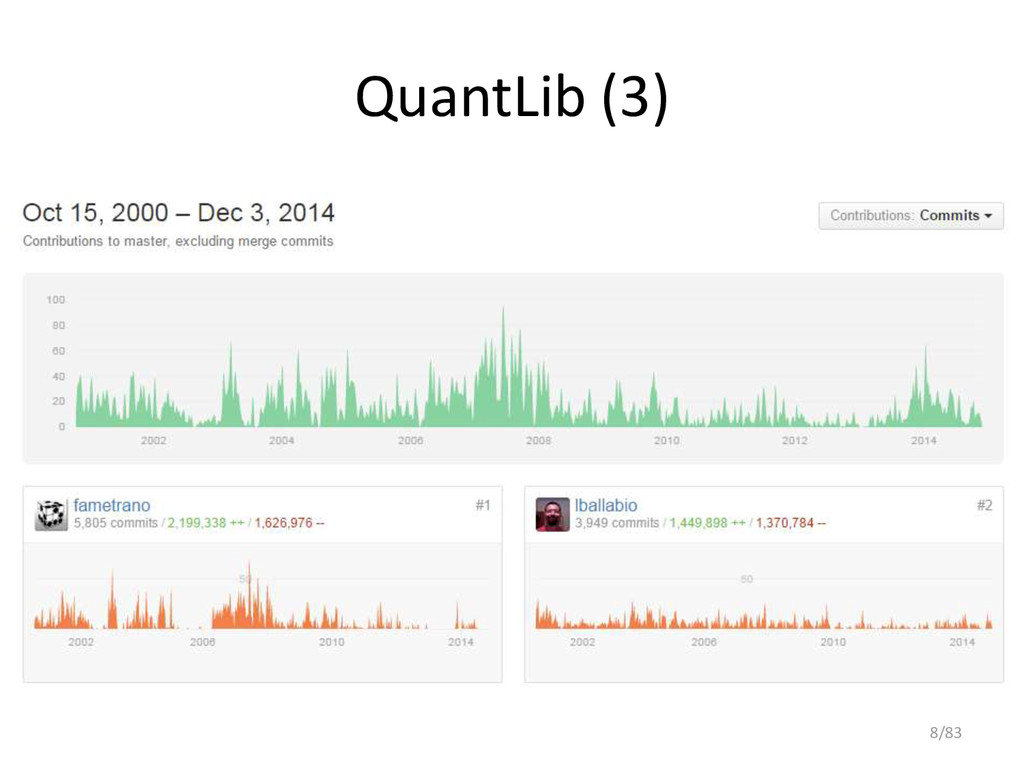

[email protected] Banca IMI IntesaSanpaolo Milano-Bicocca University QuantLib Hayek Money Düsseldorf , 4th of December 2014, QuantLib User Meeting https://speakerdeck.com/nando1970/open-source-finance-quantlib-opengamma-bitcoin

four essential freedoms: 1. The freedom to run the program as you wish, for any purpose 2. The freedom to study how the program works, and change it so it does your computing as you wish. 3. The freedom to redistribute copies. 4. The freedom to distribute copies of your modified versions to others. 3/83

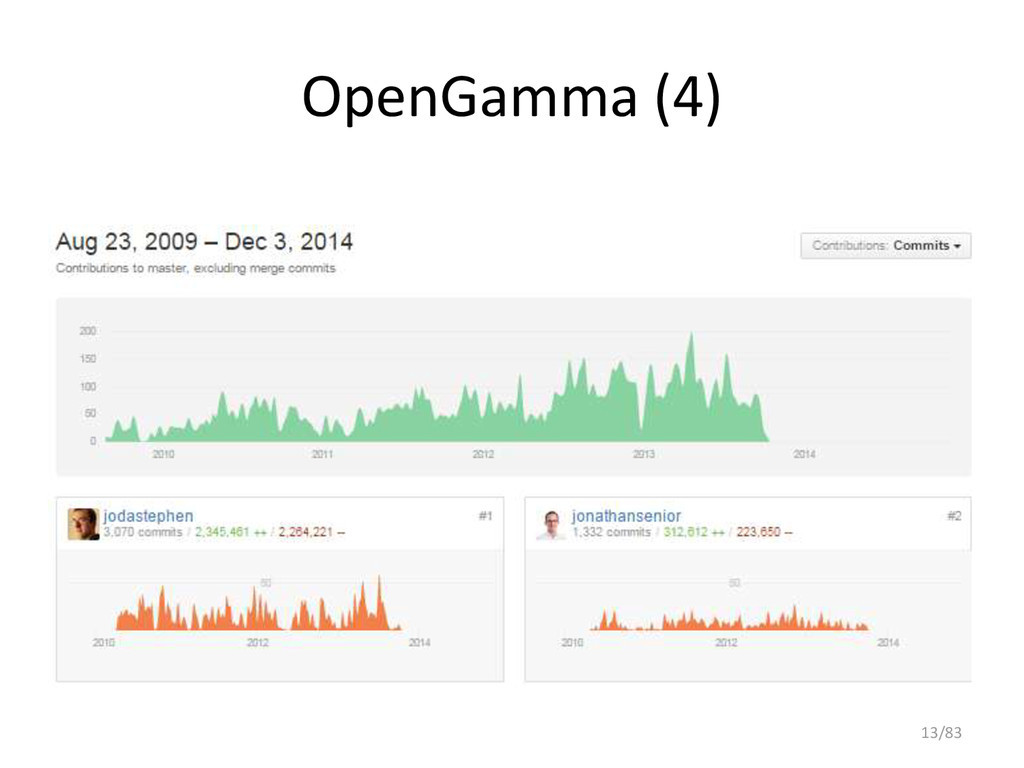

of $23.35 million from Accel Partners, Firstmark Capital, ICAP and Euclid Opportunities • Headquartered in London with an office in New York City • 70% of employees in R&D 10/83

