How will you add value and convenience to your payments? - Adrian Lovney, Cuscal

Adrian Lovney is the General Manager of Products and Services at Cuscal. 9th Annual Innovators Conference -presentation day 1: March 7th @ the Palazzo Versace, Gold Coast, Australia.

community of Independent FIs Enabling payment innovation for our community, from real-time payments to industry leading fraud management Mutual Bank Bank Reserve Bank Credit Union Financial Institution Building Society

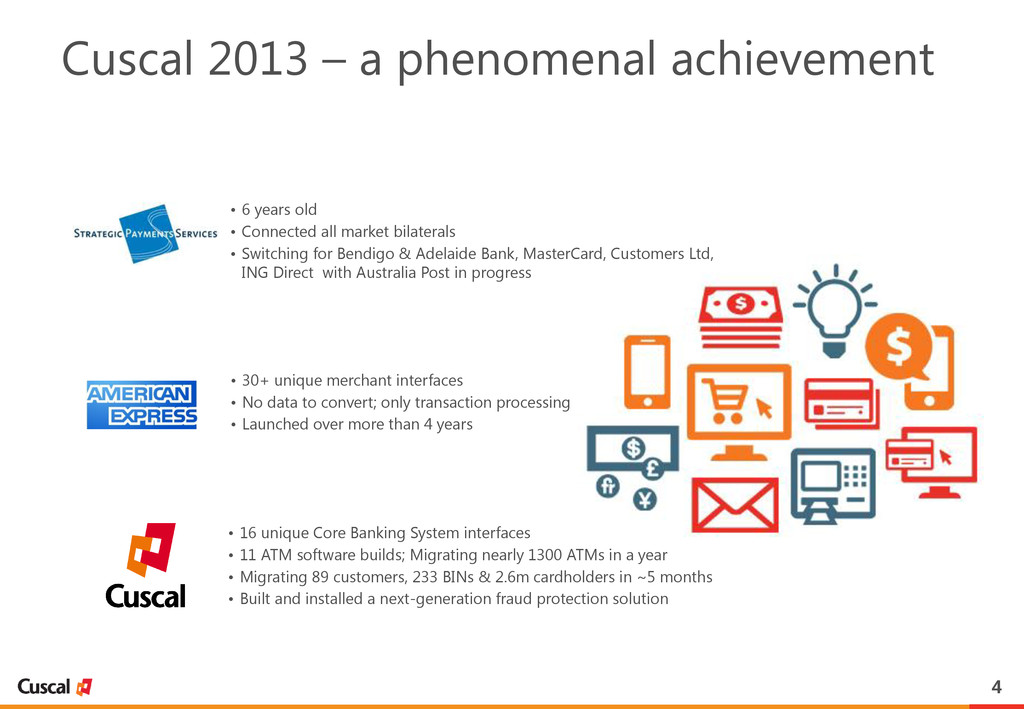

years old • Connected all market bilaterals • Switching for Bendigo & Adelaide Bank, MasterCard, Customers Ltd, ING Direct with Australia Post in progress American Express • 30+ unique merchant interfaces • No data to convert; only transaction processing • Launched over more than 4 years Cuscal • 16 unique Core Banking System interfaces • 11 ATM software builds; Migrating nearly 1300 ATMs in a year • Migrating 89 customers, 233 BINs & 2.6m cardholders in ~5 months • Built and installed a next-generation fraud protection solution

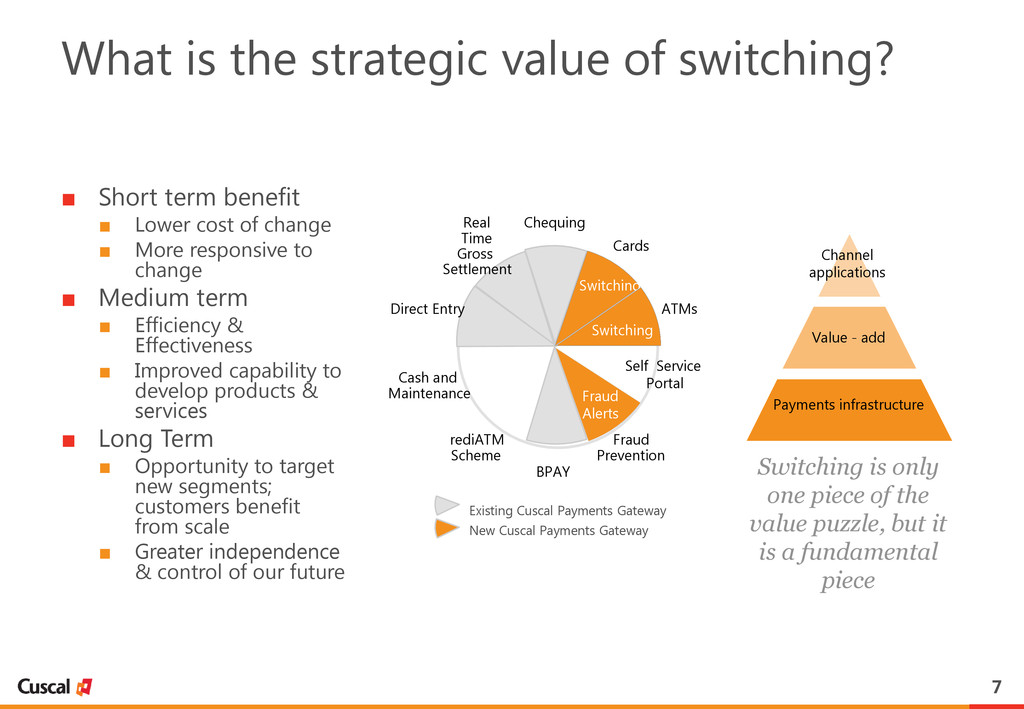

▪ More responsive to change ▪ Medium term ▪ Efficiency & Effectiveness ▪ Improved capability to develop products & services ▪ Long Term ▪ Opportunity to target new segments; customers benefit from scale ▪ Greater independence & control of our future What is the strategic value of switching? Real Time Gross Settlement Chequing Cards ATMs Self Service Portal Direct Entry Cash and Maintenance rediATM Scheme BPAY Fraud Prevention Switching Switching Fraud Alerts Existing Cuscal Payments Gateway New Cuscal Payments Gateway Switching is only one piece of the value puzzle, but it is a fundamental piece Payments infrastructure Value - add Channel applications

