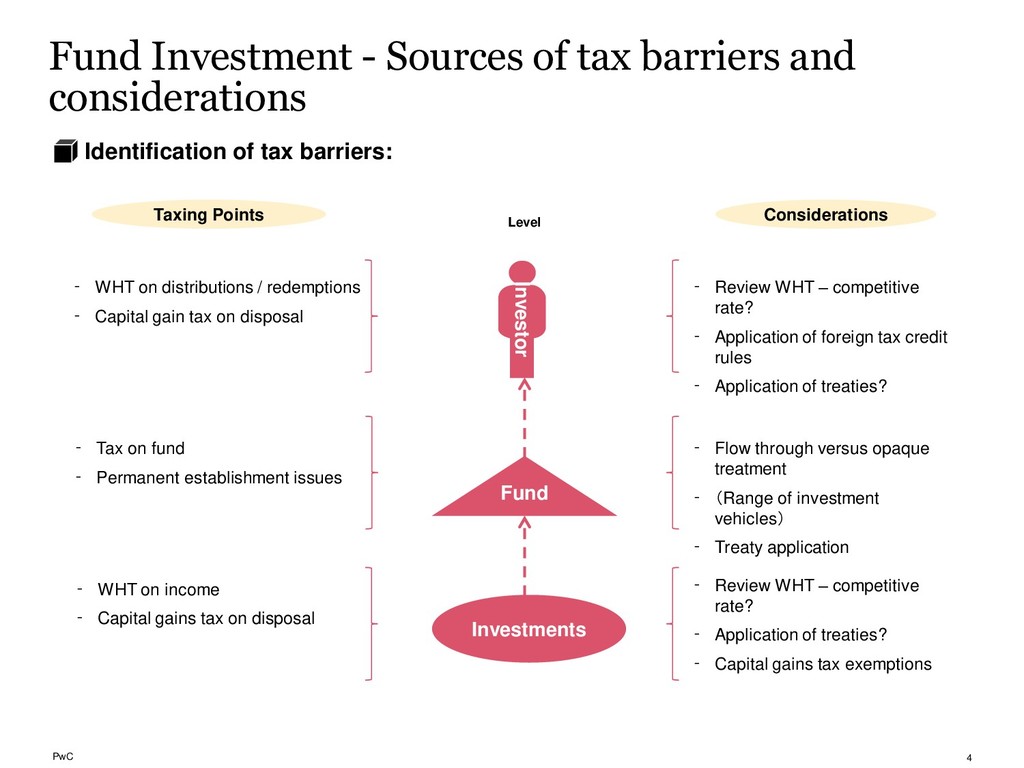

Identification of tax barriers: Taxing Points Considerations Fund Investor Investments ⁃ WHT on distributions / redemptions ⁃ Capital gain tax on disposal ⁃ Tax on fund ⁃ Permanent establishment issues ⁃ WHT on income ⁃ Capital gains tax on disposal ⁃ Review WHT – competitive rate? ⁃ Application of foreign tax credit rules ⁃ Application of treaties? ⁃ Flow through versus opaque treatment ⁃ (Range of investment vehicles) ⁃ Treaty application ⁃ Review WHT – competitive rate? ⁃ Application of treaties? ⁃ Capital gains tax exemptions Level 4

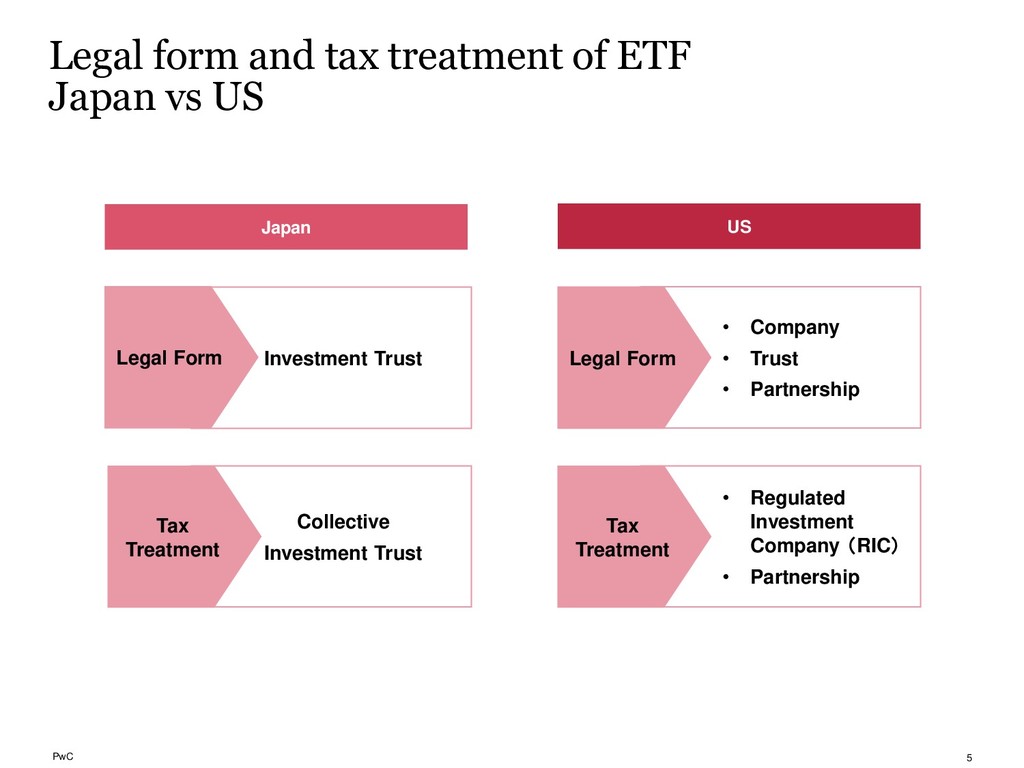

US US Japan Collective Investment Trust Tax Treatment • Regulated Investment Company (RIC) • Partnership Tax Treatment Investment Trust Legal Form • Company • Trust • Partnership Legal Form 5

