Political Challenges and Technical Solutions for Taxing Wealth Everywhere

Alex Cobham, CEO of the Tax Justice Network, sets out some of the technical and political issues surrounding wealth taxation at the annual meetings of the World Bank Group.

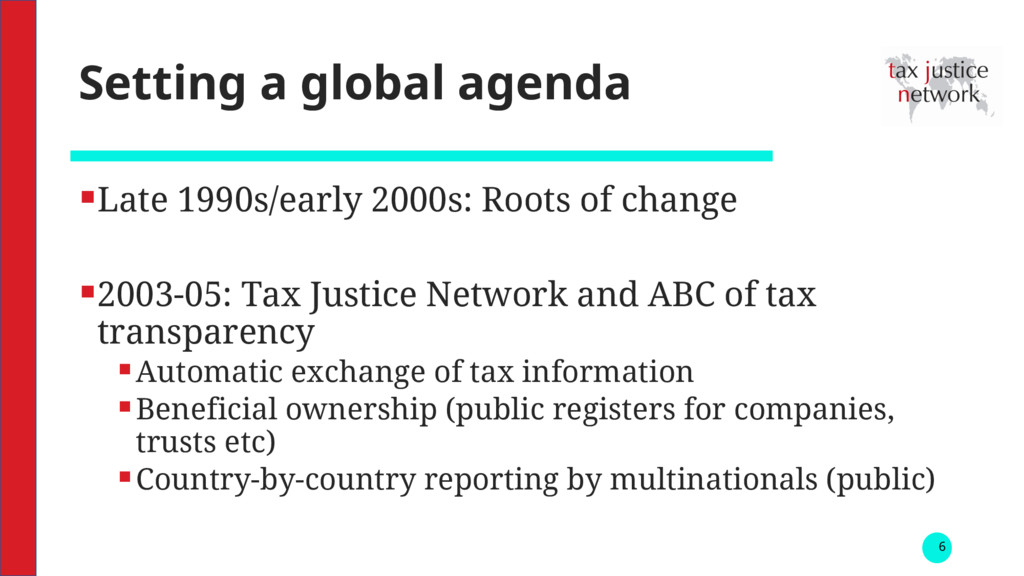

§2003-05: Tax Justice Network and ABC of tax transparency §Automatic exchange of tax information §Beneficial ownership (public registers for companies, trusts etc) §Country-by-country reporting by multinationals (public) 6