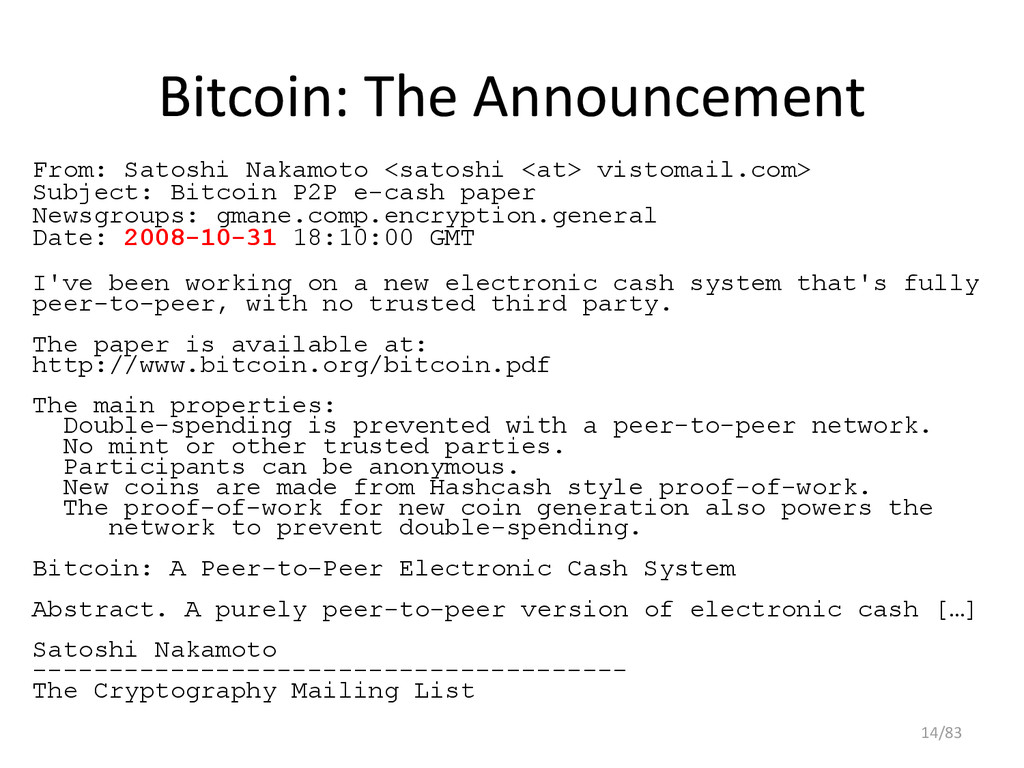

Bitcoin P2P e-cash paper Newsgroups: gmane.comp.encryption.general Date: 2008-10-31 18:10:00 GMT I've been working on a new electronic cash system that's fully peer-to-peer, with no trusted third party. The paper is available at: http://www.bitcoin.org/bitcoin.pdf The main properties: Double-spending is prevented with a peer-to-peer network. No mint or other trusted parties. Participants can be anonymous. New coins are made from Hashcash style proof-of-work. The proof-of-work for new coin generation also powers the network to prevent double-spending. Bitcoin: A Peer-to-Peer Electronic Cash System Abstract. A purely peer-to-peer version of electronic cash […] Satoshi Nakamoto --------------------------------------- The Cryptography Mailing List 14/83

Worked on Bitcoin since 2007, published the paper in 2008 • Released as open source free software in January 2009 • His involvement stops mid-2010 • Entrusted the Bitcoin SourceForge project and a copy of the alert key to Gavin Andresen, effectively his successor • Must own about 1M bitcoins, never spent Bitcoin: A peer-to-peer electronic cash system http://www.bitcoin.org/bitcoin.pdf http://mag.newsweek.com/2014/03/14/bitcoin-satoshi-nakamoto.html 15/83

long-term promise, particularly if the innovations promote a faster, more secure and more efficient payment system. • Jared Cohen: I think it’s very obvious to all of us that crypto-currencies are inevitable • Marc Andreessen: Bitcoin today is like Internet in 1994, weird and scary 20/83

