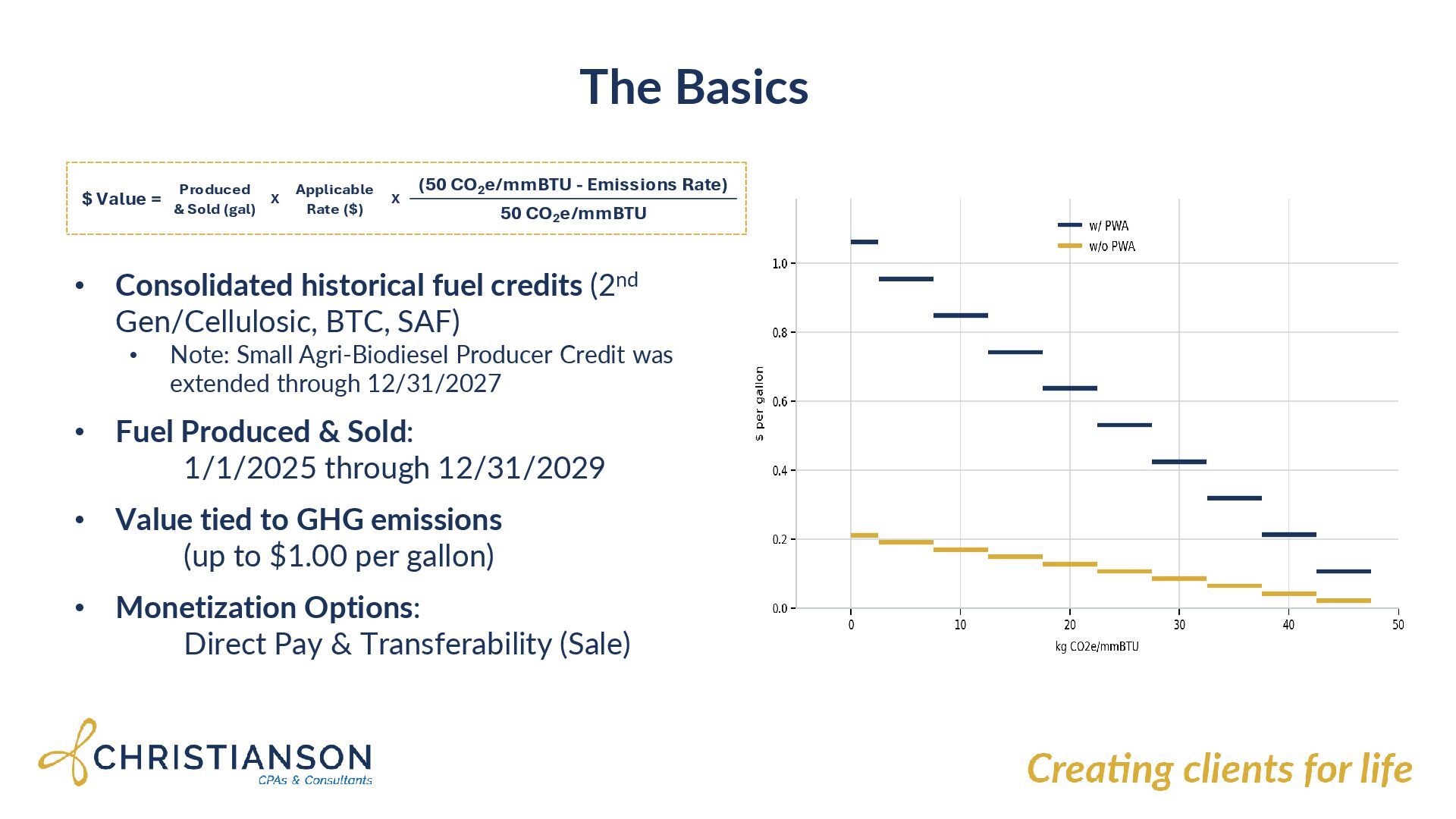

SAF) • Note: Small Agri-Biodiesel Producer Credit was extended through 12/31/2027 • Fuel Produced & Sold: 1/1/2025 through 12/31/2029 • Value tied to GHG emissions (up to $1.00 per gallon) • Monetization Options: Direct Pay & Transferability (Sale) (50 CO2 e/mmBTU - Emissions Rate) 50 CO2 e/mmBTU $ Value = Produced & Sold (gal) X X Applicable Rate ($)

