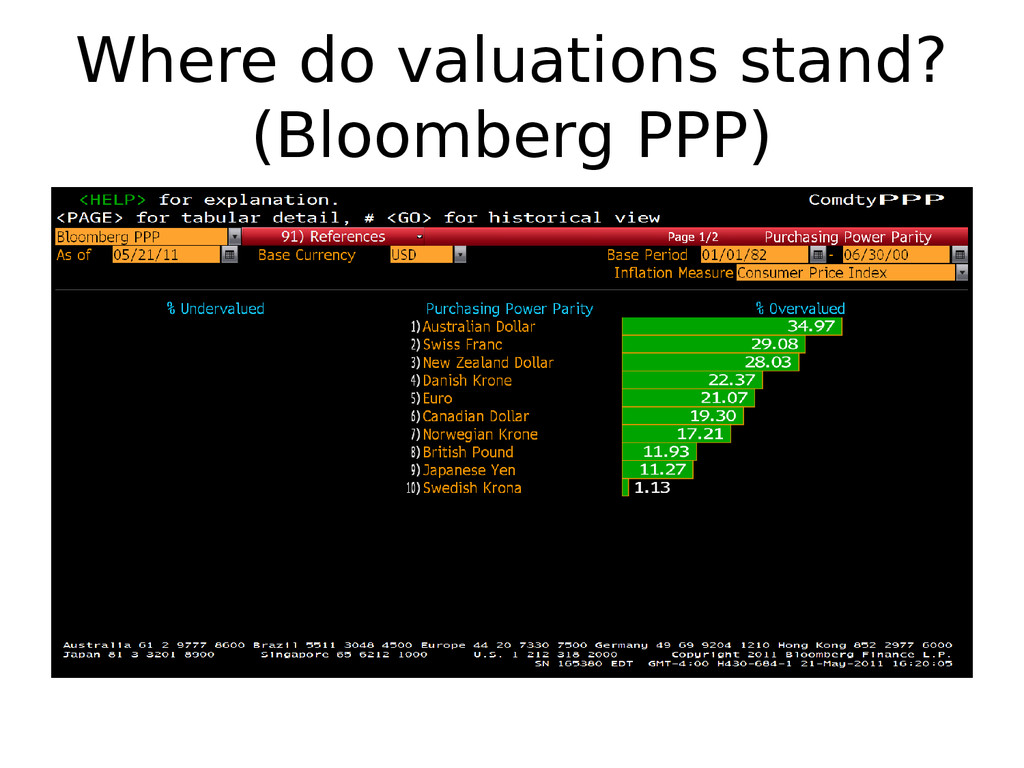

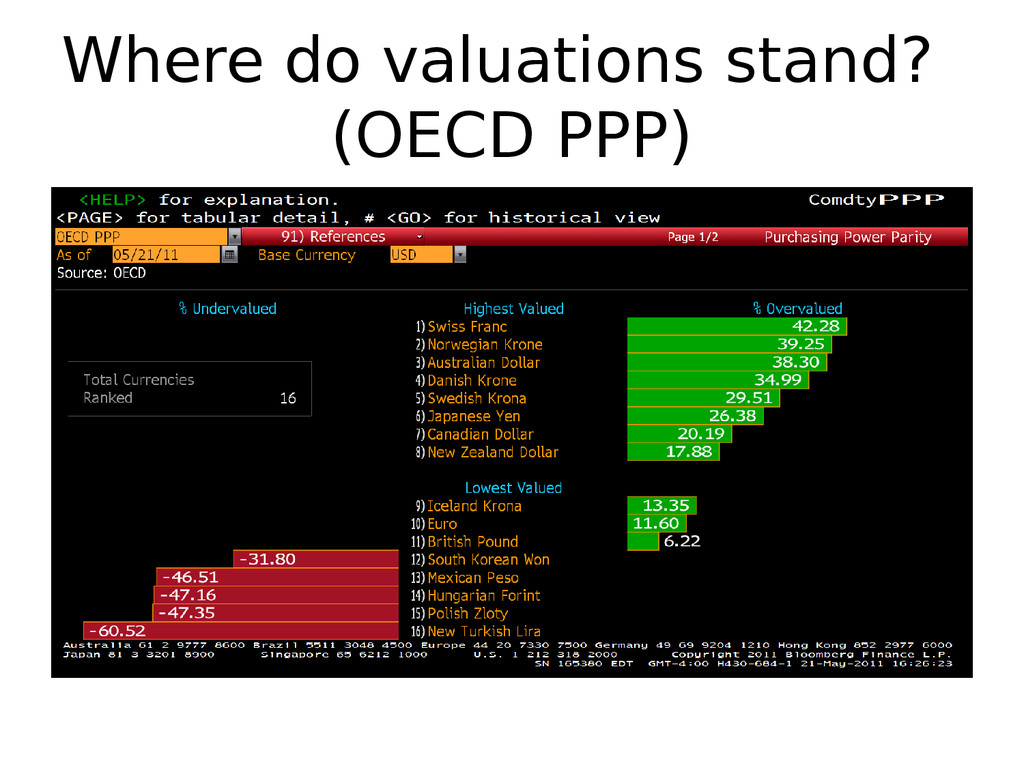

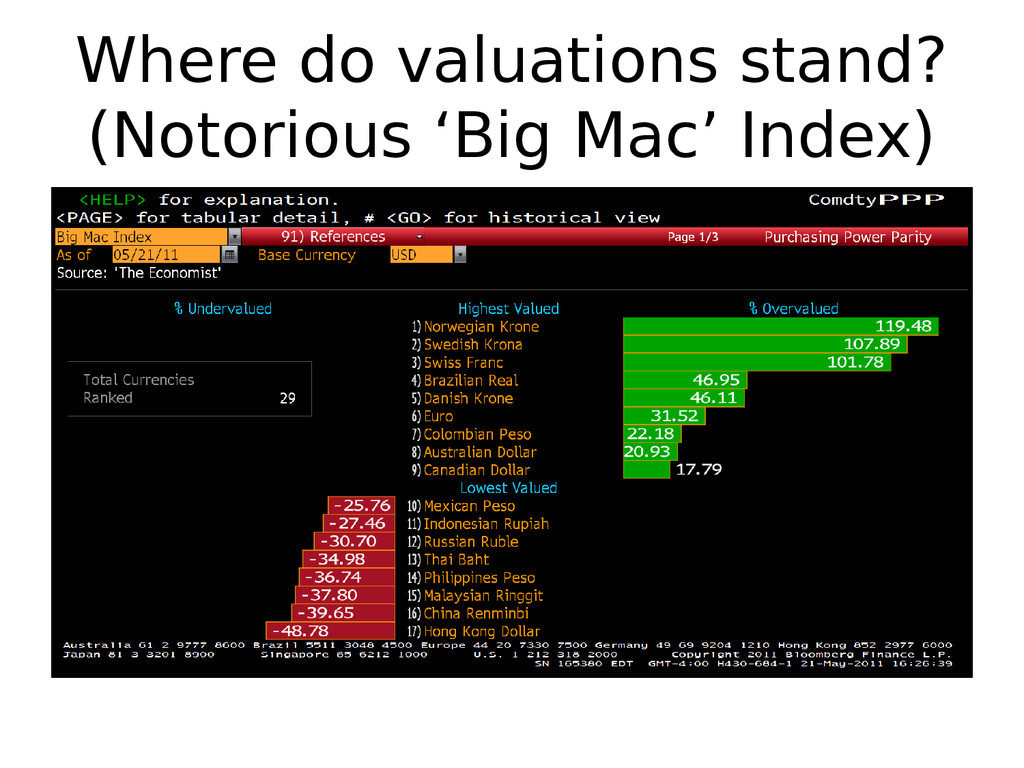

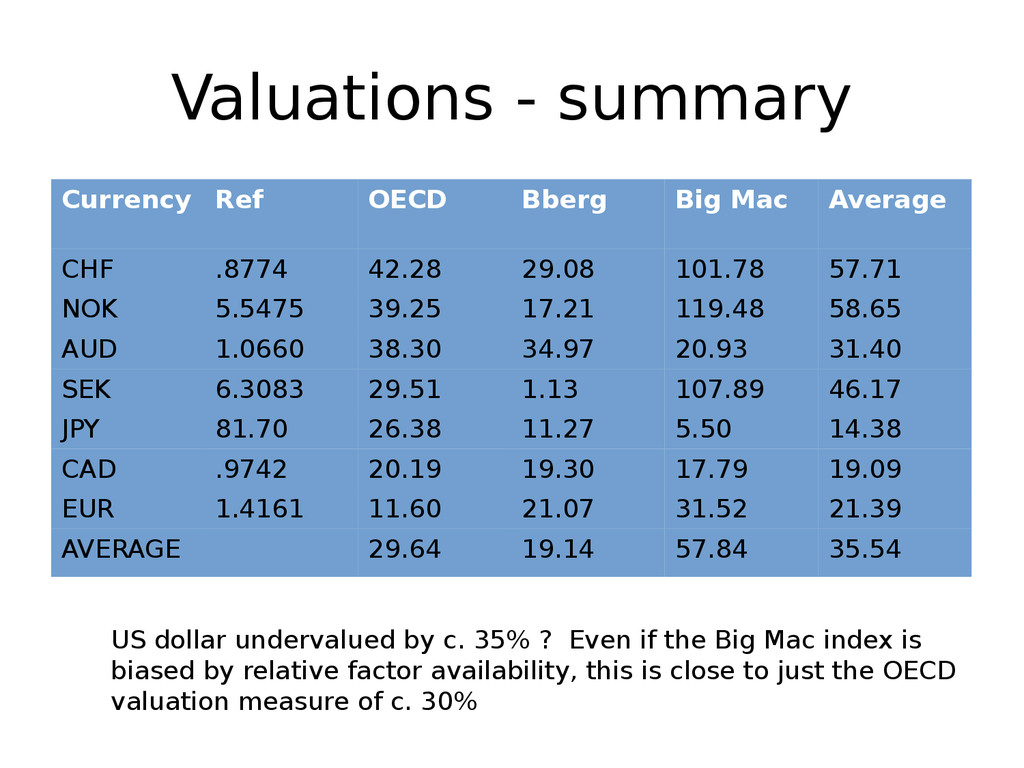

CHF .8774 42.28 29.08 101.78 57.71 NOK 5.5475 39.25 17.21 119.48 58.65 AUD 1.0660 38.30 34.97 20.93 31.40 SEK 6.3083 29.51 1.13 107.89 46.17 JPY 81.70 26.38 11.27 5.50 14.38 CAD .9742 20.19 19.30 17.79 19.09 EUR 1.4161 11.60 21.07 31.52 21.39 AVERAGE 29.64 19.14 57.84 35.54 US dollar undervalued by c. 35% ? Even if the Big Mac index is biased by relative factor availability, this is close to just the OECD valuation measure of c. 30%

