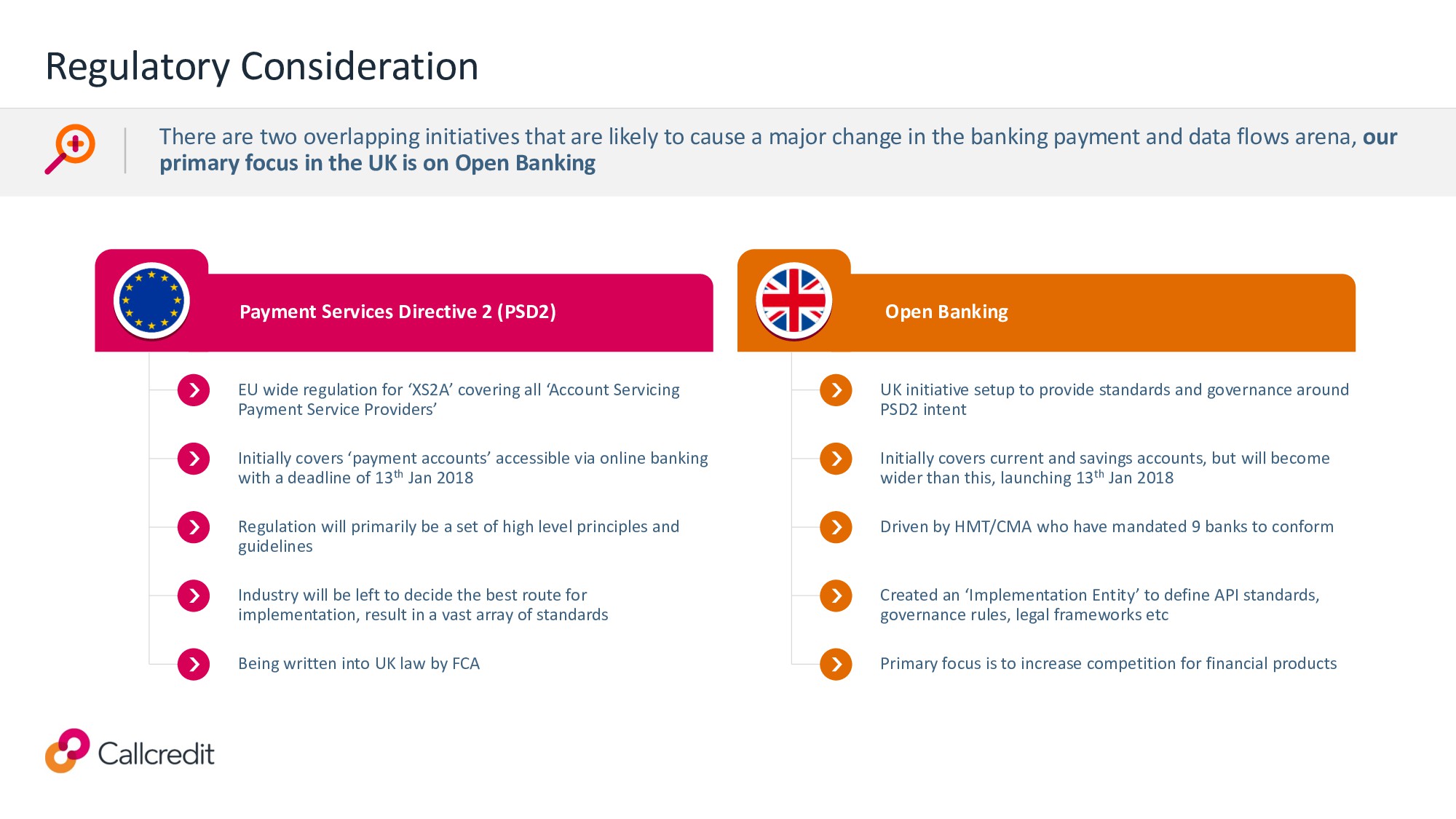

to cause a major change in the banking payment and data flows arena, our primary focus in the UK is on Open Banking Payment Services Directive 2 (PSD2) EU wide regulation for ‘XS2A’ covering all ‘Account Servicing Payment Service Providers’ Initially covers ‘payment accounts’ accessible via online banking with a deadline of 13th Jan 2018 Regulation will primarily be a set of high level principles and guidelines Industry will be left to decide the best route for implementation, result