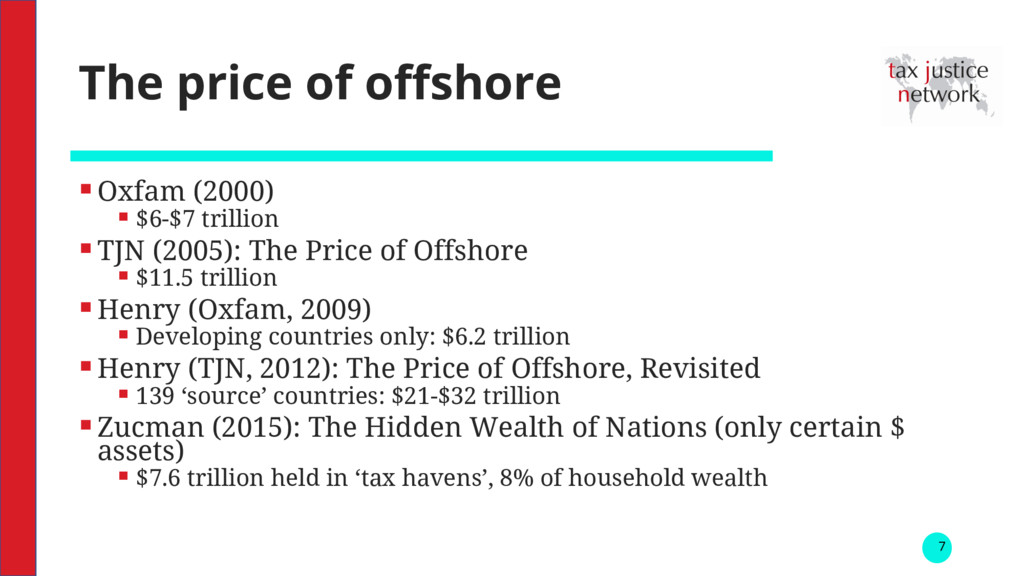

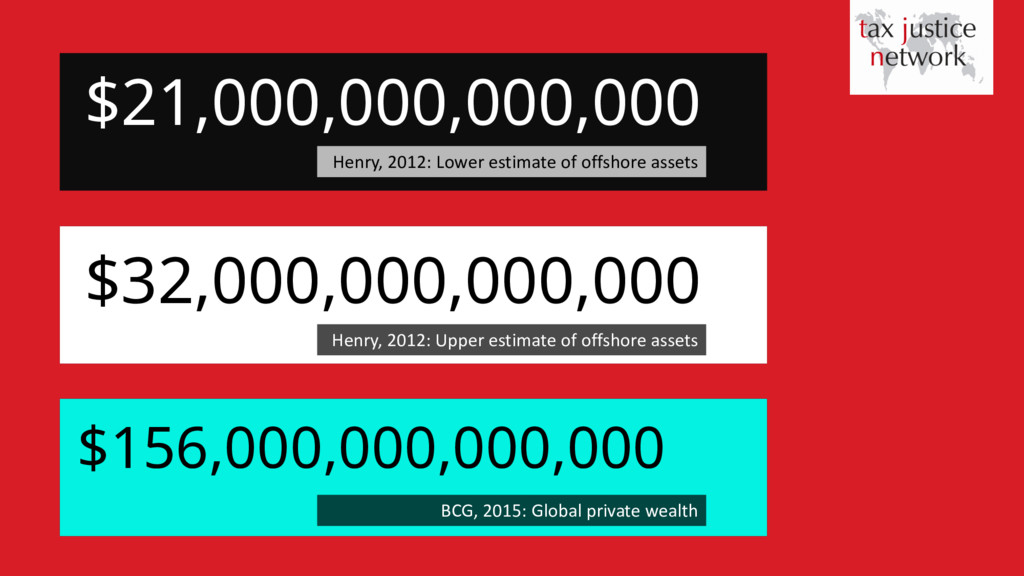

(2005): The Price of Offshore § $11.5 trillion §Henry (Oxfam, 2009) § Developing countries only: $6.2 trillion §Henry (TJN, 2012): The Price of Offshore, Revisited § 139 ‘source’ countries: $21-$32 trillion §Zucman (2015): The Hidden Wealth of Nations (only certain $ assets) § $7.6 trillion held in ‘tax havens’, 8% of household wealth 7

century-long inequality series for a number of economies §Key proposal: a global wealth tax, even levied at 0.01%, would deliver a global financial registry with multiple benefits: § Information for policymakers § Information for public debate § Information for policymaking § Information for crime prevention § … 9

put fiscal justice at the center of the policy agenda. Tax issues should not be left to those who want to escape taxes! Changes will come when more and more citizens of the world take ownership of these matters. TJN is a powerful force acting in this direction.” Thomas Piketty 10

