M. Ametrano Politecnico di Milano, Milano Bicocca University Consob, Rome, November 22, 2016 [email protected] @Ferdinando1970 http://www.slideshare.net/Ferdinando1970 https://it.linkedin.com/in/ferdinandoametrano

– prohibits financial institutions from trading, underwriting, or offering insurance in bitcoins or any other digital currency – Bitcoin is not to be considered a currency – owning bitcoins is not outlawed or prohibited • As of December 2013 BTC China was world's largest Bitcoin exchange by volume • Alibaba, China's top Internet retailer, stopped using bitcoins as of January 19 2014 5/80

Mt Gox was world's largest Bitcoin exchange by volume • In February 2014 it filed for bankruptcy protection from creditors • It announced that around 850,000 bitcoins belonging to customers and the company were missing and likely stolen, an amount valued at more than $450 million at the time • Fraud or theft? 6/80

service • Online users were able to buy illicit goodies using bitcoins, while browsing it anonymously and securely without potential traffic monitoring • Launched in February 2011, shut down in October 2013 • Ross William Ulbricht, alleged to be the owner of Silk Road, arrested in San Francisco, sentenced to life in prison • Other black markets have filled in as successors 7/80

• Just 7 years old • Without government or corporation backing • That can lose its main (China) market • With fraud/theft at its main reference exchange (Mt Gox) • With such a bad reputation (Silk Road) • That could be still alive and kicking? 8/80

or organization • Instantaneous peer-to-peer transactions • No need for trusted third party • Cryptographic security • Low-cost banking for everybody everywhere https://bitcoin.org/en/faq http://www.coindesk.com/information/ 10/80

only exist as public ledger documented transactions • A bitcoin wallet is a public address • 1FEz167JCVgBvhJBahpzmrsTNewhiwgWVG • the bitcoin public ledger (aka blockchain) certifies for everybody how many bitcoins are associated to the wallet http://blockexplorer.com/address/1FEz167JCVgBvhJBahpzmrsTNewhiwgWVG It is mine; you are REALLY encouraged to tip 11/80

The public key does not provide direct information about the private key owner • All transactions are transparent to everybody’s inspection. • Perfect persistent public account history: the public ledger is forever https://blockchain.info/ http://blockexplorer.com/ 13/80

in blocks, sequentially chained, about one block every 10 minutes • The block chain is a history of transactions resilient to network attackers • The cryptographic link between blocks requires large amount of computing power, so the block chain cannot be altered without huge resources • Computing power is measured in hash/s, hash being the basic operation needed for validation 14/80

the computing power for: – processing and validating transactions (avoiding double spending) – securing the network – synchronizing the nodes • Miners compete to process a new block of transactions. The winner provides a proof-of-work and is rewarded with the issue of new bitcoins. • Seigniorage revenues subsidize the network, making transaction almost free 16/80

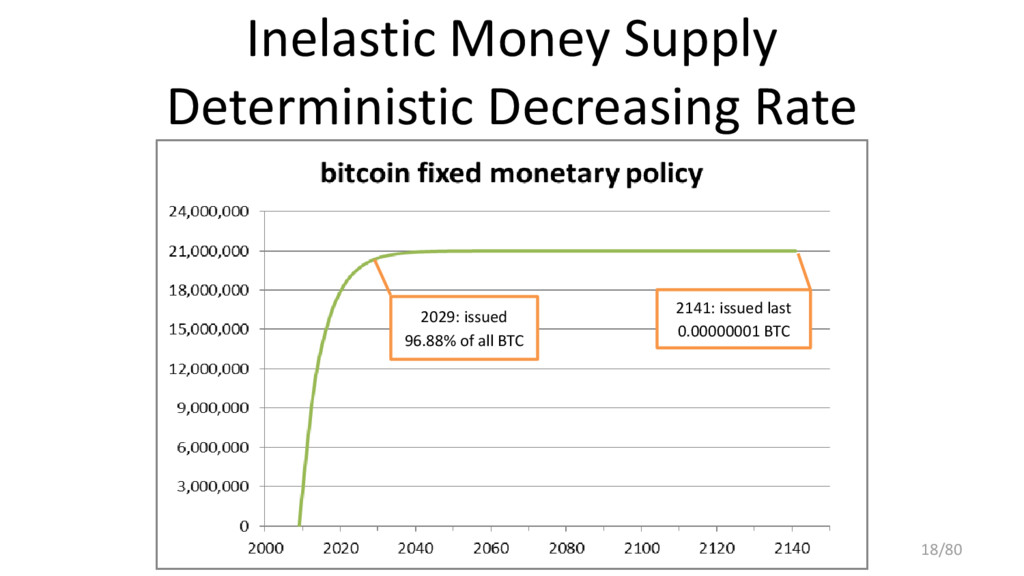

halving every 4Y • This is the only way new bitcoins are released • It is called mining because of its similarity with the progressive scarcity of gold extraction digital cash supply free of discretionary intervention 17/80