in a vast array of standards Being written into UK law by FCA Open Banking UK initiative setup to provide standards and governance around PSD2 intent Initially covers current and savings accounts, but will become wider than this, launching 13th Jan 2018 Driven by HMT/CMA who have mandated 9 banks to conform Created an ‘Implementation Entity’ to define API standards, governance rules, legal frameworks etc Primary focus is to increase competition for financial products

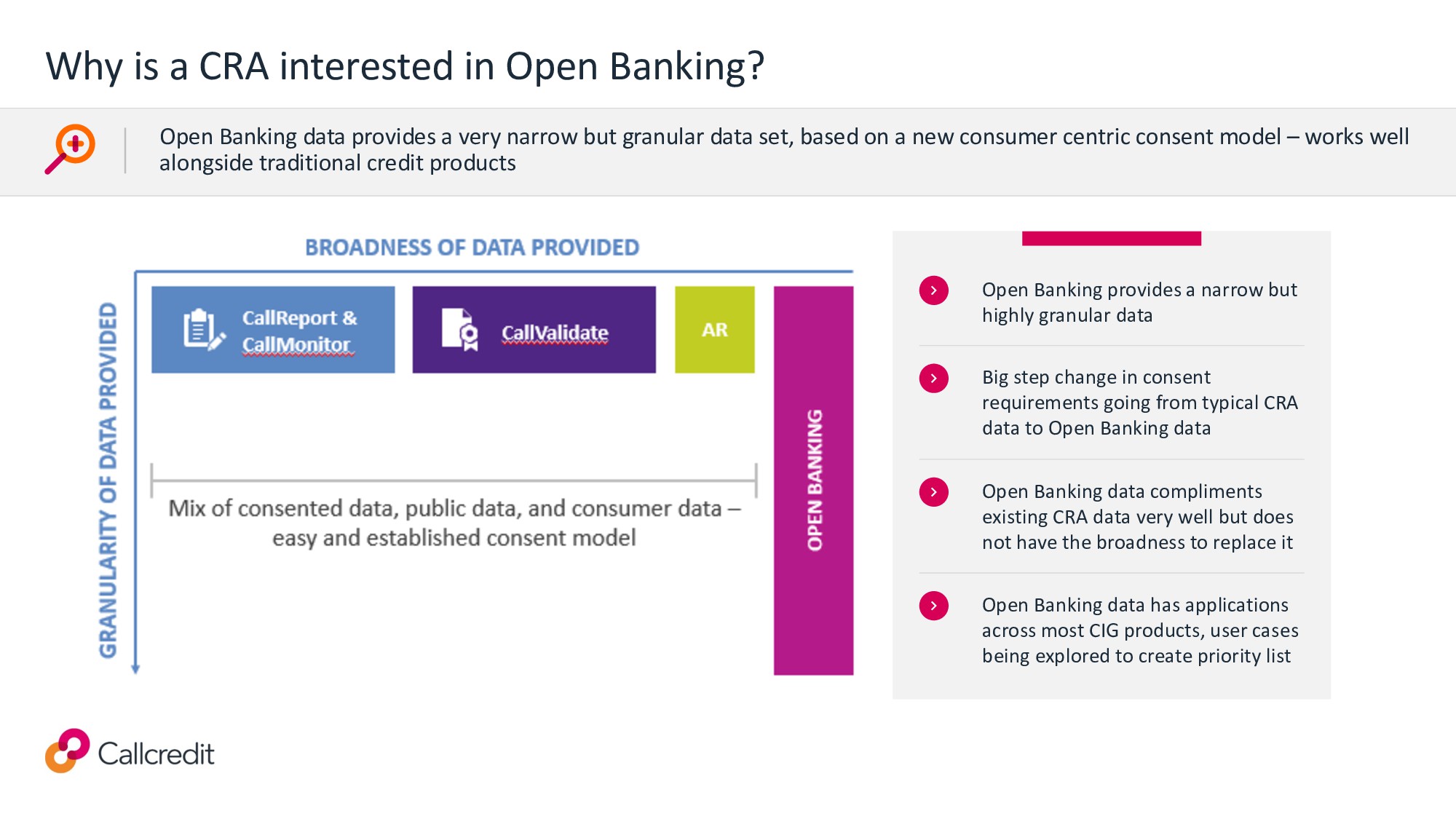