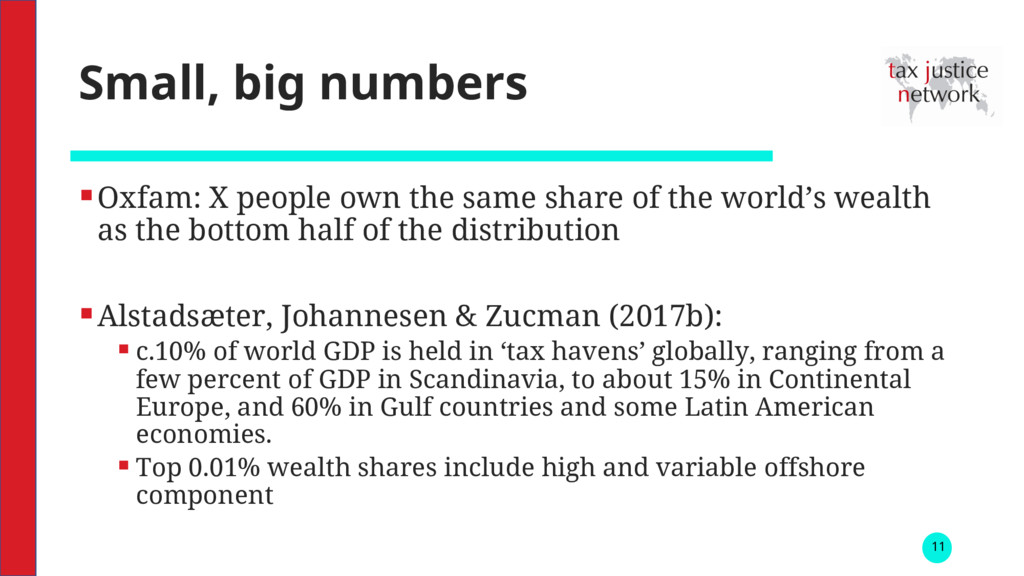

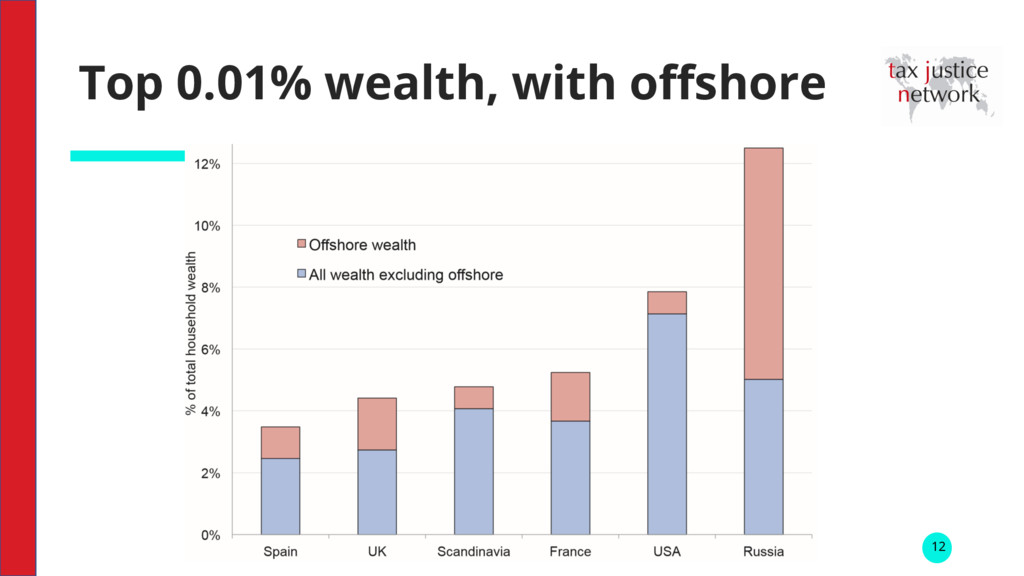

of the world’s wealth as the bottom half of the distribution §Alstadsæter, Johannesen & Zucman (2017b): § c.10% of world GDP is held in ‘tax havens’ globally, ranging from a few percent of GDP in Scandinavia, to about 15% in Continental Europe, and 60% in Gulf countries and some Latin American economies. § Top 0.01% wealth shares include high and variable offshore component 11