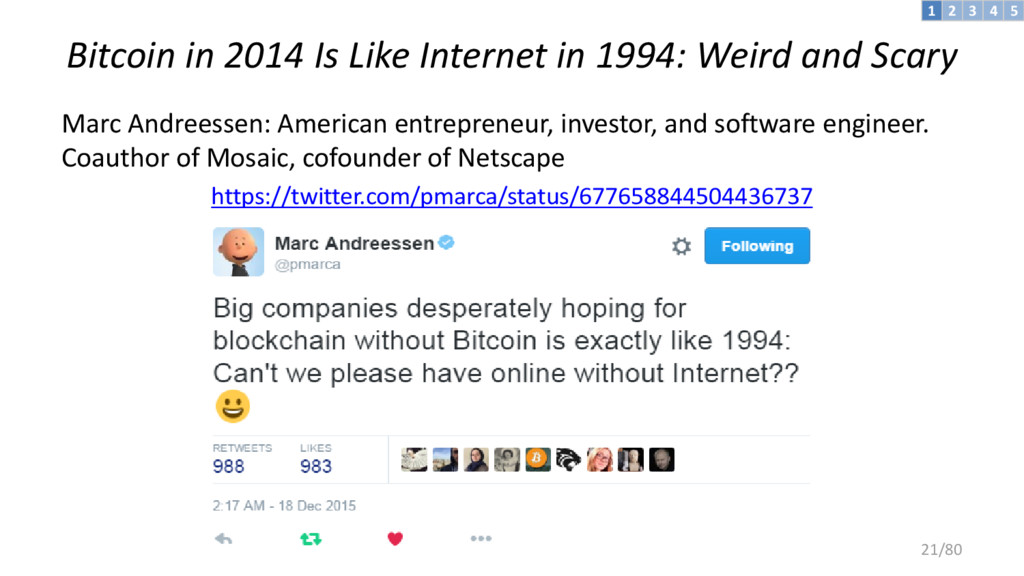

Scary Marc Andreessen: American entrepreneur, investor, and software engineer. Coauthor of Mosaic, cofounder of Netscape https://twitter.com/pmarca/status/677658844504436737 3 4 5 2 1 21/80

and services • Offered in the late ‘90s and early ‘00s by Compuserve, AOL (and to some extent MSN) • Corporates wanted to go online, but not in the wild unregulated internet, populated by anonymous agents • They eventually realized that perceived risks, which are real, are outweighed by benefits 22/80

however lags well behind the hype, amongst practitioners, policy makers and industry commentators alike. ‘Blockchain’ technology seems to promise major change for capital markets and other financial services – some say it may ultimately prove to be as important an innovation as the internet itself – but few can say exactly how or why. Michael Mainelli, Alistair Milne (2016) The Impact and Potential of Blockchain on the Securities Transaction Lifecycle http://ssrn.com/abstract=2777404 23/80

1. Game theory 2. Cryptography 3. Computer networking and data transmission 4. Economic and monetary theory Mainly not a technology, a cultural paradigm shift instead 24/80

blocks] • An append-only sequential data structure • New blocks can only be appended at the end of the chain • To change a block in the middle of the chain, all subsequent blocks need to be changed • Very inefficient compared to a relational database 25/80

transactions • Massively duplicated across network nodes • Shared with a P2P file transfer protocol • Updated by peculiar nodes, known as miners, appending new blocks of transactions 26/80

and clearing. • Miners perform the additional work required for settlement. How do they reach consensus on the transaction history? • Consensus in a distributed network with faulty (or malicious) nodes is a very hard problem known as Byzantine General Problem 27/80

incentive for the mining nodes to be honest • Miners are compensated for their proof-of- work using seigniorage revenues, i.e. with issuance of new bitcoins 28/80

asset available to reward miners Appointed validator officials required Why should validators use a blockchain, i.e. a subpar data structure, instead of a database? 29/80

by the first (and most relevant so far) blockchain • It exists only as scriptural asset, i.e. validated transaction recorded on the blockchain • It is a bearer instrument: the (private key) holder is the actual effective owner 30/80

realm, as nothing else before • It can be transferred but not duplicated • (i.e. it can be spent, but not double-spent) Bitcoin is digital gold: this is the brilliant groundbreaking achievement by Satoshi Nakamoto 31/80