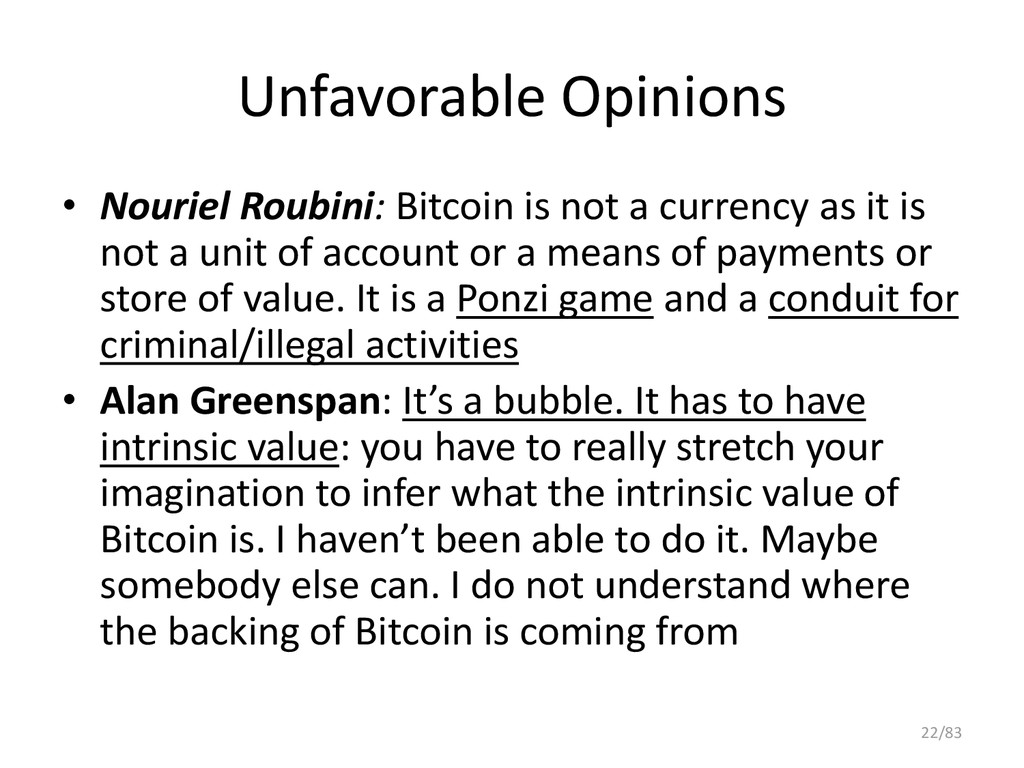

as it is not a unit of account or a means of payments or store of value. It is a Ponzi game and a conduit for criminal/illegal activities • Alan Greenspan: It’s a bubble. It has to have intrinsic value: you have to really stretch your imagination to infer what the intrinsic value of Bitcoin is. I haven’t been able to do it. Maybe somebody else can. I do not understand where the backing of Bitcoin is coming from 22/83

backed by any government or organization • instantaneous peer-to-peer transactions • no need for trusted third party • cryptographic security • low-cost banking for everybody everywhere https://bitcoin.org/en/faq http://www.coindesk.com/information/ 23/83

– prohibits financial institutions from trading, underwriting, or offering insurance in bitcoins or any other digital currency – Bitcoin is not to be considered a currency – owning bitcoins is not outlawed or prohibited • As of December 2013 BTC China was world's largest Bitcoin exchange by volume • Alibaba, China's top Internet retailer, stopped using bitcoins as of January 19 2014. 25/83

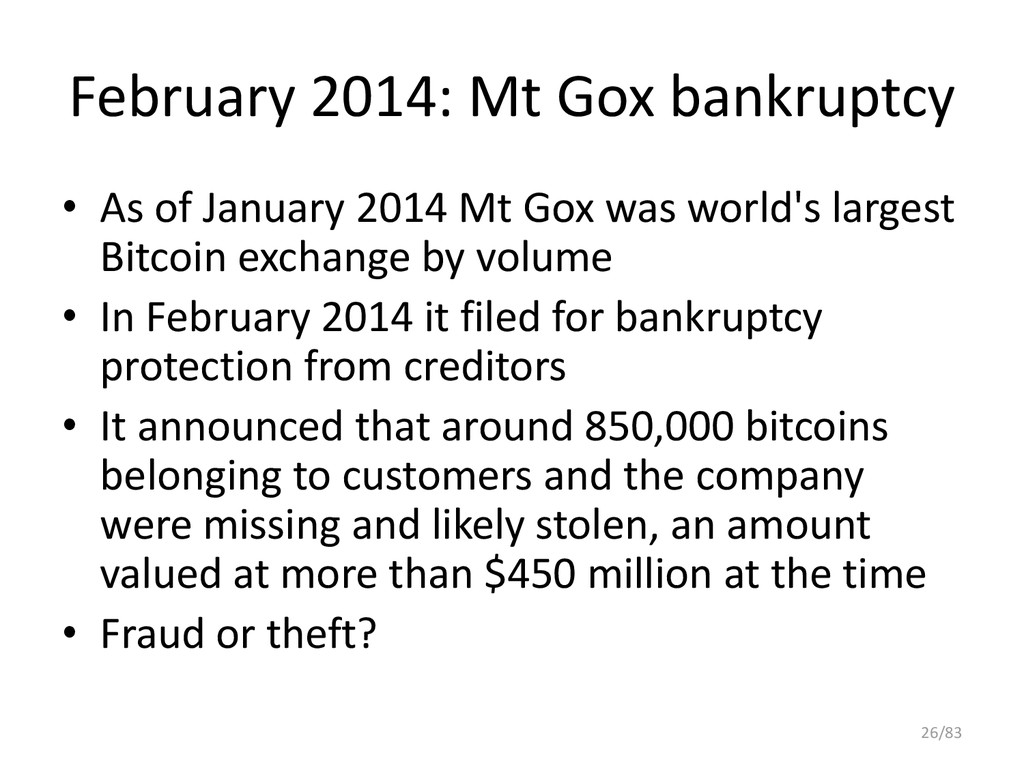

Mt Gox was world's largest Bitcoin exchange by volume • In February 2014 it filed for bankruptcy protection from creditors • It announced that around 850,000 bitcoins belonging to customers and the company were missing and likely stolen, an amount valued at more than $450 million at the time • Fraud or theft? 26/83