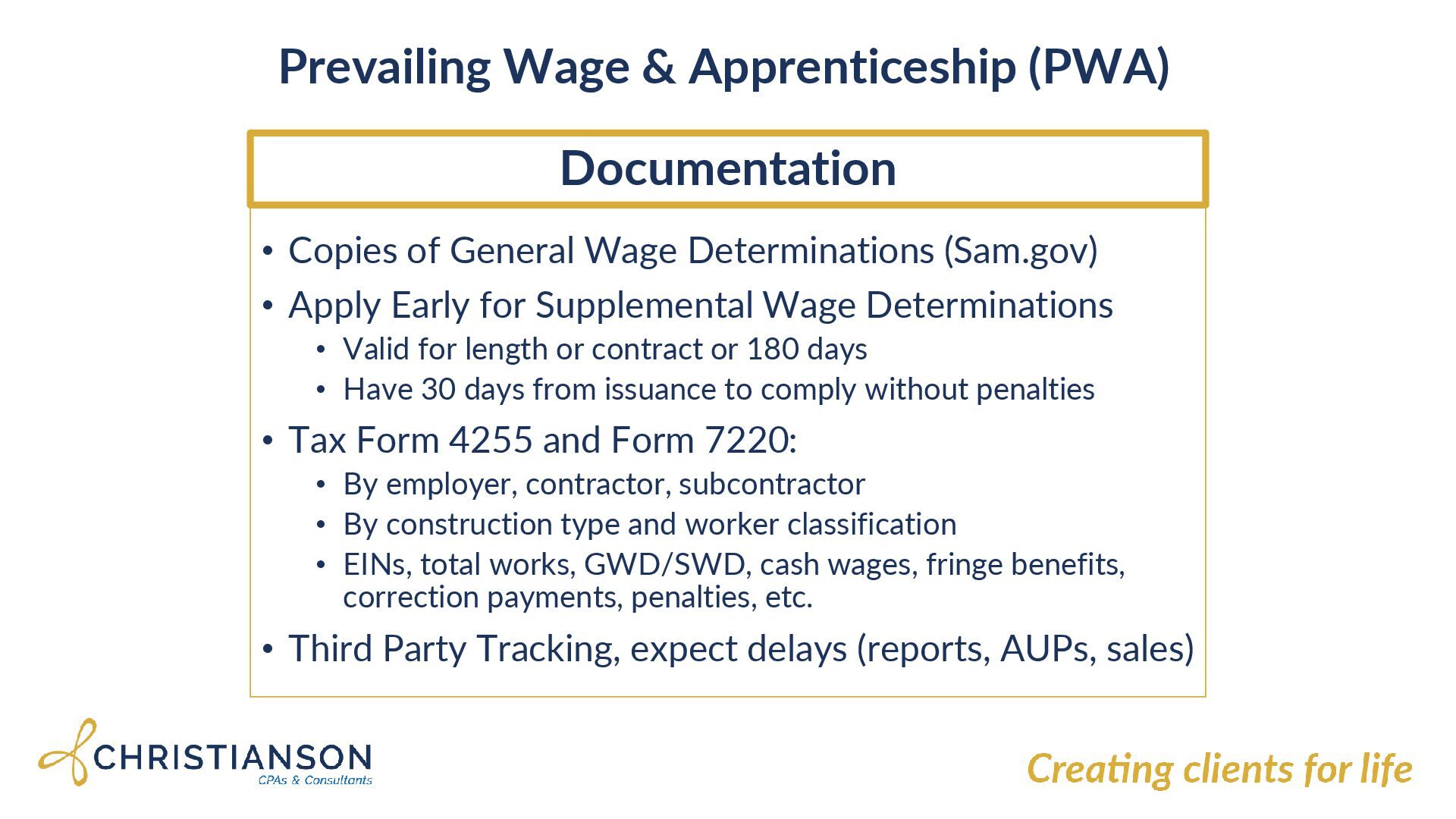

Wage Determinations (Sam.gov) • Apply Early for Supplemental Wage Determinations • Valid for length or contract or 180 days • Have 30 days from issuance to comply without penalties • Tax Form 4255 and Form 7220: • By employer, contractor, subcontractor • By construction type and worker classification • EINs, total works, GWD/SWD, cash wages, fringe benefits, correction payments, penalties, etc. • Third Party Tracking, expect delays (reports, AUPs, sales)