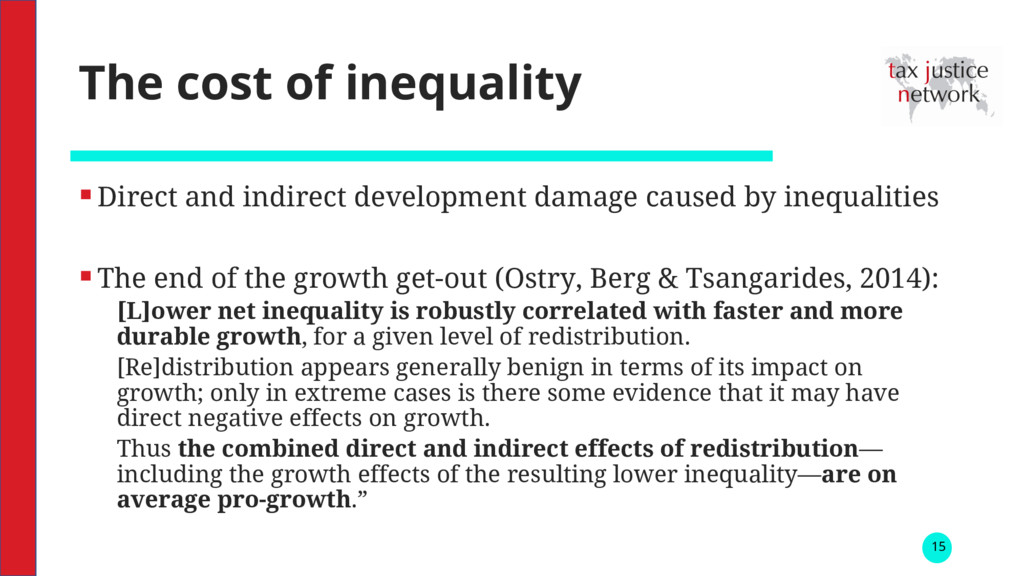

by inequalities §The end of the growth get-out (Ostry, Berg & Tsangarides, 2014): [L]ower net inequality is robustly correlated with faster and more durable growth, for a given level of redistribution. [Re]distribution appears generally benign in terms of its impact on growth; only in extreme cases is there some evidence that it may have direct negative effects on growth. Thus the combined direct and indirect effects of redistribution— including the growth effects of the resulting lower inequality—are on average pro-growth.” 15

§2008-/ Global financial crisis, and OECD country policy responses §Leaks and reactions §2013-2015: Sustainable Development Goals set (cf MDGs) § Inequalities (SDG 10 and throughout) § Tax as primary means of implementation (17.1) § Tax evasion and avoidance targeted (16.4) Confirmation of a global political moment 16

and the wealthy are highly mobile, and tax is key to their location §Blessed are the job-creators § Wealth taxes undermine incentives for innovation, investment, expansion… and ultimately employment 19

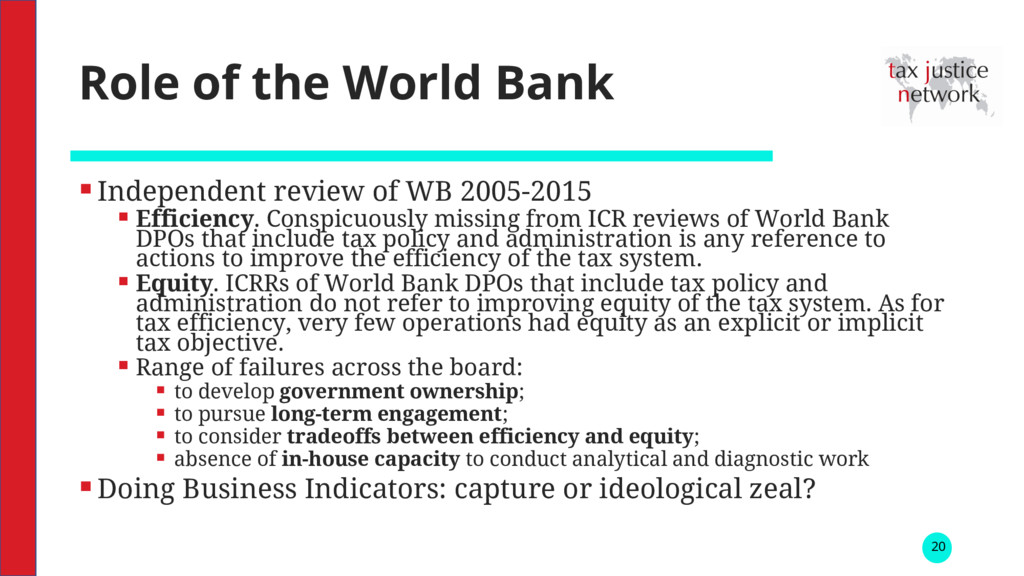

§ Efficiency. Conspicuously missing from ICR reviews of World Bank DPOs that include tax policy and administration is any reference to actions to improve the efficiency of the tax system. § Equity. ICRRs of World Bank DPOs that include tax policy and administration do not refer to improving equity of the tax system. As for tax efficiency, very few operations had equity as an explicit or implicit tax objective. § Range of failures across the board: § to develop government ownership; § to pursue long-term engagement; § to consider tradeoffs between efficiency and equity; § absence of in-house capacity to conduct analytical and diagnostic work §Doing Business Indicators: capture or ideological zeal? 20