service • online users were able to buy illicit goodies using bitcoins, while browsing it anonymously and securely without potential traffic monitoring • launched in February 2011, shut down in October 2013 • Ross William Ulbricht, alleged to be the owner of Silk Road arrested in San Francisco • Many other black markets have filled in as successors 27/83

Just 5 years old • Without government or corporation backing • That can lost its main (China) market and its main exchanges in 3 months • Subjected to fraud or theft perpetrated at its main reference exchange • With such a bad reputation That could be still alive and kicking? 28/83

– Bitcoin is a payment innovation that's taking place outside the banking industry – It's not so easy to regulate Bitcoin because there's no central issuer or network operator. This is a decentralized, global [entity] • ECB (October 2012 report): – governments and central banks would face serious difficulties if they tried to control or ban any virtual currency scheme – there is no server that could be shut down if the authorities deemed it necessary 29/83

September 2014 • Sridhar Ramaswamy, head of Google Wallet We are working in the payments team to figure out how to incorporate bitcoin into our plans • Amazon: granted patent for the use of digital currencies as payment on cloud platforms (Amazon Web Services) 32/83

bitcoins? • Buy bitcoins using USD or EUR at one of many exchanges, e.g. Bitstamp, The Rock Trading, etc. • Use bitcoins to buy: – web services – software – hardware – gambling services – Narcotics, guns, credit card numbers, etc. – Topping the list, in terms of the number of transactions, is tipping and donations 33/83

to transfer a unique digital token • the token can be exchanged, but not duplicated • keeps records of each and every transaction forever • shared with peer-to-peer technology • everyone knows the transaction happened, nobody can challenge its legitimacy • the protocol is Bitcoin extra-legal tight regulation 35/83

as block chain documented transactions • A bitcoin wallet is a public address 1FEz167JCVgBvhJBahpzmrsTNewhiwgWVG • the public ledger certifies for everybody how many bitcoins are associated to the wallet http://blockexplorer.com/address/1FEz167JCVgBvhJBahpzmrsTNewhiwgWVG It is mine; you are REALLY encouraged to tip 37/83

public key does not provide direct information about the private key owner • All transactions are transparent to everybody’s inspection. • Perfect persistent public account history: the public ledger is forever • Tool little privacy for honest people, too much for criminals https://blockchain.info/ http://blockexplorer.com/ 38/83

• private (secret) key produce a digital signature • public key used by anyone to verify the signature • The bitcoin wallet address is the public key • The private key allows spending from the wallet 39/83

The sender’s private key signs the transaction: – transacted amount – receiver’s public key • Sender’s public key verifies that the transaction: – originated from sender’s private key – has not been modified – the amount is at sender’s public key disposal • The transaction is published to the public ledger • Everybody knows that the receiver’s public key has received the transacted amount 41/83

can spend them • Securing a wallet: private key safe storage • PC client: Bitcoin Core, Armory, Electrum • Web client: blockchain.info, greenaddress.it • Cold storage: never exposed to Internet, stored away 42/83

in blocks, sequentially chained, about one block every 10 minutes • The block chain is a history of transactions resilient to network attackers • The cryptographic link between blocks requires large amount of computing power, so the block chain cannot be altered without huge resources • Computing power is measured in hash/s, hash being the basic operation needed for validation 43/83

They provide the computing power for: – processing and validating transactions (avoiding double spending) – securing the network – synchronizing the nodes 45/83

of transactions. • The winner provides a proof-of-work and is rewarded with the issue of new bitcoins. • Seigniorage revenues subsidize the network, making transaction almost free 46/83

