RASE Report Background • Where the UK AD industry is • What has been happening in the on-farm AD sector • Barriers & benefits www.methanogen.co.uk [email protected]

Water, GHG Emissions, Applied Research & Farm-scale AD Seminars on novel technology applications (emissions & soil) Raising applied science profile across industry & rural sector Working with DEFRA, AEA, EA, NE, AHBD, BBSRC & REA www.rase.org.uk

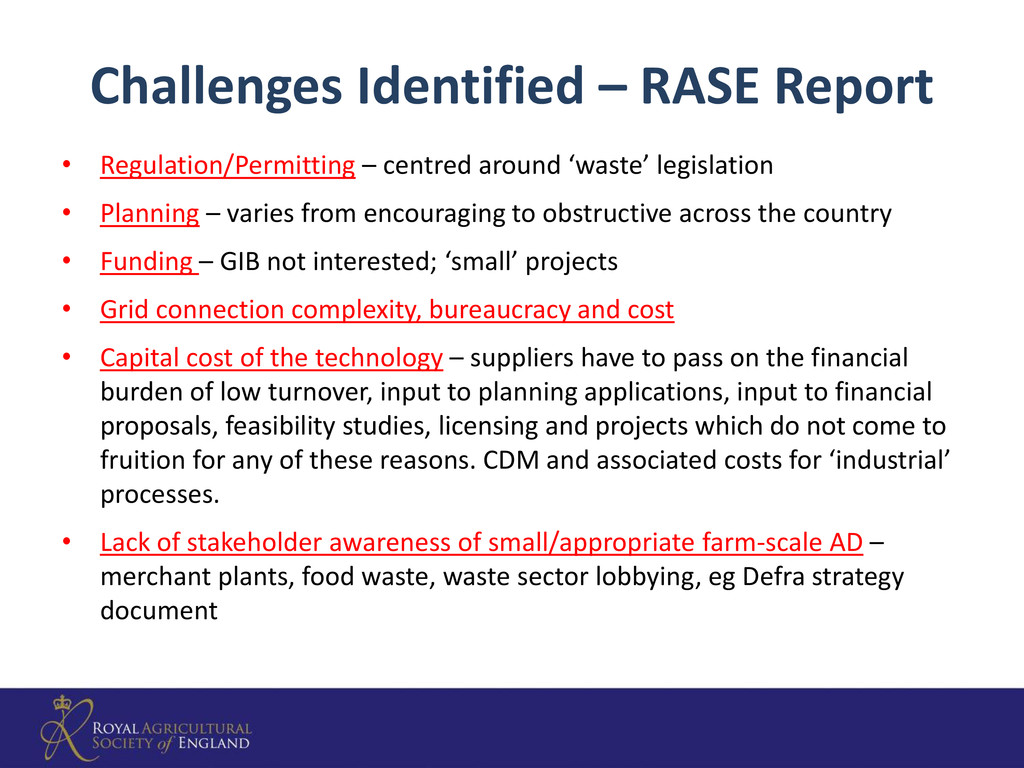

‘waste’ legislation • Planning – varies from encouraging to obstructive across the country • Funding – GIB not interested; ‘small’ projects • Grid connection complexity, bureaucracy and cost • Capital cost of the technology – suppliers have to pass on the financial burden of low turnover, input to planning applications, input to financial proposals, feasibility studies, licensing and projects which do not come to fruition for any of these reasons. CDM and associated costs for ‘industrial’ processes. • Lack of stakeholder awareness of small/appropriate farm-scale AD – merchant plants, food waste, waste sector lobbying, eg Defra strategy document