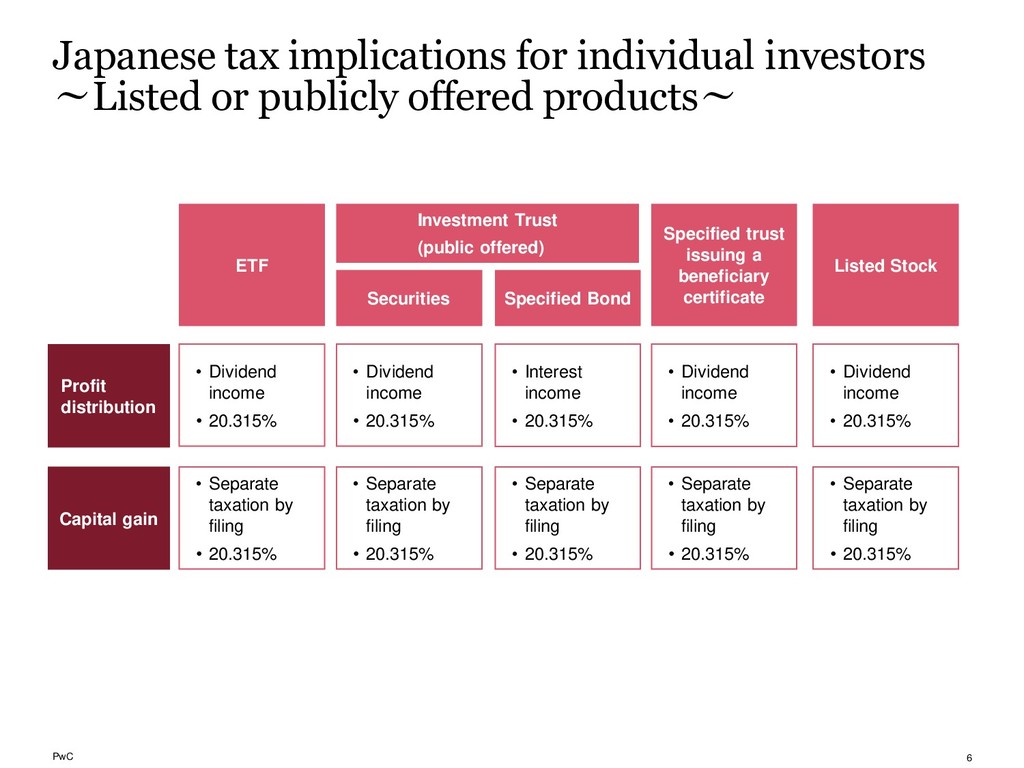

offered products~ Profit distribution Capital gain Investment Trust (public offered) • Dividend income • 20.315% • Separate taxation by filing • 20.315% Specified trust issuing a beneficiary certificate • Dividend income • 20.315% • Separate taxation by filing • 20.315% ETF • Dividend income • 20.315% • Separate taxation by filing • 20.315% Listed Stock • Dividend income • 20.315% • Separate taxation by filing • 20.315% Securities Specified Bond • Interest income • 20.315% • Separate taxation by filing • 20.315% 6