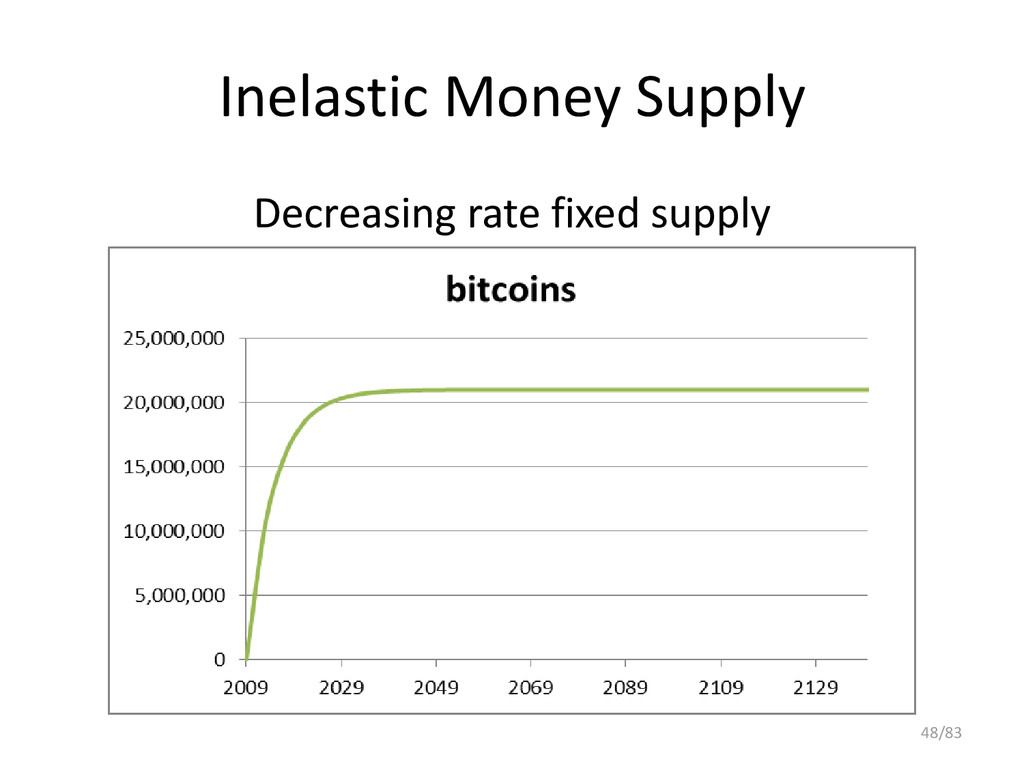

halving every 4Y • This is the only way new bitcoins are released • It is called mining because of its similarity with the progressive scarcity of gold extraction • digital cash supply free of discretionary intervention 47/83

that can be programmatically exchanged using smart contracts • Smart contracts are math (not legal) based contracts that do not need human interpretation or intervention to complete: the settlement is done by software. • Autonomous agents are software programs created for specific tasks: with Bitcoin they can now make and receive payments • Decentralized Autonomous Organizations 50/83

(car sharing) • Voting rights (liquid democracy) Distributed Autonomous Organizations: • Gambling online (no fees, no taxes) • Health insurance (without company costs) 51/83

• Put a hash value in the «comment» section of a (monetarily negligible) transaction • Hash being a fixed length string that uniquely identify an arbitrary length digital object (e.g. a txt or pdf file) • Existence of that digital object at the transaction time is proved on the block chain www.proofofexistence.com 52/83

into a gift economy • Enlarged relationship circle requires exchange economy • barter economy, coincidence of wants • trade economy, money as medium of exchange 54/83

Account Live cattle Diamonds Gold Fiat coins and notes Cryptocurrency • swappable • fungible • portable • divisible • recognizable • resistant to counterfeiting • reliably saved, stored, and retrieved • retain usefulness over time • non-perishable or with low preservation cost • relative worth unit of measure • stable value for stable price comparison • supply must be limited in some way 56/83

of every other good is measured • A good in itself: its value is governed by supply and demand • The price system measures the value of goods relative to the value of money • Good money should provide stable prices to best perform its role as unit of account 57/83

unit of money: money value decrease, price level increase • deflation hinders money’s unit of account role and encourages its hoarding. This can lead to perverse economic crisis. 58/83

authorities • institutionally designed to be independents • central bank’s main objective is to safeguard the value of the national currency • low and stable rate of inflation is the implicit or explicit goal 59/83

