Opening a business bank account in the UAE is achievable, predictable, and absolutely worth doing right the first time. Banks in Dubai, Abu Dhabi, and the free zones reward companies that present a coherent story: a clear activity scope, real economic substance, complete documents, and a factual KYC narrative. This long-form guide is written for founders and operators who want a traffic-earning article that ranks for mid-volume queries such as “business bank account UAE,” “open business bank account in Dubai,” “UAE bank account for non-residents,” “corporate KYC requirements,” “minimum balance UAE business account,” and “timeline to open bank account in the UAE.” It blends practical instructions with the exact searcher language people use when they are ready to act.

“In the UAE, speed is the reward for accuracy. The more consistent your documents, activity codes, and banking story, the faster your corporate account goes live.”

Who this guide is for

International founders running company formation in Dubai or other emirates and planning to open a corporate account quickly

Free zone and mainland businesses comparing requirements, fees, and minimum balances

HR/ops leads who need a clean onboarding path for Employment Visas aligned with banking

Finance leaders preparing KYC/AML/UBO documentation and a two-page compliance memo

Non-resident owners exploring a UAE bank account without local residency and wondering what changes for them

What counts as a “business bank account” in the UAE

When people search “business bank account UAE,” they usually mean a corporate current account with:

Multi-currency (AED, USD, EUR, GBP) and international transfers

Debit cards and expense controls for staff

Online banking with role-based permissions, maker-checker, and approval workflows

Relationship manager support and realistic monthly limits

Clean KYC/AML procedures tied to your licensed activities, UBOs, and economic substance

Free zone vs mainland through a banking lens

Both pathways work for corporate banking; the difference is how your story reads to compliance:

Free zone route works well for export-oriented services, consulting, SaaS, inter-zone B2B, and international clients. Your banking memo should emphasize foreign counterparties, corridors, multi-currency receipts, and operational substance (office tier, staff plan).

Mainland route is ideal for onshore UAE sales, retail, tenders, and service teams in the field. Your memo benefits from named domestic ICPs, ticket sizes in AED, and supplier/customer proximity.

Who can open a business bank account (and when)

Companies licensed in the UAE (free zone or mainland) with valid trade/ professional licenses

Shareholders and UBOs who can be clearly identified, screened, and documented

Directors/signatories authorized by board resolution or MOA

Non-resident owners can apply if the file demonstrates strong ties to the UAE market or credible international revenue with UAE substance

Document requirements: company, people, and operations

Banks ask for the same categories; the nuance is quality and consistency.

Company pack:

Trade/professional license, MOA or equivalent, company registry extract

Lease agreement or flexi-desk confirmation; establishment card if applicable

Board resolution for account opening and signatories

Tax registrations where relevant (VAT), ESR notifications if any

People pack:

Passports of shareholders/UBOs/directors/signatories

Emirates ID and residence visa copies (if available), or non-resident status explanation

Proofs of address (recent, matching spelling and transliteration)

CV or track record for founders (sector experience helps)

Operations pack (the part that accelerates files):

Two-page banking narrative covering what you sell, to whom, where, corridors, typical invoice sizes, currencies, seasonality, and why UAE

Specimen invoices and sample contracts (sanitized)

Client and supplier profiles by geography; pipeline view is useful

Website content consistent with your licensed activities and memo

Organizational chart, user roles for online banking (maker, checker, approver)