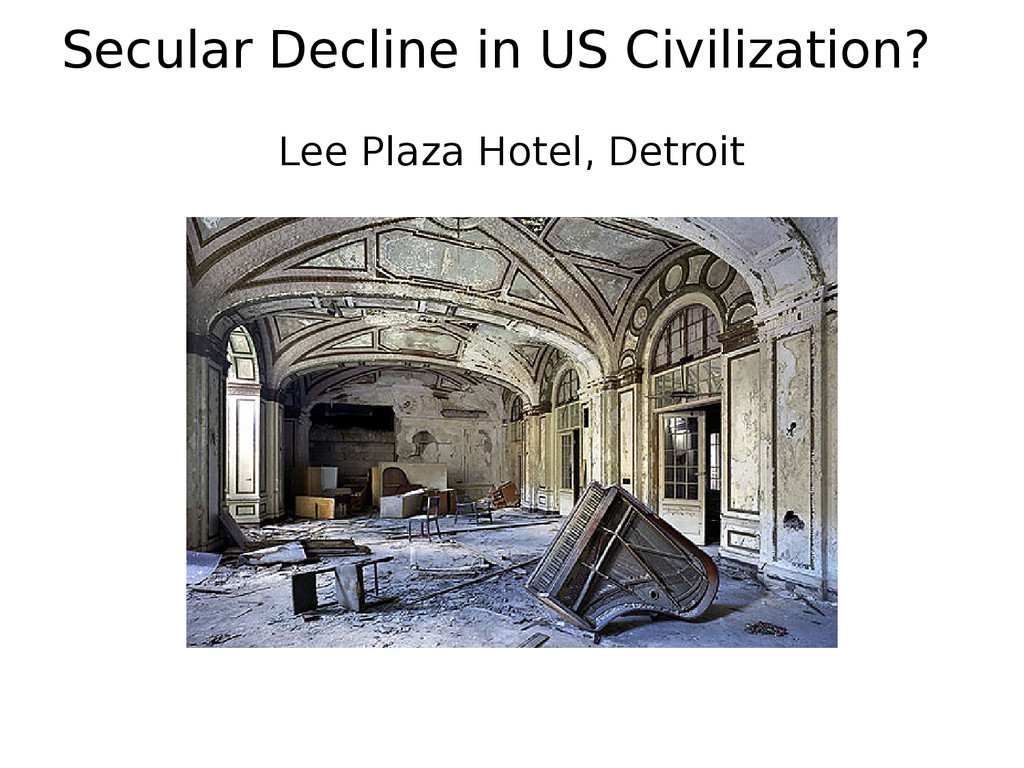

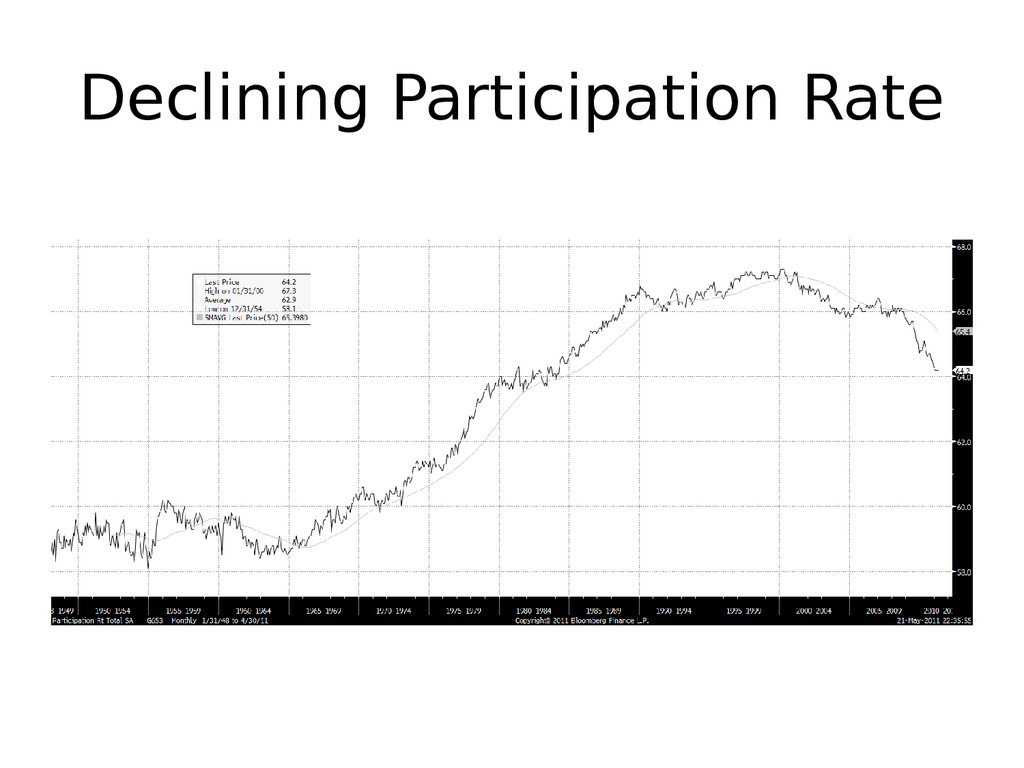

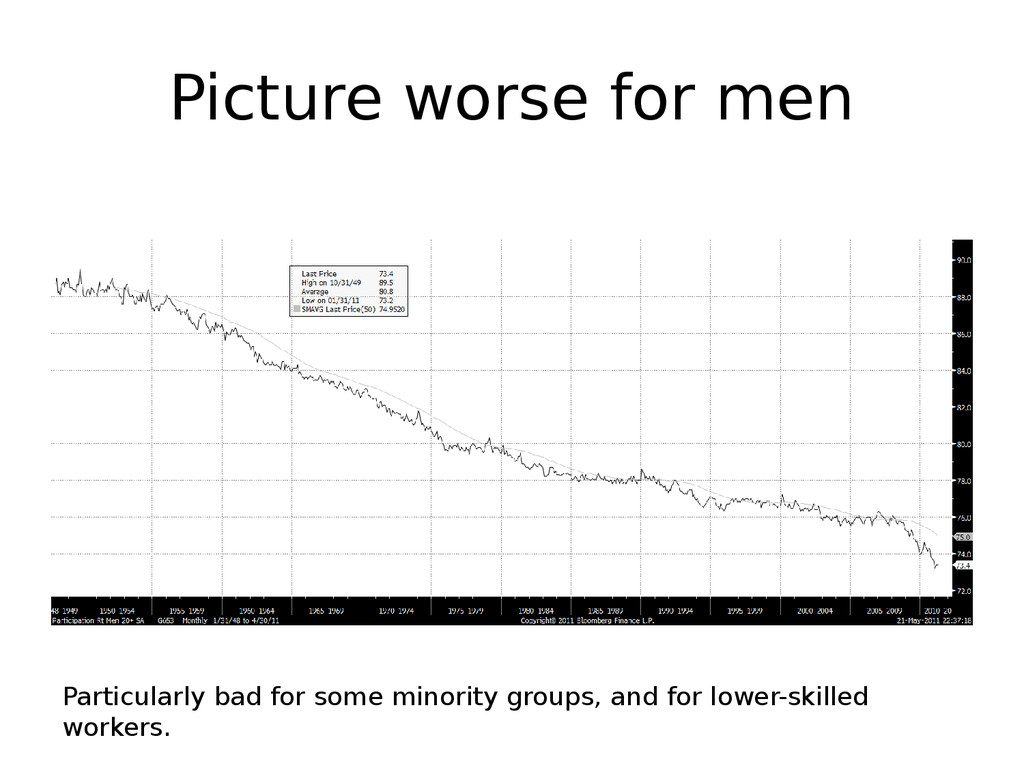

short the dollar? • Chronic current account deficit • Unmanageable debt load (public and private) vs GDP • Japanese experience suggests deleveraging will require monetary policy support for years to come to support GDP growth. QE 3, 4, 5 ? • Very polarized political scene, disturbing lack of social cohesion suggests taking tough decisions will be hard. Majority of households do not pay income tax! Political swing away from policy elite towards a more populist direction (‘Tea Party’ ascendancy). Republicans playing chicken with Democrats over the budget – risk of threatening US credibility and prestige in bond market. Black swan possibility of a technical default? • Secular decline in US civilization accompanied by a genuine ascendancy of the emerging world. Declining moral qualities (restraint, willingness to sacrifice for the future), loss of optimism. Is the American Dream dead? Wages in emerging world still cheap in USD terms vs those of US workers. • Stagnant real wages since 1970s; declining overall participation rate since 2000 – very much worse for men, particularly those from minority groups (that are in the sample statistically less skilled). • Iraq, Afghanistan, Libya. Wherever next ?