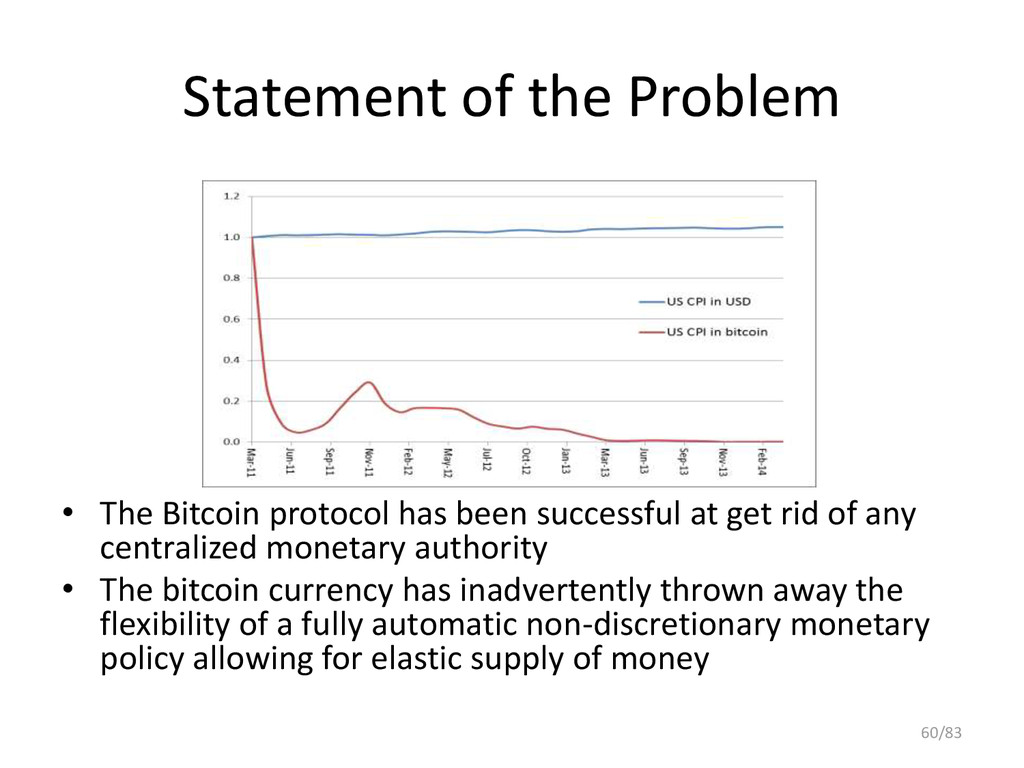

successful at get rid of any centralized monetary authority • The bitcoin currency has inadvertently thrown away the flexibility of a fully automatic non-discretionary monetary policy allowing for elastic supply of money 60/83

an almost uninterrupted story of debasements; history is largely a history of inflation engineered by governments for their gain • why government monopoly of the provision of money is regarded as indispensable? It deprived public of the opportunity to discover and use a better reliable money A Free-Market Monetary System Lecture delivered at the Gold and Monetary Conference, New Orleans, Nov. 1977 https://mises.org/daily/3204 Denationalisation of Money-The Argument Refined, Third Edition The Institute of Economics Affairs 1990 http://mises.org/books/denationalisation.pdf 62/83

Commercial banks issue their own money: – Keep the purchasing power constant – Competition between currencies Blessed will be the day when it will no longer be from the benevolence of the government that we expect good money but from the regard of the banks for their own interest 63/83

