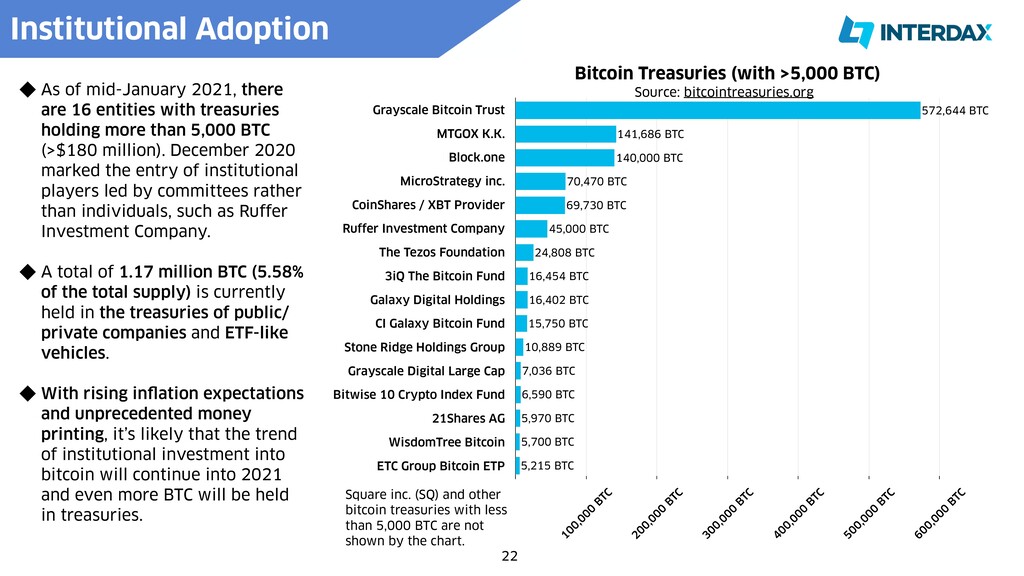

Trust MTGOX K.K. Block.one MicroStrategy inc. CoinShares / XBT Provider Ruffer Investment Company The Tezos Foundation 3iQ The Bitcoin Fund Galaxy Digital Holdings CI Galaxy Bitcoin Fund Stone Ridge Holdings Group Grayscale Digital Large Cap Bitwise 10 Crypto Index Fund 21Shares AG WisdomTree Bitcoin ETC Group Bitcoin ETP 100,000 BTC 200,000 BTC 300,000 BTC 400,000 BTC 500,000 BTC 600,000 BTC 5,215 BTC 5,700 BTC 5,970 BTC 6,590 BTC 7,036 BTC 10,889 BTC 15,750 BTC 16,402 BTC 16,454 BTC 24,808 BTC 45,000 BTC 69,730 BTC 70,470 BTC 140,000 BTC 141,686 BTC 572,644 BTC Source: bitcointreasuries.org As of mid-January 2021, there are 16 entities with treasuries holding more than 5,000 BTC (>$180 million). December 2020 marked the entry of institutional players led by committees rather than individuals, such as Ruffer Investment Company. A total of 1.17 million BTC (5.58% of the total supply) is currently held in the treasuries of public/ private companies and ETF-like vehicles. With rising in f l ation expectations and unprecedented money printing, it’s likely that the trend of institutional investment into bitcoin will continue into 2021 and even more BTC will be held in treasuries. Square inc. (SQ) and other bitcoin treasuries with less than 5,000 BTC are not shown by the chart.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Contact: ‣ [email protected] ‣ Twitter ‣ Medium ‣ Telegram](https://files.speakerdeck.com/presentations/fca15a9c97c1447685c719c78181b6a7/slide_26.jpg){kind=link}