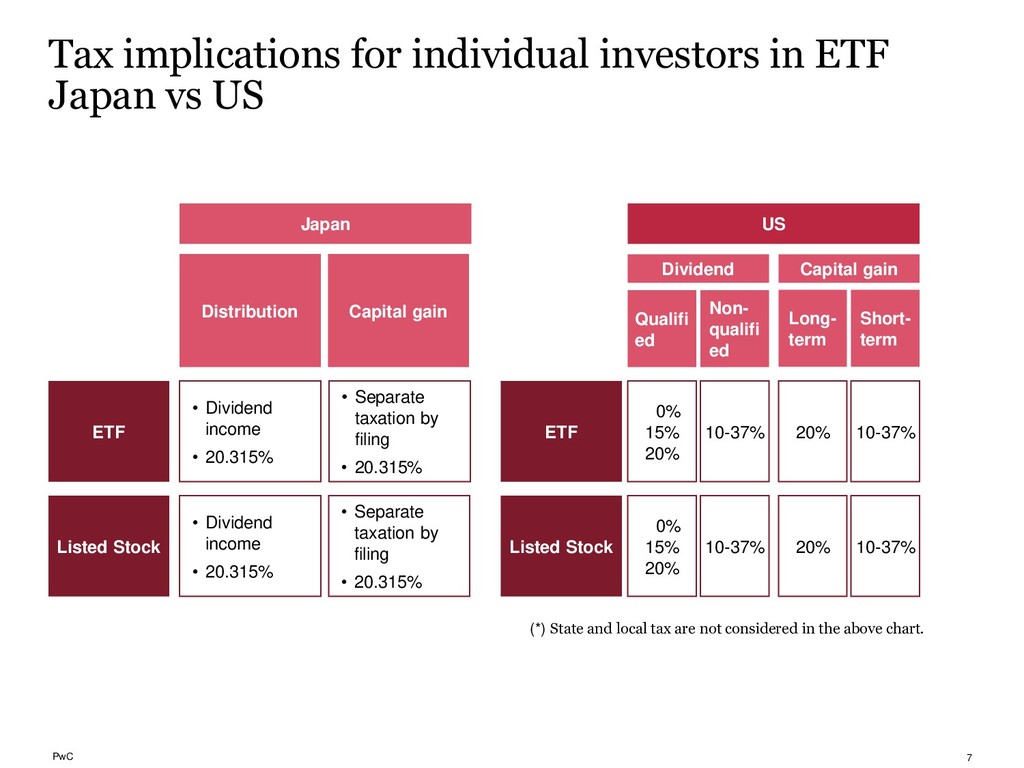

US ETF • Dividend income • 20.315% 20% 10-37% Distribution Capital gain • Separate taxation by filing • 20.315% Dividend ETF Long- term Short- term Capital gain (*) State and local tax are not considered in the above chart. 0% 15% 20% 10-37% Qualifi ed Non- qualifi ed Listed Stock • Dividend income • 20.315% • Separate taxation by filing • 20.315% 20% 10-37% Listed Stock 0% 15% 20% 10-37% US Japan 7

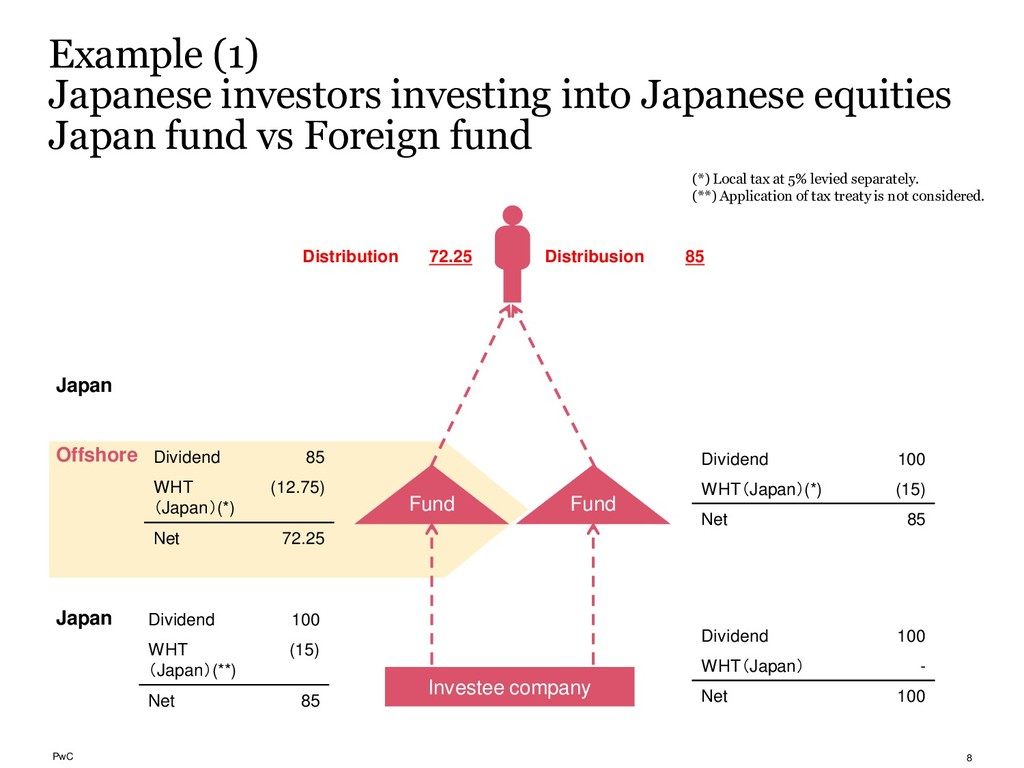

fund vs Foreign fund Investee company Fund Offshore Japan Dividend 100 WHT (Japan)(**) (15) Net 85 Dividend 85 WHT (Japan)(*) (12.75) Net 72.25 Dividend 100 WHT(Japan)(*) (15) Net 85 (*) Local tax at 5% levied separately. (**) Application of tax treaty is not considered. Distribution 72.25 Distribusion 85 Dividend 100 WHT(Japan) - Net 100 Fund Japan 8

