Concepts, LLC. Caravel helps global investment companies transition from brokerage to advisory client relationships. • Prior to Caravel, Michael served as Chairman and founding partner of RiverFront Investment Group, an $8 billion global advisory firm. • Before the launch of RiverFront, Michael served as the Chief Investment Officer for Wachovia Securities, the third largest brokerage and investment advisory firm in the US. • Michael is a featured guest on many financial news networks including CNBC, Fox Business, and Bloomberg and has been inducted into Research Magazine’s ETF Hall of Fame. • Michael graduated from the College of William & Mary and earned an MBA from the Wharton School at the University of Pennsylvania.

sell investment products. • Advisors charge a portfolio management fee. • Advisors are held to a fiduciary standard. • An advisor’s value depends upon the quality of the advisory process.

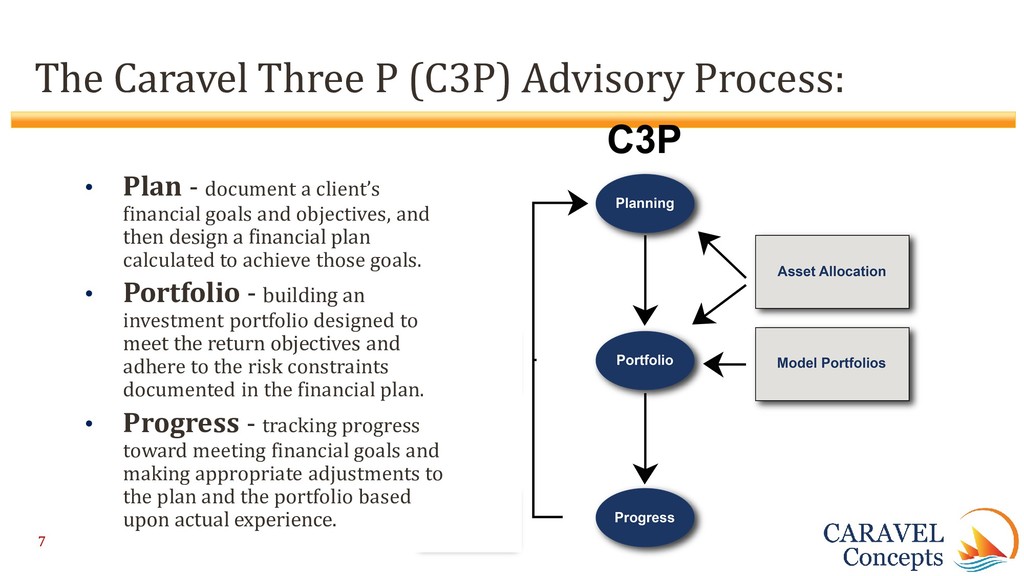

- document a client’s financial goals and objectives, and then design a financial plan calculated to achieve those goals. • Portfolio - building an investment portfolio designed to meet the return objectives and adhere to the risk constraints documented in the financial plan. • Progress - tracking progress toward meeting financial goals and making appropriate adjustments to the plan and the portfolio based upon actual experience.

better for the client. • Declining commissions & escalating regulatory pressure • Advisory firms make more money and trade at a higher valuations than brokerage firms • Advisors make a lot more money than brokers. • Advice is just a better business.

at zero. • Advisory fees start at last month’s level plus or minus market moves. • Commissions can drop precipitously in a bear market. • Advice fees decline only to the extent the market drops. • Commissions can stay depressed until confidence returns. • Advisory fees recover with the market.

effort to generate - there is only so much time in a day. • Clients won’t act on every recommendation, so time must be devoted to analyzing disparate portfolio strategies. • Advisory fees accrue automatically and discretionary advice provides for “mass customized” portfolio solutions. • Advisors can add clients and assets without adding costs.

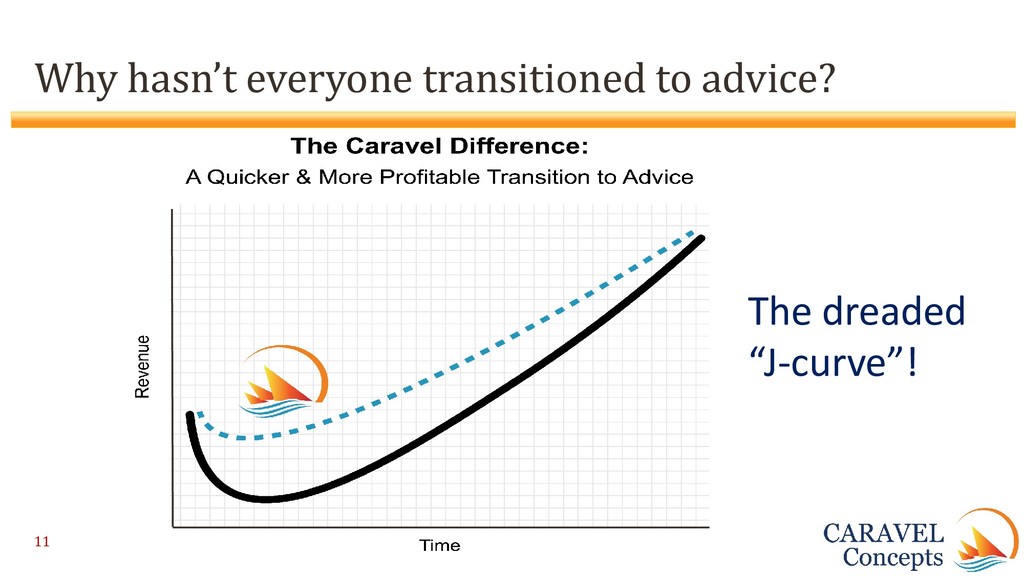

• Management commitment. • Easy to use advisory process software. • Fully built out advisory portfolio solutions, including ETFs based portfolios. • Appropriate compensation and incentive plans • Education and training.

for the client. • Solves regulatory concerns • The firm makes more money • Sales professionals make more money • The firms who lead the way reap most of the profits.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}