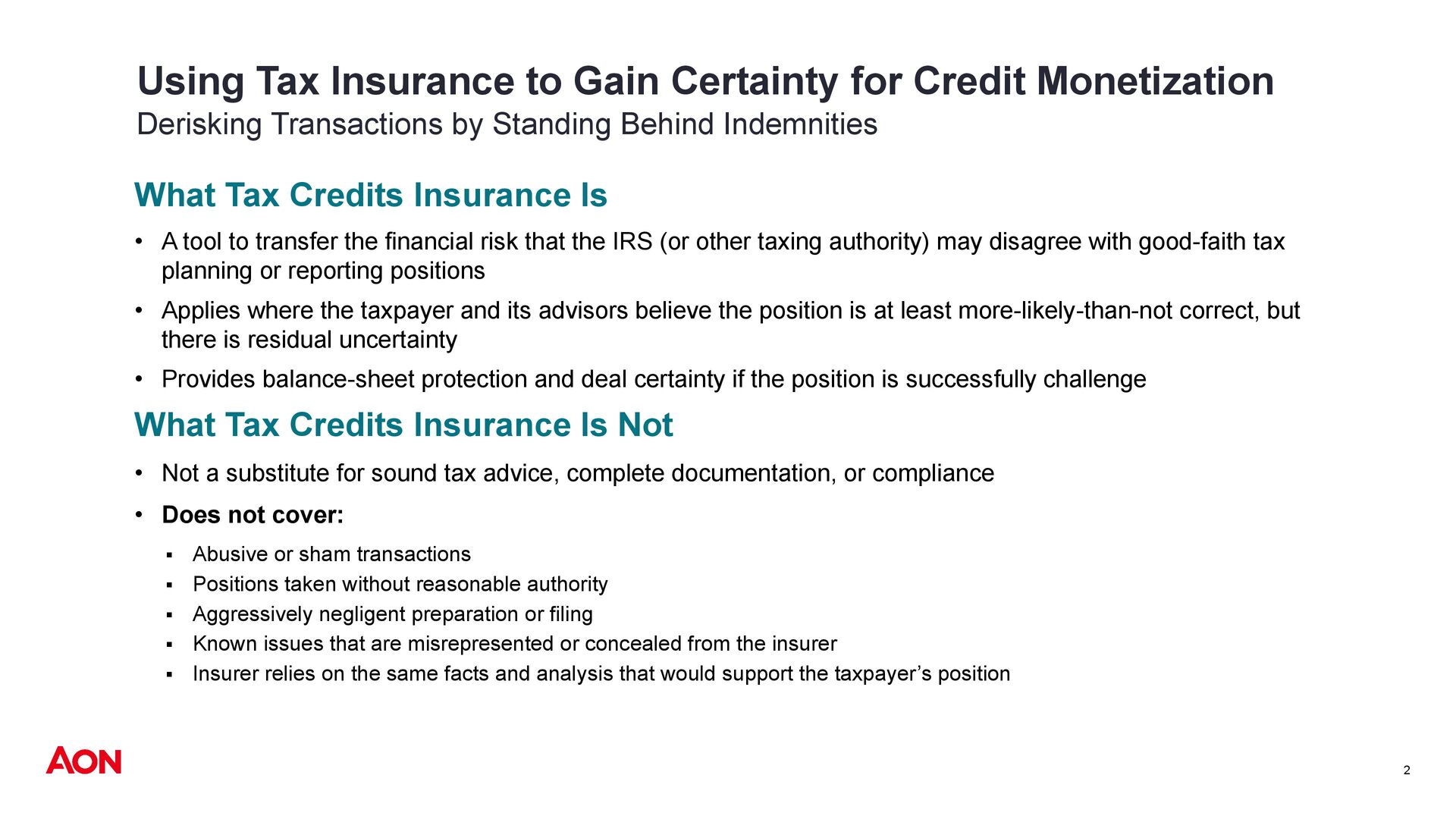

Derisking Transactions by Standing Behind Indemnities What Tax Credits Insurance Is • A tool to transfer the financial risk that the IRS (or other taxing authority) may disagree with good-faith tax planning or reporting positions • Applies where the taxpayer and its advisors believe the position is at least more-likely-than-not correct, but there is residual uncertainty • Provides balance-sheet protection and deal certainty if the position is successfully challenge What Tax Credits Insurance Is Not • Not a substitute for sound tax advice, complete documentation, or compliance • Does not cover: Abusive or sham transactions Positions taken without reasonable authority Aggressively negligent preparation or filing Known issues that are misrepresented or concealed from the insurer Insurer relies on the same facts and analysis that would support the taxpayer’s position