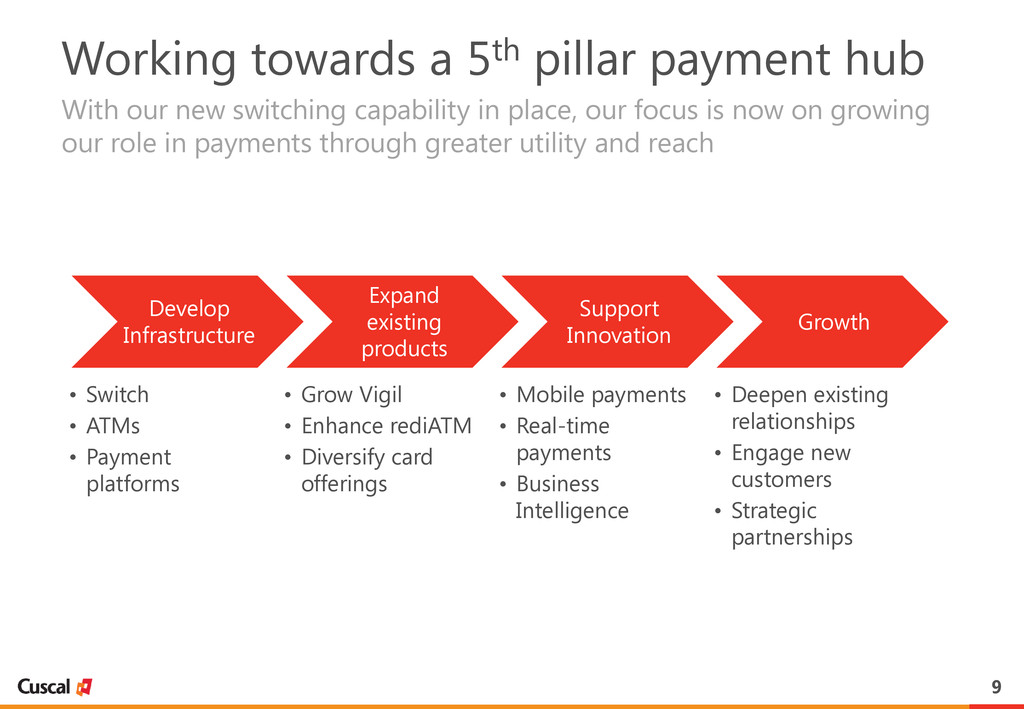

Expand existing products • Grow Vigil • Enhance rediATM • Diversify card offerings Support Innovation • Mobile payments • Real-time payments • Business Intelligence Growth • Deepen existing relationships • Engage new customers • Strategic partnerships Working towards a 5th pillar payment hub With our new switching capability in place, our focus is now on growing our role in payments through greater utility and reach

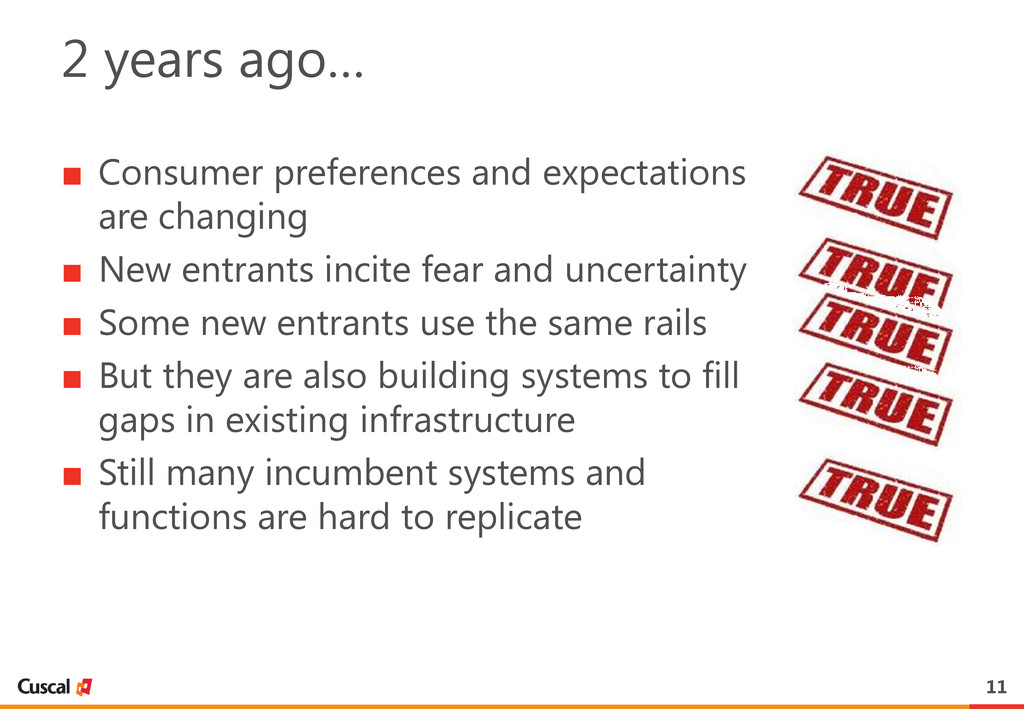

entrants incite fear and uncertainty ▪ Some new entrants use the same rails ▪ But they are also building systems to fill gaps in existing infrastructure ▪ Still many incumbent systems and functions are hard to replicate 2 years ago…

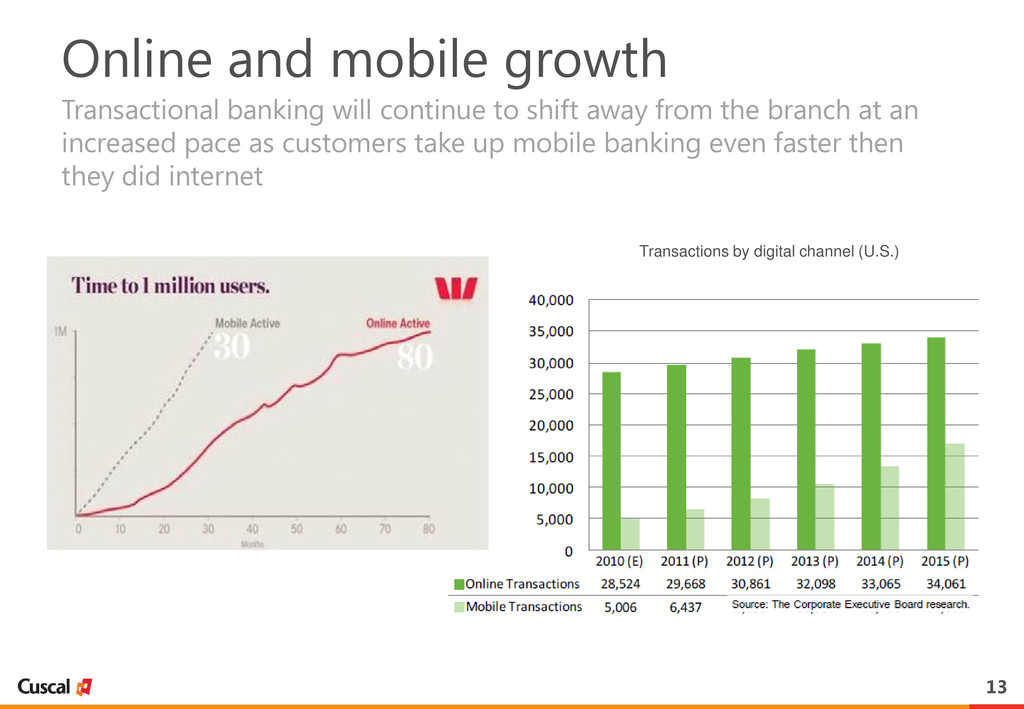

shift away from the branch at an increased pace as customers take up mobile banking even faster then they did internet Transactions by digital channel (U.S.)