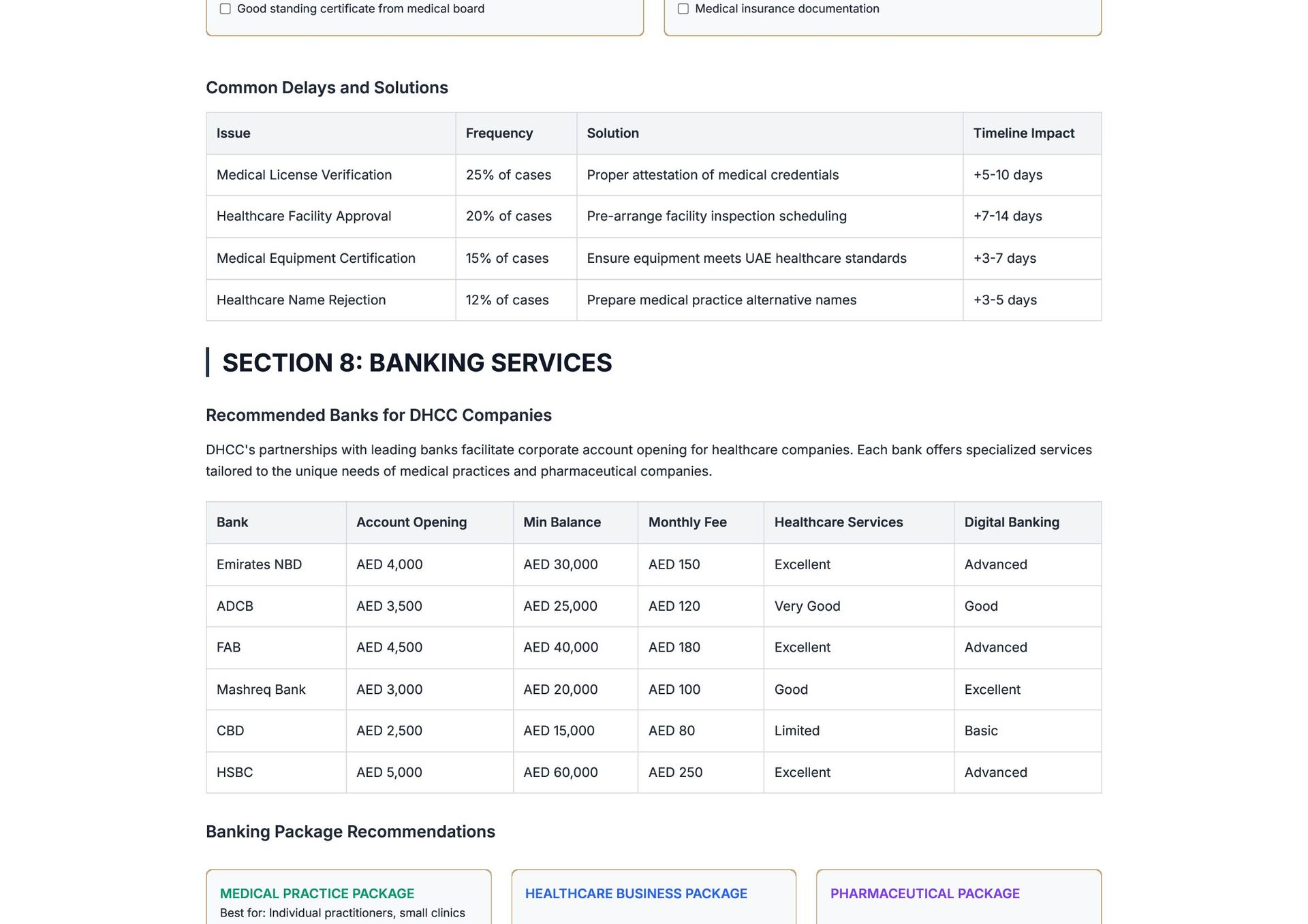

Fees, minimum balances, and practical limits

Monthly fees: often waived above a minimum average balance; otherwise modest fixed charges may apply

Minimum balance: varies by bank and account tier; align to expected monthly flows

Multi-currency: most corporate accounts support AED plus majors; confirm FX spreads, inward/outward transfer fees, and card issuance costs

Limits: initial transfer caps may start conservative; relationship managers can raise limits after usage and compliance comfort

Step-by-step: how to open a business bank account in the UAE

Pre-audit your documents

Confirm names, addresses, and transliteration match across license, passports, proofs, and lease. Fixing drift now saves weeks later.

Draft the two-page KYC memo

Keep it factual. Describe services, ICPs, corridors, typical ticket sizes, currencies, and economic substance. Avoid marketing language; compliance teams value clarity.

Prepare specimens and org details

One sanitized invoice and one template contract, plus an org chart and who will hold maker/checker/approver roles. Decide who needs card access.

Submit the application and schedule the interview

The relationship manager will test coherence: do your activities match the narrative, website, and documents? Be crisp about payment flows and counterparties.

Respond to clarifications quickly

Have PDFs ready in a version-controlled vault. Same-day answers show operational maturity and reduce additional requests.

Activation and online banking setup

Enroll users, set two-factor authentication, define approval thresholds, and test inbound/outbound transfers in all required currencies.

Further reading on a hands-on account-opening pathway, practical timelines, and orchestration tips for founders and finance teams:

https://inlex-partners.com/services/bank-account-opening/

Non-resident business banking: what changes and how to prepare

Non-resident owners often ask, “Can I open a business bank account in the UAE without residency?” The answer is yes, provided the file demonstrates:

Robust documentation of UBOs and source of funds

A credible economic-substance story (office tier, on-the-ground operations plan, travel cadence)

Real client and supplier ties, or a clear go-to-market model with international corridors

Clean, consistent artifacts and a website aligned with licensed activities

Tips that move the needle:

Show planned visits and a cadence for meetings with clients and the bank

Highlight staff roles and hiring plans tied to visa capacity

Be explicit about corridors, currencies, and sanctions-aware routing

Deep-dive for non-residents, including documentation nuance and interview preparation:

https://inlex-partners.com/services/non-resident-bank-account/

Free zone vs mainland: banking considerations in practice

Free zone companies should align activity codes and website copy to export-oriented services, inter-zone B2B, or cross-border delivery; emphasize multi-currency receipts and international corridors.