governs his behavior either because he cannot discipline himself to sacrifice a present for a future satisfaction or because he has no sense of the future. He is therefore radically improvident.'' - Edward C Banfield, The Unheavenly City Why did interest rates rise in the twentieth century? “The social time preference schedule must have shifted upward. That is, the character of the population must have changed. People on the average must have lost in moral and intellectual strength and become more present-oriented.” - Dr Hans Hermann Hoppe, Democracy: the God that Failed

world ought to be. Philosophy in any case always comes on the scene too late to give it... When philosophy paints its gloomy picture then a form of life has grown old. It cannot be rejuvenated by the gloomy picture, but only understood. Only when the dusk starts to fall does the owl of Minerva spread its wings and fly. —G.W.F. Hegel, Preface to Philosophy of Right (1820) In other words, all this has already happened. But what of the future?

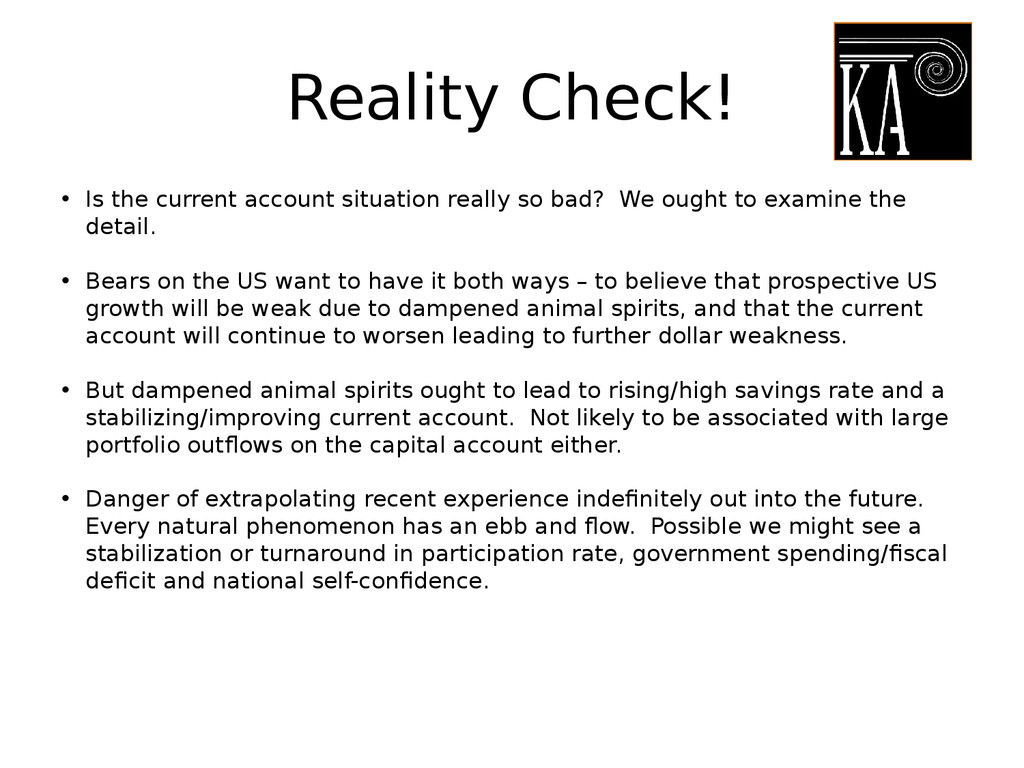

bad? We ought to examine the detail. • Bears on the US want to have it both ways – to believe that prospective US growth will be weak due to dampened animal spirits, and that the current account will continue to worsen leading to further dollar weakness. • But dampened animal spirits ought to lead to rising/high savings rate and a stabilizing/improving current account. Not likely to be associated with large portfolio outflows on the capital account either. • Danger of extrapolating recent experience indefinitely out into the future. Every natural phenomenon has an ebb and flow. Possible we might see a stabilization or turnaround in participation rate, government spending/fiscal deficit and national self-confidence.