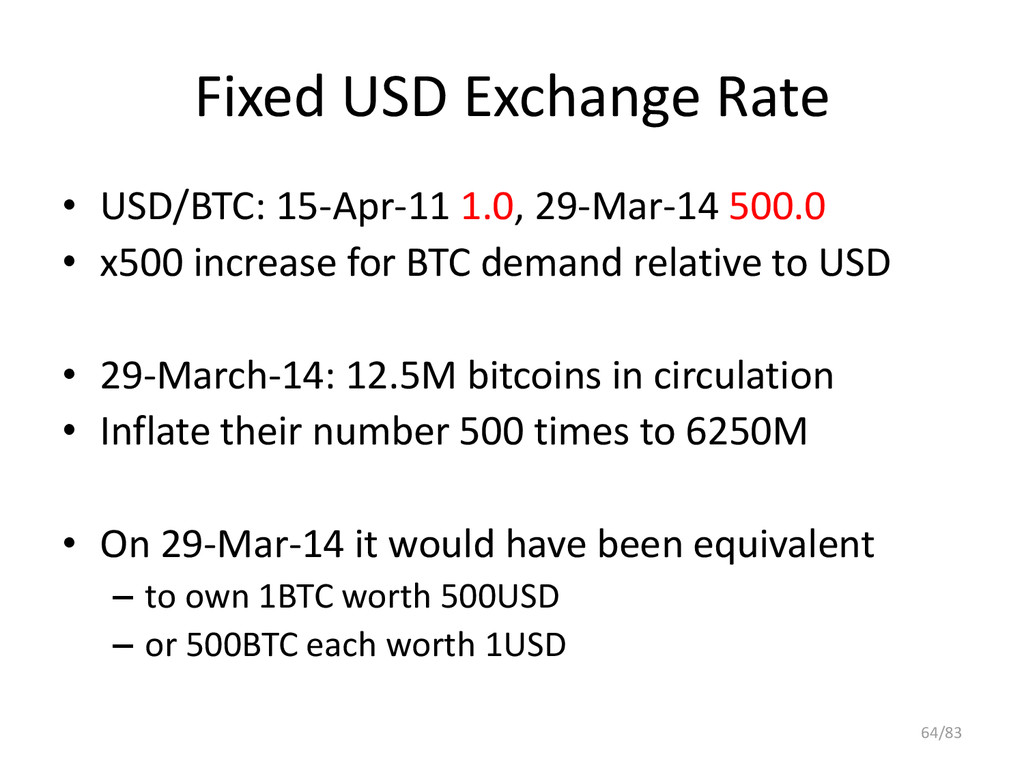

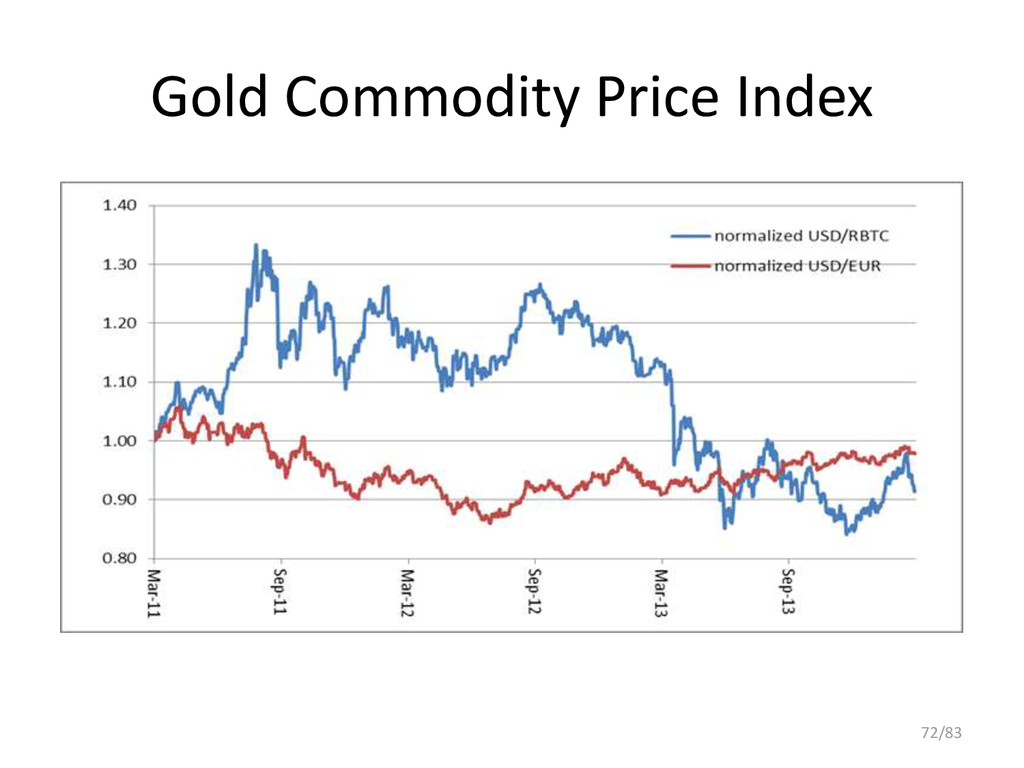

• x500 increase for BTC demand relative to USD • 29-March-14: 12.5M bitcoins in circulation • Inflate their number 500 times to 6250M • On 29-Mar-14 it would have been equivalent – to own 1BTC worth 500USD – or 500BTC each worth 1USD 64/83

investment asset leads to hoarding and limited transaction volume • Shield coin holders from the direct effects of monetary phases, restraining monetary policy’s costs and benefits to holders of seigniorage shares • Seigniorage shares are a participation in a distributed central bank: owners are entitled to seigniorage revenues in exchange for being subjected to the losses associated to coin price stability defence, obliged to validation task duties, and in charge of price index observation • Free coins from any speculative value, thus favoring money velocity and increasing the number of transactions 74/83

coins and shares. Block chain technology tracks ownership and transactions for both. • Coins are divisible, shares are not. Both can be used for transactions even if not fungible • Coins are minted as share dividends and distributed to shareholders • The right to validate transactions is reserved to shareholders, so here miner is a synonym of shareholder. • Miners are rewarded with the issuance of new shares. 75/83

in a distributed central bank • Owners are entitled to seigniorage revenues in exchange for being: – subjected to the losses associated to coin price stability defense – obliged to validation task duties – In charge of price index observation – network security, node synchronization, etc. • Shares are cryptographically identifiable, so those involved in double spending attempts are invalidated and “burned” away 76/83

pegged to a price index in order to make its value essentially constant at parity • Share price instead is free to float: expectations about expansionary monetary phases increment it, while contractionary phases depress it. 77/83