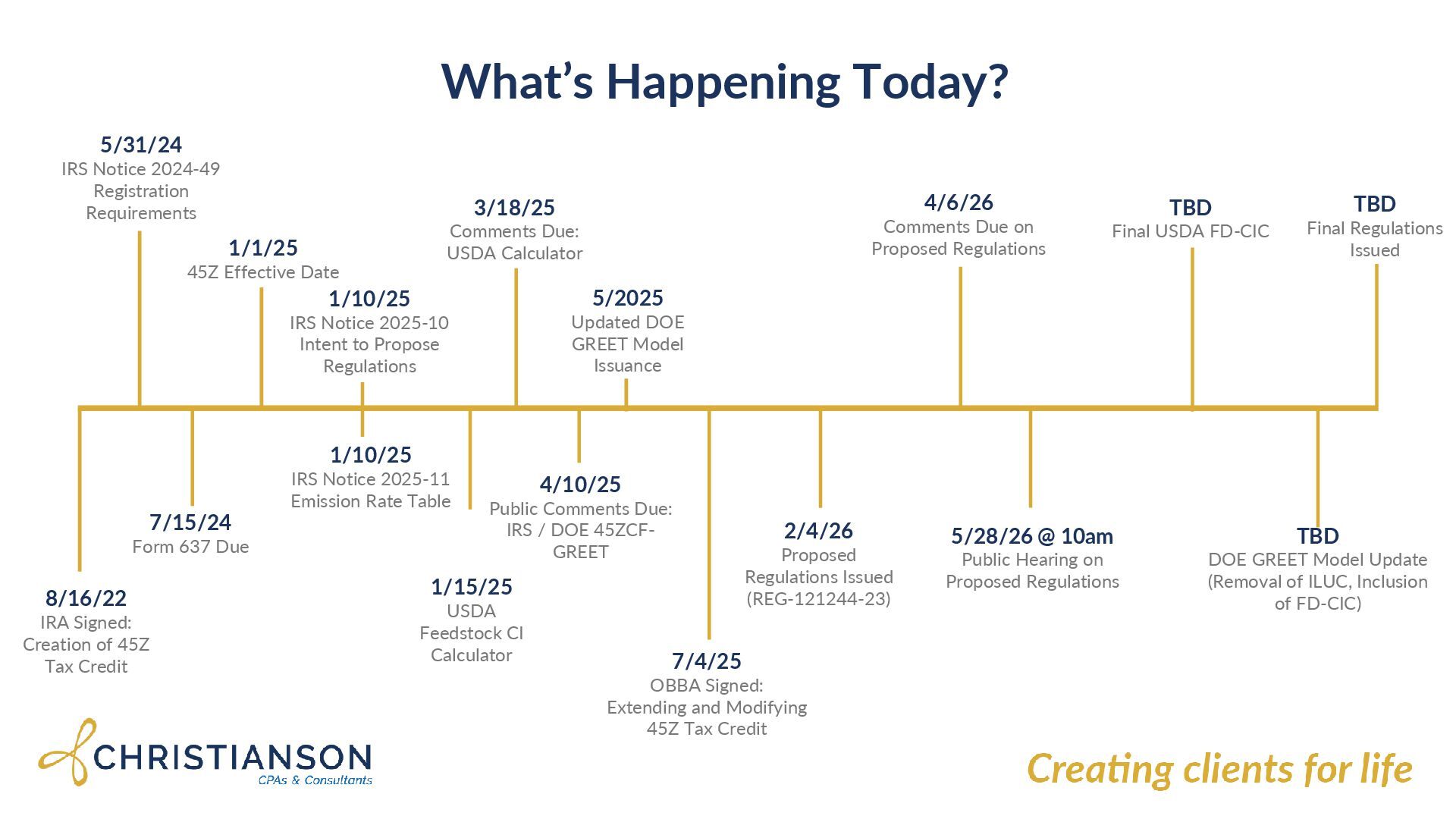

Form 637 Due 1/1/25 45Z Effective Date 1/10/25 IRS Notice 2025-11 Emission Rate Table 1/10/25 IRS Notice 2025-10 Intent to Propose Regulations 1/15/25 USDA Feedstock CI Calculator 3/18/25 Comments Due: USDA Calculator 4/10/25 Public Comments Due: IRS / DOE 45ZCF- GREET 5/2025 Updated DOE GREET Model Issuance 2/4/26 Proposed Regulations Issued (REG-121244-23) 4/6/26 Comments Due on Proposed Regulations 5/28/26 @ 10am Public Hearing on Proposed Regulations TBD Final USDA FD-CIC TBD DOE GREET Model Update (Removal of ILUC, Inclusion of FD-CIC) TBD Final Regulations Issued 8/16/22 IRA Signed: Creation of 45Z Tax Credit 7/4/25 OBBA Signed: Extending and Modifying 45Z Tax Credit

followed the playbook we had • Real-time decisions based on IRS intent-to-propose • Proposed regulations arrived after year-end • For 2025, you still have a choice: • Intent-to-propose guidance or proposed regulations • One framework, applied consistently • Market is already moving to proposed rules • Flexibility ends with final regulations

(carbon capture) • §45V (clean hydrogen) • §48 ITC claimed in lieu of §45V (hydrogen-related ITC) • Still a facility-level rule: • Qualified facility defined to include carbon capture equipment • Ownership and credit claimant do not matter • Flexibility across tax years: • Eligibility alone does not trigger disqualification • “allowable” vs. “allowed” language • Facilities may switch credit regimes year-to-year • No stacking within the same taxable year