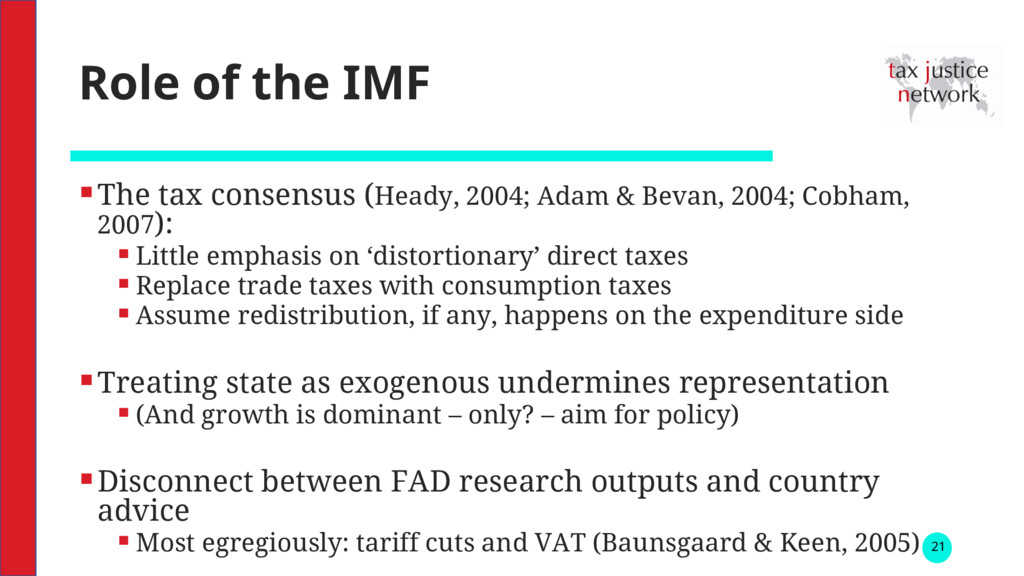

& Bevan, 2004; Cobham, 2007): § Little emphasis on ‘distortionary’ direct taxes § Replace trade taxes with consumption taxes § Assume redistribution, if any, happens on the expenditure side §Treating state as exogenous undermines representation § (And growth is dominant – only? – aim for policy) §Disconnect between FAD research outputs and country advice § Most egregiously: tariff cuts and VAT (Baunsgaard & Keen, 2005) 21

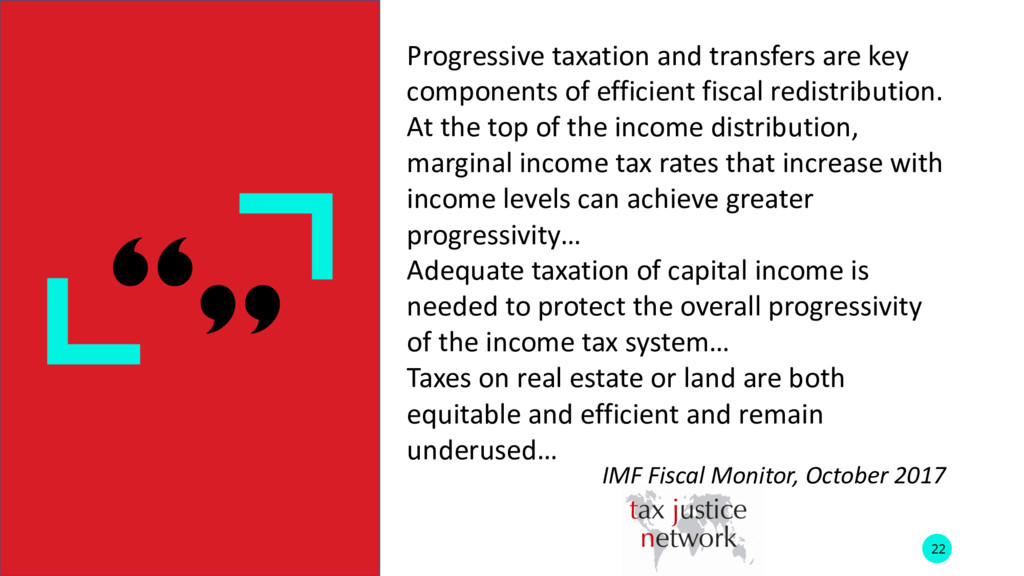

fiscal redistribution. At the top of the income distribution, marginal income tax rates that increase with income levels can achieve greater progressivity… Adequate taxation of capital income is needed to protect the overall progressivity of the income tax system… Taxes on real estate or land are both equitable and efficient and remain underused… IMF Fiscal Monitor, October 2017 22