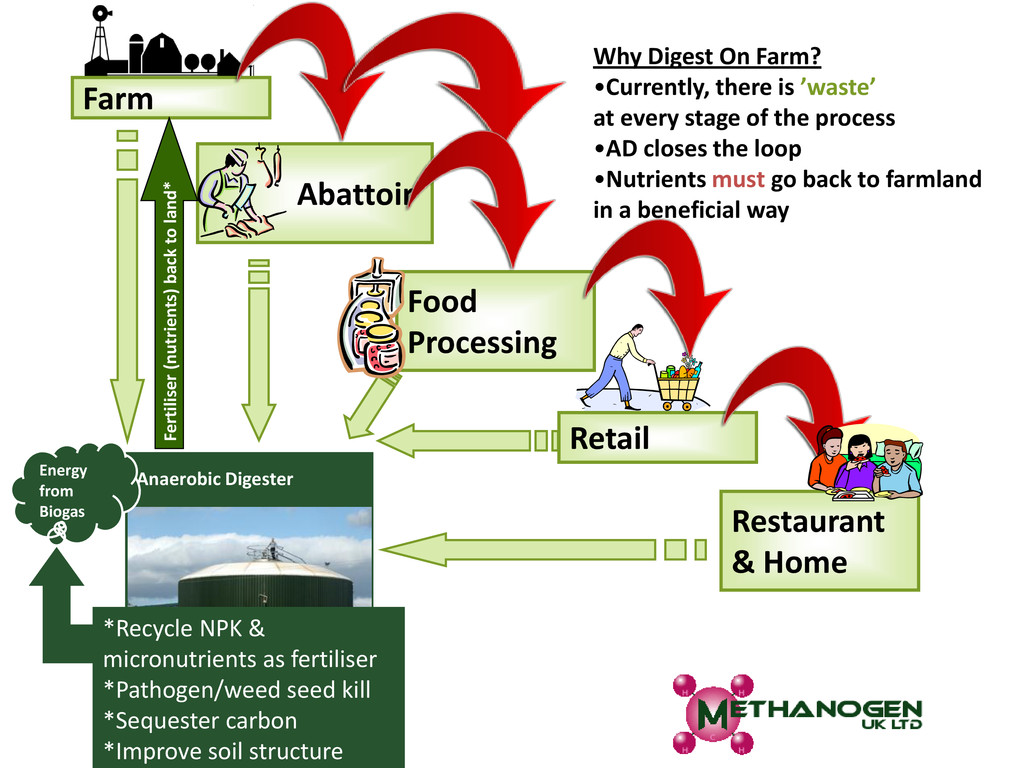

Why Digest On Farm? •Currently, there is ’waste’ at every stage of the process •AD closes the loop •Nutrients must go back to farmland in a beneficial way Energy from Biogas *Recycle NPK & micronutrients as fertiliser *Pathogen/weed seed kill *Sequester carbon *Improve soil structure Fertiliser (nutrients) back to land*

Reduction in carbon dioxide, nitrous oxide and methane losses to atmosphere greatly reduced GHG potential • Renewable energy production • Offensive odours eliminated • Reduction in BOD (80-95%) • Addition of humus improves the physical properties of soil water holding capacity, aeration, water soluble aggregates and increased crop production up to 20-30% www.methanogen.co.uk [email protected]

presentation AD is not just a Renewable Energy Technology Current incentives (FITs, RHI) do not value the carbon savings of digesting slurries, manures and other wasted agricultural by-products and co-products If 14.7p is for the electricity valuing all the positive externalities Would result in a FIT of 77.3p! Total savings of 2738kg CO2e www.methanogen.co.uk [email protected]

benefit is not just NPK, but significant and essential trace elements • Fertiliser performance is superior, as nutrients are more readily available, particularly Nitrogen • Digestate does not hinder clover growth like synthetic fertilisers. • Faster re-grazing – healthier animals • Increased ley life • Production of energy and fertiliser reduces costs of food production, improves profitability and adds an income stream to the farm www.methanogen.co.uk [email protected] Further Benefits:

and DECC: directly and through industry bodies (eg REA and ADBA). Critical to keep the industry growing, especially with long project lead times. • Links to Europe through suppliers and IEA Task 37 – “Don’t reinvent the wheel” • Defra AD Strategy document with a number of very useful outcomes: NNFCC Biogas-info site first place to start • Funding still remains an issue • Grid connection complexity, bureaucracy and cost. Still variable, but more help, including from companies such as Good Energy, Ecotricity • Work on digestate and quality through WRAP, REA, ADBA and associated bodies.

