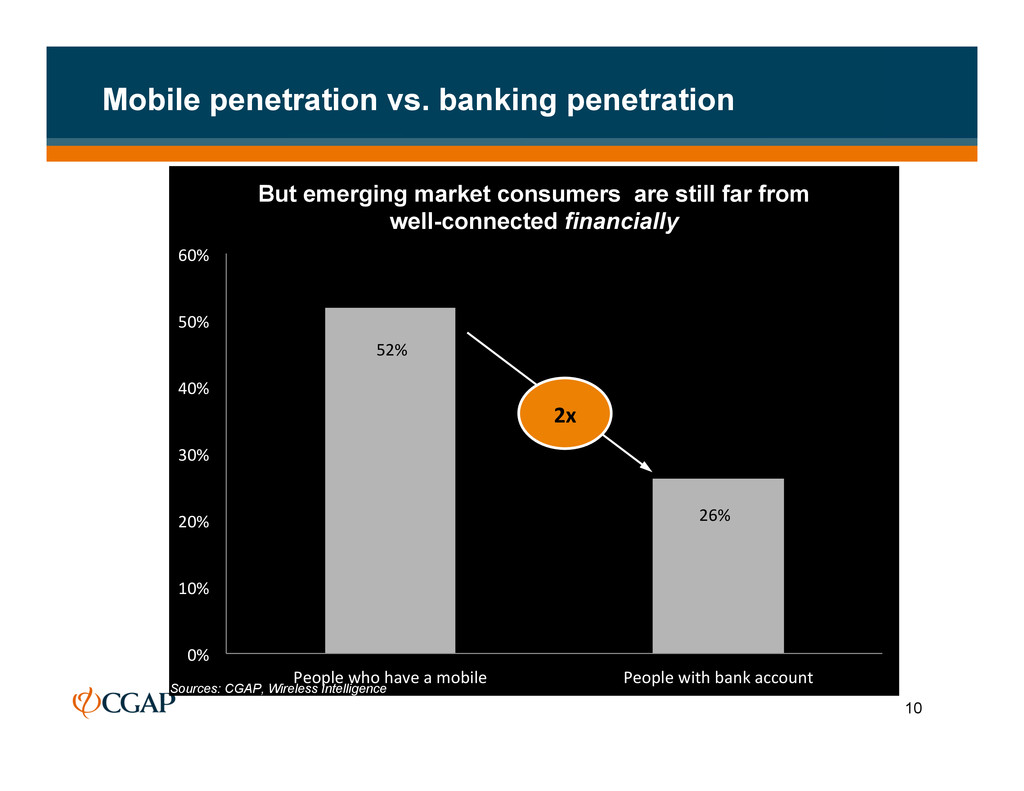

10% 20% 30% 40% 50% 60% People who have a mobile People with bank account But emerging market consumers are still far from well-connected financially 2x Sources: CGAP, Wireless Intelligence 10