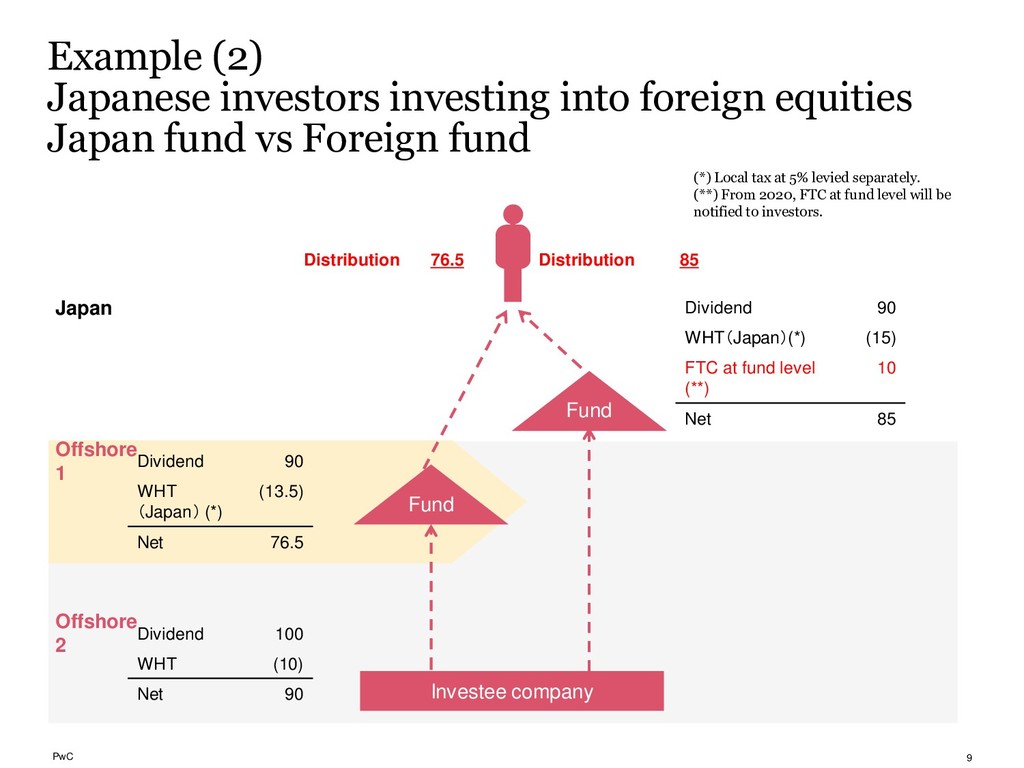

fund vs Foreign fund Investee company Dividend 100 WHT (10) Net 90 Dividend 90 WHT (Japan) (*) (13.5) Net 76.5 Dividend 90 WHT(Japan)(*) (15) FTC at fund level (**) 10 Net 85 (*) Local tax at 5% levied separately. (**) From 2020, FTC at fund level will be notified to investors. Distribution 76.5 Distribution 85 ファンド Fund Fund Offshore 1 Japan Offshore 2 9

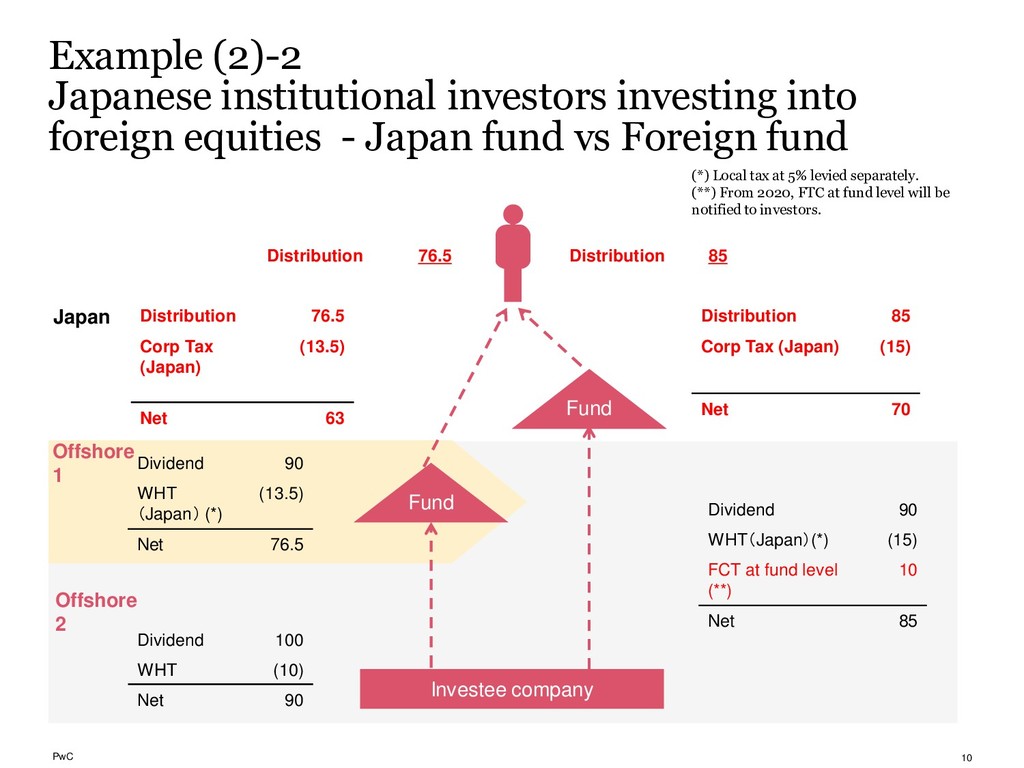

- Japan fund vs Foreign fund Dividend 100 WHT (10) Net 90 Dividend 90 WHT (Japan) (*) (13.5) Net 76.5 Dividend 90 WHT(Japan)(*) (15) FCT at fund level (**) 10 Net 85 (*) Local tax at 5% levied separately. (**) From 2020, FTC at fund level will be notified to investors. Distribution 76.5 Distribution 85 ファンド Distribution 85 Corp Tax (Japan) (15) Net 70 Distribution 76.5 Corp Tax (Japan) (13.5) Net 63 Offshore 1 Japan Offshore 2 Investee company Fund Fund 10