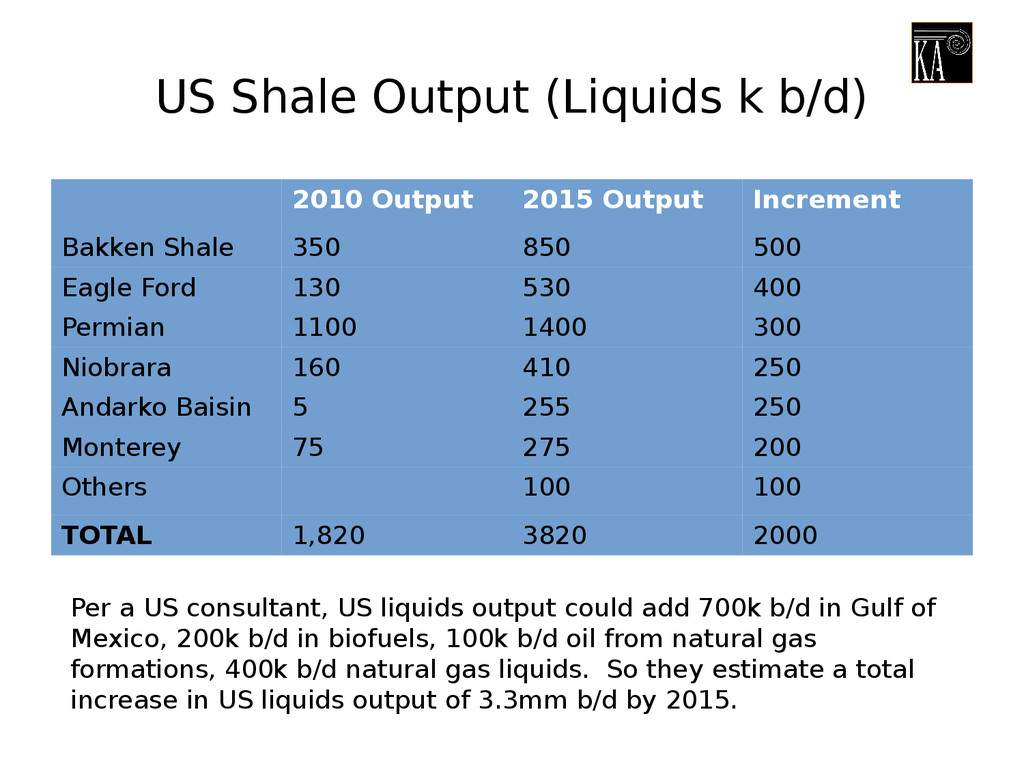

Increment Bakken Shale 350 850 500 Eagle Ford 130 530 400 Permian 1100 1400 300 Niobrara 160 410 250 Andarko Baisin 5 255 250 Monterey 75 275 200 Others 100 100 TOTAL 1,820 3820 2000 Per a US consultant, US liquids output could add 700k b/d in Gulf of Mexico, 200k b/d in biofuels, 100k b/d oil from natural gas formations, 400k b/d natural gas liquids. So they estimate a total increase in US liquids output of 3.3mm b/d by 2015.

