Optimizing the customer on-boarding ecosystem - Imelda Newton, Veda

Imelda Newton is the General Manager of Fraud and Identity at Veda. 9th Annual Innovators Conference – presentation day 2, March 8th @ the Palazzo Versace, Gold Coast, Australia

experience, - improve operational efficiency, - minimize the risk of fraud, - meet compliance obligations Imelda Newton GM Fraud and Identity Solutions February 2013 Veda - Commercial in Confidence Copyright 2013

customer on-boarding 2 Lost customers due to quality of experience Time consuming Adding to operational costs and paper trail Expensive Mandatory requirement that is audited Compliance driven Not repeatable, open to interpretation and potentially fraud Subjective process Who is this prospect and can I trust them? Veda - Commercial in Confidence Copyright 2013

Customer satisfaction Growth of revenue Increase market share Occurrence of fraud Brand image Meet compliance requirements 3 Who are they? How do they behave? Veda - Commercial in Confidence Copyright 2013

insights company. Veda accumulates, transforms and connects data in order to provide our customers with great insights. We have access to a diverse range of systems and data points that provide us with quality information and scale. 4 Veda - Commercial in Confidence Copyright 2013

bureau and related service in Australia and New Zealand holding information on 19.7 million credit active people and 5.5 million businesses. • Every day we report on the credit status of 100,000 people and businesses applying for credit on both sides of the Tasman. • Over 13,000 Corporate customers and 600,000 Consumer customers in Australia and New Zealand. • 100% Australian owned Company. • Thought leadership and innovation with expansion into business lines including Fraud & Electronic Verification, Automotive bureau, and Marketing Services. Veda - Commercial in Confidence Copyright 2013

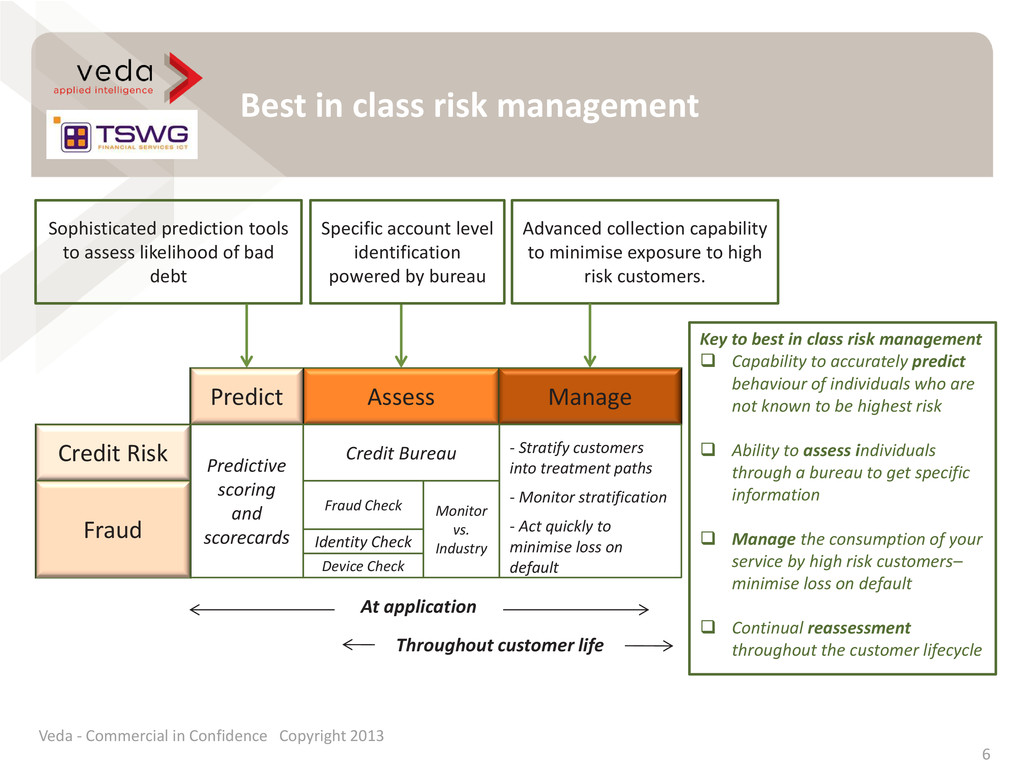

Predict Manage Credit Bureau Predictive scoring and scorecards - Stratify customers into treatment paths - Monitor stratification - Act quickly to minimise loss on default Specific account level identification powered by bureau Sophisticated prediction tools to assess likelihood of bad debt Advanced collection capability to minimise exposure to high risk customers. At application Key to best in class risk management Capability to accurately predict behaviour of individuals who are not known to be highest risk Ability to assess individuals through a bureau to get specific information Manage the consumption of your service by high risk customers– minimise loss on default Continual reassessment throughout the customer lifecycle Fraud Check Identity Check Device Check Monitor vs. Industry Throughout customer life Veda - Commercial in Confidence Copyright 2013

want to do business with you ….. 7 Knowing more about who is coming in via the on-line channel Understanding the exposure to fraud Industry issues with verifying Identities and avoiding losses to fraud Mapping a real life identity with the person presenting it Assess Manage At application Throughout customer life At application Veda - Commercial in Confidence Copyright 2013