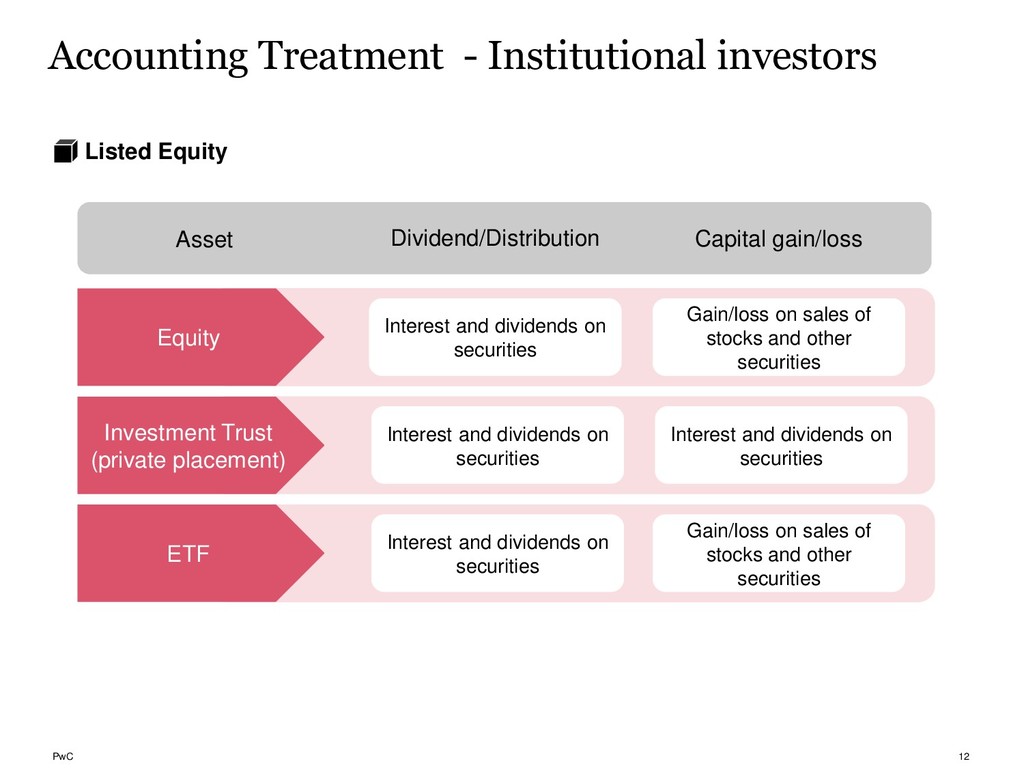

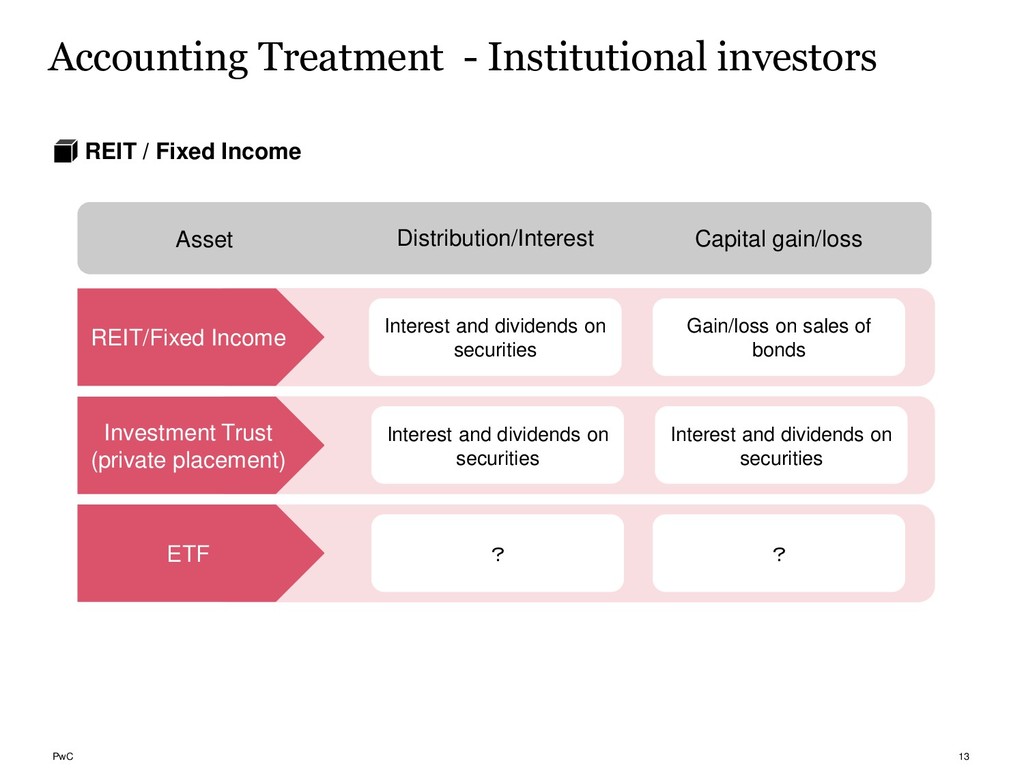

dividends on securities Gain/loss on sales of stocks and other securities Equity Interest and dividends on securities Interest and dividends on securities Investment Trust (private placement) Interest and dividends on securities Gain/loss on sales of stocks and other securities ETF Dividend/Distribution Capital gain/loss Asset 12

bonds REIT/Fixed Income Interest and dividends on securities Interest and dividends on securities Investment Trust (private placement) ? ? ETF Distribution/Interest Capital gain/loss Asset Accounting Treatment - Institutional investors REIT / Fixed Income 13