• Its adoption was not centrally planned • For centuries it has been the most successful form of money • It has bootstrapped all monetary systems we know of • It has been surpassed by other kind of money without becoming obsolete bitcoin • Its adoption has not been centrally planned • It is the most successful form of cryptocurrency • It will bootstrap new monetary systems • It might be surpassed by more advanced type of cryptocurrencies without becoming obsolete 32

value (legal tender, social contract) • Currency based on paper/ink security • Discretionary governance • Wicksellian interest-rate approach bitcoin • No intrinsic value (digital gold) • Currency based on math/cryptographic security • Algorithmic governance • Deterministic supply 34

born into a gift economy 2. Enlarged relationship circle requires exchange economy 3. Barter economy: coincidence of wants 4. Trade economy: money as medium of exchange 5. Global information economy: supranational digital money 35/80

cost • Why pay a fee to move bytes representing wealth? • Why only 9-5, Monday-Friday? • Who (and when) will gift humanity with a global instantaneous free p2p payment network? BANK 36/80

• Permissionless: no regulator • Censorship resistant: no frozen funds • Open-access: no discrimination, no amount limits, 24/7, 365 days • Free: negligible transaction costs • Borderless: no geographic limits • Transnational: no specific jurisdiction applies • Secure: non falsifiable, non repudiable transactions • Resilient: nothing has been able to stop it or break it 37/80

the commodity money standard – resistance to corrosion and oxidation – high malleability – relative easiness of purity assessment – Pleasant color • Gold purity certification • Representative money • Fractional receipt money • Fiat money and legal tender 38/80

of coinage is an almost uninterrupted story of debasements; history is largely a history of inflation engineered by governments for their gain • why government monopoly of the provision of money is regarded as indispensable? It deprived public of the opportunity to discover and use a better reliable money Blessed will be the day when it will no longer be from the benevolence of the government that we expect good money but from the regard of the banks for their own interest A Free-Market Monetary System, Gold and Monetary Conference, New Orleans, Nov. 1977, https://mises.org/daily/3204 Hayek, F. A., Denationalisation of Money, The Institute of Economic Affairs,http://www.mises.org/books/denationalisation.pdf 39/80

no barrier to enter, no editorial control – Email has not been designed by a consortium of postal agencies – Internet has not been developed by a consortium of telcos • Will a decentralized transactional economy be shaped by a consortium of banks? 40/80