undenatured (ASTM D8651) ethanol may qualify • “Use in a trade or business” • Returns to the statutory standard • Buyer does not need to personally consume the fuel as transportation fuel • Eliminates the “use as a fuel” gloss from notice-stage guidance • Sales through marketers and intermediaries • Removes uncertainty for wholesalers, resellers, and distributors • Related-party sales followed by resale • Broader look-through approach adopted • Sales qualify if fuel is ultimately sold to an unrelated party in a qualifying transaction • Fuel sold for further processing • Upstream sale not disqualified solely because fuel becomes feedstock (e.g., ethanol → SAF) • Credit limitation shifts downstream to avoid double-crediting

GREET models within the same tax year • EAC incrementality • Shift from a facility placed-in-service to a first sub-50 CI production trigger • Indirect Land Use Change (ILUC) • Statutorily excluded for fuel produced after 12/31/2025 • Removes ILUC prospectively; residual uncertainty for certain 2025 fact patterns • Provisional Emissions Rate (PER) process • DOE validates the fuel-specific methodology (not the rate) • PER is determined by the IRS through the tax • Determine by Fuel Type/Methodology, not facility specifics • Negative emissions rates • Still waiting on Treasury to publish • Resolves treatment prospectively; limited clarity for early-year production

CSA incorporation pending USDA’s final FD-CIC model • Scope: • Crops: Corn, Soybeans, Sorghum • Practices: tillage reduction, cover crops, fertilizer management • How CI is calculated • County-level emission factors by crop and practice • Farm-level CI = weighted average across fields • Non-CSA acres default to national averages • Documentation required • Field location, crop volumes, and practice evidence • CI benefit must be tracked through the supply chain