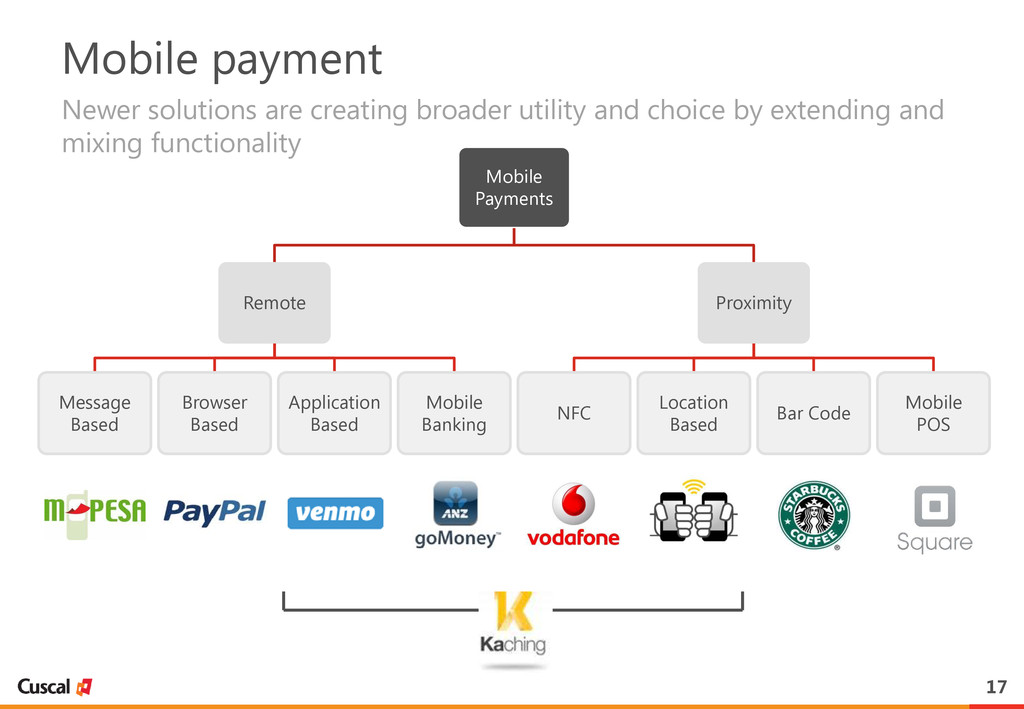

Mobile Banking Proximity NFC Location Based Bar Code Mobile POS Mobile payment Newer solutions are creating broader utility and choice by extending and mixing functionality