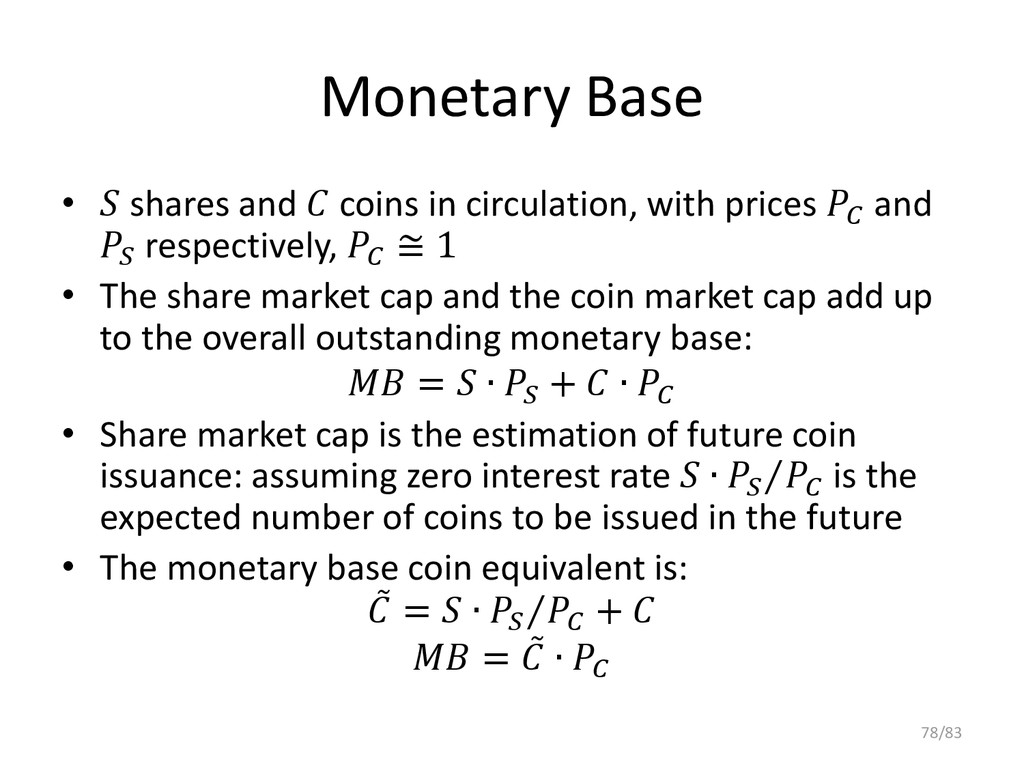

and respectively, ≅ 1 • The share market cap and the coin market cap add up to the overall outstanding monetary base: = ∙ + ∙ • Share market cap is the estimation of future coin issuance: assuming zero interest rate ∙ is the expected number of coins to be issued in the future • The monetary base coin equivalent is: = ∙ + = ∙ 78/83

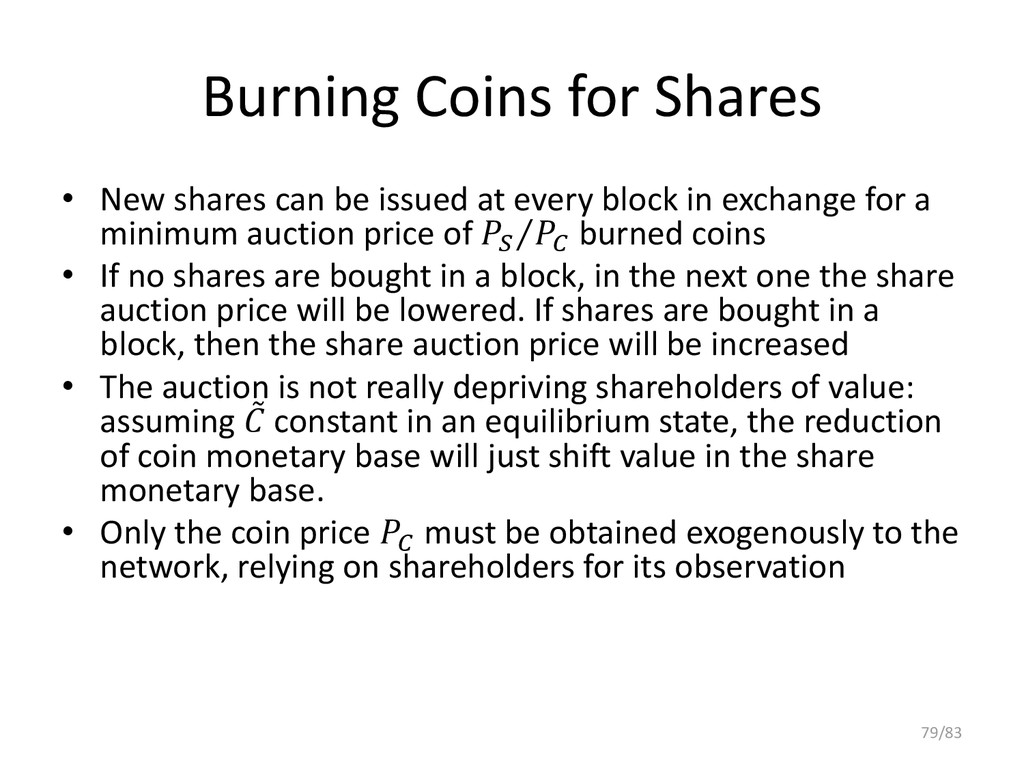

at every block in exchange for a minimum auction price of burned coins • If no shares are bought in a block, in the next one the share auction price will be lowered. If shares are bought in a block, then the share auction price will be increased • The auction is not really depriving shareholders of value: assuming constant in an equilibrium state, the reduction of coin monetary base will just shift value in the share monetary base. • Only the coin price must be obtained exogenously to the network, relying on shareholders for its observation 79/83

minted and paid as share dividends. • This limits the appreciation potential of , as for a given coin market cap value ∙ , the number of coins increases depressing . • As long as > 1 the share price is obviously non-negative > 0, as coins are expected to be paid as dividend. 80/83

on short-term: shares lose value • is always incorporating the expectation of future coins “stored” into the market share price, so as soon as decreases then less future coins are expected and will experience a pull to parity proportional to the share market cap loss. • the share defensive help is exhausted when approaches zero. • < 1 and > 0: price stability might be still defended if the market will consider further share devaluation enough to restore parity; • ≅ 0 and > 0: this is the realization of the bitcoin case, with shares being equivalent to bitcoins • < 1 and ≅ 0: price stability cannot be preserved unless coins are burned; • ≅ 0 and ≅ 0: the cryptomoney is dead 81/83

1977), Denationalisation of Money - The Argument Refined, The Institute of Economic Affairs, mises.org/books/denationalisation.pdf • Dowd, K. (2014), New Private Monies: A Bit- Part Player?, http://www.iea.org.uk/publications/research/ new-private-monies-a-bit-part-player 82/83

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Favorable Opinions • Ben Bernanke: [the virtual currency] may hold](https://files.speakerdeck.com/presentations/9e096d905d7501321d7846edf37ef1d2/slide_19.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}