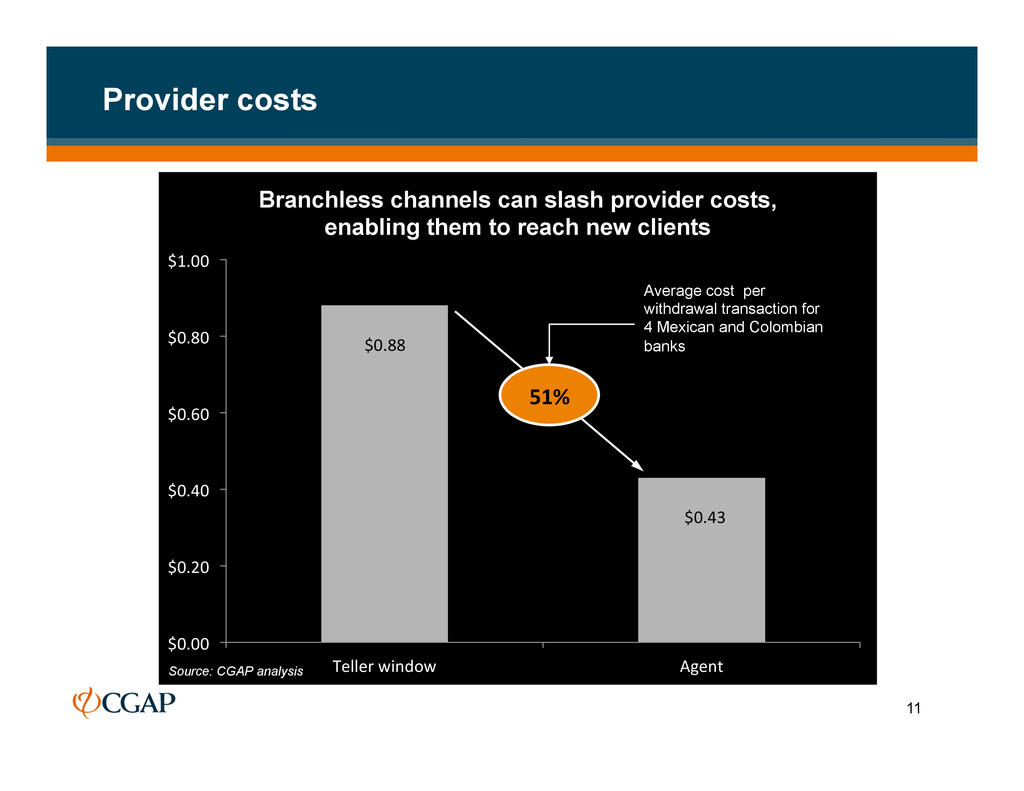

$0.20 $0.40 $0.60 $0.80 $1.00 Teller window Agent Branchless channels can slash provider costs, enabling them to reach new clients 51% Average cost per withdrawal transaction for 4 Mexican and Colombian banks Source: CGAP analysis 11

