a recovering lawyer (don’t hold it against me). • Currently, I’m the Chair of Fintech Australia. We’re Australia’s leading Fintech industry Association. • Former GM Stone & Chalk, Melbourne. • Founder of Fintech Victoria. • Also, was a part of the Federal Government’s Fintech Advisory Group and a member of ASIC’s Digital Finance Advisory Committee and lead Fintech Australia’s working group on Open Banking. • Angel investor in early stage Fintech startups. Come talk to me if you’re an early stage startup.

to be a huge transformation for the Australian economy… but it’ll take time. • Fintech startups will lead the disruption. • Open Banking is but one part of the puzzle and the real break outs will occur when other industries come on board in subsequent phases. • New exciting products will emerge that will make consumers’ lives better. • There are still near term challenges as the regime is implemented. • Open banking will be a ‘narrative disruption’ in financial services. It’ll reduce data moats and change the way consumers interact with the industry.

to where we are today with the CDR. The journey started with the Murray (2014) and the Harper Reviews (2015). • Both recognised the role opening up data could play in improving financial outcomes. • However, the really foundational work was done by the Productivity Commission in its Data Availability and Use Inquiry (2017). • This proposed a bold economy wide CDR to give individuals and SMEs greater access to their data. • This culminated in the Farrell Report (2018) which provided the how a CDR could be established. The Federal Government has agreed to the recommendations made in the report and implementation began.

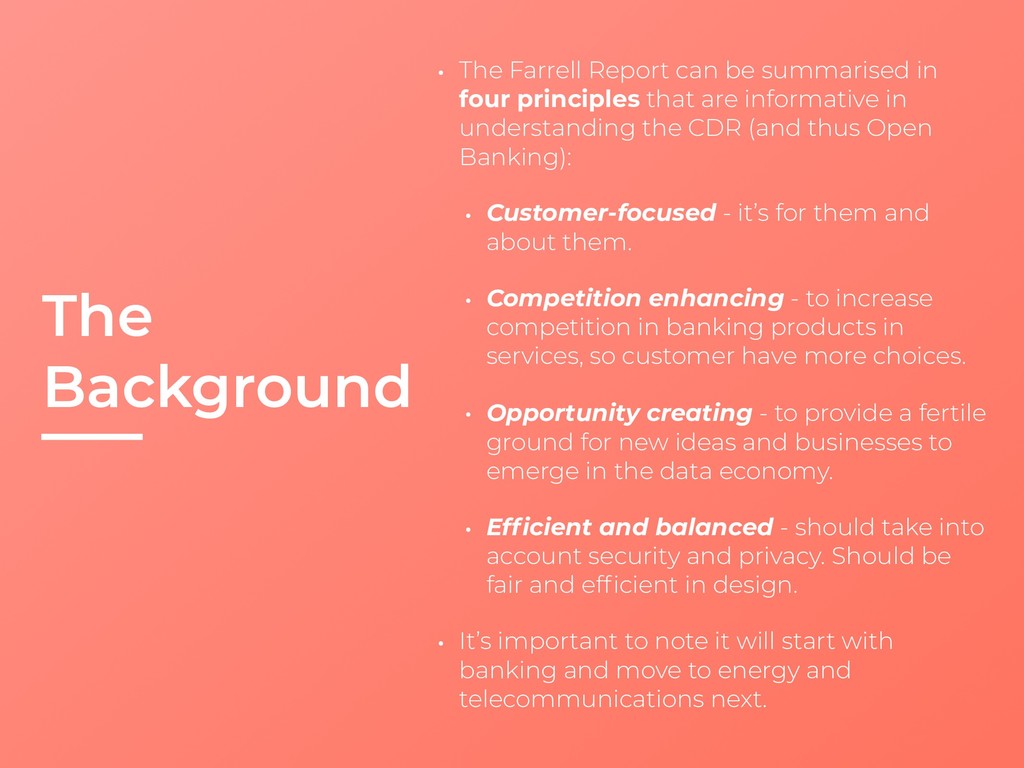

four principles that are informative in understanding the CDR (and thus Open Banking): • Customer-focused - it’s for them and about them. • Competition enhancing - to increase competition in banking products in services, so customer have more choices. • Opportunity creating - to provide a fertile ground for new ideas and businesses to emerge in the data economy. • Efficient and balanced - should take into account security and privacy. Should be fair and efficient in design. • It’s important to note it will start with banking and move to energy and telecommunications next.

