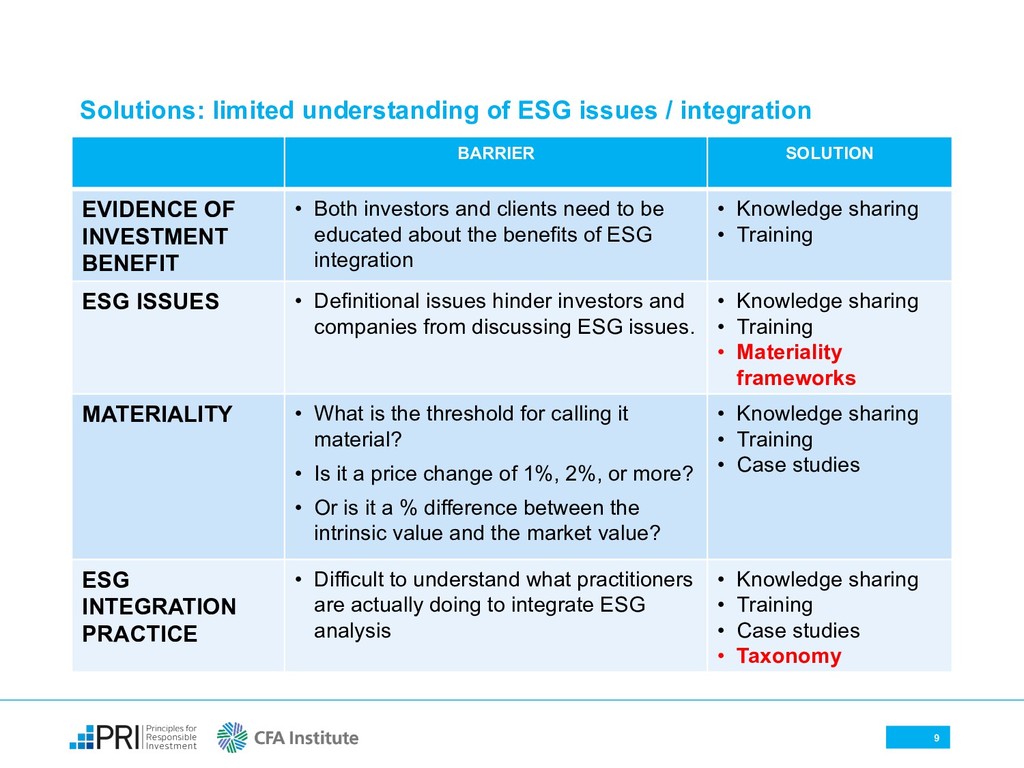

groups - CERES, CFA Institute, GIIN, GSIA, ICGN, UNEP-FI, PRI, FCLT - convene to speak with ‘a more unified voice’ on corporate ESG reporting § Work with a standard-setting group known as the Corporate Reporting Dialogue – CDP, CDSB, FASB, GRI, ISO, IFRS, IIRC, SASB - to incorporate material ESG-issues in accounting standards (starting with climate) § Ultimately, working towards a global, standardised and comparable reporting standard that includes ESG and ‘real-world impact’ ESG reporting by asset owners and investment managers 13 Solutions: lack of ESG data / limited ESG research

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}