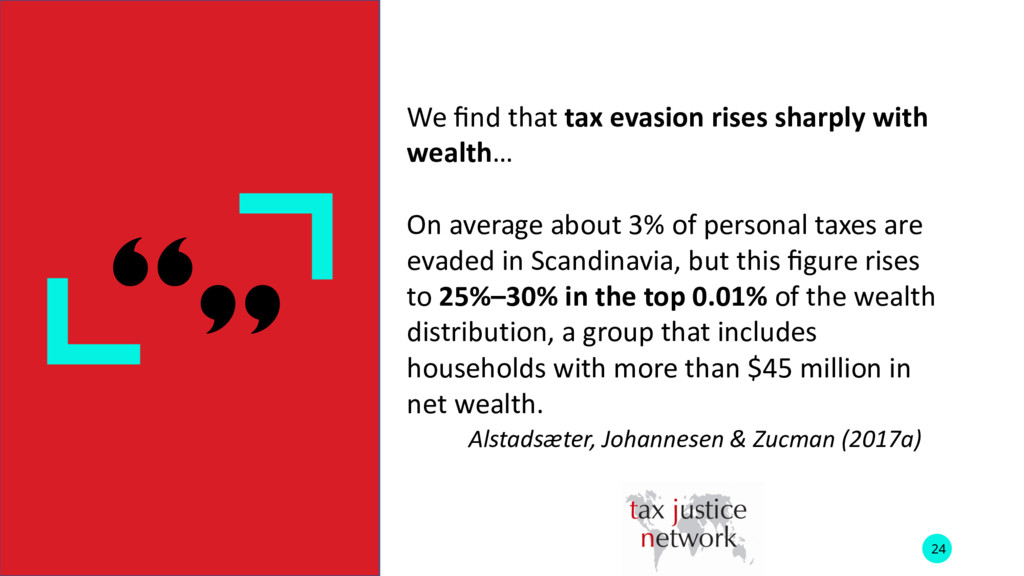

On average about 3% of personal taxes are evaded in Scandinavia, but this figure rises to 25%–30% in the top 0.01% of the wealth distribution, a group that includes households with more than $45 million in net wealth. Alstadsæter, Johannesen & Zucman (2017a) 24

owners of wealth are not scrupulously honest; effective wealth tax is impossible. §Do we know – can we know – who owns wealth? §The ‘end’ of bank secrecy §Registers of beneficial ownership… §…Global financial registry 25

the potential for: § Linking information held (TINs – and global?) § Expanding information exchange networks §Evidence from the US (IRS, various) suggests that taxpayer compliance rates increase 7- or 8-fold when information is automatically provided to authorities by a third party. §But which countries are included in information exchange? 26

long-standing TJN position – fully multilateral, automatic exchange of financial information (AEoI) §So far however, it has failed to live up to that billing: § Not multilateral, but dating system of bilateral preferences; and § Rigid reciprocity requirements §Result: § Much less progress overall than expected, and § Systematic exclusion of lower-income countries which may suffer most 27

preferences §Ownership data strengthens both market and state functioning §Publication of aggregate undeclared wealth data ensures accountability for progress §To the extent that tax compliance depends on (perceptions of) redistribution and others’ compliance, public information on the gap between declared and undeclared wealth can support tax morale 29

with ‘best practice’ baseline – e.g. capital gains tax, SDG inequality targets §Information best practice: § use and integration of taxpayer information § communication with public § recognition of political horizon issues => accountability key § ABC of tax transparency §Wealth tax preparation § CRS-readiness, and openness of other participants? § Willingness to take counter-measures against opacity? 30

IMF, UN and member states § Flexible reciprocity arrangements § Revert to intended multilateral approach § Develop SDG indicator/s (under 16.4): § Proportion of world (GDP, population) to which jurisdictions provide AEoI § Ratio of declared to (declared + undeclared) offshore wealth (where AEoI) § Ratio of registered legal entities for which public beneficial ownership info § International financial transparency convention (+counter- measures) § Explore potential for global financial registry 31

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}