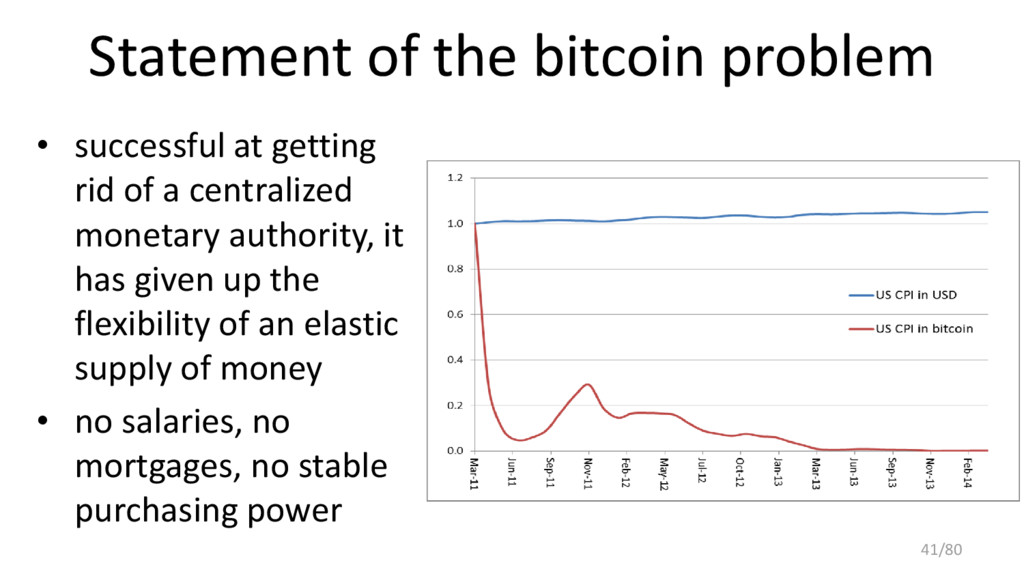

of a centralized monetary authority, it has given up the flexibility of an elastic supply of money • no salaries, no mortgages, no stable purchasing power 41/80

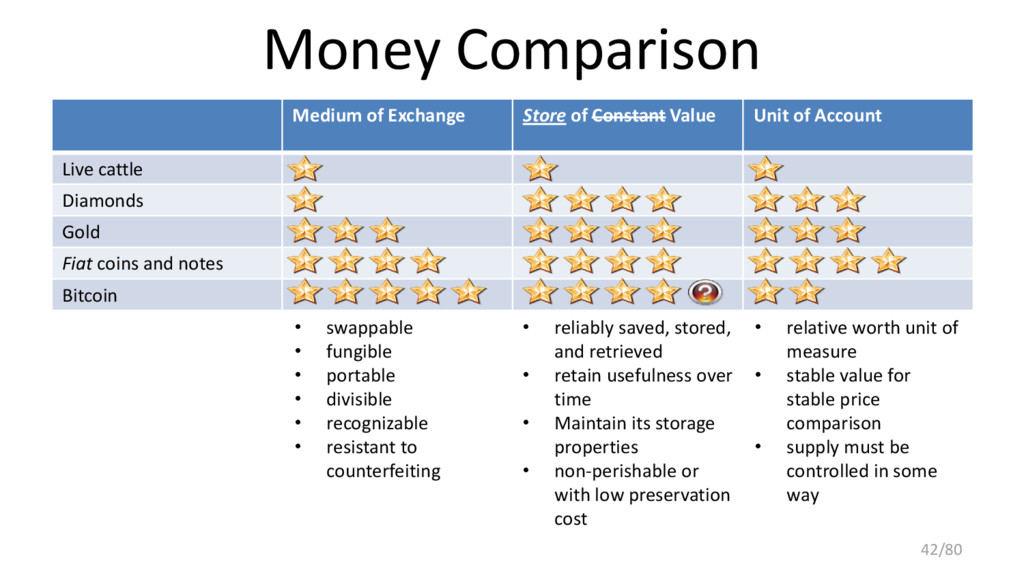

of Account Live cattle Diamonds Gold Fiat coins and notes Bitcoin • swappable • fungible • portable • divisible • recognizable • resistant to counterfeiting • reliably saved, stored, and retrieved • retain usefulness over time • Maintain its storage properties • non-perishable or with low preservation cost • relative worth unit of measure • stable value for stable price comparison • supply must be controlled in some way 42/80

unit of account against which the value of every other good is measured • The price system measures the value of goods relative to the value of money Good money should provide stable prices to best perform its role as unit of account 43/80

symmetallism • Fixed value of bullion (Aneurin Williams 1892) • Compensated dollar (1911-20 Irving Fisher) • Commodity Reserve Currency (1932 J. Goudriaan, 1937-44 B. Graham, 1942 F. Graham, 1951 M. Friedman) • ANCAP basket (1982 Robert Hall) • Futures contracts (1984 Miles, 1989-95 Sumner) • Quasi-futures contract (1994 Kevin Dowd) • Price index option (2000 Kevin Dowd) 44/80

supply • Price stability paradigm with respect to a reference basket • Concurrent cryptocurrencies will compete in monetary policy definition and reference basket choices 45/80

