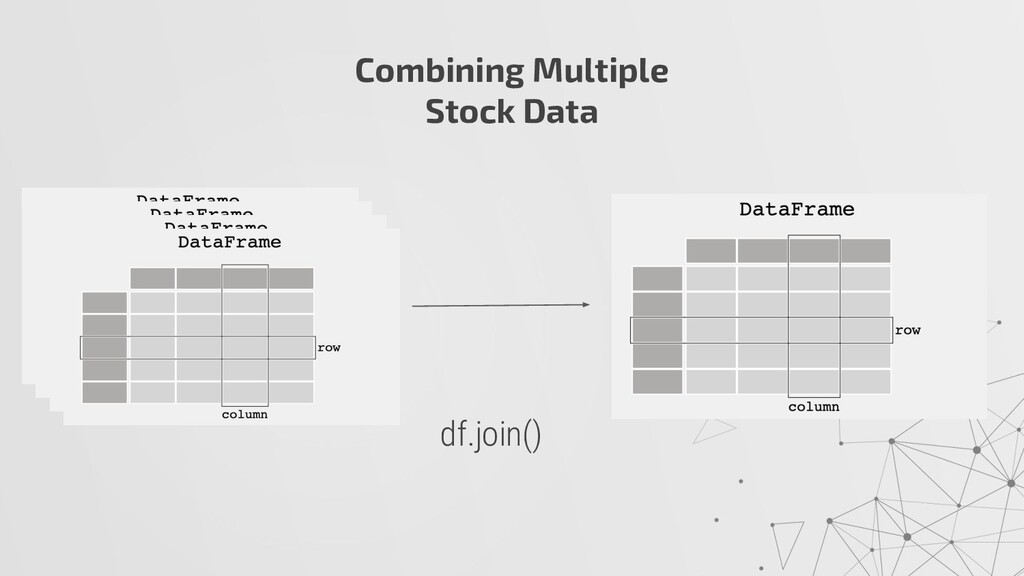

Computing Tools” matplotlib/ seaborn yfinance “Offers a reliable, threaded, and Pythonic way to download historical market data from Yahoo! finance” Python Visualization Libraries