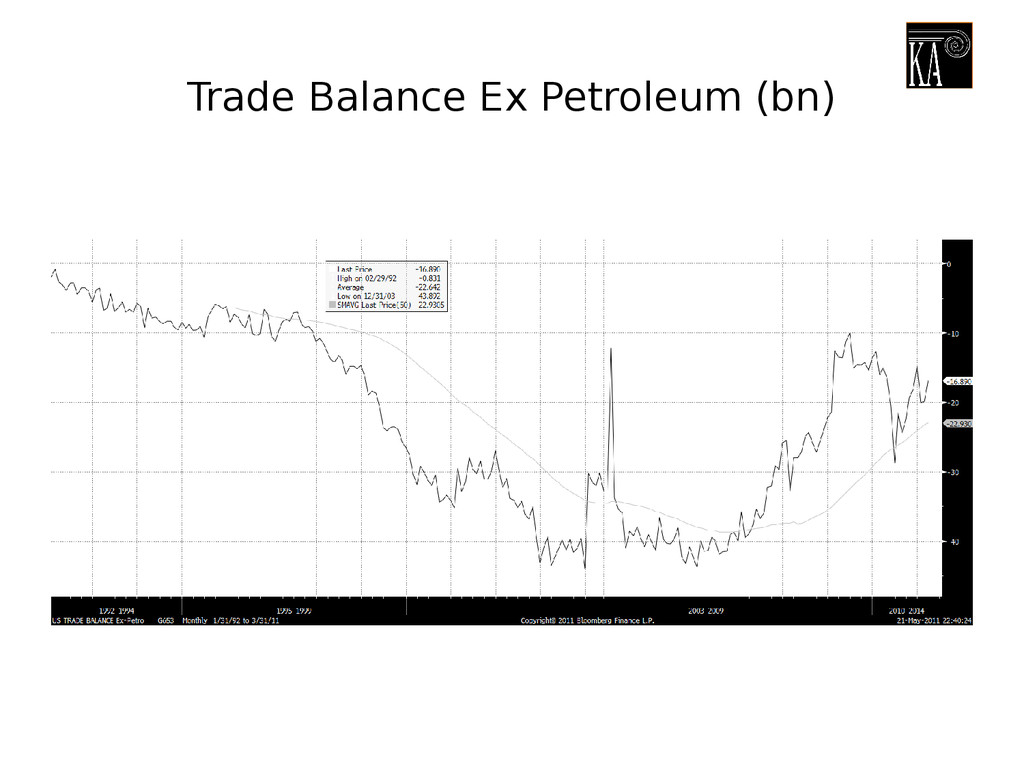

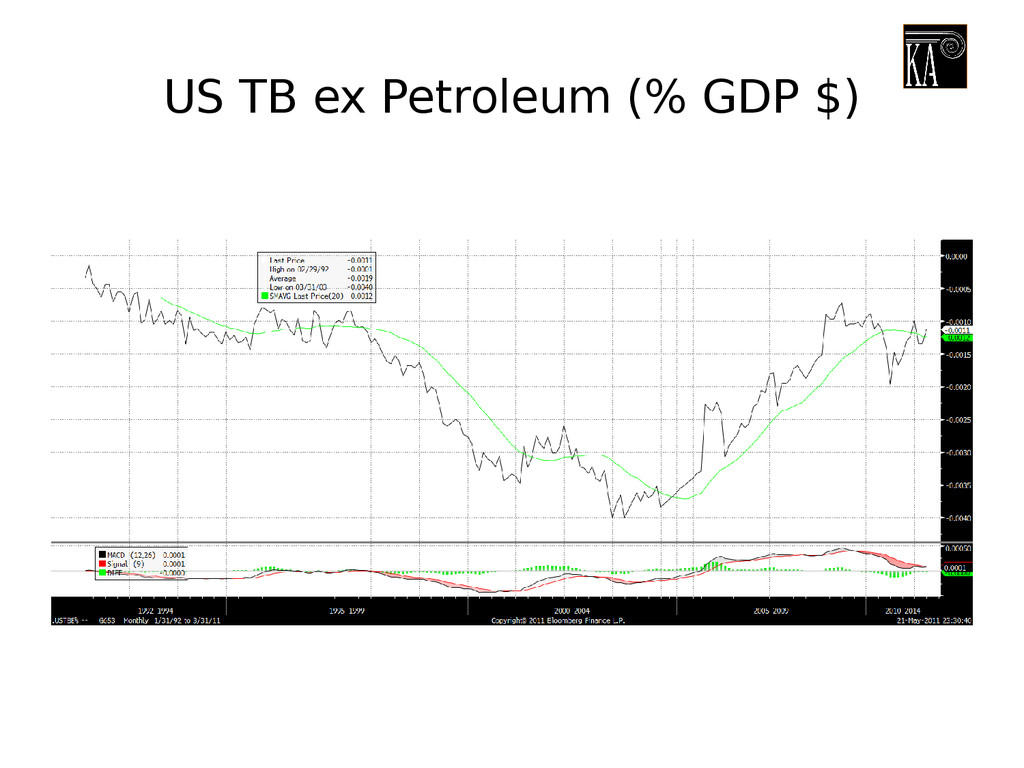

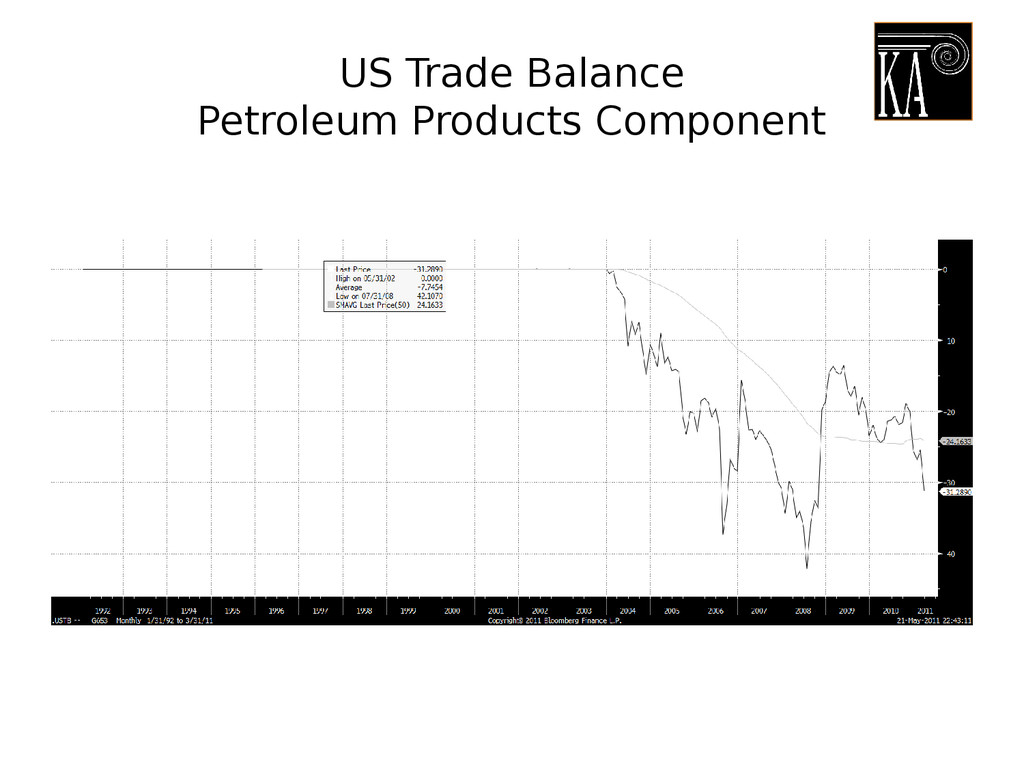

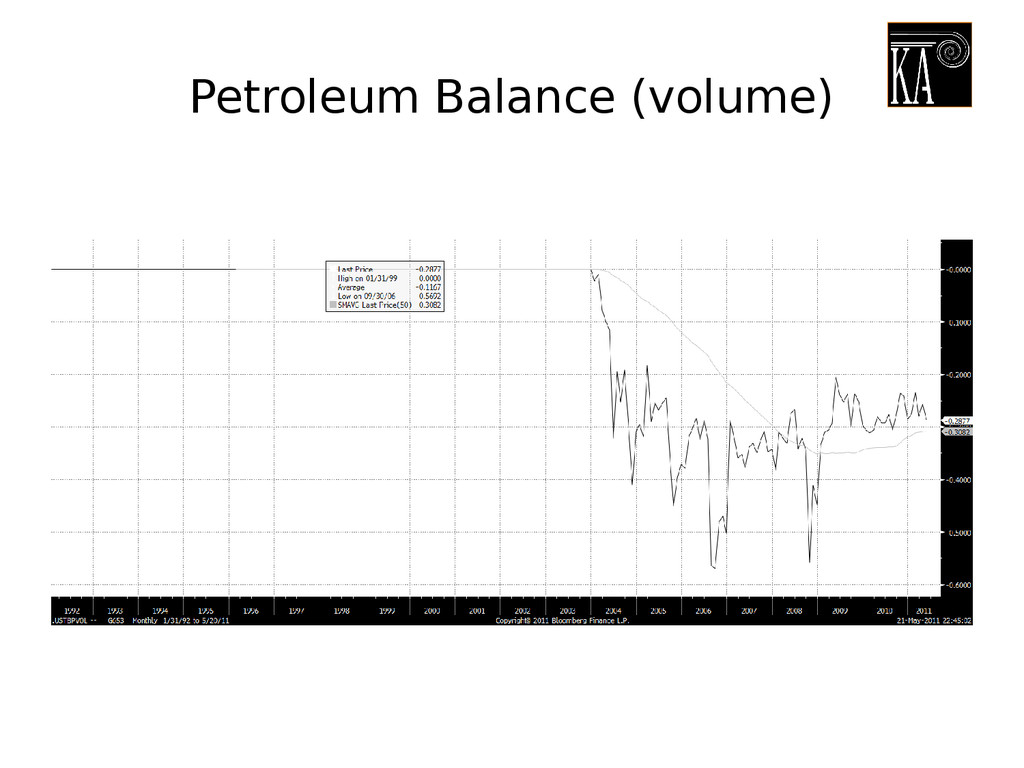

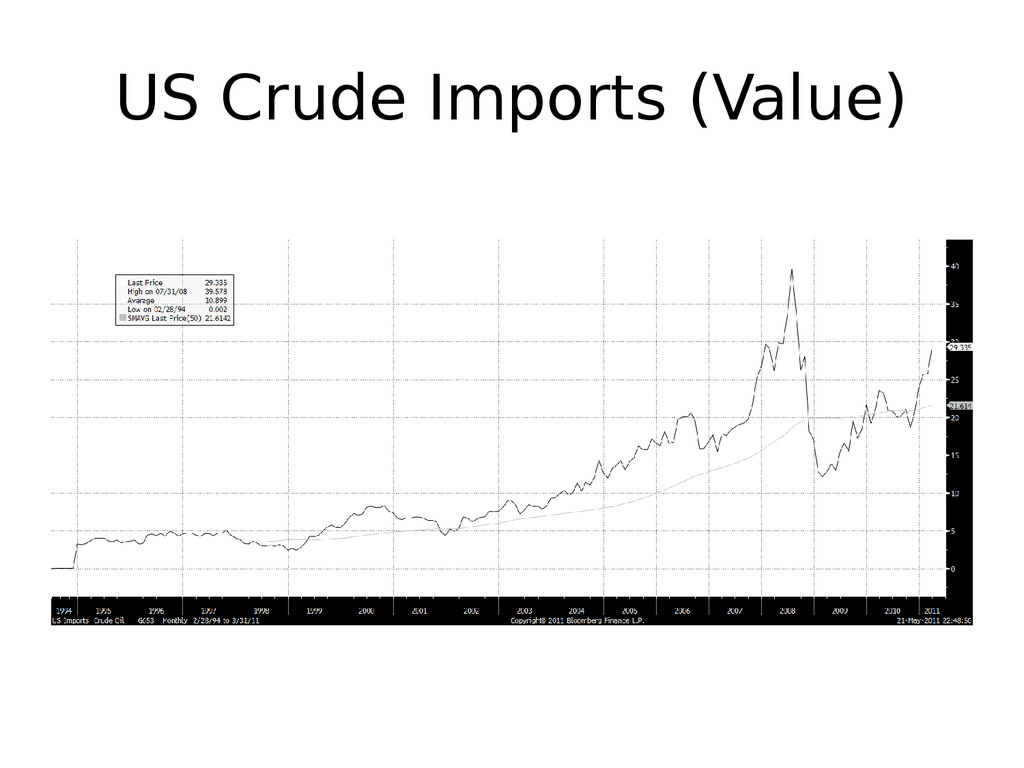

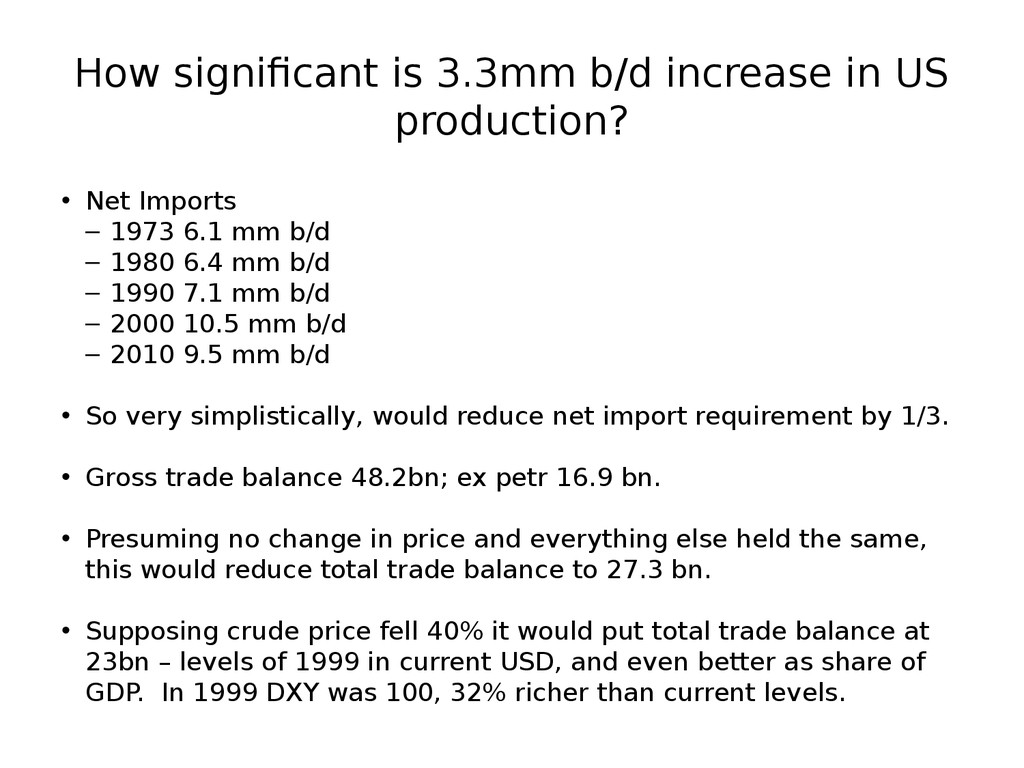

Net Imports – 1973 6.1 mm b/d – 1980 6.4 mm b/d – 1990 7.1 mm b/d – 2000 10.5 mm b/d – 2010 9.5 mm b/d • So very simplistically, would reduce net import requirement by 1/3. • Gross trade balance 48.2bn; ex petr 16.9 bn. • Presuming no change in price and everything else held the same, this would reduce total trade balance to 27.3 bn. • Supposing crude price fell 40% it would put total trade balance at 23bn – levels of 1999 in current USD, and even better as share of GDP. In 1999 DXY was 100, 32% richer than current levels.