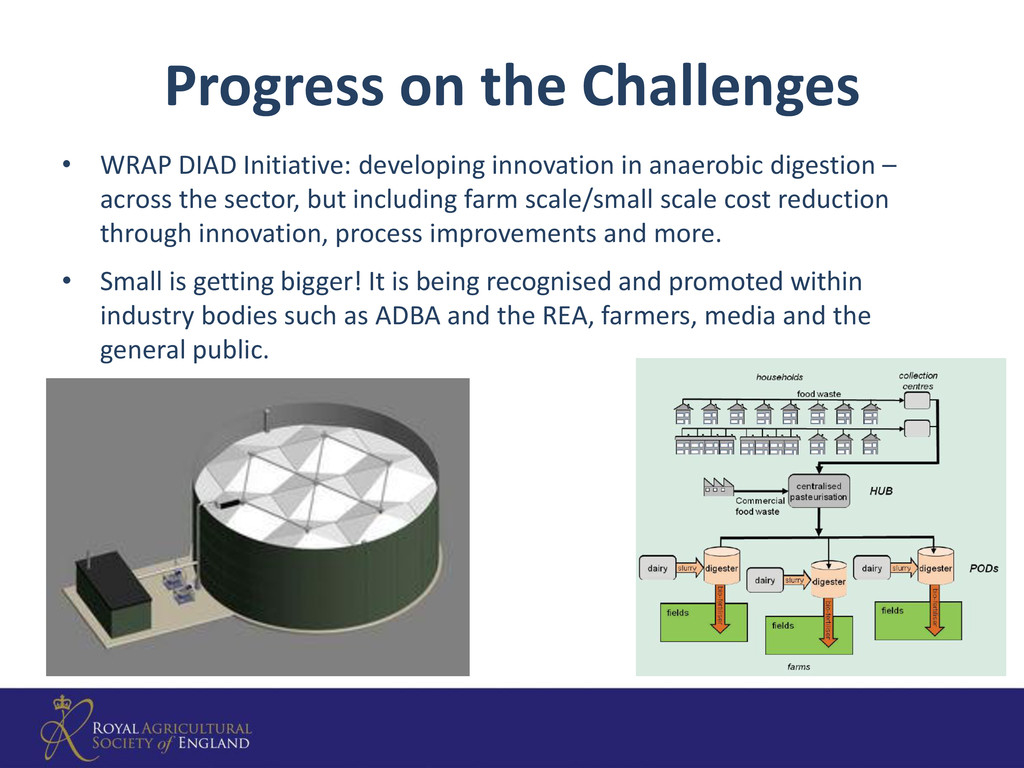

in anaerobic digestion – across the sector, but including farm scale/small scale cost reduction through innovation, process improvements and more. • Small is getting bigger! It is being recognised and promoted within industry bodies such as ADBA and the REA, farmers, media and the general public.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![www.methanogen.co.uk [email protected]](https://files.speakerdeck.com/presentations/6714eb705e760130f6bb22000a952b58/slide_11.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![www.methanogen.co.uk [email protected] Source: Defra 2010 Ag Stats Current Practice: Organic](https://files.speakerdeck.com/presentations/6714eb705e760130f6bb22000a952b58/slide_16.jpg){kind=link}

{kind=link}

![[1] ADBA R&D Conference, Nov 11, John Walsh, Bangor University](https://files.speakerdeck.com/presentations/6714eb705e760130f6bb22000a952b58/slide_18.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

![Angie Bywater Methanogen (UK) Ltd [email protected] www.methanogen.co.uk M: 07753 571371](https://files.speakerdeck.com/presentations/6714eb705e760130f6bb22000a952b58/slide_22.jpg){kind=link}

{kind=link}