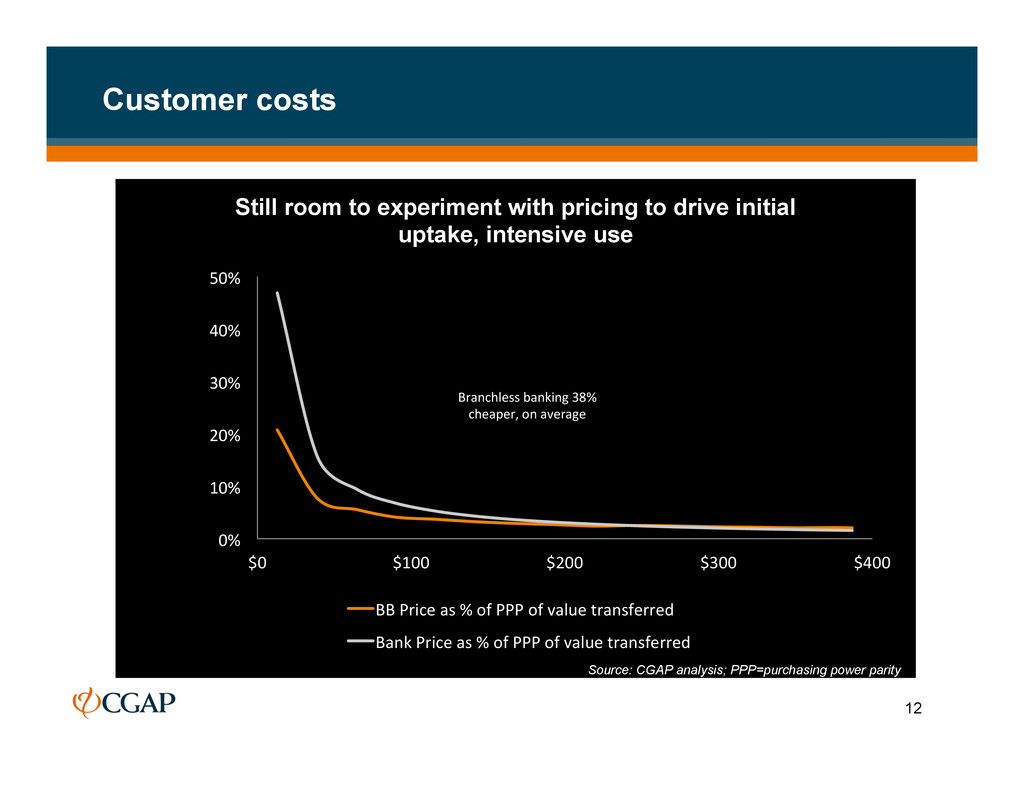

40% 50% $0 $100 $200 $300 $400 Axis Title Axis Title Still room to experiment with pricing to drive initial uptake, intensive use BB Price as % of PPP of value transferred Bank Price as % of PPP of value transferred Branchless banking 38% cheaper, on average Source: CGAP analysis; PPP=purchasing power parity 12

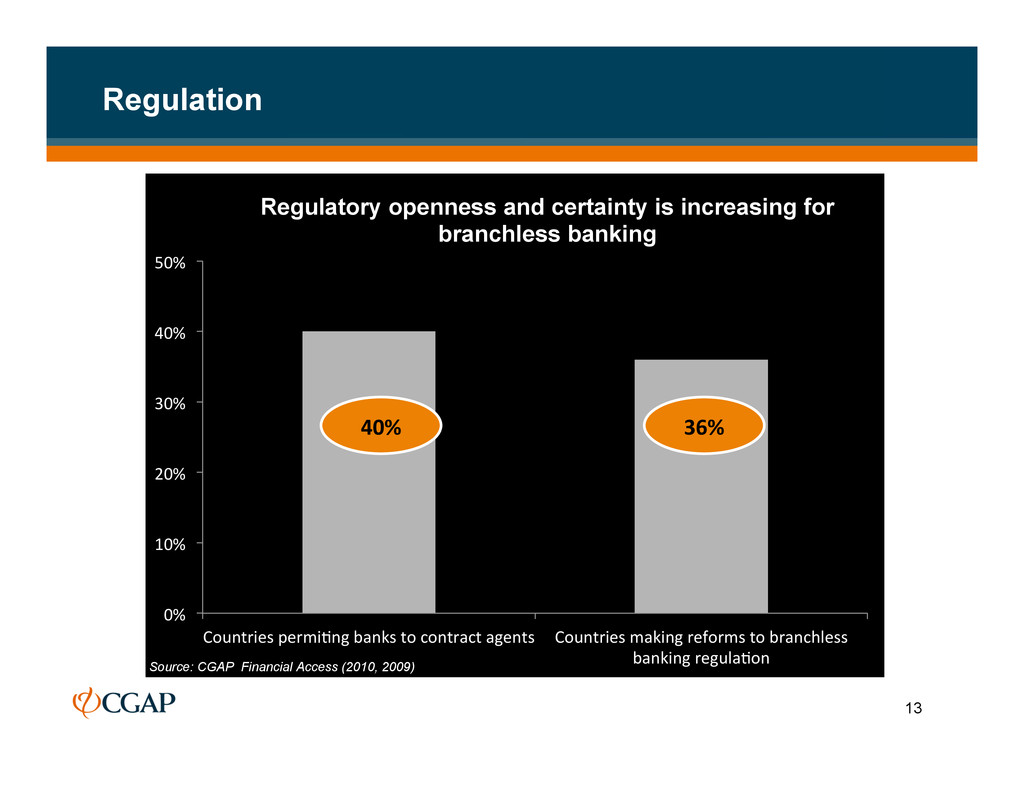

50% Countries permiRng banks to contract agents Countries making reforms to branchless banking regulaRon Regulatory openness and certainty is increasing for branchless banking 40% 36% Source: CGAP Financial Access (2010, 2009) 13