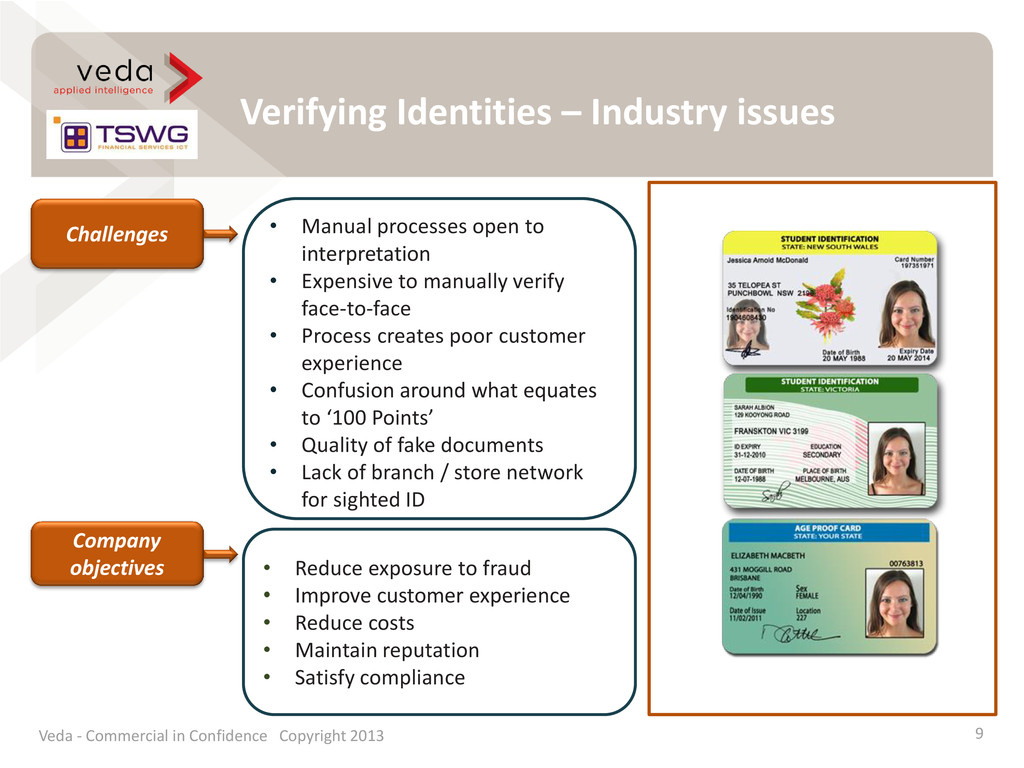

to interpretation • Expensive to manually verify face-to-face • Process creates poor customer experience • Confusion around what equates to ‘100 Points’ • Quality of fake documents • Lack of branch / store network for sighted ID Company objectives • Reduce exposure to fraud • Improve customer experience • Reduce costs • Maintain reputation • Satisfy compliance 9 Veda - Commercial in Confidence Copyright 2013

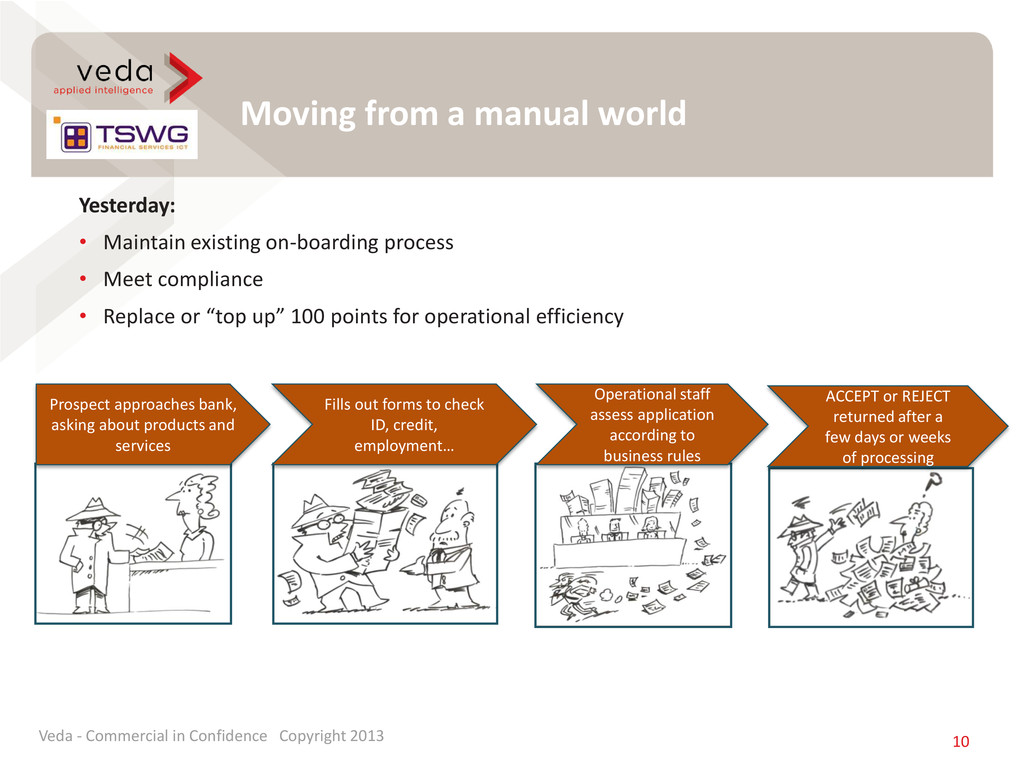

• Replace or “top up” 100 points for operational efficiency Moving from a manual world Prospect approaches bank, asking about products and services Fills out forms to check ID, credit, employment… Operational staff assess application according to business rules ACCEPT or REJECT returned after a few days or weeks of processing Veda - Commercial in Confidence Copyright 2013

