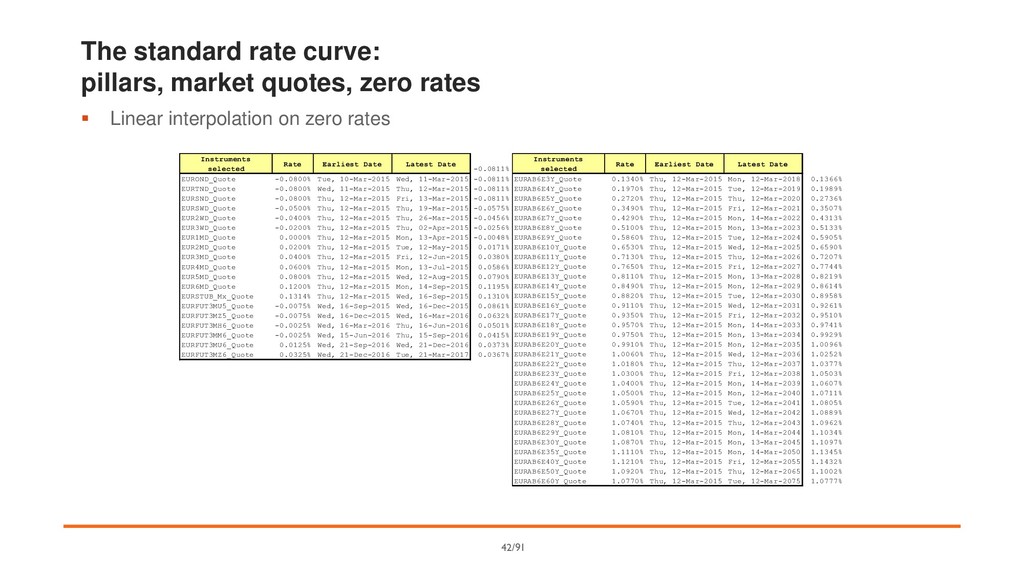

Linear interpolation on zero rates Instruments selected Rate Earliest Date Latest Date EURAB6E3Y_Quote 0.1340% Thu, 12-Mar-2015 Mon, 12-Mar-2018 0.1366% EURAB6E4Y_Quote 0.1970% Thu, 12-Mar-2015 Tue, 12-Mar-2019 0.1989% EURAB6E5Y_Quote 0.2720% Thu, 12-Mar-2015 Thu, 12-Mar-2020 0.2736% EURAB6E6Y_Quote 0.3490% Thu, 12-Mar-2015 Fri, 12-Mar-2021 0.3507% EURAB6E7Y_Quote 0.4290% Thu, 12-Mar-2015 Mon, 14-Mar-2022 0.4313% EURAB6E8Y_Quote 0.5100% Thu, 12-Mar-2015 Mon, 13-Mar-2023 0.5133% EURAB6E9Y_Quote 0.5860% Thu, 12-Mar-2015 Tue, 12-Mar-2024 0.5905% EURAB6E10Y_Quote 0.6530% Thu, 12-Mar-2015 Wed, 12-Mar-2025 0.6590% EURAB6E11Y_Quote 0.7130% Thu, 12-Mar-2015 Thu, 12-Mar-2026 0.7207% EURAB6E12Y_Quote 0.7650% Thu, 12-Mar-2015 Fri, 12-Mar-2027 0.7744% EURAB6E13Y_Quote 0.8110% Thu, 12-Mar-2015 Mon, 13-Mar-2028 0.8219% EURAB6E14Y_Quote 0.8490% Thu, 12-Mar-2015 Mon, 12-Mar-2029 0.8614% EURAB6E15Y_Quote 0.8820% Thu, 12-Mar-2015 Tue, 12-Mar-2030 0.8958% EURAB6E16Y_Quote 0.9110% Thu, 12-Mar-2015 Wed, 12-Mar-2031 0.9261% EURAB6E17Y_Quote 0.9350% Thu, 12-Mar-2015 Fri, 12-Mar-2032 0.9510% EURAB6E18Y_Quote 0.9570% Thu, 12-Mar-2015 Mon, 14-Mar-2033 0.9741% EURAB6E19Y_Quote 0.9750% Thu, 12-Mar-2015 Mon, 13-Mar-2034 0.9929% EURAB6E20Y_Quote 0.9910% Thu, 12-Mar-2015 Mon, 12-Mar-2035 1.0096% EURAB6E21Y_Quote 1.0060% Thu, 12-Mar-2015 Wed, 12-Mar-2036 1.0252% EURAB6E22Y_Quote 1.0180% Thu, 12-Mar-2015 Thu, 12-Mar-2037 1.0377% EURAB6E23Y_Quote 1.0300% Thu, 12-Mar-2015 Fri, 12-Mar-2038 1.0503% EURAB6E24Y_Quote 1.0400% Thu, 12-Mar-2015 Mon, 14-Mar-2039 1.0607% EURAB6E25Y_Quote 1.0500% Thu, 12-Mar-2015 Mon, 12-Mar-2040 1.0711% EURAB6E26Y_Quote 1.0590% Thu, 12-Mar-2015 Tue, 12-Mar-2041 1.0805% EURAB6E27Y_Quote 1.0670% Thu, 12-Mar-2015 Wed, 12-Mar-2042 1.0889% EURAB6E28Y_Quote 