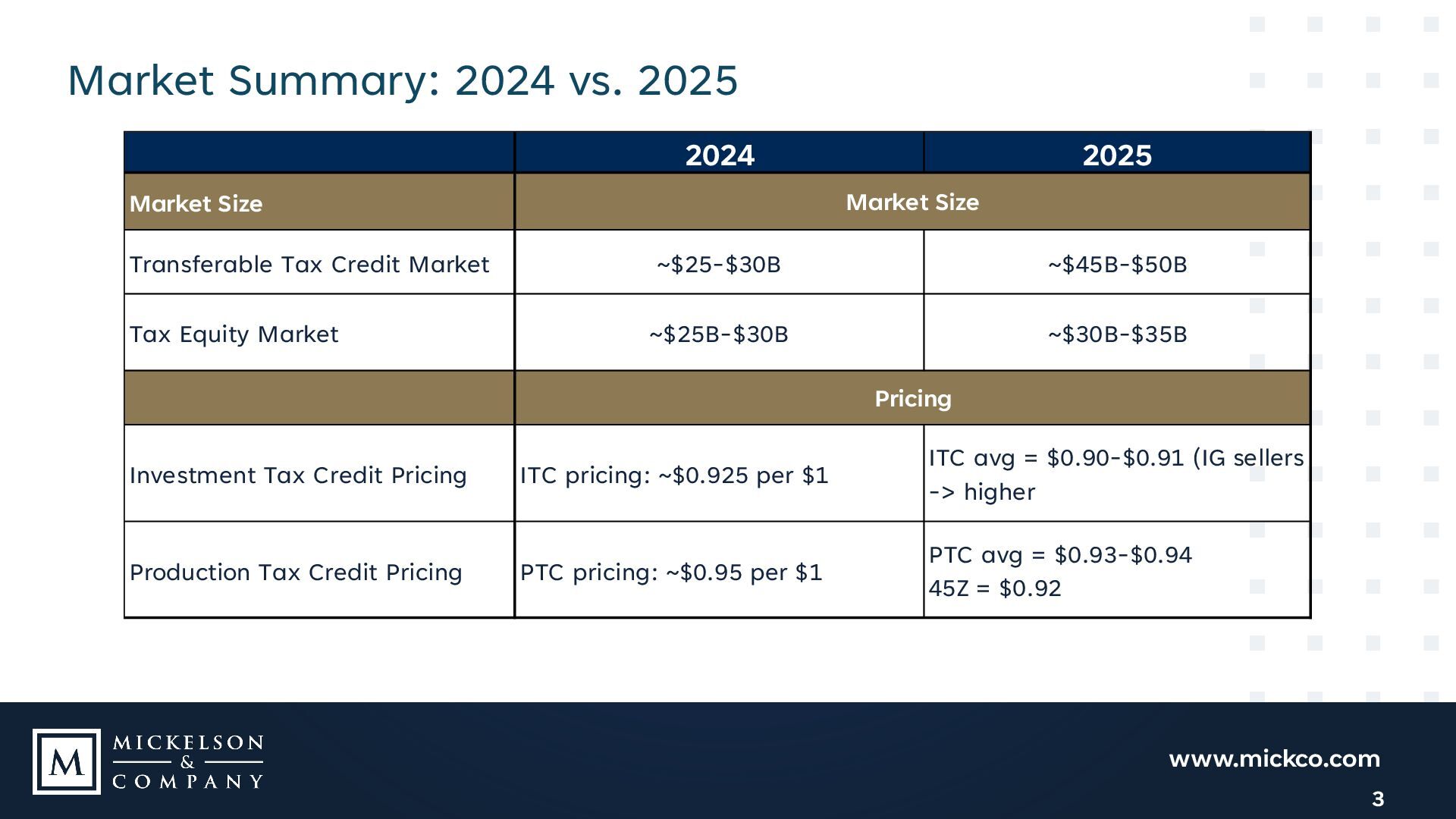

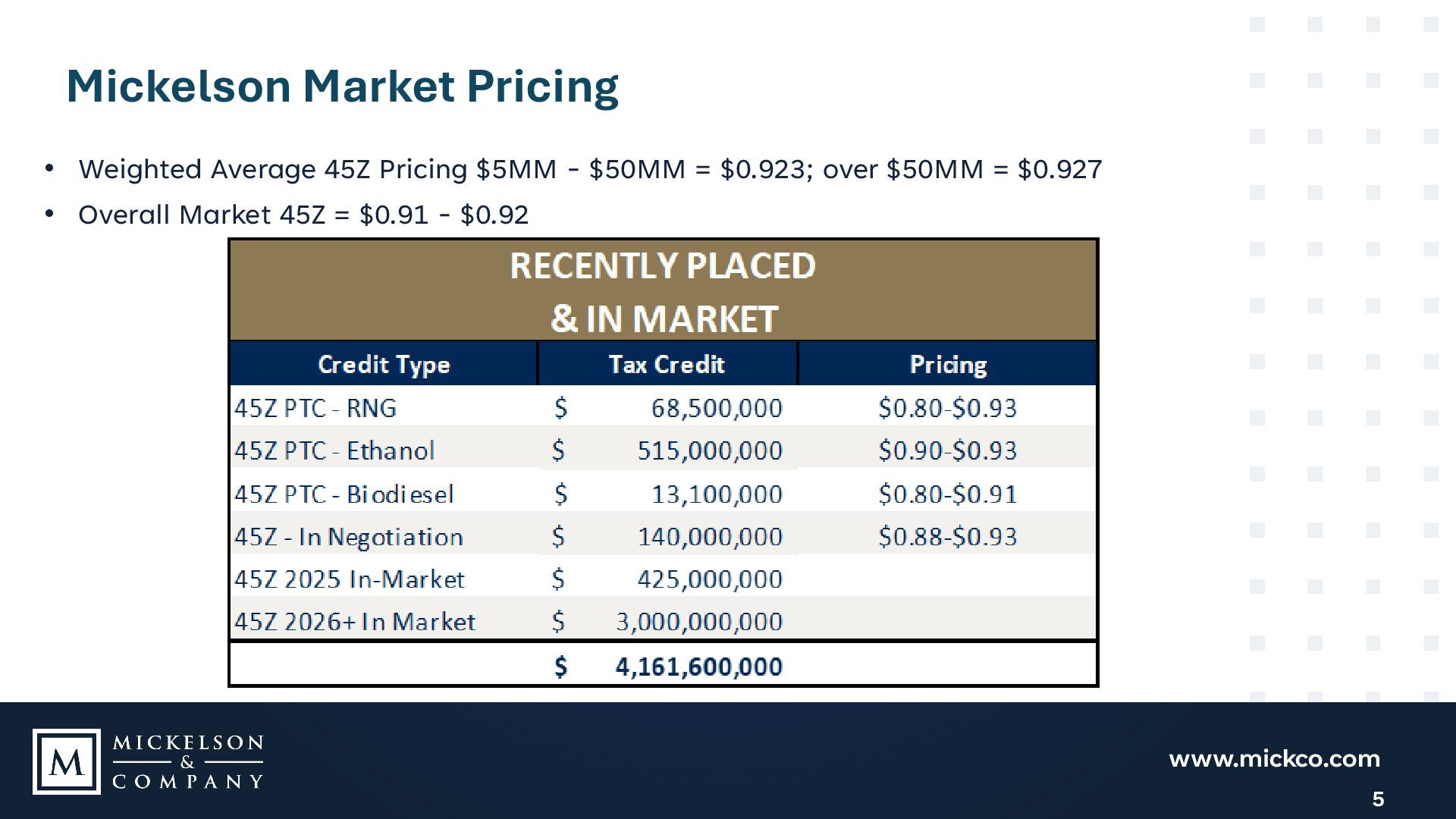

for c-corporations by close to $947 billion over the next decade • 100% bonus depreciation, R&D, expanded deductions and other favorable tax treatment • Focus on educating new buyers new to transferability • Buyers who’ve done tax equity historically opting to stick with tax equity but may supplement for excess capacity with transferability • Expect larger capacities and more buyers educated in transferability to bolster demand, but unknown how quickly can absorb onslaught of supply (may compress pricing) • Ethanol 45Z only one piece of overall transferability market 2