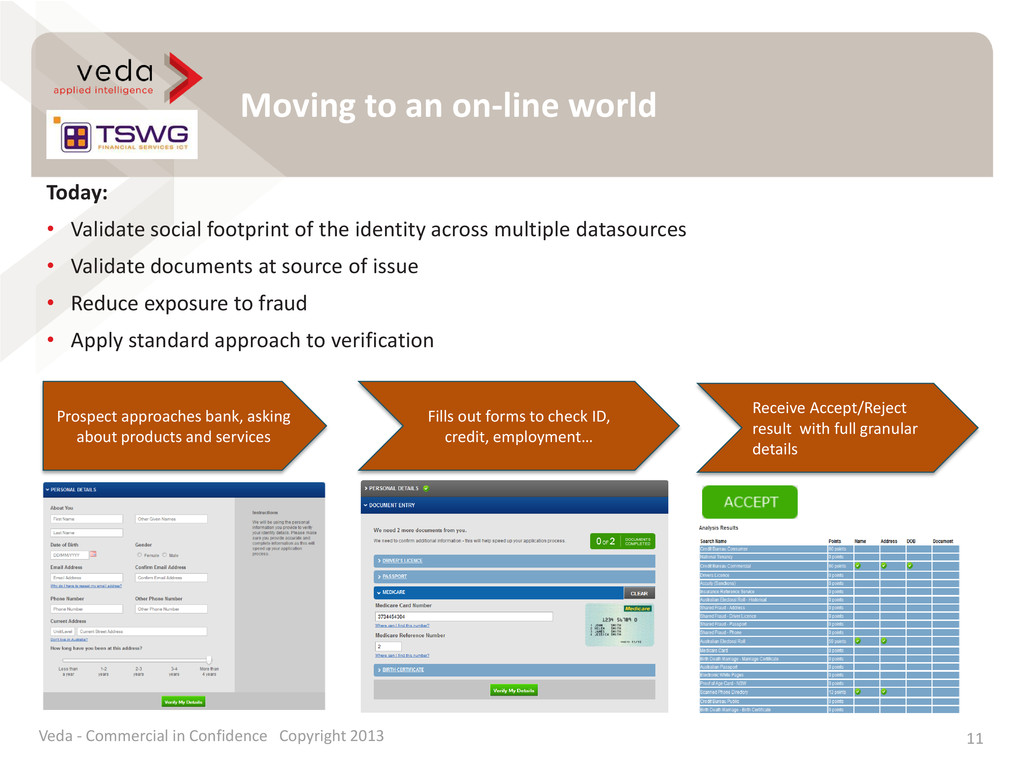

footprint of the identity across multiple datasources • Validate documents at source of issue • Reduce exposure to fraud • Apply standard approach to verification Prospect approaches bank, asking about products and services Fills out forms to check ID, credit, employment… Receive Accept/Reject result with full granular details Veda - Commercial in Confidence Copyright 2013

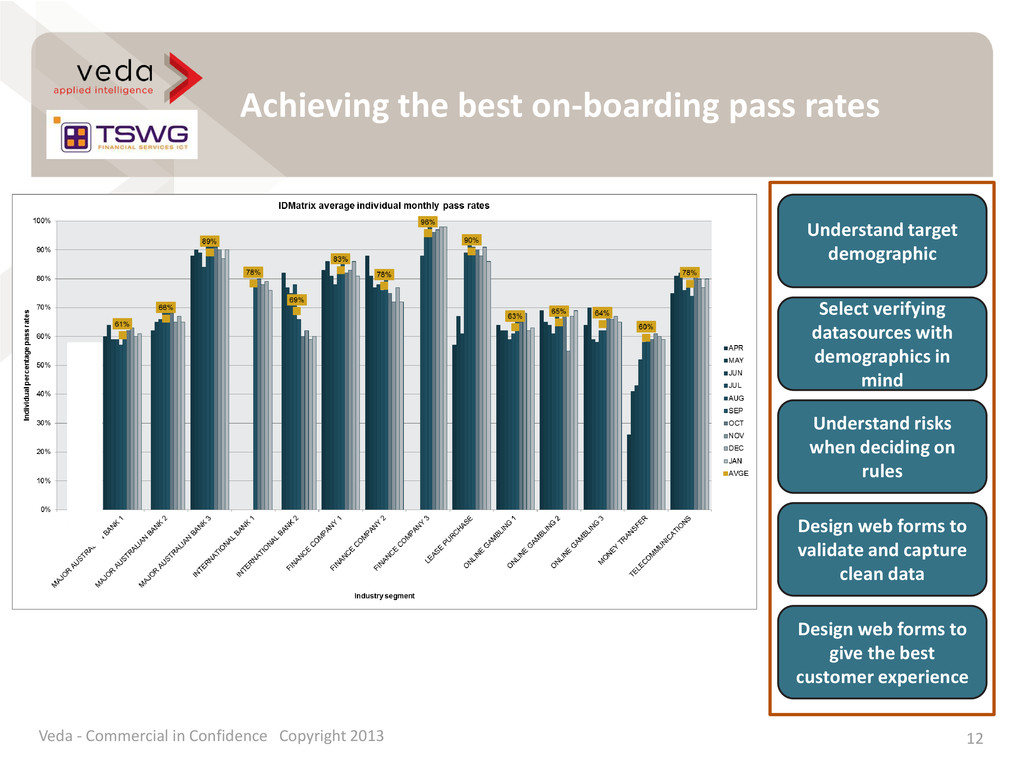

in Confidence Copyright 2013 Understand target demographic Select verifying datasources with demographics in mind Understand risks when deciding on rules Design web forms to validate and capture clean data Design web forms to give the best customer experience

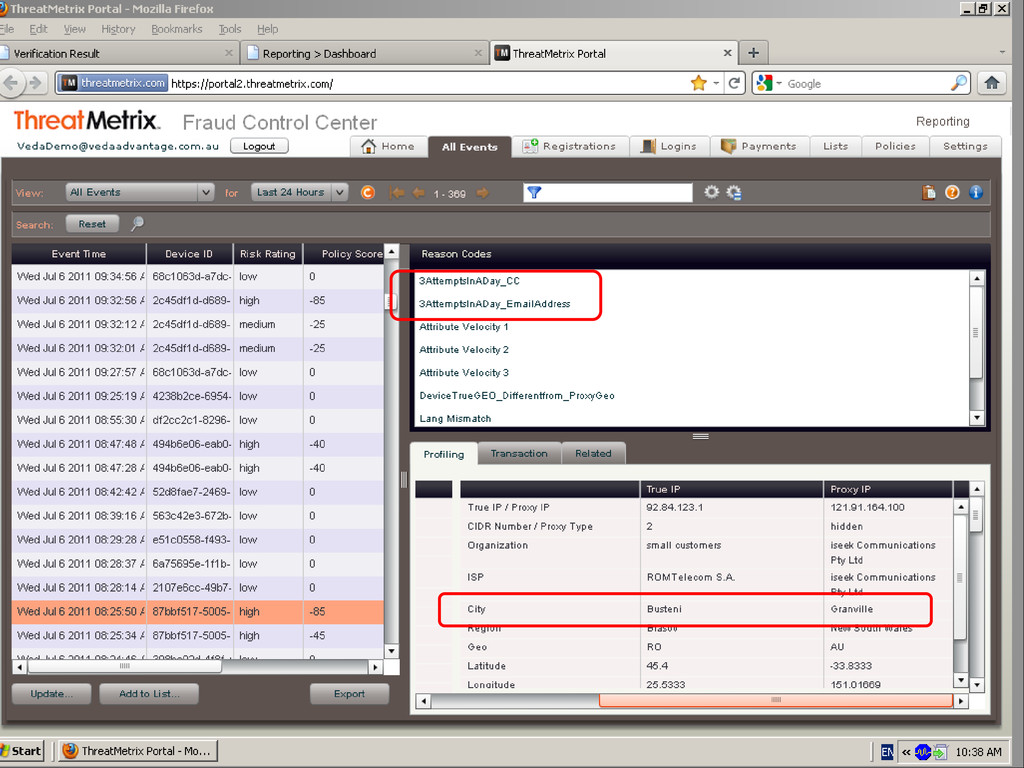

on-line channels 14 Challenges • Account takeovers • Internet used for 70% of account takeovers • Use of stolen credit cards resulting in chargebacks • Inability to reconcile real location with “presented” location • Inability to recognise a “good” returning device • Inability to recognise fraudulent behaviour that can lead to revenue loss Company objectives • Reduce exposure to fraud • Reduce chargebacks • Improve customer experience • Reduce investigation costs • Maintain reputation Veda - Commercial in Confidence Copyright 2013