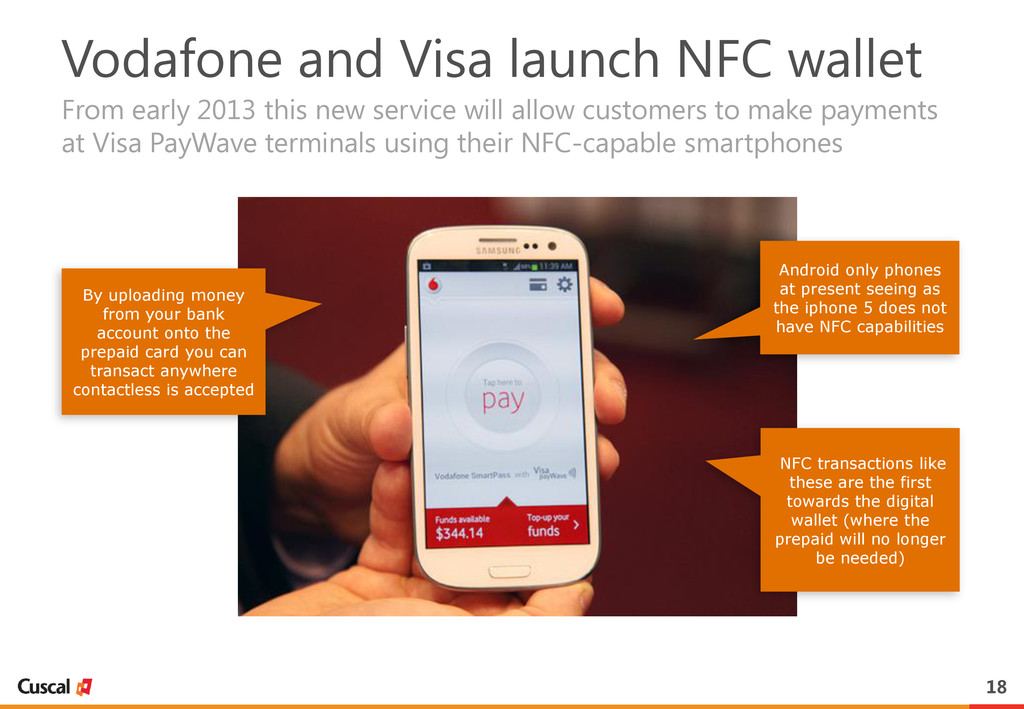

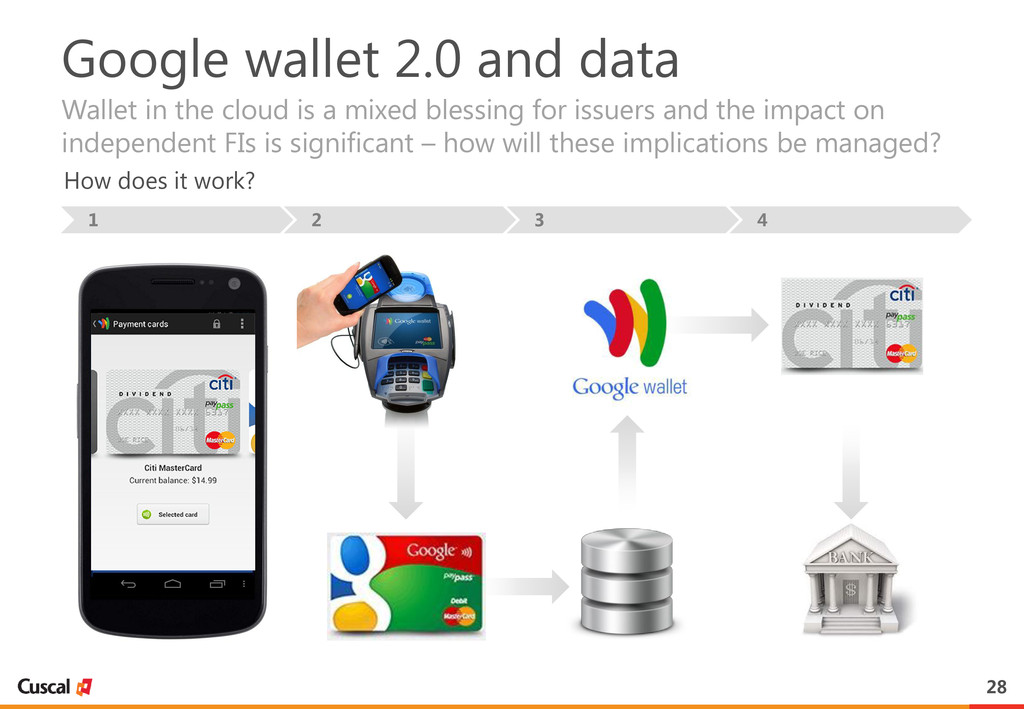

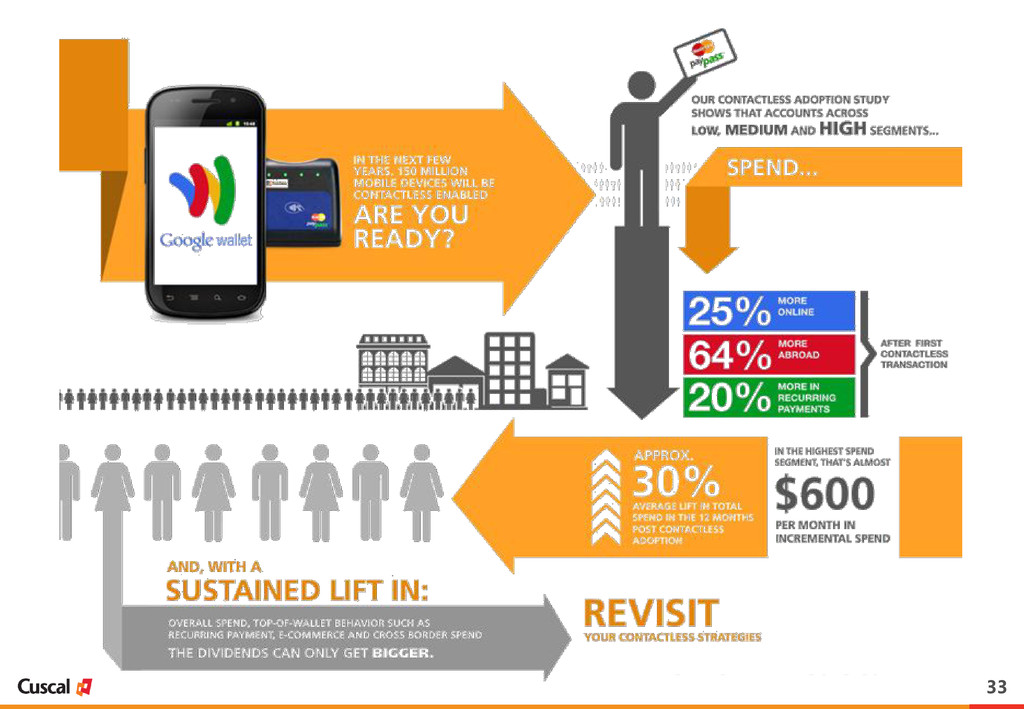

this new service will allow customers to make payments at Visa PayWave terminals using their NFC-capable smartphones Android only phones at present seeing as the iphone 5 does not have NFC capabilities By uploading money from your bank account onto the prepaid card you can transact anywhere contactless is accepted NFC transactions like these are the first towards the digital wallet (where the prepaid will no longer be needed)

and trusted payment solution across multiple channels. Customisable shopping preferences Shoppers can manage their cards, track shipping and set customised alerts on their account. Visa trust and credibility One of the world’s most trusted payment brands – both online and off. Frictionless checkout Customers only need a username and password and do not have to repeatedly enter personal information. Flexible, open platform Supports major credit or debit cards (Visa, MasterCard, American Express). Targeted, relevant offers Customers can opt to receive near-real-time offers from the merchants they value most. V.Me is a single solution that delivers a secure, convenient experience that cardholders expect 1 HSN Consultants: The Nilson Report, Sept 2011

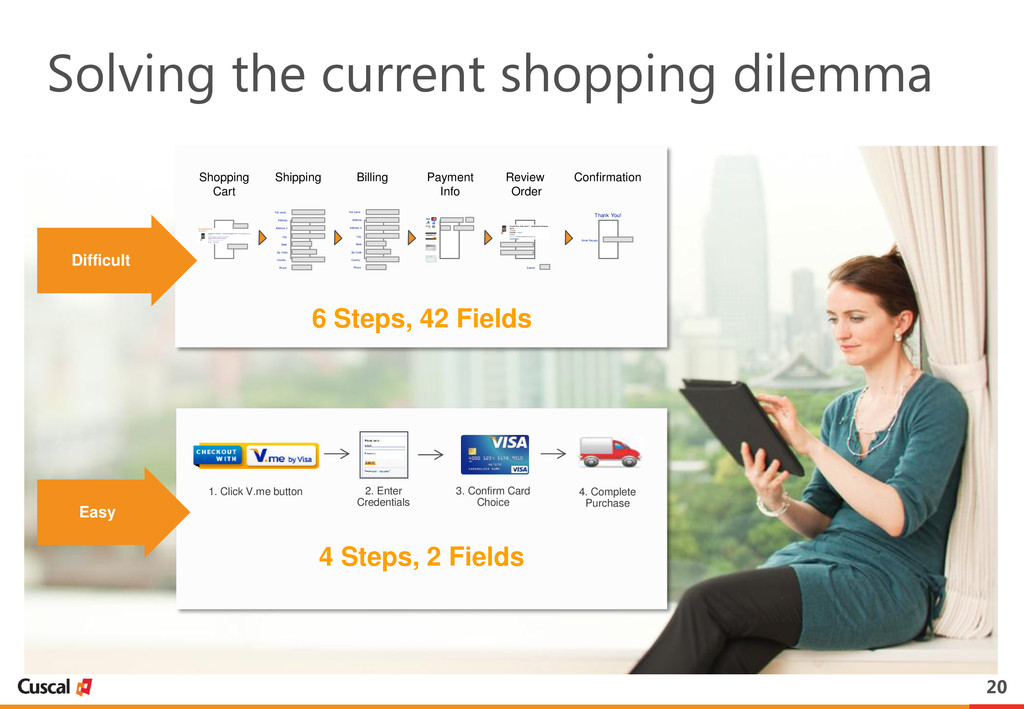

4. Complete Purchase 1. Click V.me button 6 Steps, 42 Fields 4 Steps, 2 Fields 2. Enter Credentials Difficult Easy Billing Payment Info Shipping Review Order Confirmation Shopping Cart Full name Address Address 2 City State Zip Code Country Phone Full name Address Address 2 City State Zip Code Country Phone Thank You! Submit Email Receipt