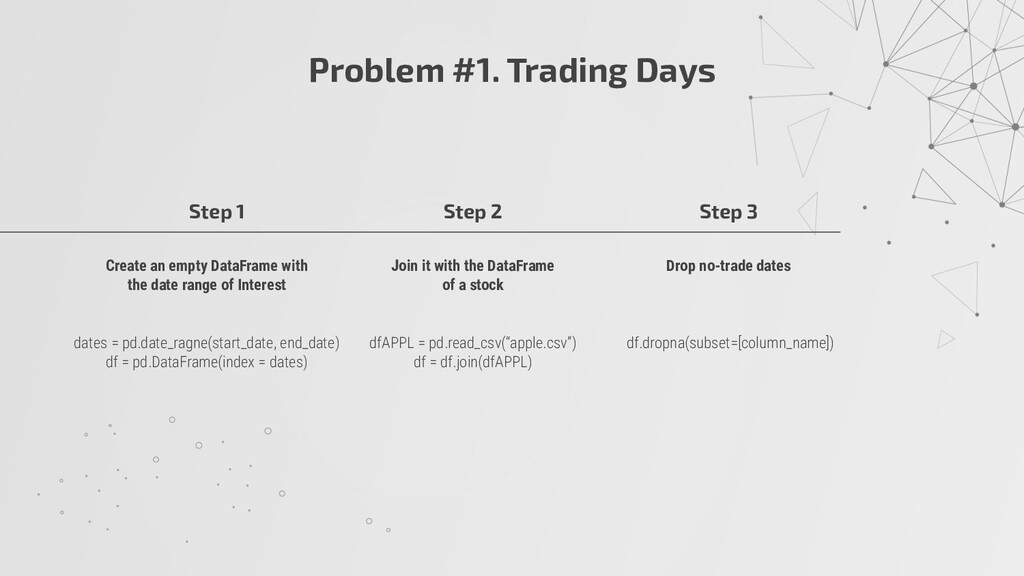

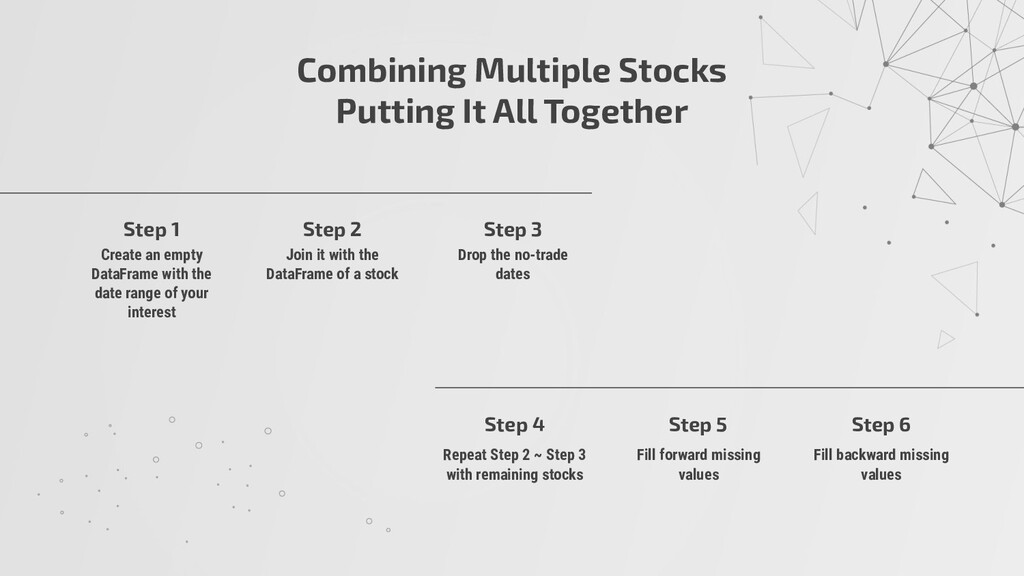

with the date range of Interest dates = pd.date_ragne(start_date, end_date) df = pd.DataFrame(index = dates) Step 2 Join it with the DataFrame of a stock dfAPPL = pd.read_csv(“apple.csv”) df = df.join(dfAPPL) Step 3 Drop no-trade dates df.dropna(subset=[column_name])

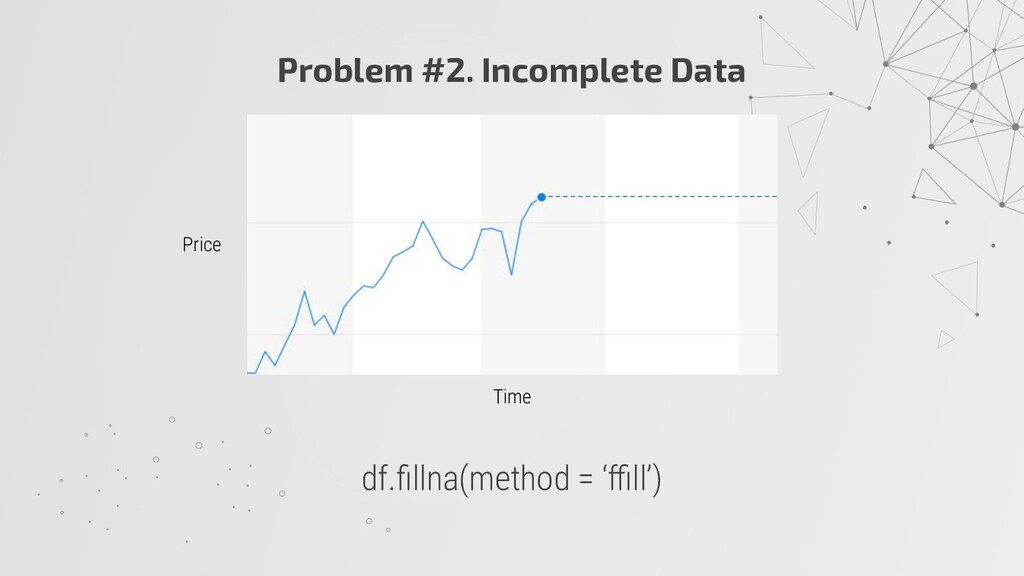

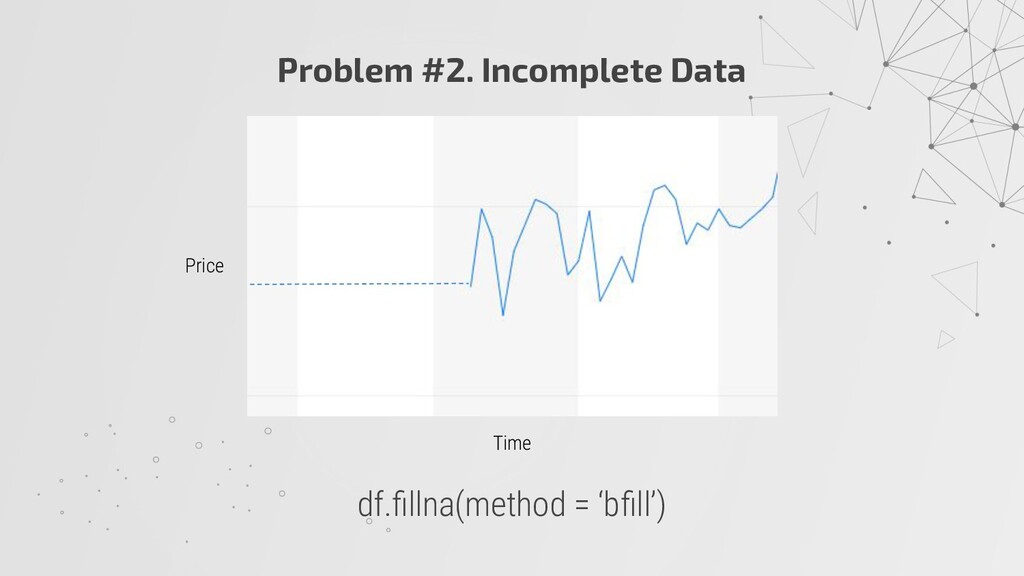

an empty DataFrame with the date range of your interest Step 2 Join it with the DataFrame of a stock Step 3 Drop the no-trade dates Step 4 Repeat Step 2 ~ Step 3 with remaining stocks Step 5 Fill forward missing values Step 6 Fill backward missing values

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Plotting Multiple Stocks in a Graph df / df[0] Time](https://files.speakerdeck.com/presentations/40a3777139aa4a5a8e6ae123fc67522d/slide_22.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}