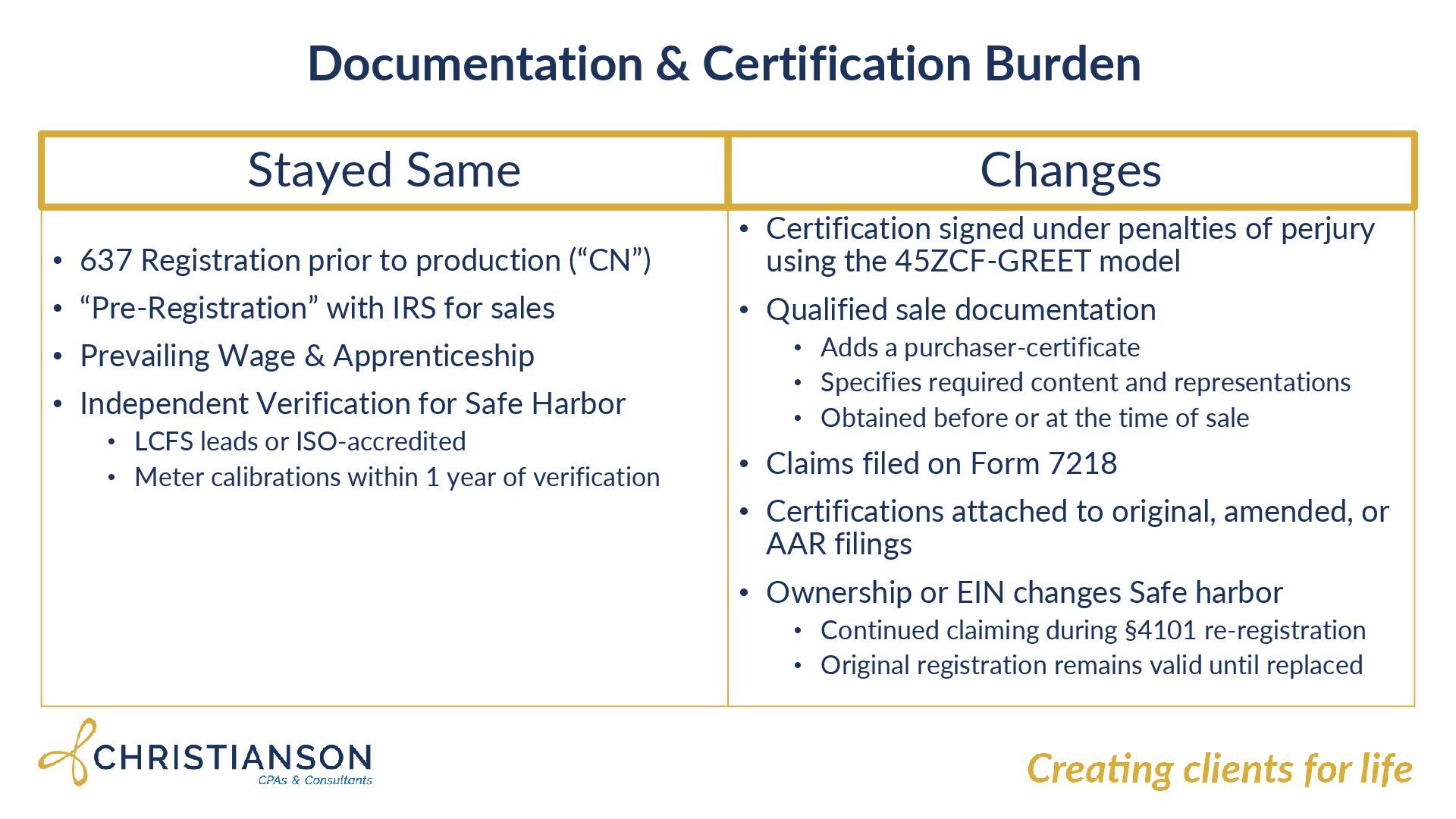

to production (“CN”) • “Pre-Registration” with IRS for sales • Prevailing Wage & Apprenticeship • Independent Verification for Safe Harbor • LCFS leads or ISO-accredited • Meter calibrations within 1 year of verification Changes • Certification signed under penalties of perjury using the 45ZCF-GREET model • Qualified sale documentation • Adds a purchaser-certificate • Specifies required content and representations • Obtained before or at the time of sale • Claims filed on Form 7218 • Certifications attached to original, amended, or AAR filings • Ownership or EIN changes Safe harbor • Continued claiming during §4101 re-registration • Original registration remains valid until replaced

estimable • Tax: On return in which credit is generated and transferred • Deductible: • Energy Attribute Credits (EACs) • Climate-Smart Ag (CSA) feedstock premiums • Emissions modeling and verification costs • CPA due diligence and technical substantiation • PWA tracking and AUPs • Nondeductible (IRC §265): • Broker or placement fees • Legal fees tied to transfer agreements • Tax credit insurance premiums • Facts-and-Circumstances matter • Costs associated with a sale are nondeductible even if the transfer does not go through