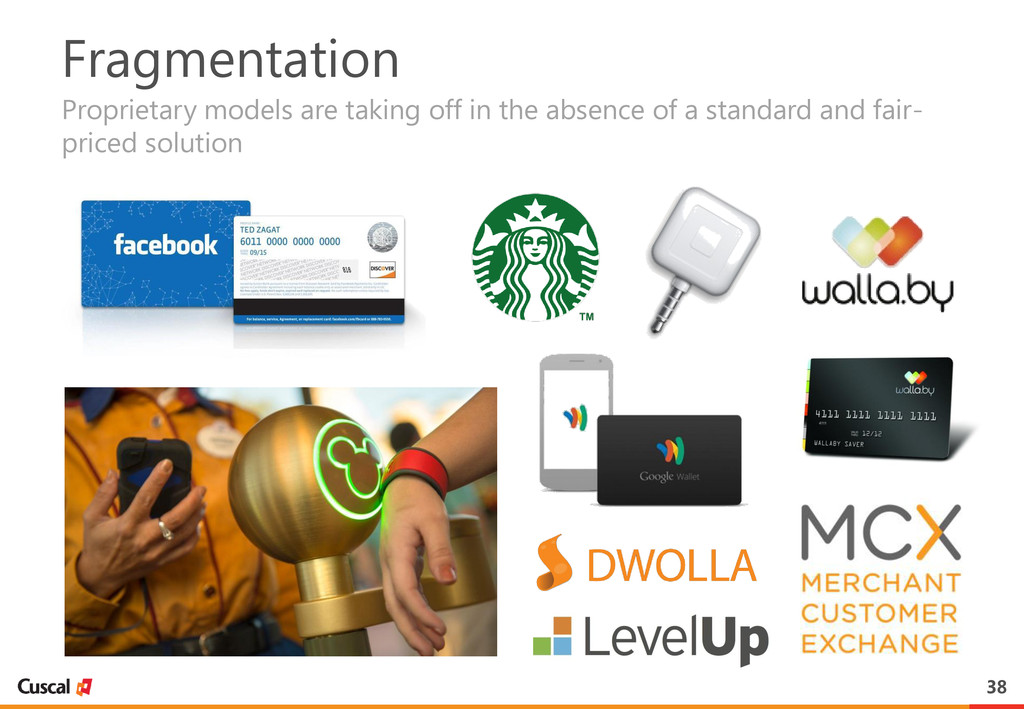

to meet small-merchant needs, rapid evolution and varying approaches create a highly competitive and fragmented environment Mobile POS iPhone Case Dongle QR/Barcode Location/App-Based Empty-Hands