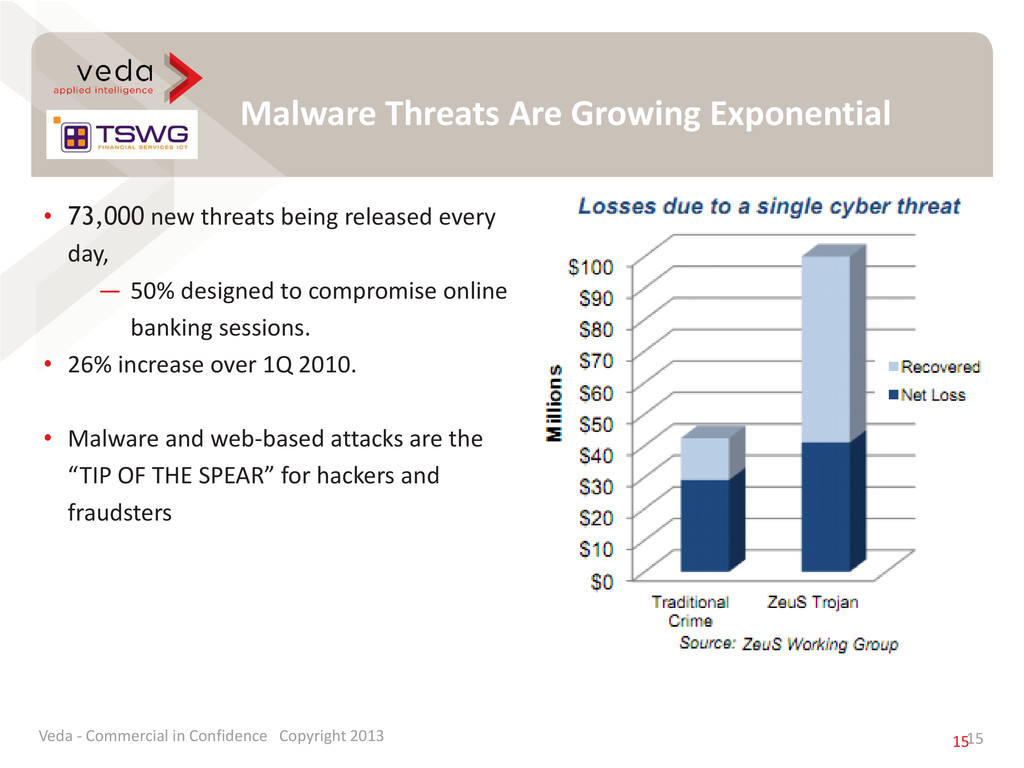

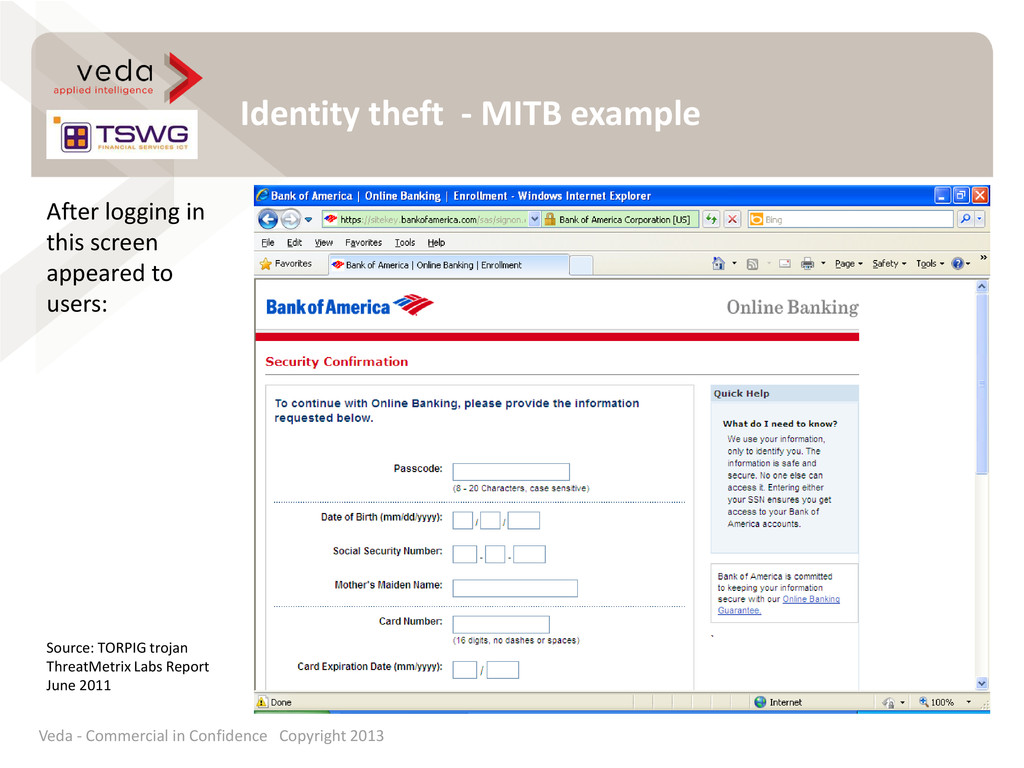

threats being released every day, ― 50% designed to compromise online banking sessions. • 26% increase over 1Q 2010. • Malware and web-based attacks are the “TIP OF THE SPEAR” for hackers and fraudsters Veda - Commercial in Confidence Copyright 2013