Scope for pricing out rate hikes as periphery continues to deteriorate, particularly if inflation concerns recede. • Greece cannot possibly pay back its government debt. • Nascent shift to radical right means that time is running out for EU integrationists. Bailouts politically unpopular, and EU fiscal union seems very far away.

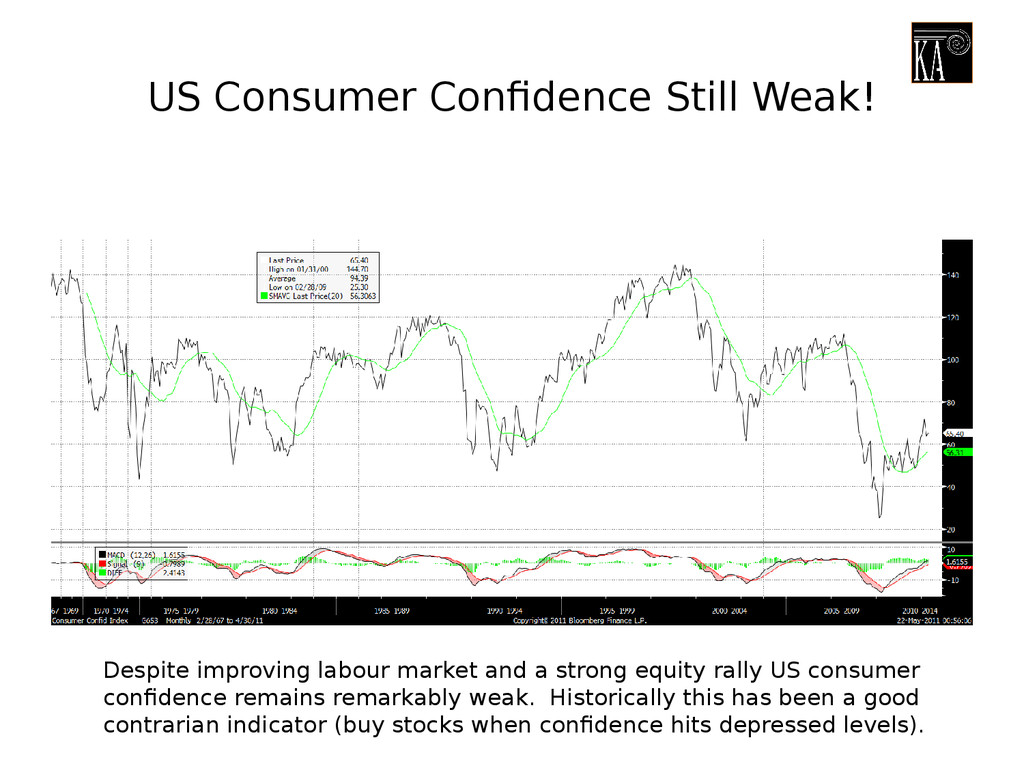

a strong equity rally US consumer confidence remains remarkably weak. Historically this has been a good contrarian indicator (buy stocks when confidence hits depressed levels).

Perhaps because of elevated gasoline (and other commodity) prices. This has been a focus of much popular discontent towards the Fed. • Most bullish phase for commodities is abundant liquidity and relative weak growth. Ie crude is high because dollar is weak and because the effective Fed Funds rate is low. • The effective Fed Funds rate is low in part because consumer (and business) confidence is weak. • Headline and core inflation both currently low. Tightening in rental market (vacancy rate was 12%; now 9.5%, 2012 5%) implies pickup in the large OER and tenant’s rent component of CPI. Core inflation 1.8% by year end 2011 according to DB. • QE2 ends shortly. A pickup in hiring and spending would be associated with upward revisions to interest rate expectations, which would tend to support the dollar and weaken gas prices – which would tend to lead to improving consumer confidence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}