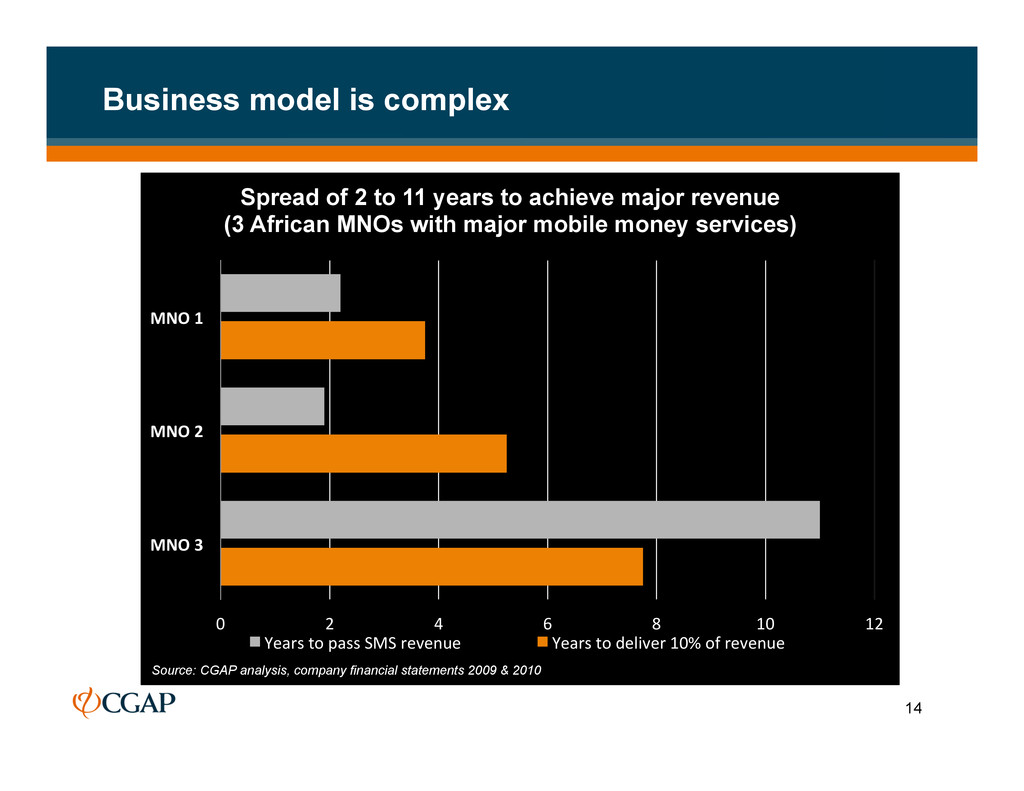

6 8 10 12 MNO 3 MNO 2 MNO 1 Spread of 2 to 11 years to achieve major revenue (3 African MNOs with major mobile money services) Years to pass SMS revenue Years to deliver 10% of revenue Source: CGAP analysis, company financial statements 2009 & 2010 14

KENYA Denise BRAZIL Source: CGAP analysis Daily Agent Profits (USD) Source: CGAP analysis But a universal requirement is understanding the agent’s business case 16

across all levels of the population Source: Jack & Suri, 2012; http://www.slate.com/blogs/future_tense/2012/02/27/m_pesa_ict4d_and_mobile_banking_for_the_poor_.html 19