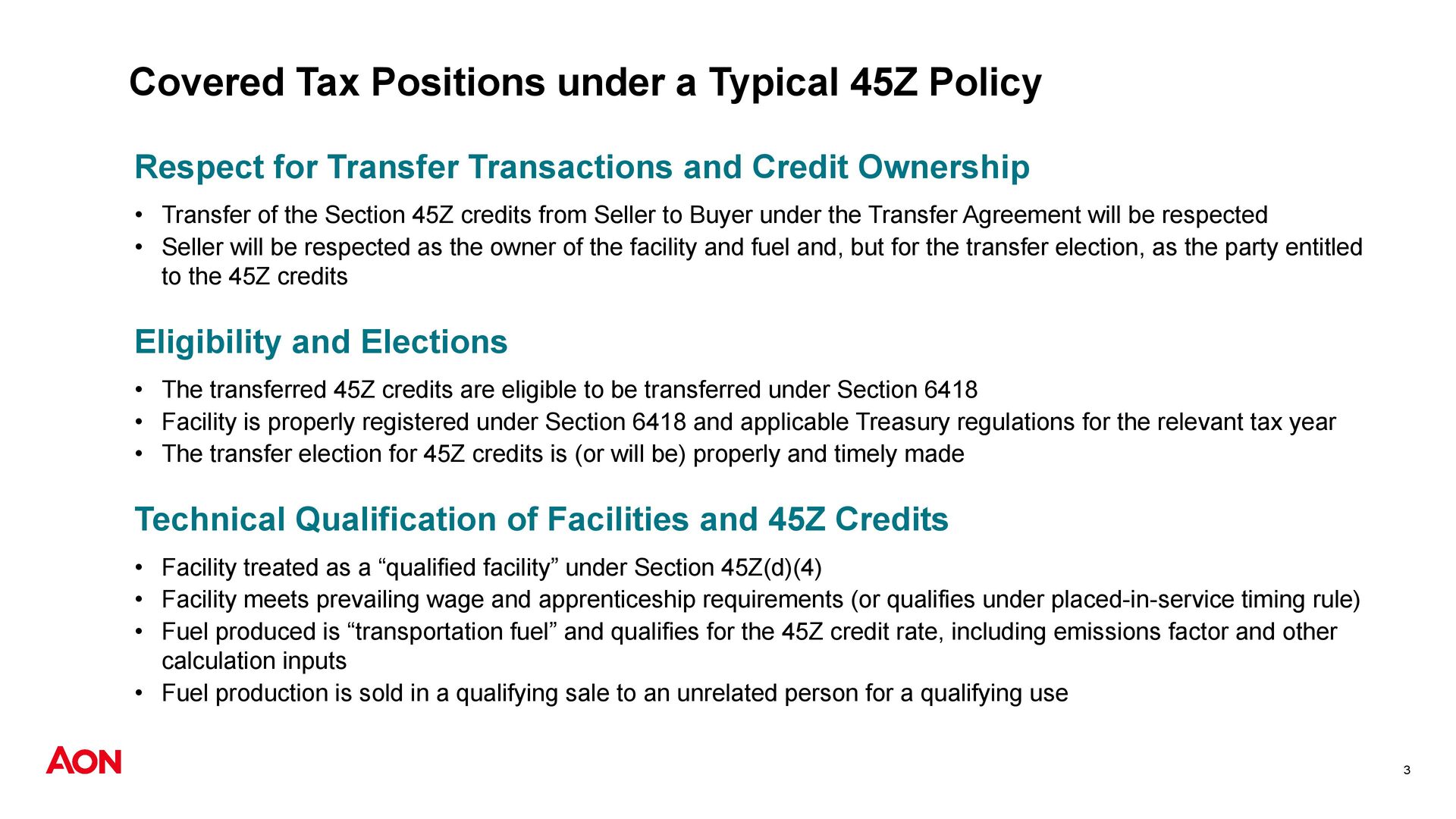

for Transfer Transactions and Credit Ownership • Transfer of the Section 45Z credits from Seller to Buyer under the Transfer Agreement will be respected • Seller will be respected as the owner of the facility and fuel and, but for the transfer election, as the party entitled to the 45Z credits Eligibility and Elections • The transferred 45Z credits are eligible to be transferred under Section 6418 • Facility is properly registered under Section 6418 and applicable Treasury regulations for the relevant tax year • The transfer election for 45Z credits is (or will be) properly and timely made Technical Qualification of Facilities and 45Z Credits • Facility treated as a “qualified facility” under Section 45Z(d)(4) • Facility meets prevailing wage and apprenticeship requirements (or qualifies under placed-in-service timing rule) • Fuel produced is “transportation fuel” and qualifies for the 45Z credit rate, including emissions factor and other calculation inputs • Fuel production is sold in a qualifying sale to an unrelated person for a qualifying use