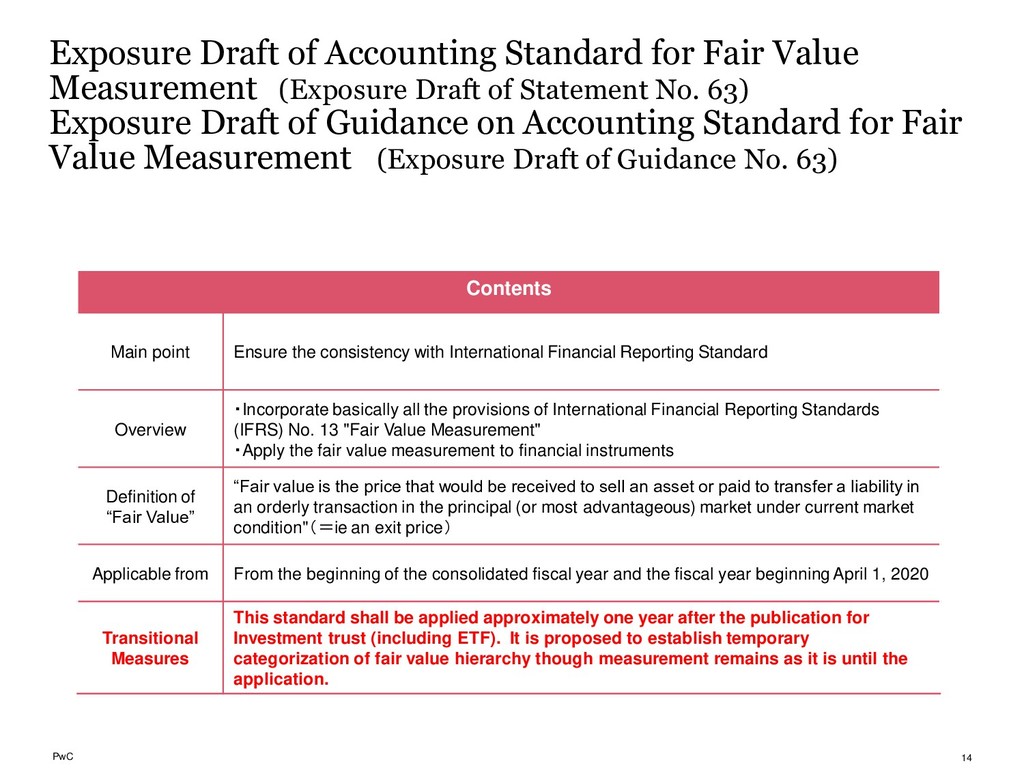

(Exposure Draft of Statement No. 63) Exposure Draft of Guidance on Accounting Standard for Fair Value Measurement (Exposure Draft of Guidance No. 63) 14 Contents Main point Ensure the consistency with International Financial Reporting Standard Overview ・Incorporate basically all the provisions of International Financial Reporting Standards (IFRS) No. 13 "Fair Value Measurement" ・Apply the fair value measurement to financial instruments Definition of “Fair Value” “Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market under current market condition"(=ie an exit price) Applicable from From the beginning of the consolidated fiscal year and the fiscal year beginning April 1, 2020 Transitional Measures This standard shall be applied approximately one year after the publication for Investment trust (including ETF). It is proposed to establish temporary categorization of fair value hierarchy though measurement remains as it is until the application.