1.0740% Thu, 12-Mar-2015 Thu, 12-Mar-2043 1.0962% EURAB6E29Y_Quote 1.0810% Thu, 12-Mar-2015 Mon, 14-Mar-2044 1.1034% EURAB6E30Y_Quote 1.0870% Thu, 12-Mar-2015 Mon, 13-Mar-2045 1.1097% EURAB6E35Y_Quote 1.1110% Thu, 12-Mar-2015 Mon, 14-Mar-2050 1.1345% EURAB6E40Y_Quote 1.1210% Thu, 12-Mar-2015 Fri, 12-Mar-2055 1.1432% EURAB6E50Y_Quote 1.0920% Thu, 12-Mar-2015 Thu, 12-Mar-2065 1.1002% EURAB6E60Y_Quote 1.0770% Thu, 12-Mar-2015 Tue, 12-Mar-2075 1.0777% Instruments selected Rate Earliest Date Latest Date -0.0811% EUROND_Quote -0.0800% Tue, 10-Mar-2015 Wed, 11-Mar-2015 -0.0811% EURTND_Quote -0.0800% Wed, 11-Mar-2015 Thu, 12-Mar-2015 -0.0811% EURSND_Quote -0.0800% Thu, 12-Mar-2015 Fri, 13-Mar-2015 -0.0811% EURSWD_Quote -0.0500% Thu, 12-Mar-2015 Thu, 19-Mar-2015 -0.0575% EUR2WD_Quote -0.0400% Thu, 12-Mar-2015 Thu, 26-Mar-2015 -0.0456% EUR3WD_Quote -0.0200% Thu, 12-Mar-2015 Thu, 02-Apr-2015 -0.0256% EUR1MD_Quote 0.0000% Thu, 12-Mar-2015 Mon, 13-Apr-2015 -0.0048% EUR2MD_Quote 0.0200% Thu, 12-Mar-2015 Tue, 12-May-2015 0.0171% EUR3MD_Quote 0.0400% Thu, 12-Mar-2015 Fri, 12-Jun-2015 0.0380% EUR4MD_Quote 0.0600% Thu, 12-Mar-2015 Mon, 13-Jul-2015 0.0586% EUR5MD_Quote 0.0800% Thu, 12-Mar-2015 Wed, 12-Aug-2015 0.0790% EUR6MD_Quote 0.1200% Thu, 12-Mar-2015 Mon, 14-Sep-2015 0.1195% EURSTUB_Mx_Quote 0.1314% Thu, 12-Mar-2015 Wed, 16-Sep-2015 0.1310% EURFUT3MU5_Quote -0.0075% Wed, 16-Sep-2015 Wed, 16-Dec-2015 0.0861% EURFUT3MZ5_Quote -0.0075% Wed, 16-Dec-2015 Wed, 16-Mar-2016 0.0632% EURFUT3MH6_Quote -0.0025% Wed, 16-Mar-2016 Thu, 16-Jun-2016 0.0501% EURFUT3MM6_Quote -0.0025% Wed, 15-Jun-2016 Thu, 15-Sep-2016 0.0415% EURFUT3MU6_Quote 0.0125% Wed, 21-Sep-2016 Wed, 21-Dec-2016 0.0373% EURFUT3MZ6_Quote 0.0325% Wed, 21-Dec-2016 Tue, 21-Mar-2017 0.0367% 42/91

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}