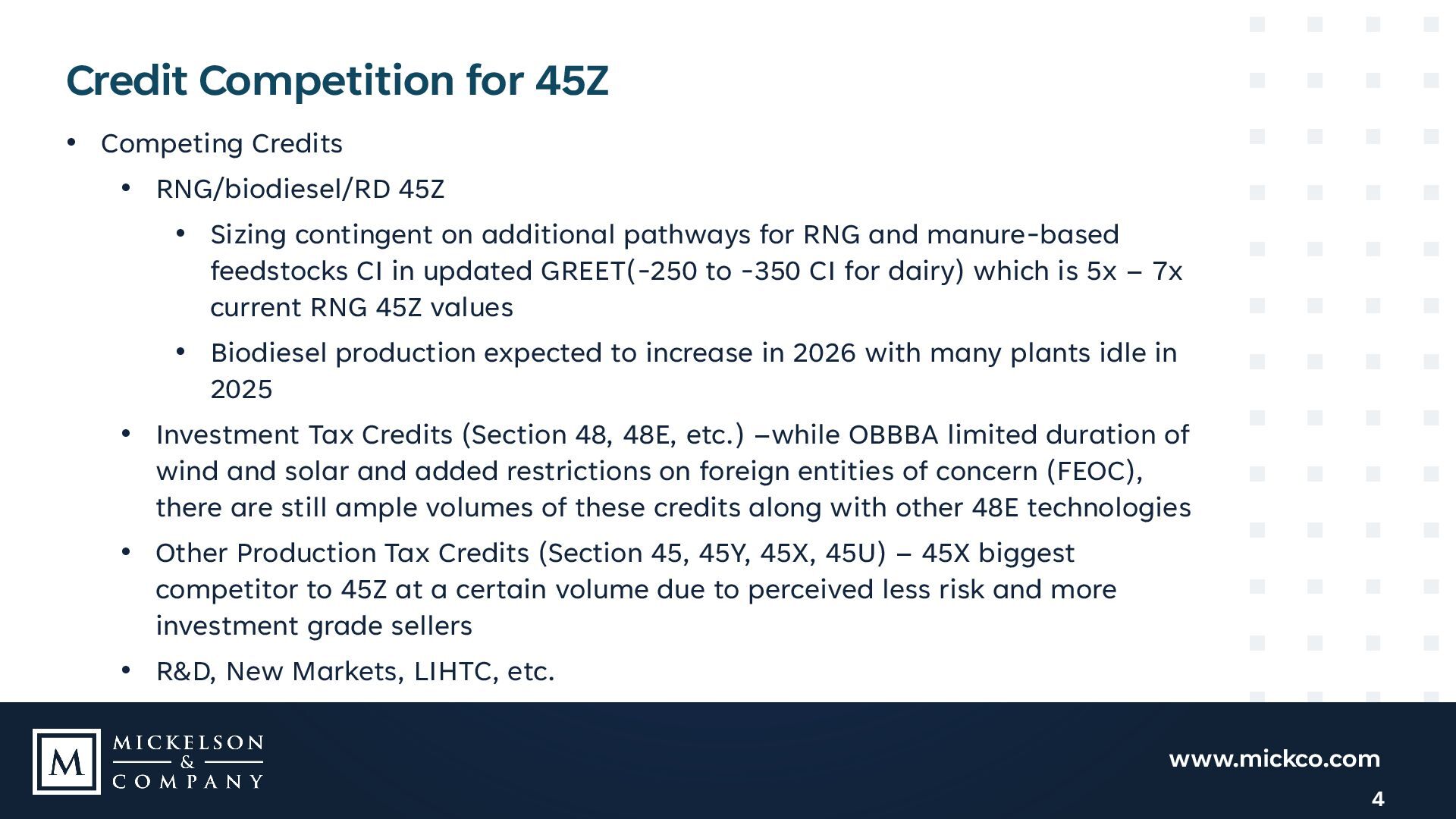

• Sizing contingent on additional pathways for RNG and manure-based feedstocks CI in updated GREET(-250 to -350 CI for dairy) which is 5x – 7x current RNG 45Z values • Biodiesel production expected to increase in 2026 with many plants idle in 2025 • Investment Tax Credits (Section 48, 48E, etc.) –while OBBBA limited duration of wind and solar and added restrictions on foreign entities of concern (FEOC), there are still ample volumes of these credits along with other 48E technologies • Other Production Tax Credits (Section 45, 45Y, 45X, 45U) – 45X biggest competitor to 45Z at a certain volume due to perceived less risk and more investment grade sellers • R&D, New Markets, LIHTC, etc. www.mickco.com 4

2025 with closings ramping up in December • Delays in transacting due to timing of OBBBA - buyers adjusted for favorable tax treatment while sellers delayed in diligence work such as PWA compliance and CI modeling • Q1 slow with less demand as year end consumes buyers but outlook on pricing remains stable in low 90s • No crystal ball for where pricing stabilizes as 2025 market picks back up and buyers take on 2026 to match estimated payments • General buyer requirements to mitigate risk and arrive at market pricing still not fully determined, i.e. opinion vs. memo, indemnity vs. insurance, multi-year structures likely • Each buyer has individualized “buy box” or “investment thesis” • Continued focus on buyer education, acquisition, and repeat purchases • More activity with proposed regs and reliance 6

• Match fundings with estimated payment dates • Utilize advisors for diligence (CPAs and legal counsel) • Strength of financials and/or tax credit insurance key for decision • Not willing to take disallowance risk for a tax credit • Multi-year commitment attractive • Rely on advisors and advisors’ diligence requirements • Comfortable to close/fund without full year complete • May purchase smaller amount to get comfortable before doing larger transactions • Request third party advisor fee reimbursement capped at reasonable rate to cover expense outlay 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}