Mainland companies benefit from onshore testimonials, local counterparties, and AED-denominated flows; show how your office and staff support delivery.

In both cases, your economic substance—lease, visa capacity, support model—needs to make sense relative to planned revenue and payment volumes.

Common reasons for delays (and how to avoid them)

Inconsistency between license activities, website descriptions, and the KYC memo

Name or address mismatches across documents; outdated proofs; missing attestations

Vague customer profiles, unexplained corridors, or unclear currencies

Lack of economic substance: no lease details, no user roles, no operational plan

Slow responses to clarifications; inability to produce clean PDFs quickly

Business banking checklist (copy-paste)

Use this list to organize your file and avoid ping-pong:

Trade/professional license, MOA/registry extract, board resolution for signatories

Lease or flexi-desk confirmation; establishment card if applicable

Passports of shareholders/UBOs/directors/signatories

Emirates ID and visas (if available), or non-resident explanation

Proofs of address that match passports and spellings

Two-page KYC narrative: services, ICPs, corridors, ticket sizes, currencies, substance

Specimen contract and specimen invoice (sanitized)

Organizational chart; user access plan (maker/checker/approver)

Website content aligned with activities and narrative

Document vault with version-controlled PDFs; naming convention for instant retrieval

Test plans for inbound/outbound transfers and multi-currency flows after activation

Policy for card issuance, user permissions, approval thresholds, and notifications

Quarterly review: limits vs usage, corridors, FX needs, compliance updates

Process owner for renewals, attestations, ESR, VAT, corporate tax changes

Explore a consolidated corporate-account overview, including multi-currency options and SME-friendly workflows:

https://inlex-partners.com/services/business-bank-account-uae/

Post-activation: keep compliance boring and predictable

Banking is not a one-time sprint; it is an operating rhythm. Maintain:

A quarterly ops review to align transaction volumes with limits, corridors, and FX needs

An updated KYC memo when you launch new products, add geographies, or change pricing models

A living document vault with the latest licenses, leases, signatory resolutions, and IDs

A sanctions-aware routing policy and an escalation path for unusual transactions

An audit trail for who changed user permissions, thresholds, or beneficiaries

Relevant mid-volume queries: update KYC UAE, compliance review UAE, increase bank limits UAE, add new corridor UAE, sanctions screening policy, beneficiary approval workflow.

Hiring and visas: why immigration sequencing supports banking

Banks look for operational reality. Sequencing Employment Visas and Emirates IDs for founders and finance staff signals credible presence. Match visa capacity to your office tier and hiring plan; publish a dependents brief for senior candidates; keep a tracker for entry permits, medicals, biometrics, e-visas, and ID collection. The more your corporate rhythms look predictable, the more comfortable compliance becomes with higher limits and faster clarifications.

FAQ: concise, snippet-ready answers

How long does it take to open a business bank account in the UAE?

Simple files can move in a few business days after the interview; more complex cases take longer. Most delay comes from inconsistent documents or vague KYC narratives.

Do I need residency to open a corporate account?

Not strictly, but non-resident files must present stronger ties, substance, and a coherent operating plan. Expect enhanced due diligence.

What documents are mandatory?

License pack, MOA/registry extract, board resolution, lease/office proof, passports and UBO proofs, proofs of address, a two-page KYC memo, and specimen contracts/invoices.

What minimum balance and fees should I expect?

Ranges vary by bank and account tier. Align the minimum balance to your forecast; aim to waive monthly fees through usage or average balances.

Which currencies can I use?

AED plus major currencies are common. Confirm FX spreads, transfer fees, and cut-off times before you lock corridors.

Why do banks ask for a website?

Because the website must reflect licensed activities and your banking narrative. Incoherence triggers clarifications and slows approval.

What if my application was rejected?

Fix inconsistencies, upgrade substance (office tier, staffing plan), clarify corridors, and redraft the KYC memo. Then re-apply with a tighter file.

Final word for operators

Treat bank onboarding like a release train: define owners, set buffers, log artifacts, and test flows. The UAE rewards companies that operate with clarity—clean documents, a grounded narrative, and a realistic plan for growth. Do that, and your corporate account becomes a lever, not a bottleneck.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}