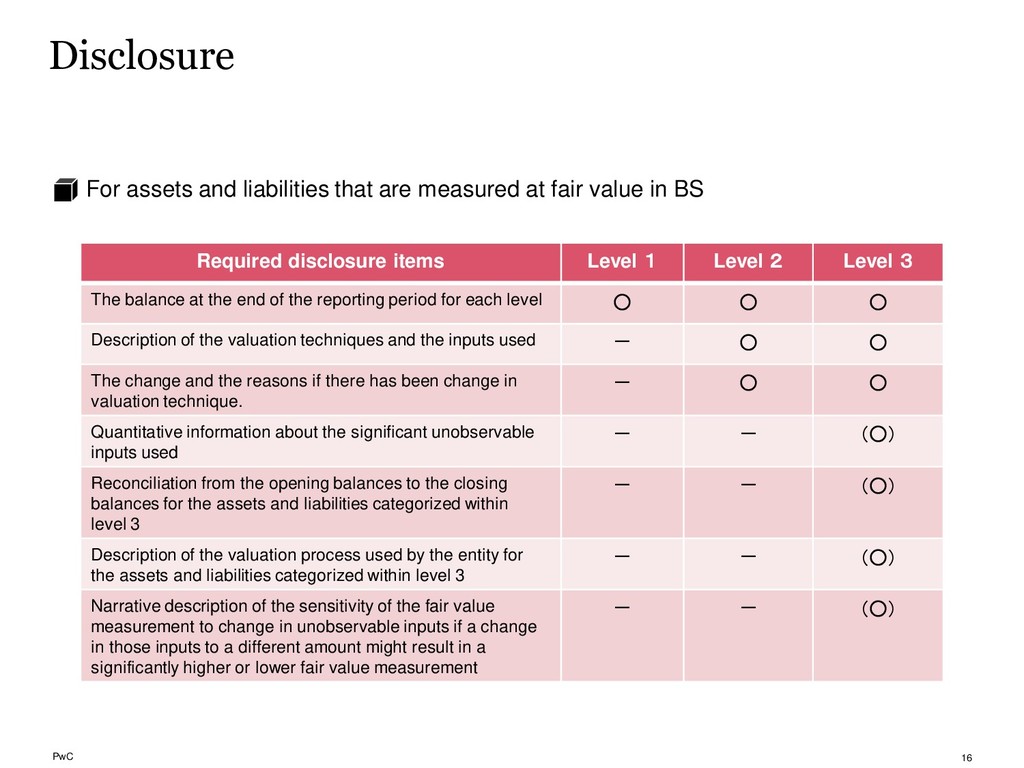

value in BS 16 Disclosure Required disclosure items Level 1 Level 2 Level 3 The balance at the end of the reporting period for each level ◦ ◦ ◦ Description of the valuation techniques and the inputs used - ◦ ◦ The change and the reasons if there has been change in valuation technique. - ◦ ◦ Quantitative information about the significant unobservable inputs used - - (◦) Reconciliation from the opening balances to the closing balances for the assets and liabilities categorized within level 3 - - (◦) Description of the valuation process used by the entity for the assets and liabilities categorized within level 3 - - (◦) Narrative description of the sensitivity of the fair value measurement to change in unobservable inputs if a change in those inputs to a different amount might result in a significantly higher or lower fair value measurement - - (◦)

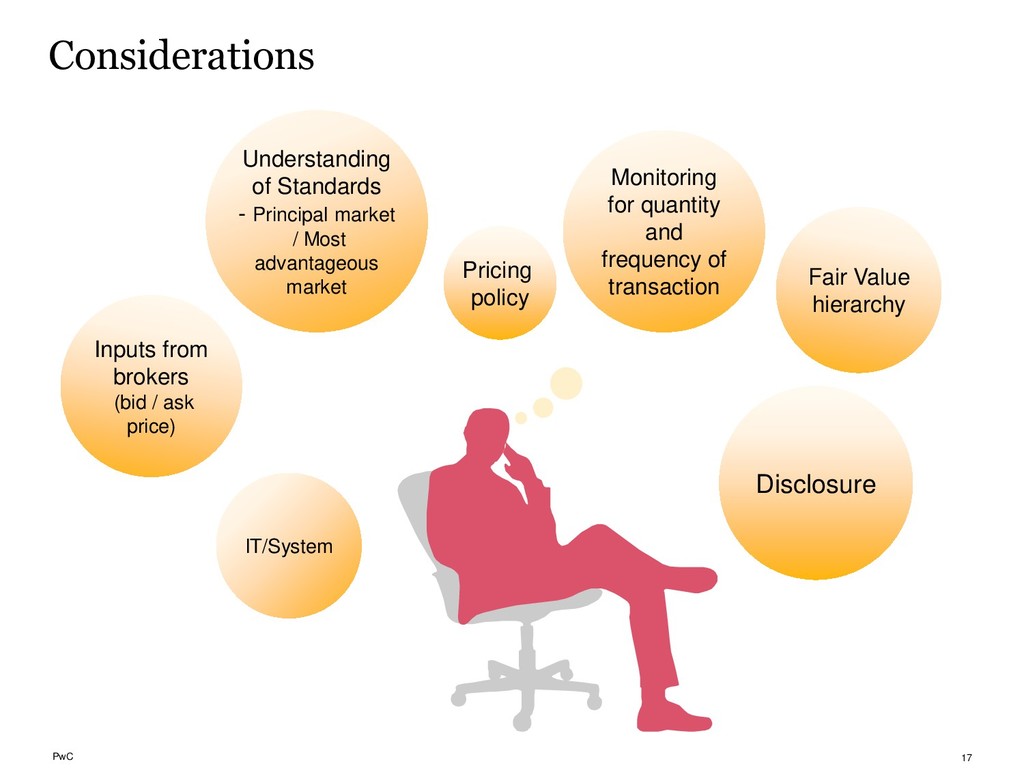

Most advantageous market Disclosure IT/System Inputs from brokers (bid / ask price) Monitoring for quantity and frequency of transaction Pricing policy Fair Value hierarchy