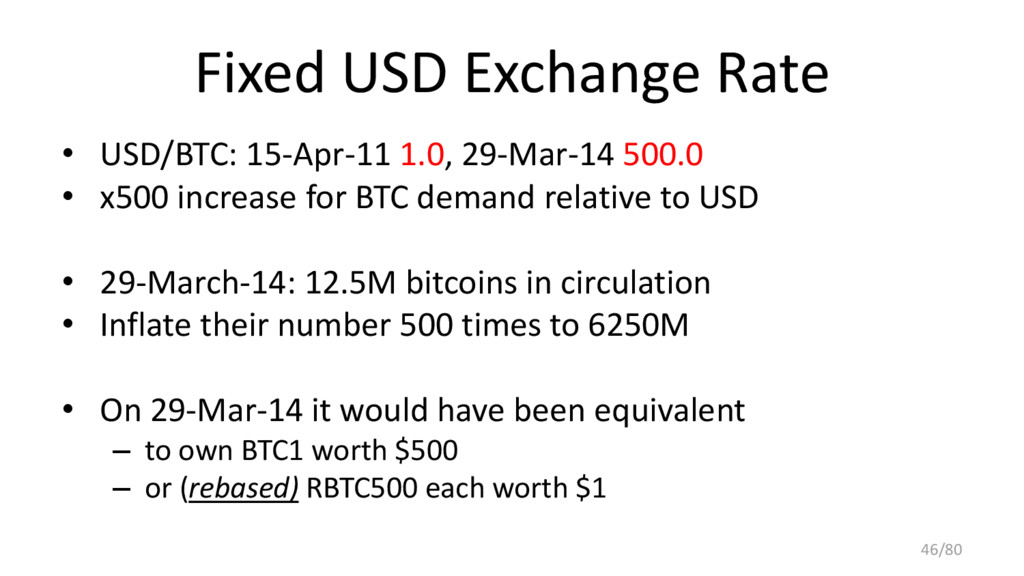

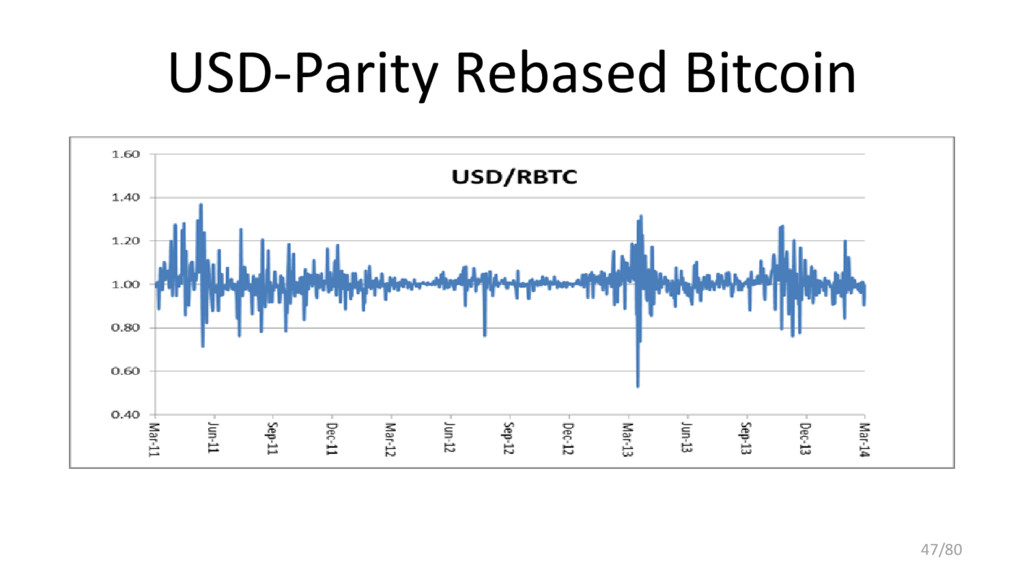

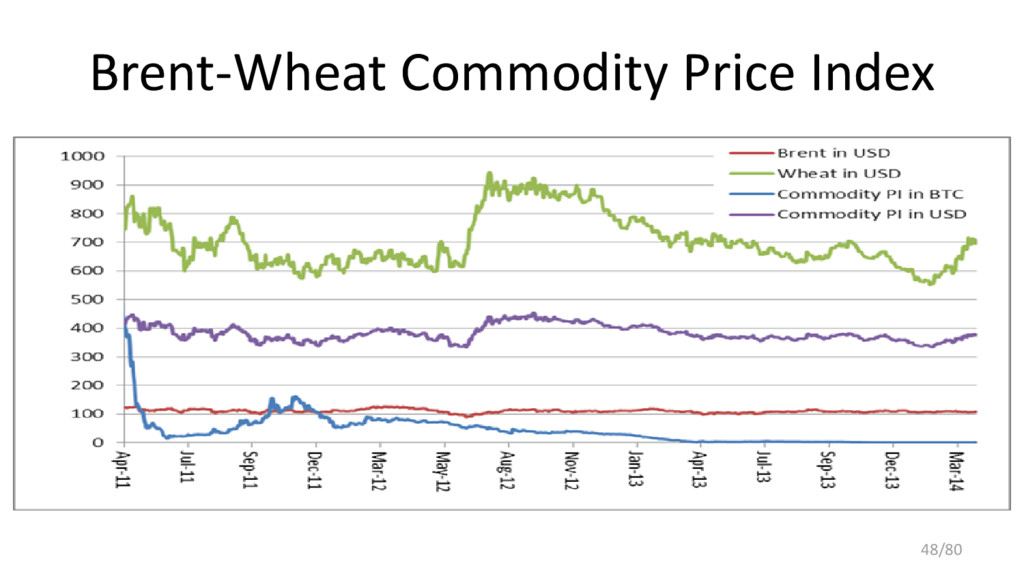

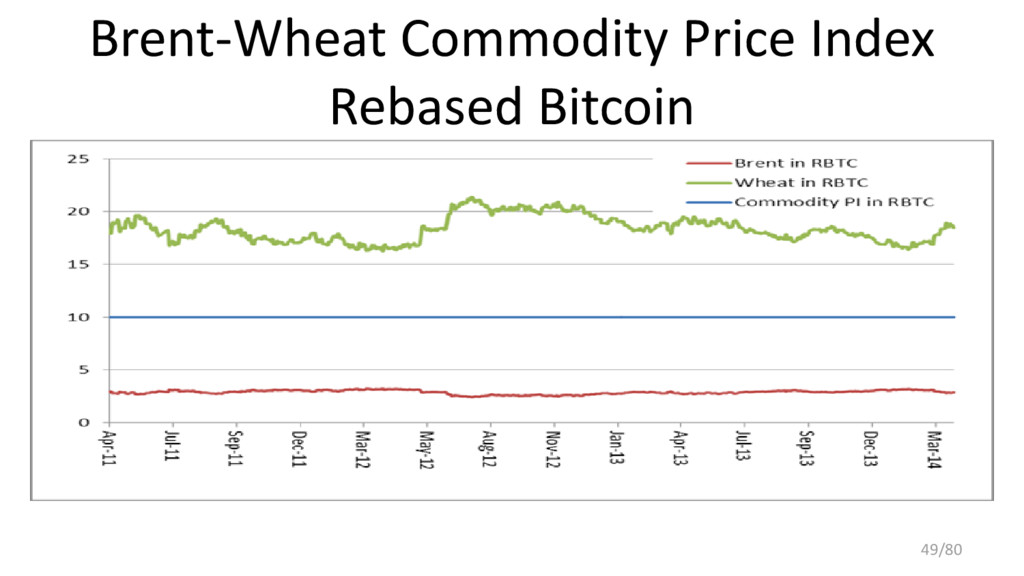

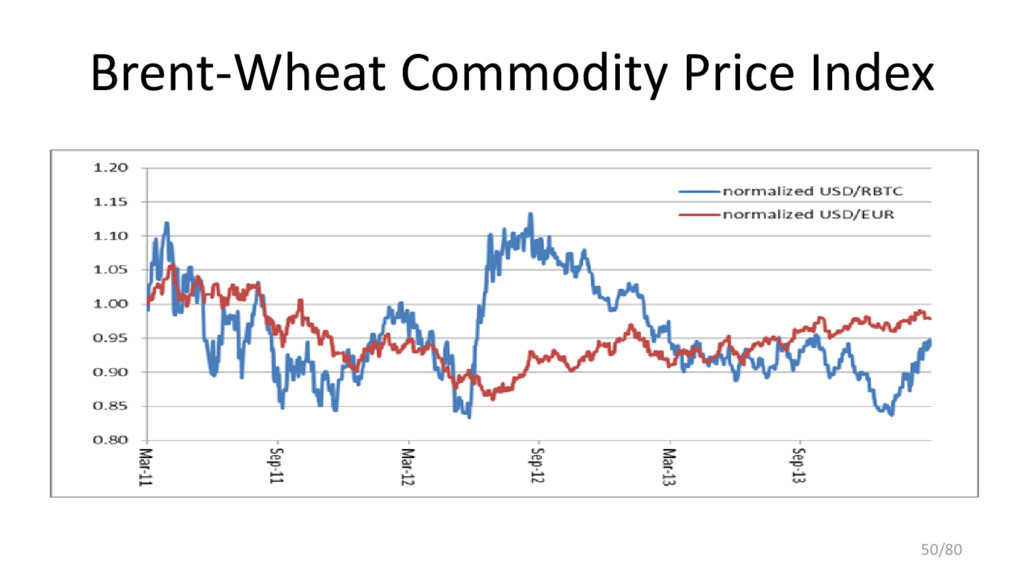

• x500 increase for BTC demand relative to USD • 29-March-14: 12.5M bitcoins in circulation • Inflate their number 500 times to 6250M • On 29-Mar-14 it would have been equivalent – to own BTC1 worth $500 – or (rebased) RBTC500 each worth $1 46/80

sake of discussion, basically to leverage its historic price series • Bitcoin is good as it is: more of a cryptocommodity than a cryptocurrency, bitcoin is digital cryptogold 51/80

are the agents of the transaction history consensus algorithm • Miners can also be the agents of the reference price consensus algorithm • Shelling points: unbiased market prices are focal prices for the average consensus process • Miners as (black market) brokers 52/80

relative price stability and sensitivity, and competitive markets might suggest Commodity Price Index alterations • The Commodity Price Index is composed of technically unconstrained numbers • Nothing could stop the majority of miners from changing the Commodity Price Index definition • Proof-of-stake is crucial: the prerogative to change the Price Index is not oligopolistic power abuse, but the proper right of the majority to rule about its own money 53/80

stability – Salaries, mortgages, forward payments are now possible • Problems: – Number of coins in a wallet changes without direct in/out flows – Purchasing power of a given wallet is not stable – Miners are in charge of reference basket maintenance – Coins still have speculative investment appeal and so enjoy limited transaction usage 54/80