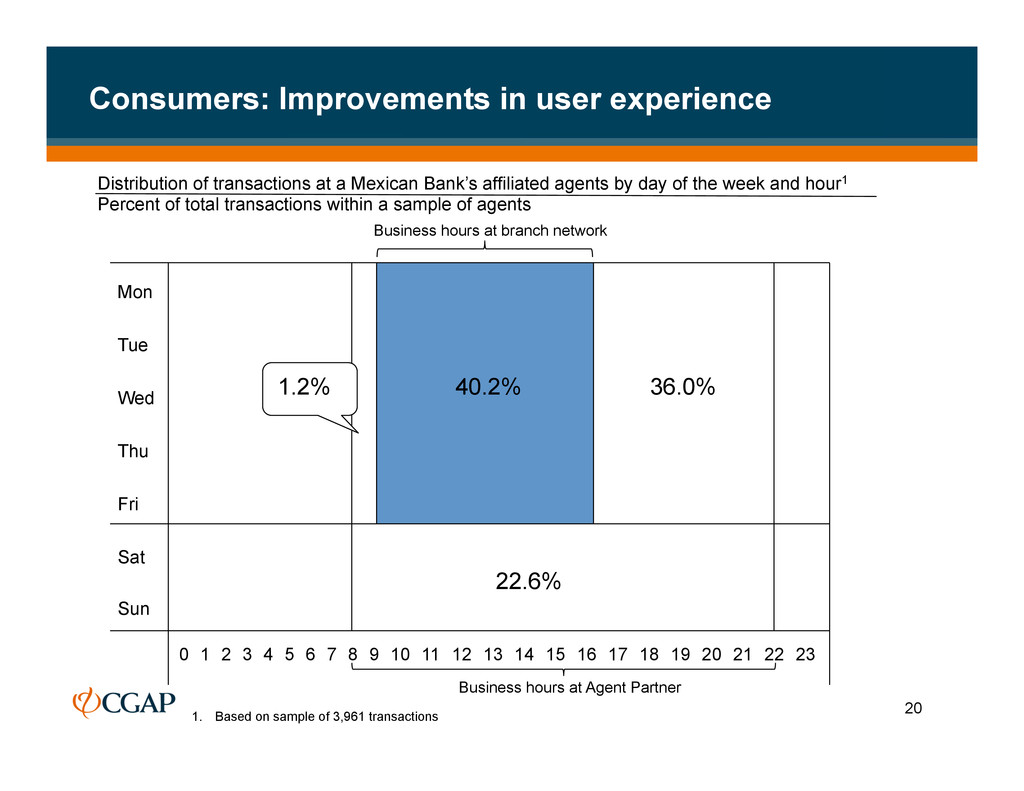

day of the week and hour1 Percent of total transactions within a sample of agents 1. Based on sample of 3,961 transactions Mon Tue Wed Thu Fri Sat Sun 1 0 2 3 4 5 6 10 8 12 14 16 18 20 22 21 23 9 7 11 13 15 17 19 22.6% 36.0% 1.2% 40.2% Business hours at Agent Partner Business hours at branch network Consumers: Improvements in user experience 20