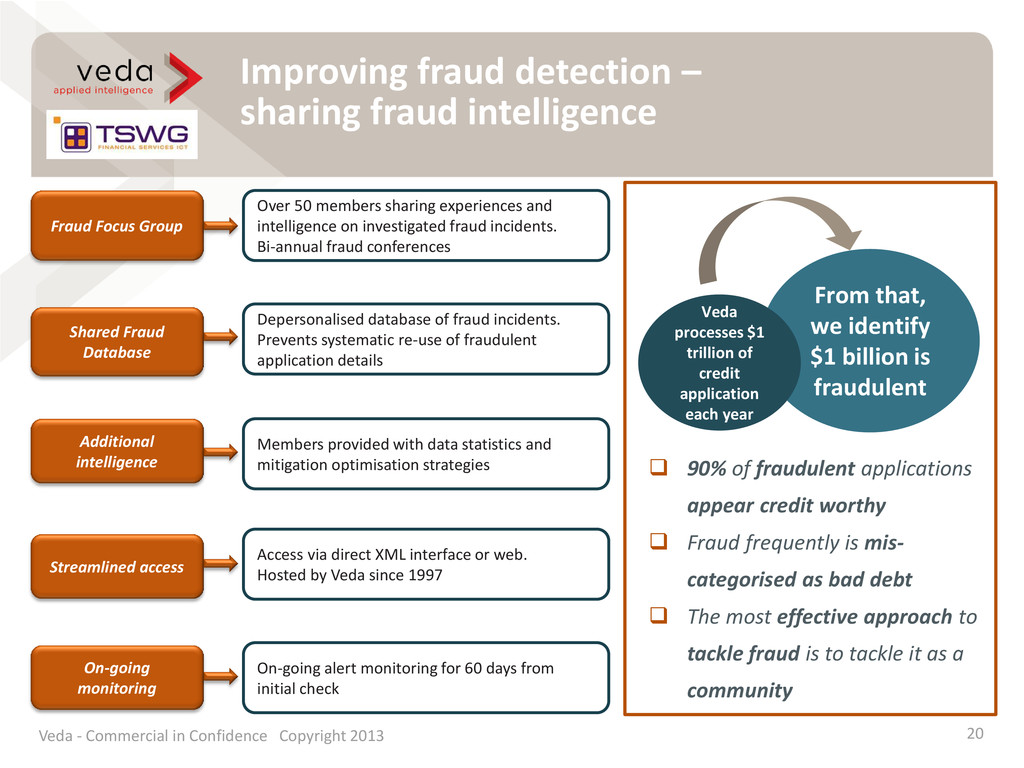

90% of fraudulent applications appear credit worthy Fraud frequently is mis- categorised as bad debt The most effective approach to tackle fraud is to tackle it as a community From that, we identify $1 billion is fraudulent Veda processes $1 trillion of credit application each year Challenges • Credit applications appear clean • Internal fraud records limited • Identity fraud on the rise • Counterfeit credit cards on the increase • Falsified / fake documentation is on the rise, and the “quality” is improving • Organised fraud ring activity increasing Company objectives • Reduce exposure to fraud • Improve customer experience • Reduce investigation costs • Maintain reputation Veda - Commercial in Confidence Copyright 2013

going away • Fraudsters continue to “try it on”, little regard for consequences • Online channels mean applications will be submitted to multiple organisations Falsified documentation harder to spot • Bank statements • ATO NOAs (Notice Of Assessment) • Payslips • Identity documents 3rd party fraud rings increasing • Solicitors • Brokers • Accountants Veda - Commercial in Confidence Copyright 2013

fraudulent applications appear credit worthy Fraud frequently is mis- categorised as bad debt The most effective approach to tackle fraud is to tackle it as a community From that, we identify $1 billion is fraudulent Veda processes $1 trillion of credit application each year Fraud Focus Group Over 50 members sharing experiences and intelligence on investigated fraud incidents. Bi-annual fraud conferences Shared Fraud Database Depersonalised database of fraud incidents. Prevents systematic re-use of fraudulent application details Streamlined access Access via direct XML interface or web. Hosted by Veda since 1997 Additional intelligence Members provided with data statistics and mitigation optimisation strategies On-going monitoring On-going alert monitoring for 60 days from initial check 20 Veda - Commercial in Confidence Copyright 2013

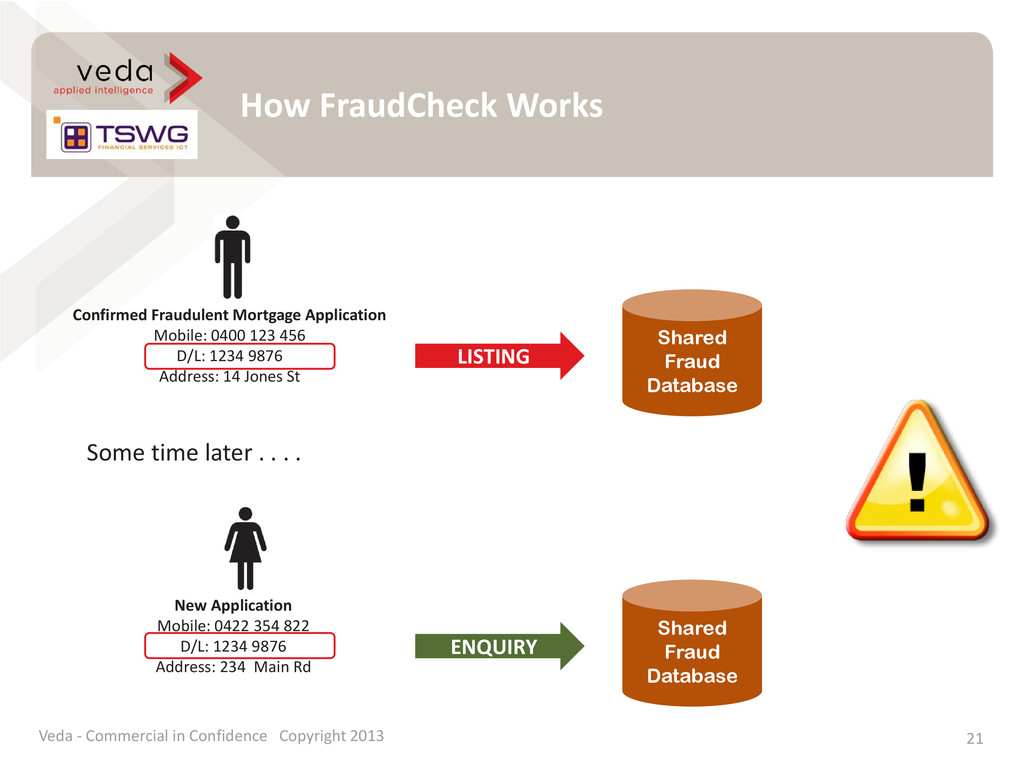

123 456 D/L: 1234 9876 Address: 14 Jones St Shared Fraud Database LISTING Some time later . . . . New Application Mobile: 0422 354 822 D/L: 1234 9876 Address: 234 Main Rd Shared Fraud Database ENQUIRY Veda - Commercial in Confidence Copyright 2013