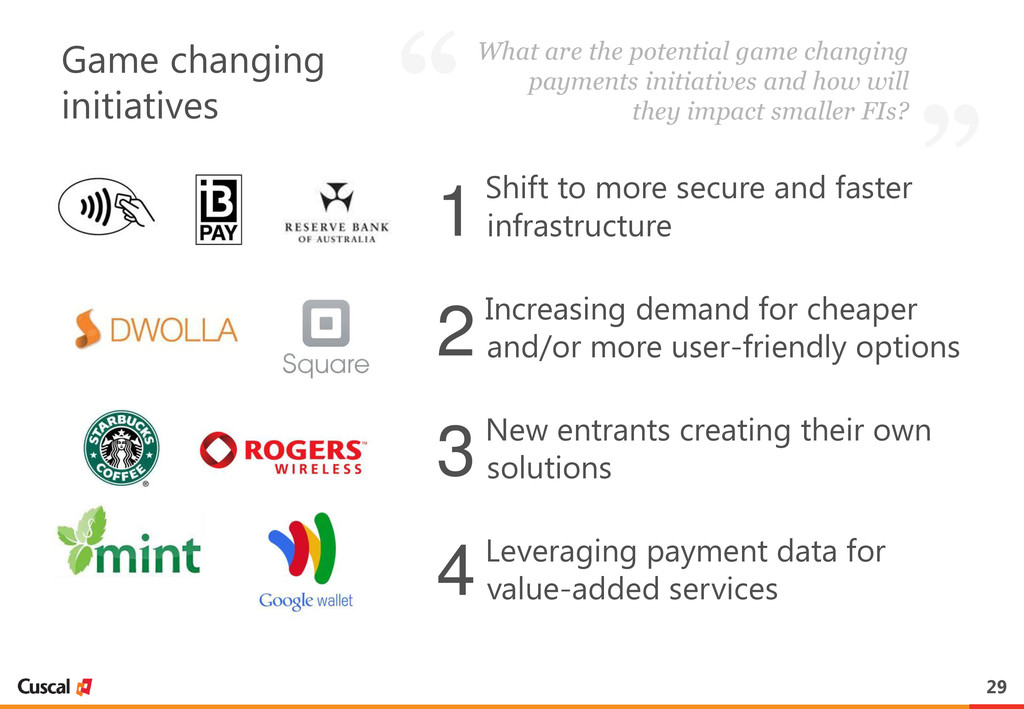

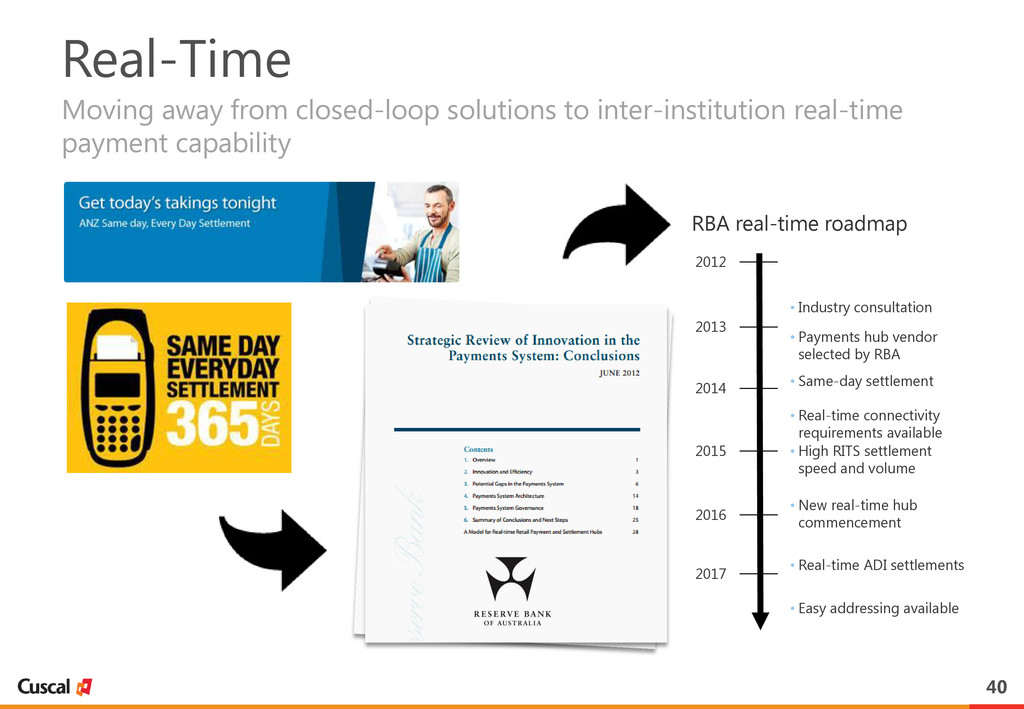

the potential game changing payments initiatives and how will they impact smaller FIs? Shift to more secure and faster infrastructure Increasing demand for cheaper and/or more user-friendly options New entrants creating their own solutions Leveraging payment data for value-added services 1 2 3 4

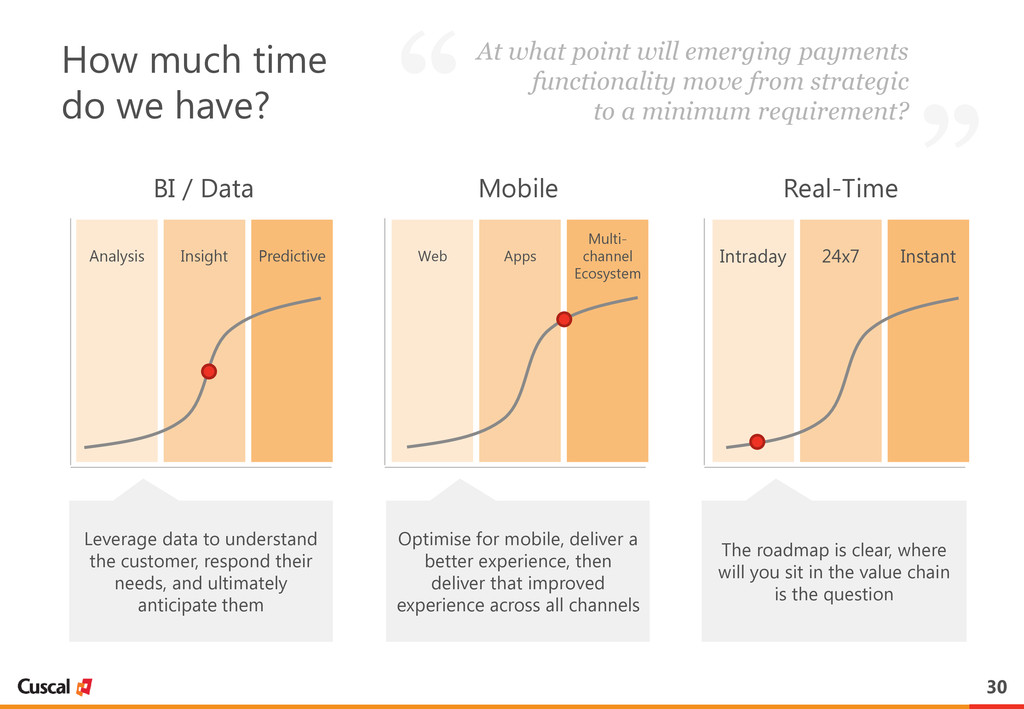

Intraday 24x7 Instant Analysis Insight Predictive How much time do we have? At what point will emerging payments functionality move from strategic to a minimum requirement? BI / Data Real-Time Mobile Leverage data to understand the customer, respond their needs, and ultimately anticipate them Optimise for mobile, deliver a better experience, then deliver that improved experience across all channels The roadmap is clear, where will you sit in the value chain is the question

convenience) are as effective at driving consumer recognition of benefit and behavioural change as large changes in financial gain 1) Incremental Innovation