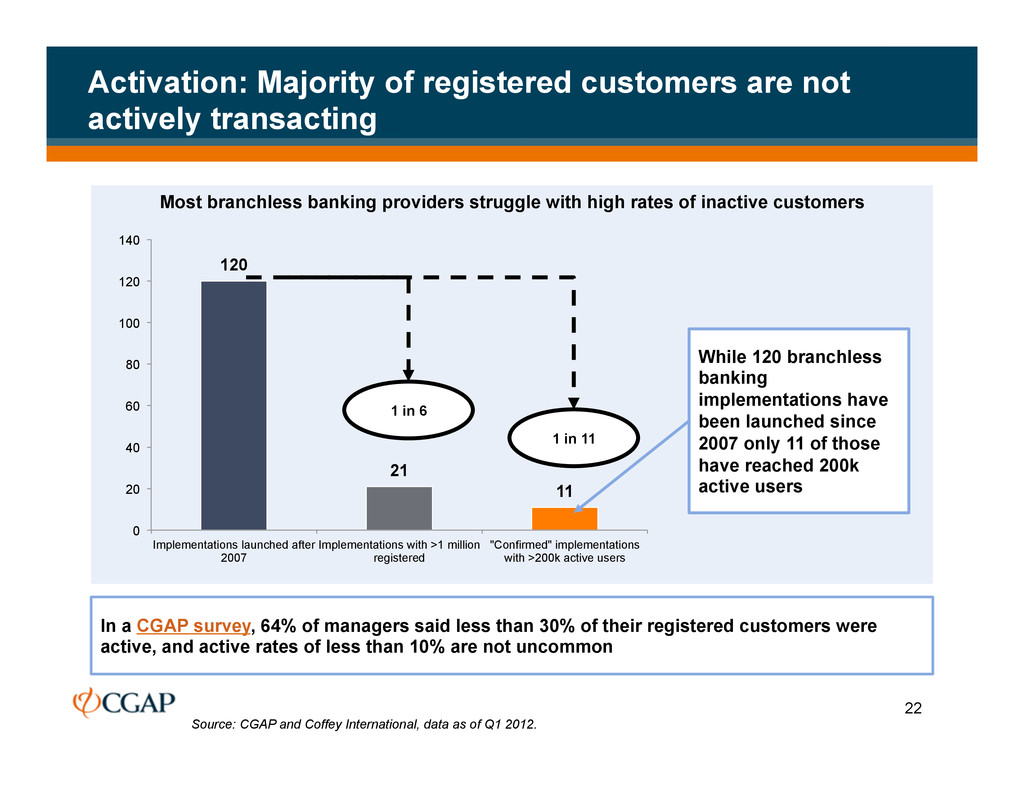

customers Activation: Majority of registered customers are not actively transacting 120 21 11 0 20 40 60 80 100 120 140 Implementations launched after 2007 Implementations with >1 million registered "Confirmed" implementations with >200k active users 1 in 11 1 in 6 While 120 branchless banking implementations have been launched since 2007 only 11 of those have reached 200k active users In a CGAP survey, 64% of managers said less than 30% of their registered customers were active, and active rates of less than 10% are not uncommon Source: CGAP and Coffey International, data as of Q1 2012. 22

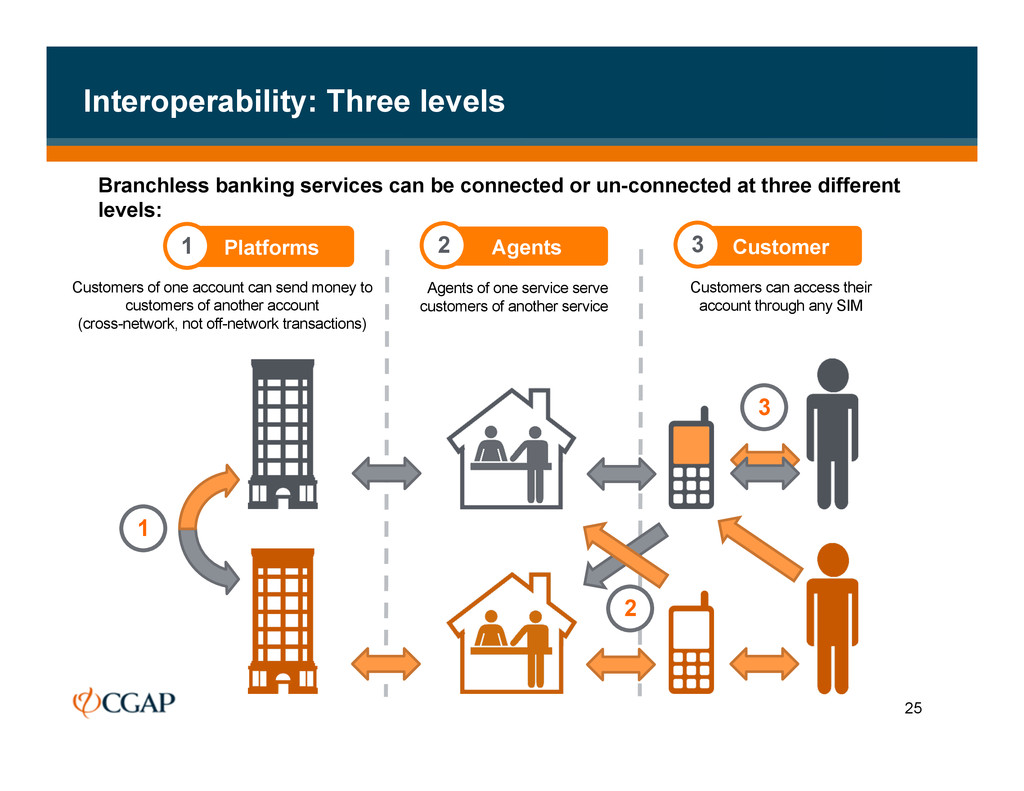

un-connected at three different levels: Platforms Agents Customer 1 2 3 Customers of one account can send money to customers of another account (cross-network, not off-network transactions) Agents of one service serve customers of another service Customers can access their account through any SIM 1 2 3 25

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}