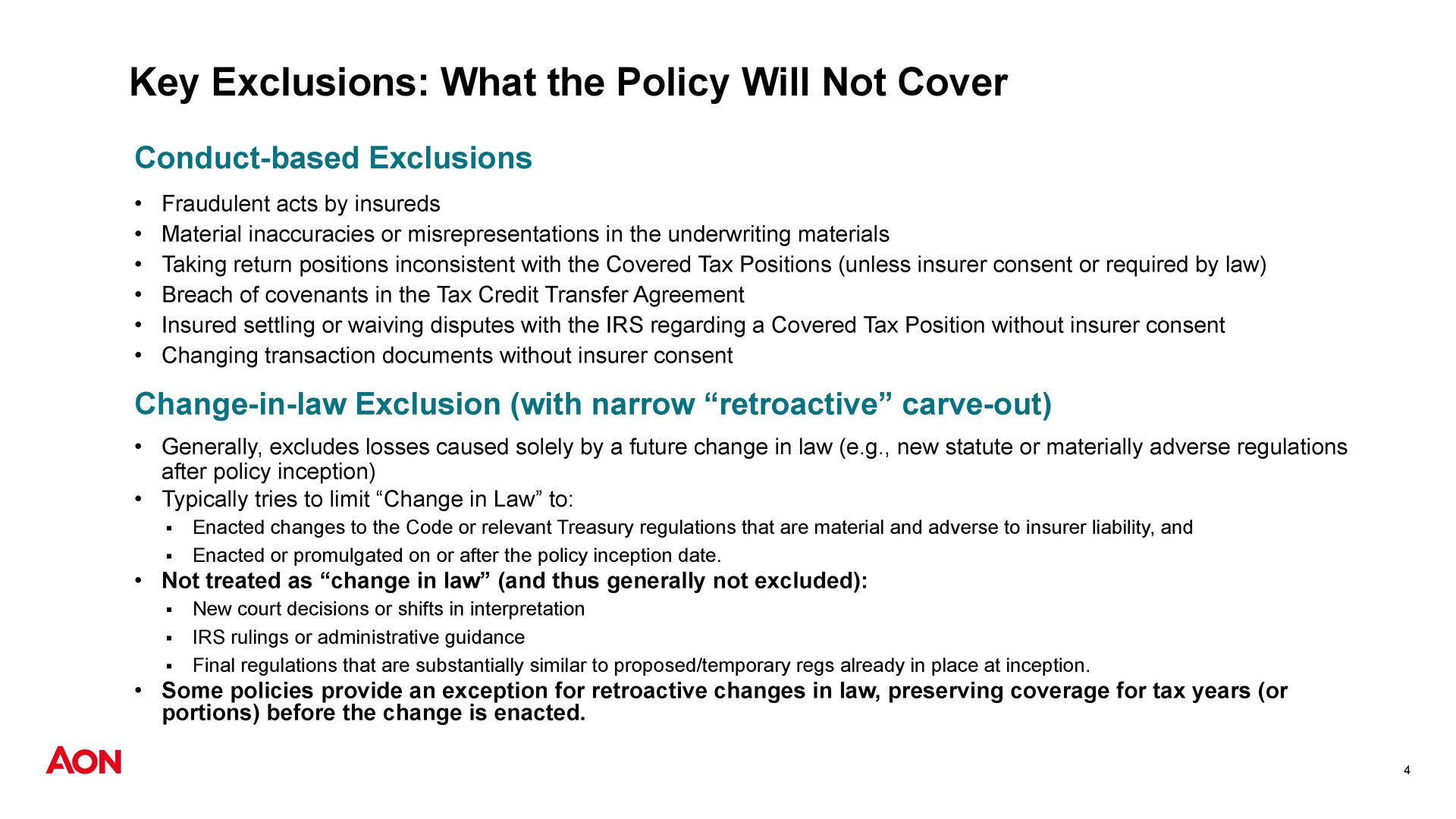

Exclusions • Fraudulent acts by insureds • Material inaccuracies or misrepresentations in the underwriting materials • Taking return positions inconsistent with the Covered Tax Positions (unless insurer consent or required by law) • Breach of covenants in the Tax Credit Transfer Agreement • Insured settling or waiving disputes with the IRS regarding a Covered Tax Position without insurer consent • Changing transaction documents without insurer consent Change-in-law Exclusion (with narrow “retroactive” carve-out) • Generally, excludes losses caused solely by a future change in law (e.g., new statute or materially adverse regulations after policy inception) • Typically tries to limit “Change in Law” to: Enacted changes to the Code or relevant Treasury regulations that are material and adverse to insurer liability, and Enacted or promulgated on or after the policy inception date. • Not treated as “change in law” (and thus generally not excluded): New court decisions or shifts in interpretation IRS rulings or administrative guidance Final regulations that are substantially similar to proposed/temporary regs already in place at inception. • Some policies provide an exception for retroactive changes in law, preserving coverage for tax years (or portions) before the change is enacted.