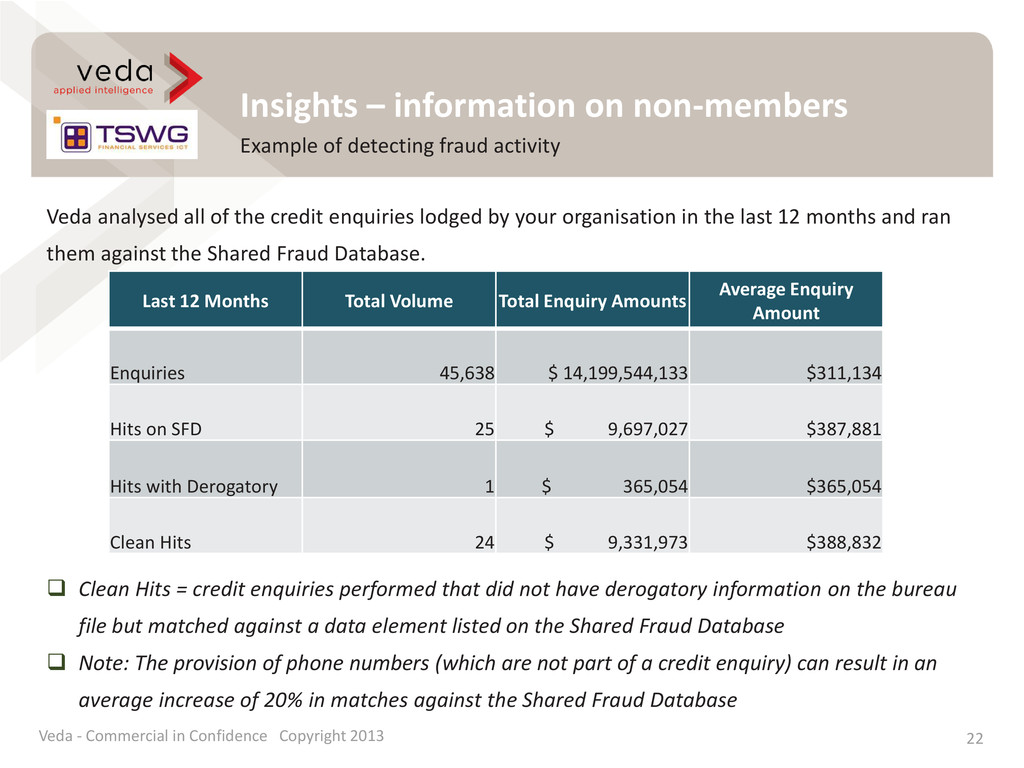

22 Veda analysed all of the credit enquiries lodged by your organisation in the last 12 months and ran them against the Shared Fraud Database. Last 12 Months Total Volume Total Enquiry Amounts Average Enquiry Amount Enquiries 45,638 $ 14,199,544,133 $311,134 Hits on SFD 25 $ 9,697,027 $387,881 Hits with Derogatory 1 $ 365,054 $365,054 Clean Hits 24 $ 9,331,973 $388,832 Clean Hits = credit enquiries performed that did not have derogatory information on the bureau file but matched against a data element listed on the Shared Fraud Database Note: The provision of phone numbers (which are not part of a credit enquiry) can result in an average increase of 20% in matches against the Shared Fraud Database Veda - Commercial in Confidence Copyright 2013

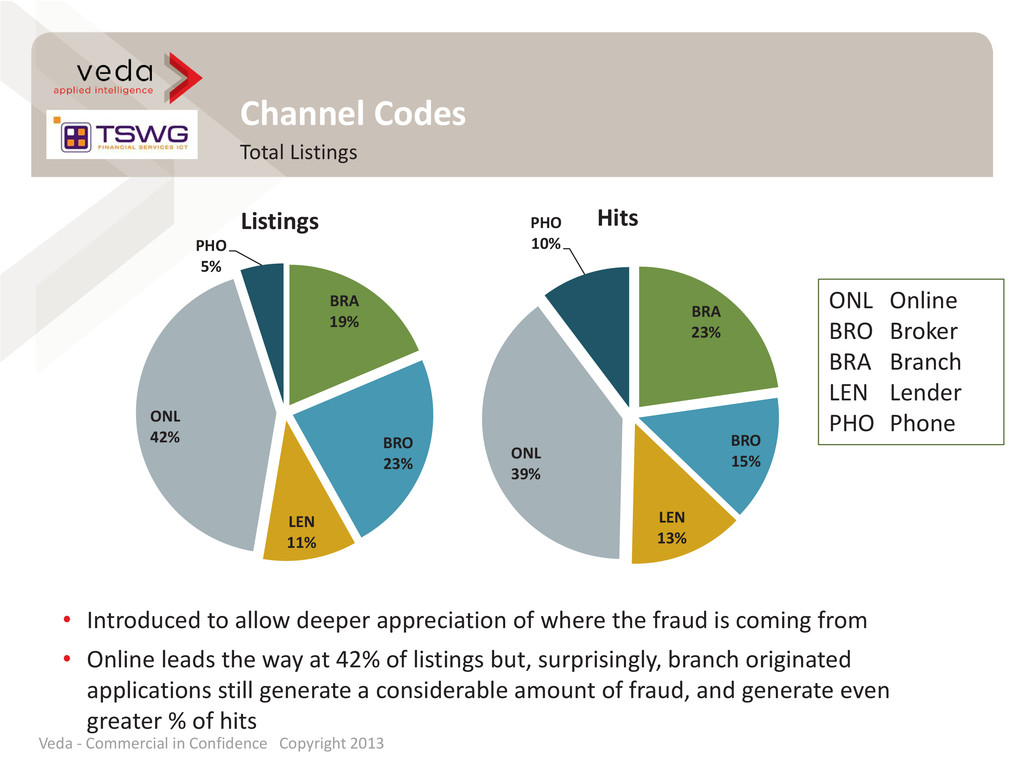

of where the fraud is coming from • Online leads the way at 42% of listings but, surprisingly, branch originated applications still generate a considerable amount of fraud, and generate even greater % of hits ONL Online BRO Broker BRA Branch LEN Lender PHO Phone BRA 19% BRO 23% LEN 11% ONL 42% PHO 5% Listings BRA 23% BRO 15% LEN 13% ONL 39% PHO 10% Hits Veda - Commercial in Confidence Copyright 2013