demand with two non-fungible assets: coins and shares – see Sams (2014) A Note on Cryptocurrency Stabilisation: Seigniorage Shares https://github.com/rmsams/stablecoins/blob/master/paper.pdf • Leverage bitcoin as reserve asset – see Ametrano (2016) Price Stability Using Bitcoin as Reserve Asset http://ssrn.com/abstract=2508296 55/80

• Everything else tracked with blockchain technology is somebody’s liability A healthy digital transactional economy requires a native digital asset to be used for payment and collateral; it makes no sense to only have liabilities! the same is true for other native digital assets (ethereum, litecoin, etc.) of less secure blockchains 57/80

of Blockchain and Virtual Currencies, Intesa Sanpaolo, discusses the relationship between bitcoin and blockchain, and outlines how banks can stay ahead of this evolving landscape. 58

email was the killer Internet app • Impossible to imagine Google, Facebook, Amazon • 2016: bitcoin is the killer Blockchain app • More ambitious apps will be built on blockchain, but they have not been really imagined yet, and they will need a native digital asset 59/80

hashed to producing a short unique identifier, equivalent to its digital fingerprint. • Such a fingerprint can be associated to a bitcoin transaction (irrelevant amount) and hence registered on the blockchain • Blockchain immutability provides non-repudiable time-stamp, proving the existence of the data file in that specific status at that moment in time • This generic process is even undergoing some standardization to achieve third party auditable verification: broker-dealers could use it to satisfy regulatory prescriptions 60/80

is preserved by a computation power unparalleled in human history • Other transactional networks can tap into this security via anchoring (i.e. periodic time- stamping of the network status) • Bitcoin miners as global outsourced decentralized security of the future 61/80

and digital IDs [not really blockchain] As for the rest, it is basically hype. Questions always to be answered: • Can be achieved with a database? • What consensus is required? (distributed, bilateral, centralized) • What kind of security is required: preventive, detective, or corrective? (ok / yes today, probably not in the future/ no) • Blockchain is absolutely not suited for storing large amount of data 62/80

project intended to bring blockchains to finance” • Its Distributed Ledger Group is developing a proprietary platform, named Corda: “Corda is a distributed ledger platform […] we are not building a blockchain” • A revamped SWIFT secure messaging protocol on cryptographic proof & bilateral ledger steroids? • Goldman Sachs and Santander just left the consortium 65/80

validated and cleared, then settled shortly thereafter, automatically without a central authority • In the financial world, cash transactions only are cleared and settled automatically without a central authority 66/80