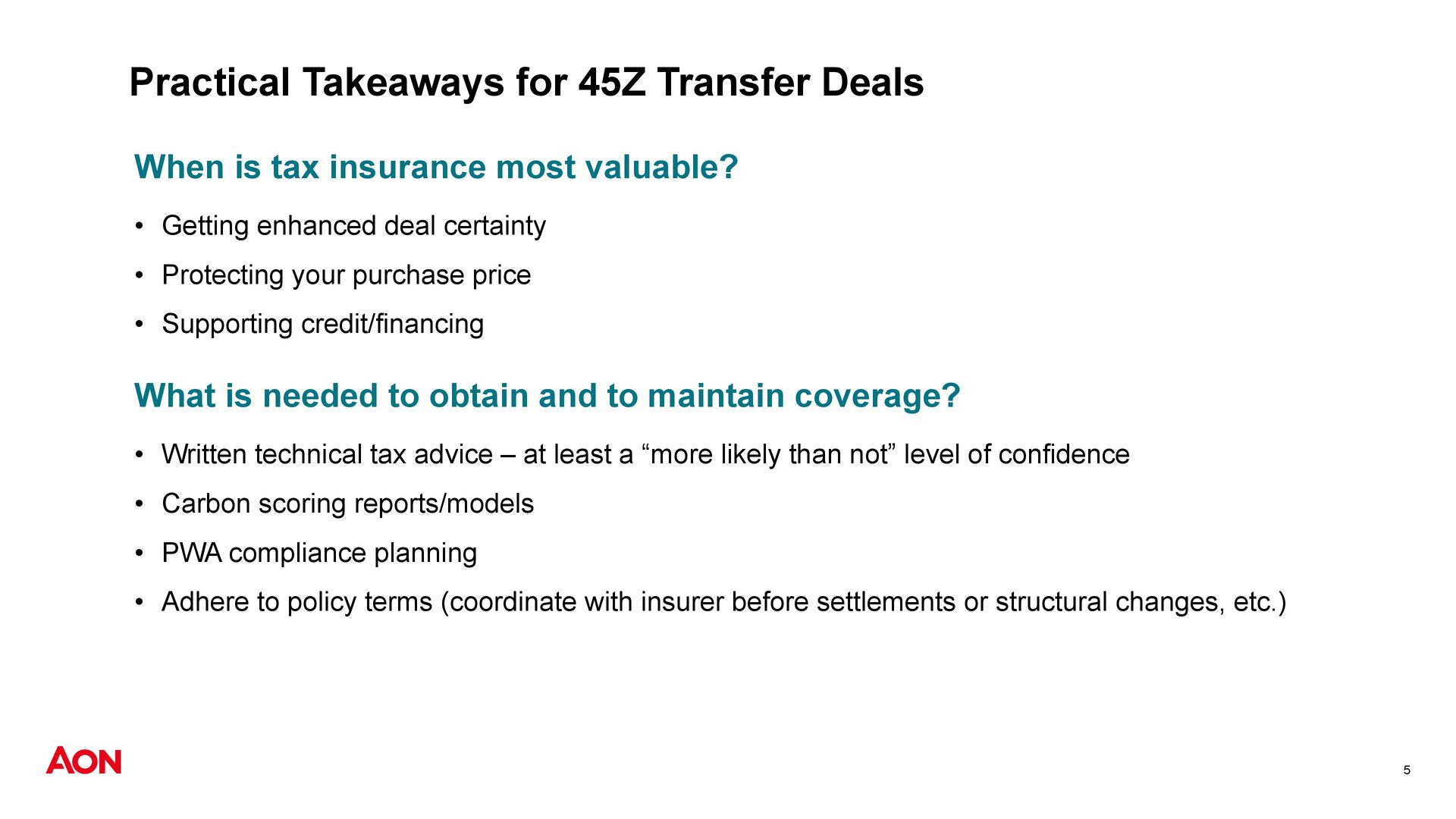

insurance most valuable? • Getting enhanced deal certainty • Protecting your purchase price • Supporting credit/financing What is needed to obtain and to maintain coverage? • Written technical tax advice – at least a “more likely than not” level of confidence • Carbon scoring reports/models • PWA compliance planning • Adhere to policy terms (coordinate with insurer before settlements or structural changes, etc.)

Aon plc (NYSE: AON) exists to shape decisions for the better — to protect and enrich the lives of people around the world. Through actionable analytic insight, globally integrated Risk Capital and Human Capital expertise, and locally relevant solutions, our colleagues provide clients in over 120 countries and sovereignties with the clarity and confidence to make better risk and people decisions that help protect and grow their businesses. Follow Aon on LinkedIn, X, Facebook and Instagram. Stay up-to-date by visiting Aon's newsroom and sign up for news alerts here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}