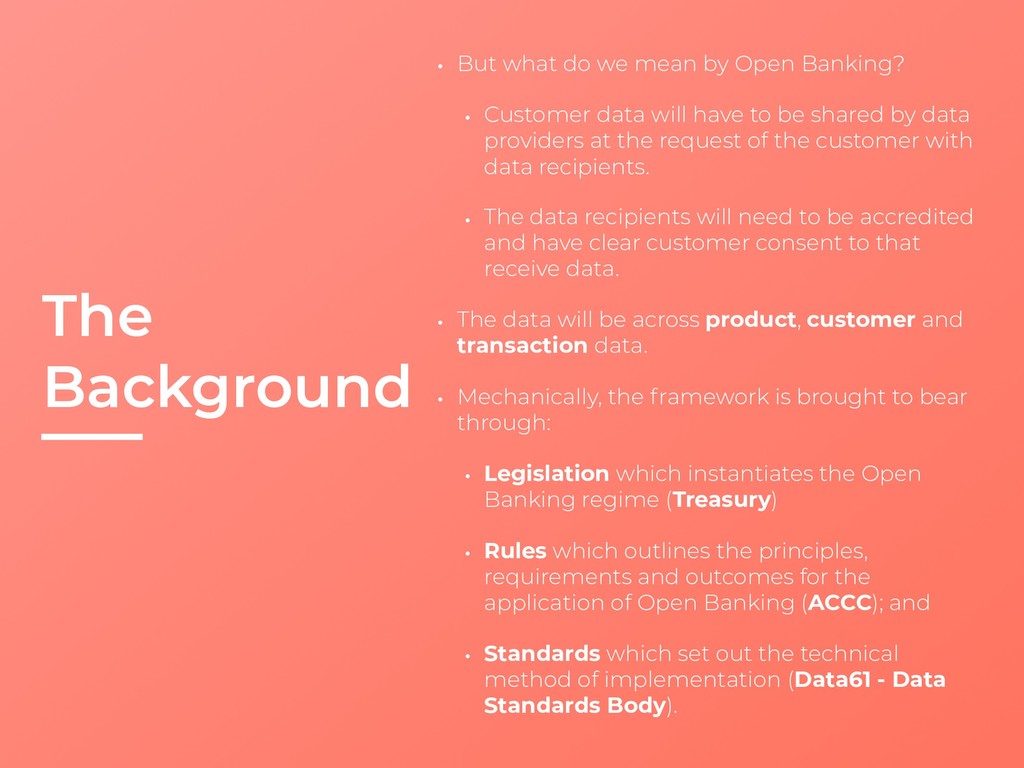

Banking? • Customer data will have to be shared by data providers at the request of the customer with data recipients. • The data recipients will need to be accredited and have clear customer consent to that receive data. • The data will be across product, customer and transaction data. • Mechanically, the framework is brought to bear through: • Legislation which instantiates the Open Banking regime (Treasury) • Rules which outlines the principles, requirements and outcomes for the application of Open Banking (ACCC); and • Standards which set out the technical method of implementation (Data61 - Data Standards Body).

CDR was enacted into law in August 2019. A designation was passed in September which identified Banking as the first sector. • The ACCC released their 'locked down’ version of the proposed rules this month. • The standards are being worked on by Data61 and are in draft form. • July 2019 marked the beginning of the regime with the 4 major banks required to provide product reference data on accounts. • February 2020 will be when the 4 major banks will need to make data on transaction, credit and debit card, deposits and transactions accounts available. • July 2020 the major 4 banks will also make data available on mortgage accounts. Other ADIs will need to make product data on accounts available. • February 2021 the major 4 will need to make transaction data available on all covered products.