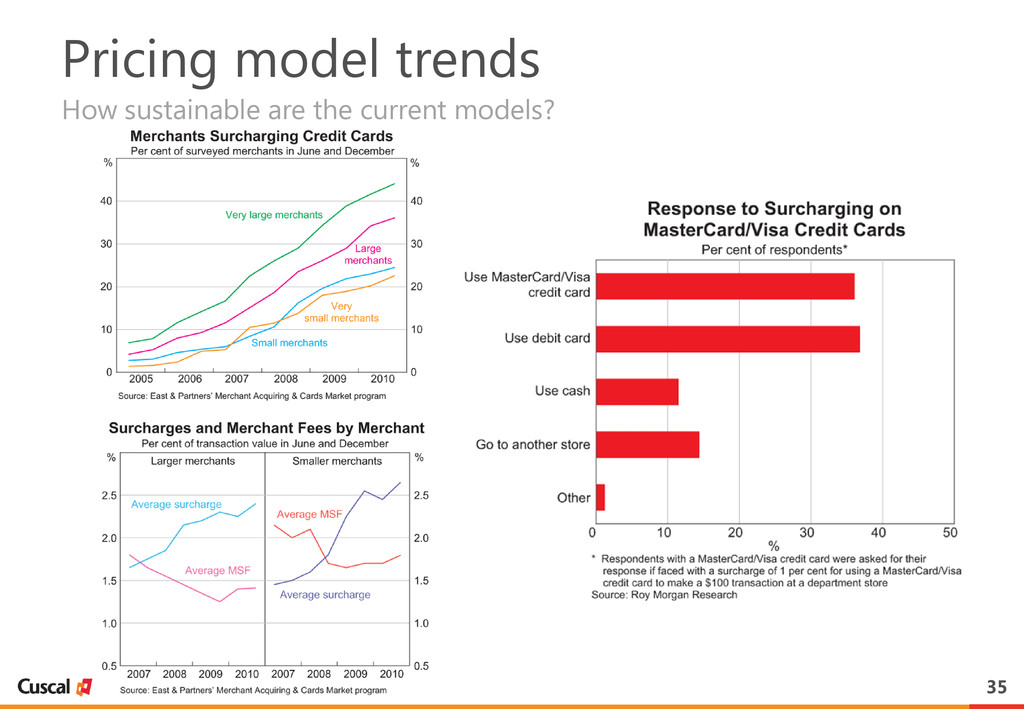

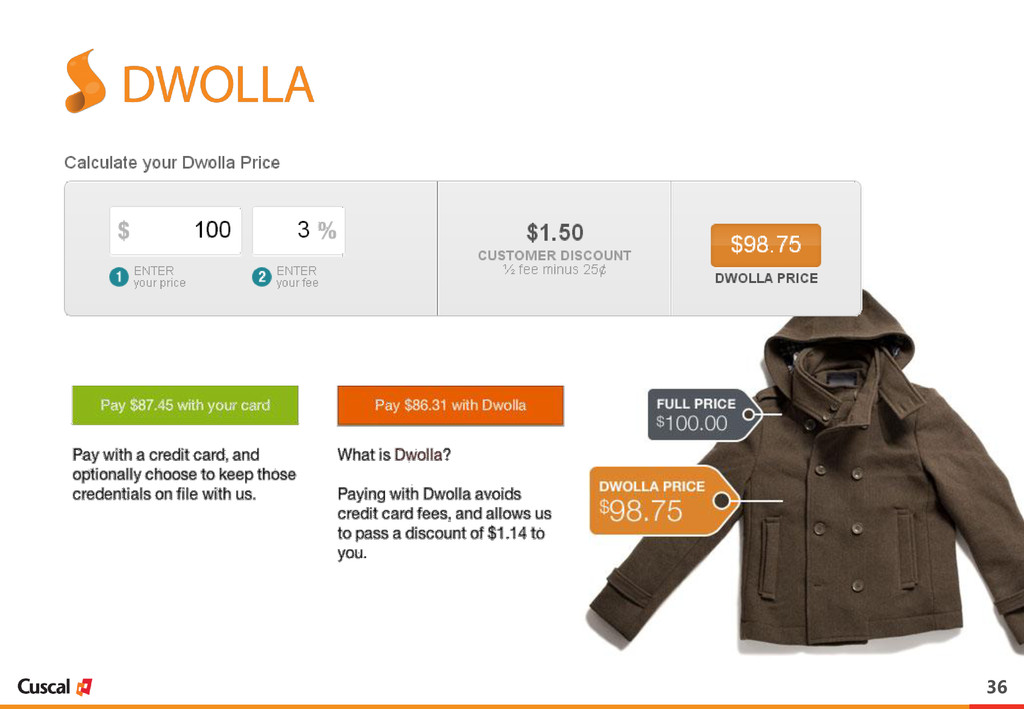

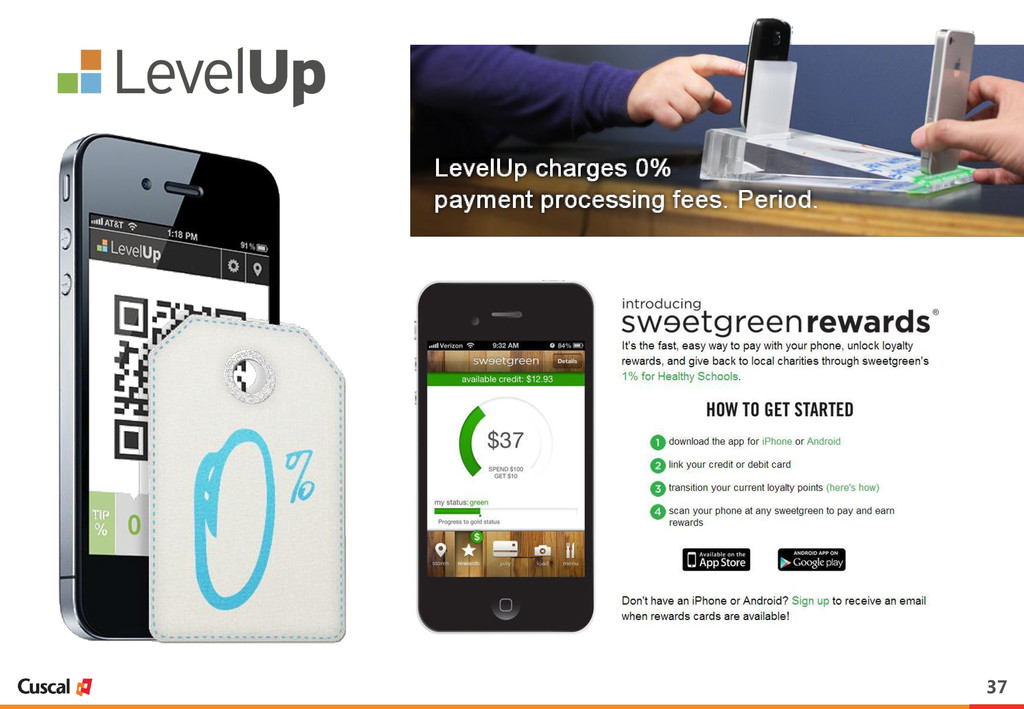

lack of initiative by incumbents, and existing pricing structures being called into question No MSF! $0.25 Flat Fee per transaction Buy now, pay later Accept mobile payments in minutes Send money worldwide in real-time