execute, clear and settle in days • Not a technological problem • Consensus by reconciliation of multiple independent ledgers: a checks and balances system that allows for prescriptions, corrections, and restrictions 67/80

short selling and netting almost impossible • Instant settlement (e.g. for payments) has costs: who should pay for them? • It costs: who should pay for it? 68/80

problematic: [… it] is appealing […] it would mean people have direct access to the ultimate risk-free asset [...] it could exacerbate liquidity risk by lowering the frictions involved in running to central bank money [...] it could fundamentally and perhaps abruptly re-shape banking. Mark Carney, Governor of the Bank of England, June 2016 http://www.bankofengland.co.uk/publications/Documents/speeches/2016/speech914.pdf • IMF sponsored blockchain tokens might replace Special Drawing Rights: unrealistic as it would severely undermine US dollar predominance • A free instantaneous P2P payment network is a great opportunity for retail banks (probably worth a consortium) 70/80

intensive: not clear which agent would perform it, its economic incentive, which models it should use • variation margin automated payments: programmatic access to payment funds entails huge operational risks • the default of counterparty would leave the other party exposed to the market risks usually covered by initial margin: i.e. initial margin are still required 71/80

• Without a central governing node how to manage priorities between conflicting updates? Which consensus model? • Bilateral consensus? Really?!?!? • Central governance: back to DB admin • What if the single authoritative data source is hacked? Which reference can be used to fix it? 72/80

the main Ethereum project, it raised >$160m as leaderless Venture Capital • The terms of The DAO are set forth in the smart contract code […] Nothing […] may modify or add any additional obligations or guarantees beyond those set forth in The DAO’s code • Based on its self-executing nature an agent diverted about $50m from The DAO to its own child-DAO start-up • If code is law, then this is not a theft: it is a feature • Beware of extreme automation 73/80

into account the seigniorage revenues invested, each transaction on the bitcoin blockchain has a cost of about 5-10USD • Cheaper forms of consensus have not been proven yet • Even in the case of basic bilateral consensus through digital signatures (something hardly innovative or disruptive...) the integration cost in the existing infrastructure is not going to be irrelevant 74/80

hashed to producing a short unique identifier, equivalent to its digital fingerprint. • Such a fingerprint can be associated to a bitcoin transaction (irrelevant amount) and hence registered on the blockchain • Blockchain immutability provides non-repudiable time-stamp, proving the existence of the data file in that specific status at that moment in time. • This process is undergoing standardization: third party auditability makes it suitable for regulatory prescriptions 75/80

is preserved by a computation power unparalleled in human history • Other transactional networks can tap into this security via anchoring (i.e. periodic time- stamping of the network status) • Bitcoin miners as global outsourced decentralized security of the future 76/80

Can be achieved with a database? • What consensus is required? (distributed, bilateral, centralized) • What kind of security is required: – Preventive (ok) – Detective (ok today, probably not in the future) – Corrective? (no) 77/80

for regulation • Private permissioned DLTs are supposedly being built from the ground up according to regulatory compliance guidelines • Regulators should examine DLT under the light of the existing regulatory framework • To regulate in advance on the basis of vague ephemeral discussions about DLT would be problematic and might stifle innovation. • The necessity for ad-hoc regulation is not evident yet, and there has not been a motivated explicit request for it. 78/80

of my recent presentation to Bank of Italy (Rome) and the European Banking Federation (Bruxelles): https://speakerdeck.com/nando1970/about-bitcoin-and-blockchain-1 • Joint answer with Barucci, Marazzina, and Zanero to the ESMA consultation on DLT for securities markets: https://drive.google.com/drive/folders/0B8tGDTaBY4-Nb3ZuRmgzRXJXOUk • My recent article for the Swift Institute newsletter https://www.linkedin.com/pulse/bitcoin-blockchain-dlt-chimera-ferdinando-maria-ametrano 79/80

digital asset such as bitcoin; • Bitcoin is digital gold and can be as relevant as physical gold for the history of civilization, money, and finance • Unrealistic expectations arise from distributed ledger hype: no reference implementation has emerged yet • Instant settlement, cash on the ledger, shared data set, and improved automation are not easy to obtain • Time-stamping and anchoring are promising applications • Hardly disruptive, DLT might be evolutionary DB tech 80/80

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}