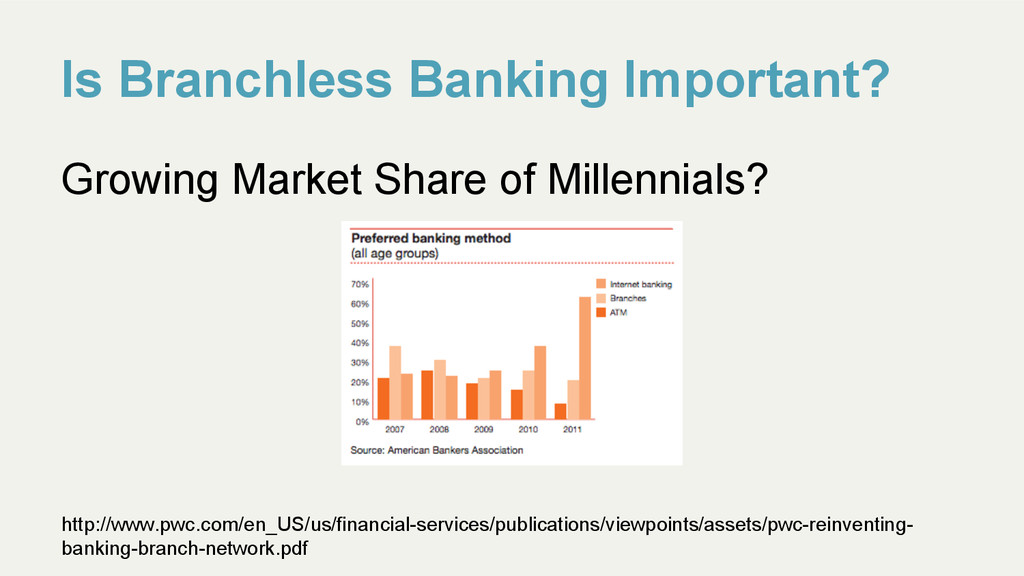

It is the mobile age. Smartphones and tablets have become incredibly popular in such a short span of time; providing access to internet services to a larger and broader demographic audience. The proliferation of social media, cloud applications, and e-commerce have redefined the banking expectations and needs of a customer. Therefore the mobile/internet channel is fast becoming a banking distribution channel that banks should focus on.

As this goes on, the widening of gap between customers and financial services would be inevitable. This leads to opportunities for new products, services, or even a new kind of "bank" to compete, disrupt the industry, and fulfil that demand.

The seminar will look at the importance, business model, implementation for mobile branchless banking & payment in this region (Singapore/South East Asia).

This presentation was given at Singapore Management University (SMU)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}