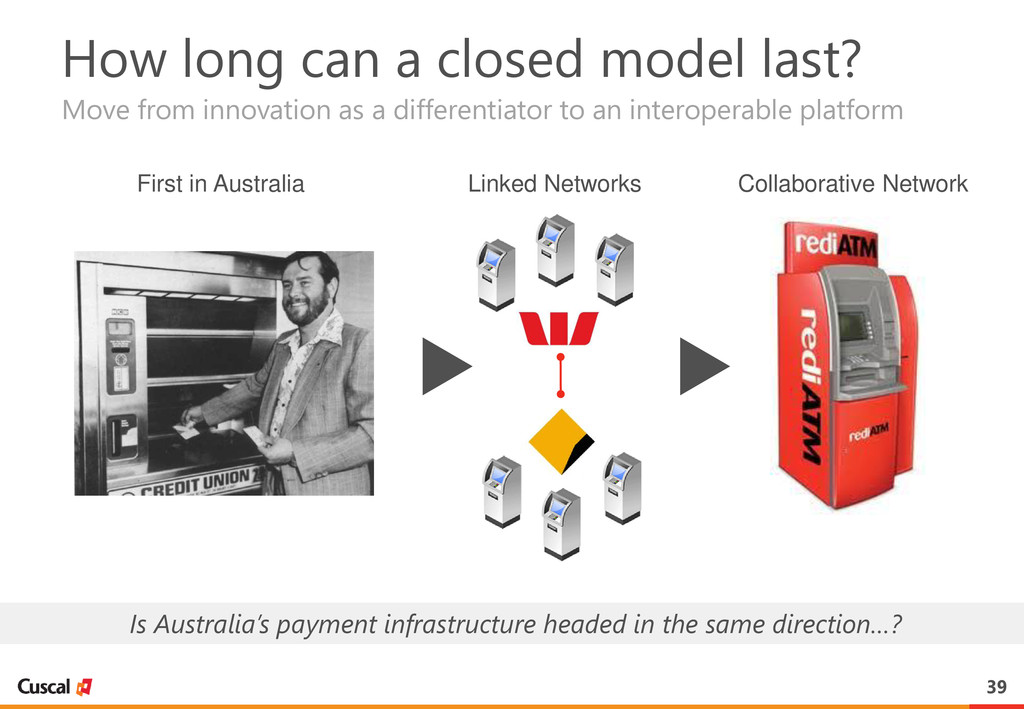

innovation as a differentiator to an interoperable platform First in Australia Linked Networks Collaborative Network Is Australia’s payment infrastructure headed in the same direction…?

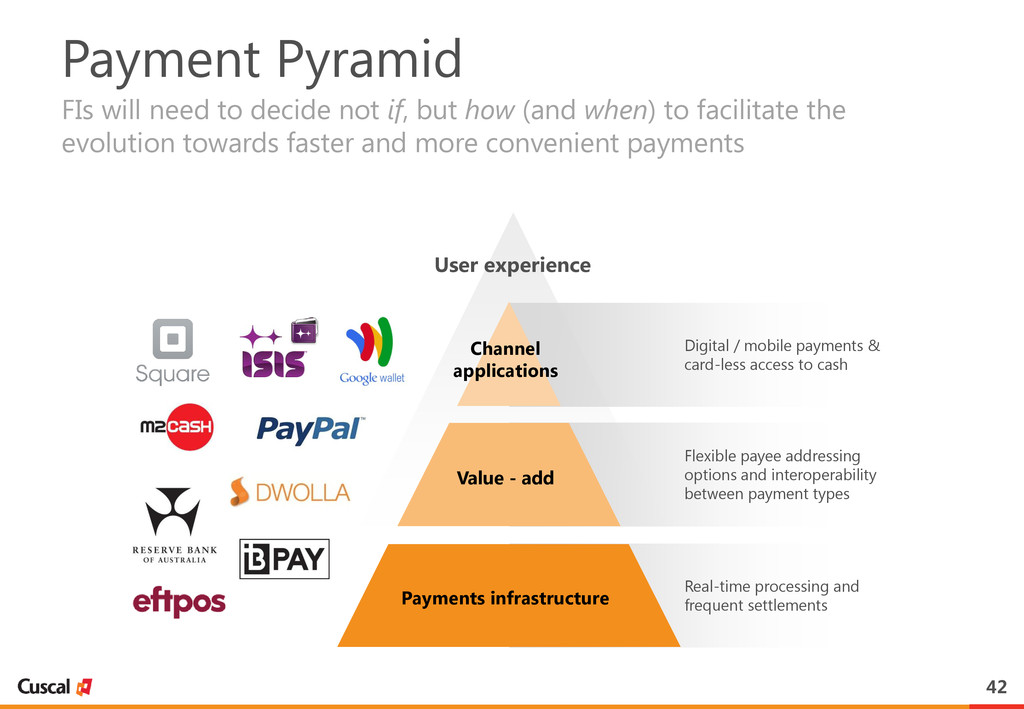

but how (and when) to facilitate the evolution towards faster and more convenient payments User experience Payments infrastructure Value - add Channel applications Digital / mobile payments & card-less access to cash Flexible payee addressing options and interoperability between payment types Real-time processing and frequent settlements

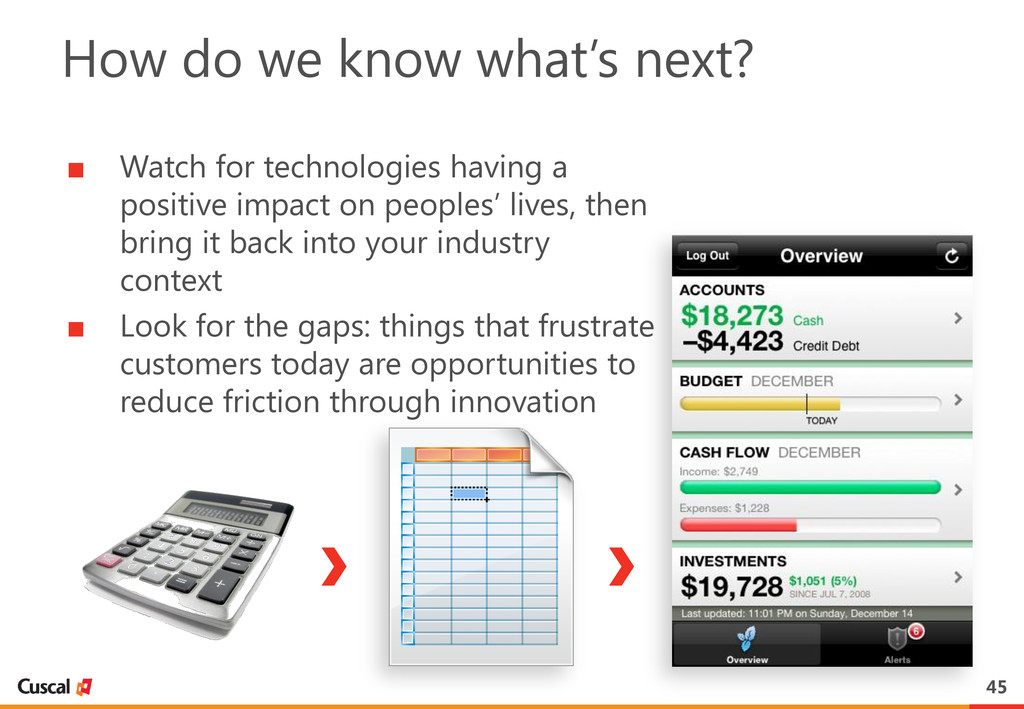

peoples’ lives, then bring it back into your industry context ▪ Look for the gaps: things that frustrate customers today are opportunities to reduce friction through innovation How do we know what’s next?

About Cuscal Next generation payments platform, owned by its customers An authorised deposit-taking institution regulated by the Australian Prudential regulatory Authority. Issued with a long-term rating of “A+” by Standard & Poor’s. Operates rediATM, the national ATM network. Uniquely a multi-institutional settler for all our customers. rediATM has 100+ issuers and acquirers. Sponsors the issuance of 2.8 million domestic EFTPOS and VISA Debit cards. Most recently we have built and launched our own modern and agile payments switch to deliver greater value to our customers and enable growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}