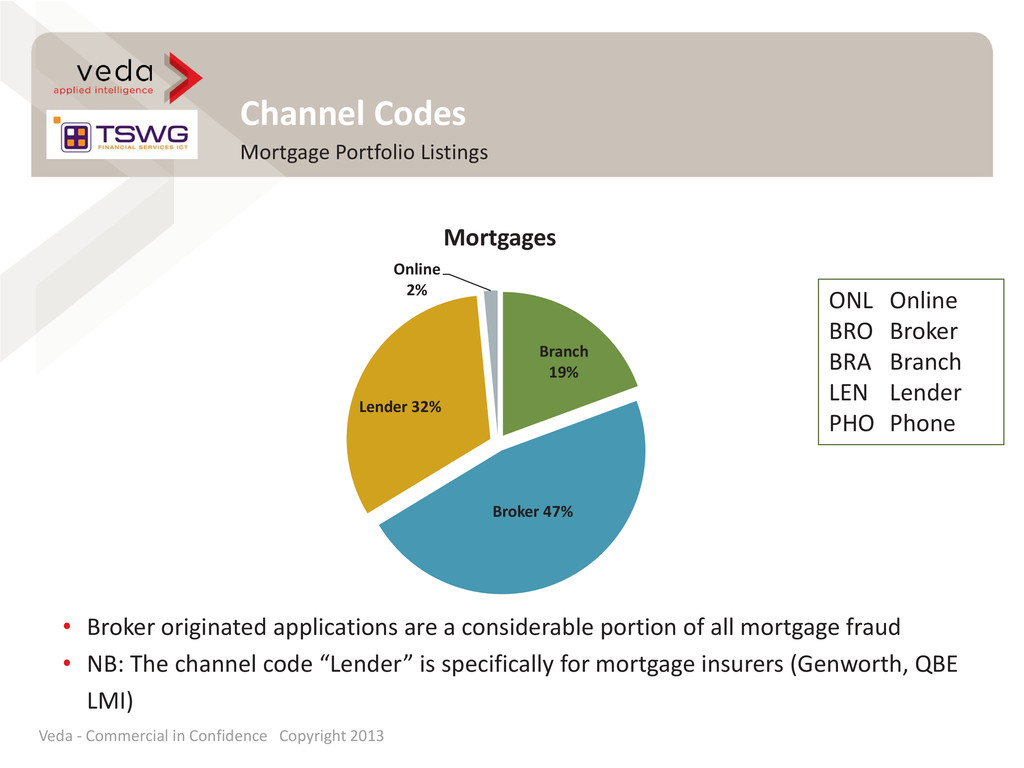

a considerable portion of all mortgage fraud • NB: The channel code “Lender” is specifically for mortgage insurers (Genworth, QBE LMI) Branch 19% Broker 47% Lender 32% Online 2% Mortgages ONL Online BRO Broker BRA Branch LEN Lender PHO Phone Veda - Commercial in Confidence Copyright 2013

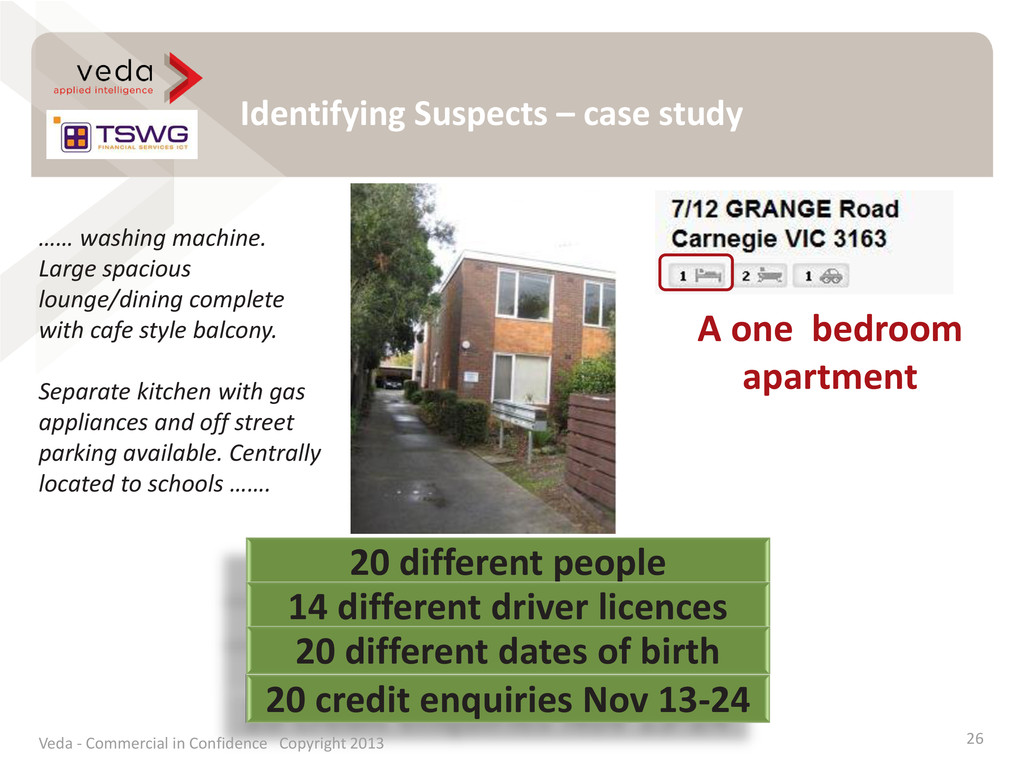

different driver licences 20 different dates of birth 20 credit enquiries Nov 13-24 …… washing machine. Large spacious lounge/dining complete with cafe style balcony. Separate kitchen with gas appliances and off street parking available. Centrally located to schools ……. A one bedroom apartment Veda - Commercial in Confidence Copyright 2013