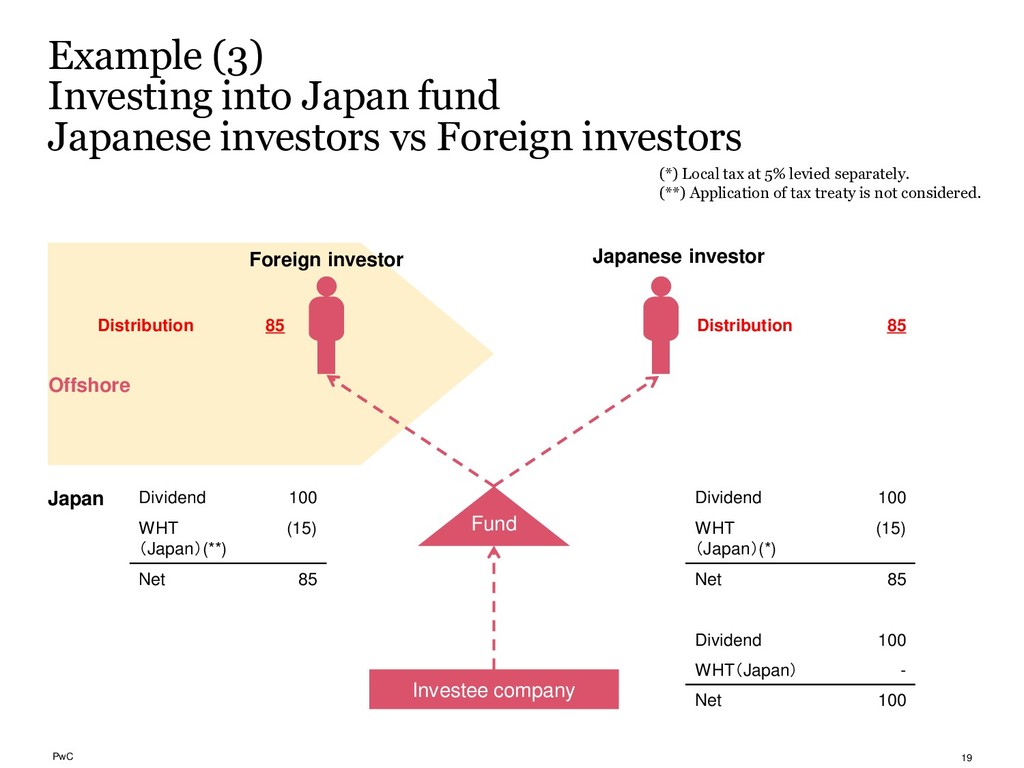

Foreign investors Fund Investee company Dividend 100 WHT (Japan)(**) (15) Net 85 Dividend 100 WHT (Japan)(*) (15) Net 85 Distribution 85 Distribution 85 Dividend 100 WHT(Japan) - Net 100 Foreign investor Japanese investor (*) Local tax at 5% levied separately. (**) Application of tax treaty is not considered. Offshore Japan 19

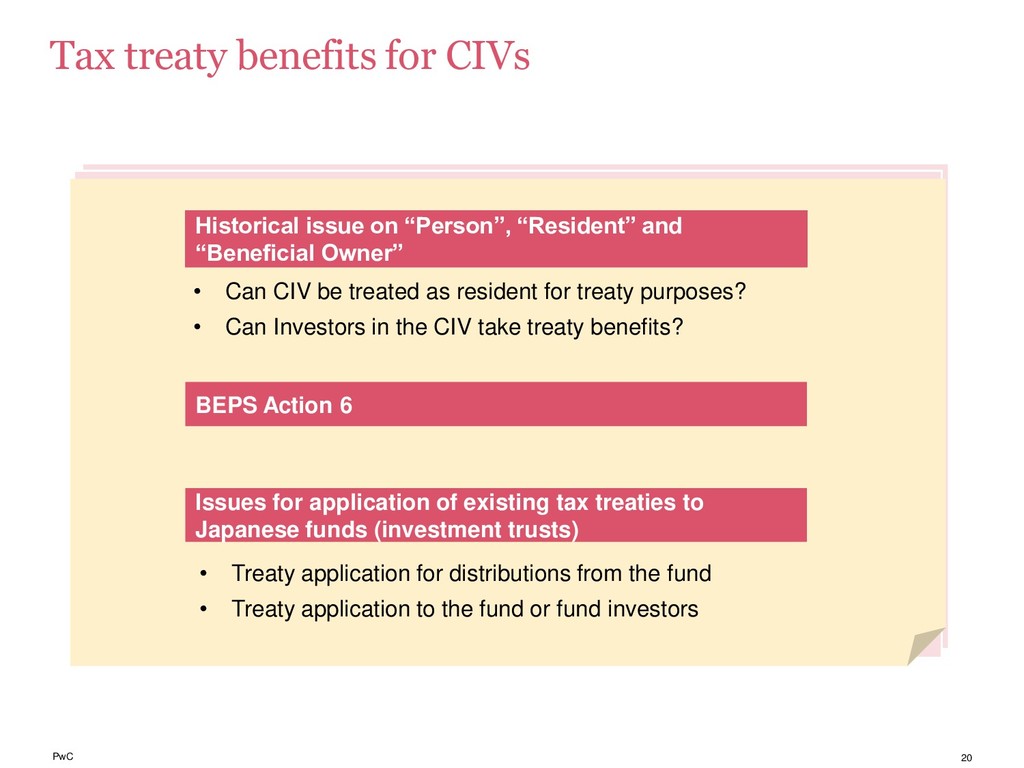

“Resident” and “Beneficial Owner” • Can CIV be treated as resident for treaty purposes? • Can Investors in the CIV take treaty benefits? BEPS Action 6 Issues for application of existing tax treaties to Japanese funds (investment trusts) • Treaty application for distributions from the fund • Treaty application to the fund or fund investors 20

2019 PricewaterhouseCoopers Aarata LLC. All rights reserved. PwC refers to the PwC Network member firms in Japan and/or their specified subsidiaries, and may sometimes refer to the PwC Network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. Contacts PricewaterhouseCoopers Aarata LLC Dai Tsujita Asset & Wealth Management, Partner Tel: 090-6492-5789 E-mail: [email protected] PwC Tax Japan Akemi Kito Certified Public Accountant, Financial Services, Partner Tel: 03-5251-2461 E-mail: [email protected] 21

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![PwC 辻田 大 第三金融部長(資産運用) パートナー Tel: 090-6492-5789 E-mail: [email protected] ©](https://files.speakerdeck.com/presentations/d55a1ccc73b349c2bac0a33d060ffc29/slide_21.jpg){kind=link}