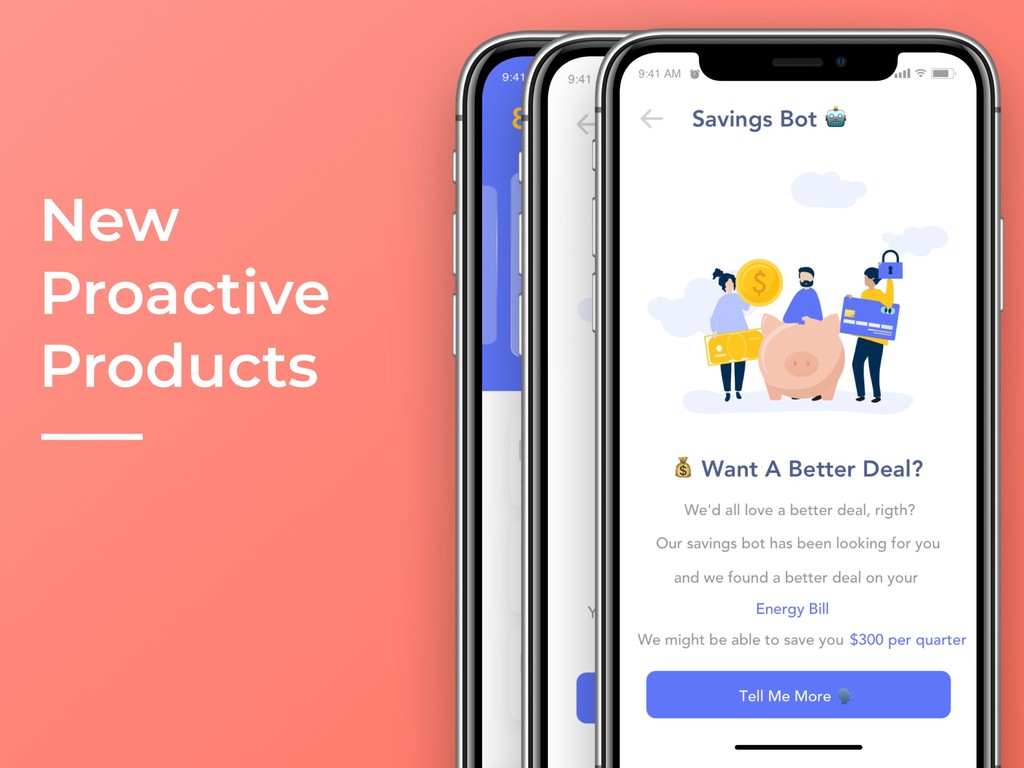

Open Banking will drive more consumer choice, lower costs to consumers and improve competition in financial services. • This Cambrian Explosion of new use cases will make banking more transparent and provide Fintech startups with an opportunity to compete against incumbents. • If you believe that data is the new oil, Open Banking should result in it becoming the new salt. • But how are startups thinking about Open Banking? What are the likely use cases to emerge in the space? • Is this going to be a narrative violation or a narrative continuation?

it will take time. • We’re not there yet. Still work to be done for the regime to really work for Fintech startups. Some are near term - eg. assurance program, role of intermediaries. • While others are longer term questions - eg tiered accreditation. • Costs associated with accreditation is still a potential challenge. • But overall the Open Banking regime provides a glimpse into the future as Australia moves towards a true data economy.

struggle to compete with incumbents due to resources, capability and scale. • The narrative is already being violated as we see startups take on incumbent banks - eg. Revolut has hit 6 million customer globally. • Open Banking will spur this trend as greater access to data will begin to level the playing field for startups and allow for more data driven products. • But there is a huge opportunity for incumbents to partner with startups - eg. Bud and ANZ.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Reach Out Email: [email protected] Twitter: @alantsen](https://files.speakerdeck.com/presentations/9e9735055e8048d4938a868f666bb285/slide_14.jpg){kind=link}