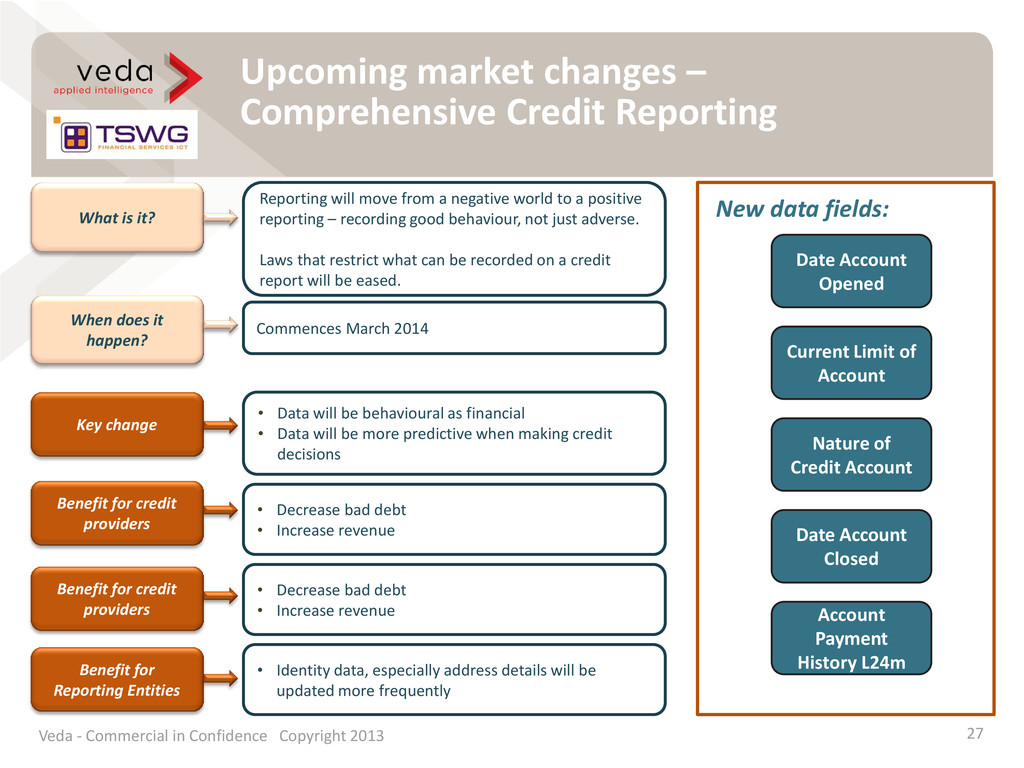

What is it? Reporting will move from a negative world to a positive reporting – recording good behaviour, not just adverse. Laws that restrict what can be recorded on a credit report will be eased. When does it happen? Commences March 2014 Benefit for credit providers • Decrease bad debt • Increase revenue Key change • Data will be behavioural as financial • Data will be more predictive when making credit decisions Benefit for Reporting Entities • Identity data, especially address details will be updated more frequently 27 Date Account Opened Current Limit of Account Nature of Credit Account Date Account Closed Account Payment History L24m Benefit for credit providers • Decrease bad debt • Increase revenue Veda - Commercial in Confidence Copyright 2013

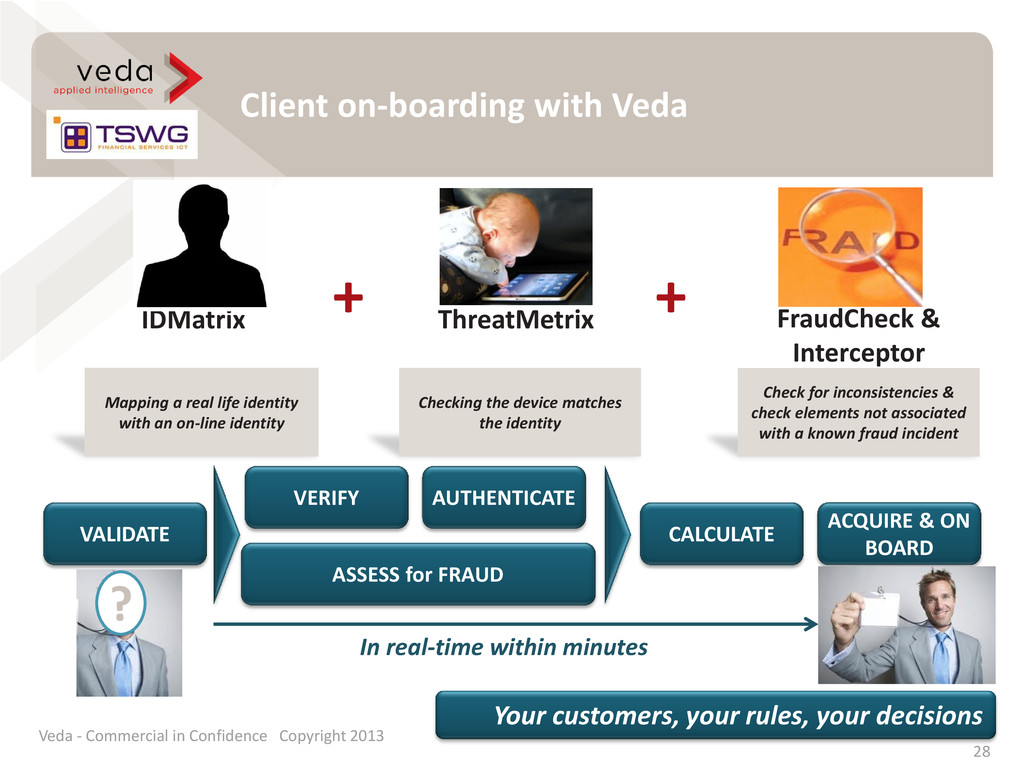

CALCULATE ACQUIRE & ON BOARD In real-time within minutes ? Your customers, your rules, your decisions 28 Checking the device matches the identity Check for inconsistencies & check elements not associated with a known fraud incident Mapping a real life identity with an on-line identity Veda - Commercial in Confidence Copyright 2013 IDMatrix ThreatMetrix FraudCheck & Interceptor + +

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}