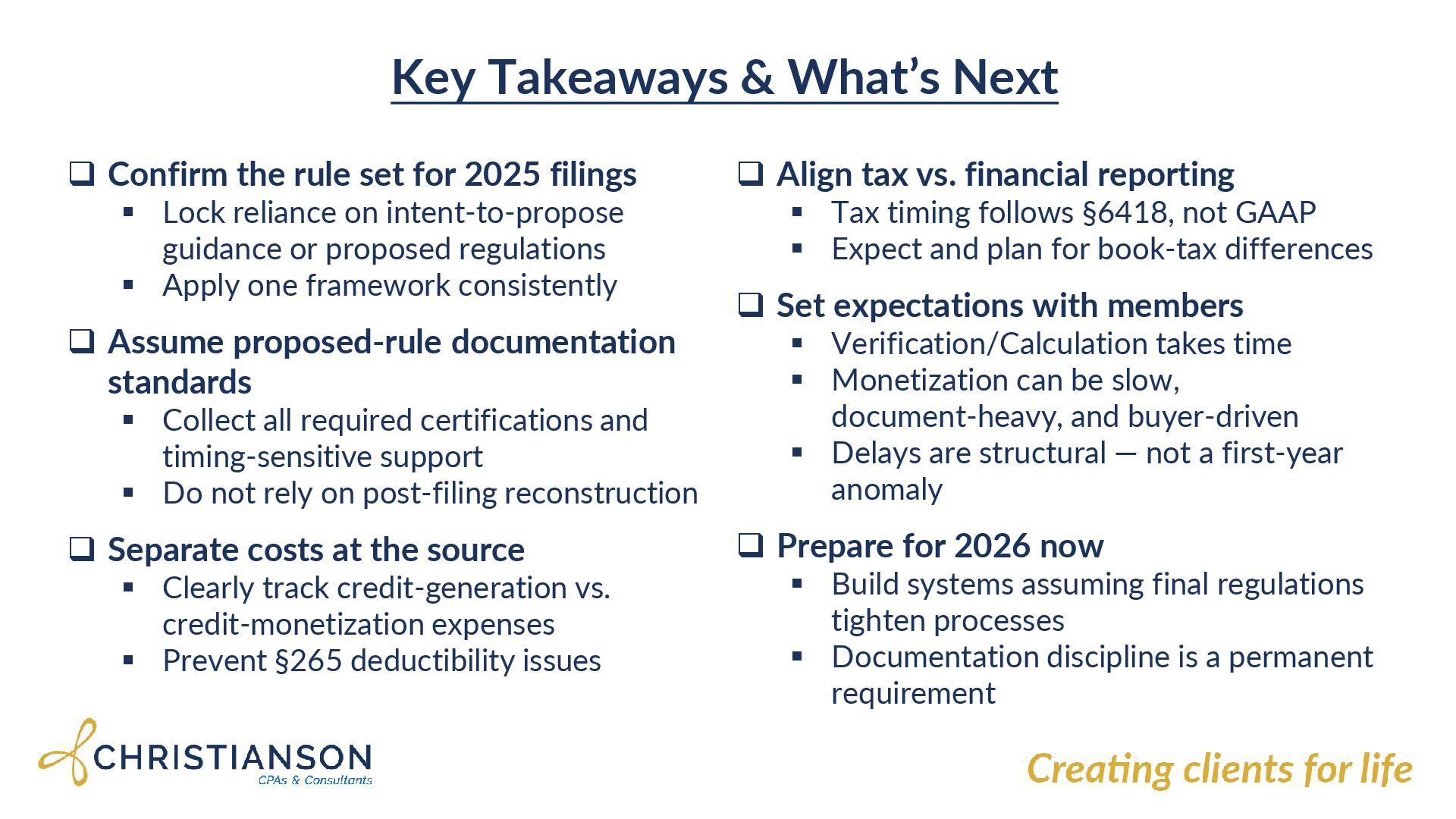

for 2025 filings Lock reliance on intent-to-propose guidance or proposed regulations Apply one framework consistently Assume proposed-rule documentation standards Collect all required certifications and timing-sensitive support Do not rely on post-filing reconstruction Separate costs at the source Clearly track credit-generation vs. credit-monetization expenses Prevent §265 deductibility issues Align tax vs. financial reporting Tax timing follows §6418, not GAAP Expect and plan for book-tax differences Set expectations with members Verification/Calculation takes time Monetization can be slow, document-heavy, and buyer-driven Delays are structural — not a first-year anomaly Prepare for 2026 now Build systems assuming final regulations tighten processes Documentation discipline is a permanent requirement

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![For more information [email protected] 320.441.5509 Rebecca Johnson Manager Creating Clients](https://files.speakerdeck.com/presentations/2d67dcf587cf46e4a2a0fc08dcc20d99/slide_12.jpg){kind=link}