provides a narrow but highly granular data Open Banking data compliments existing CRA data very well but does not have the broadness to replace it Big step change in consent requirements going from typical CRA data to Open Banking data Open Banking data has applications across most CIG products, user cases being explored to create priority list Open Banking data provides a very narrow but granular data set, based on a new consumer centric consent model – works well alongside traditional credit products

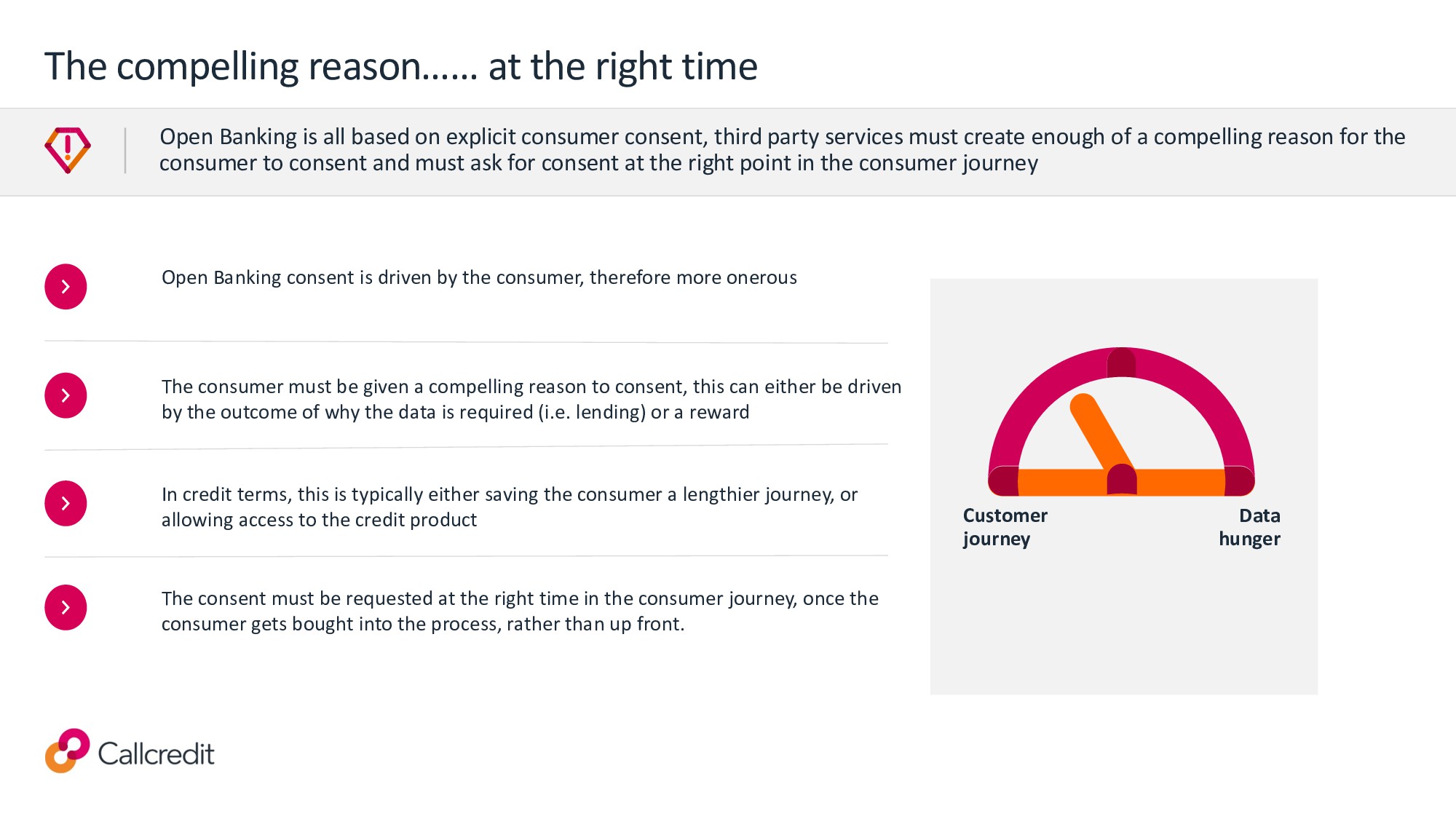

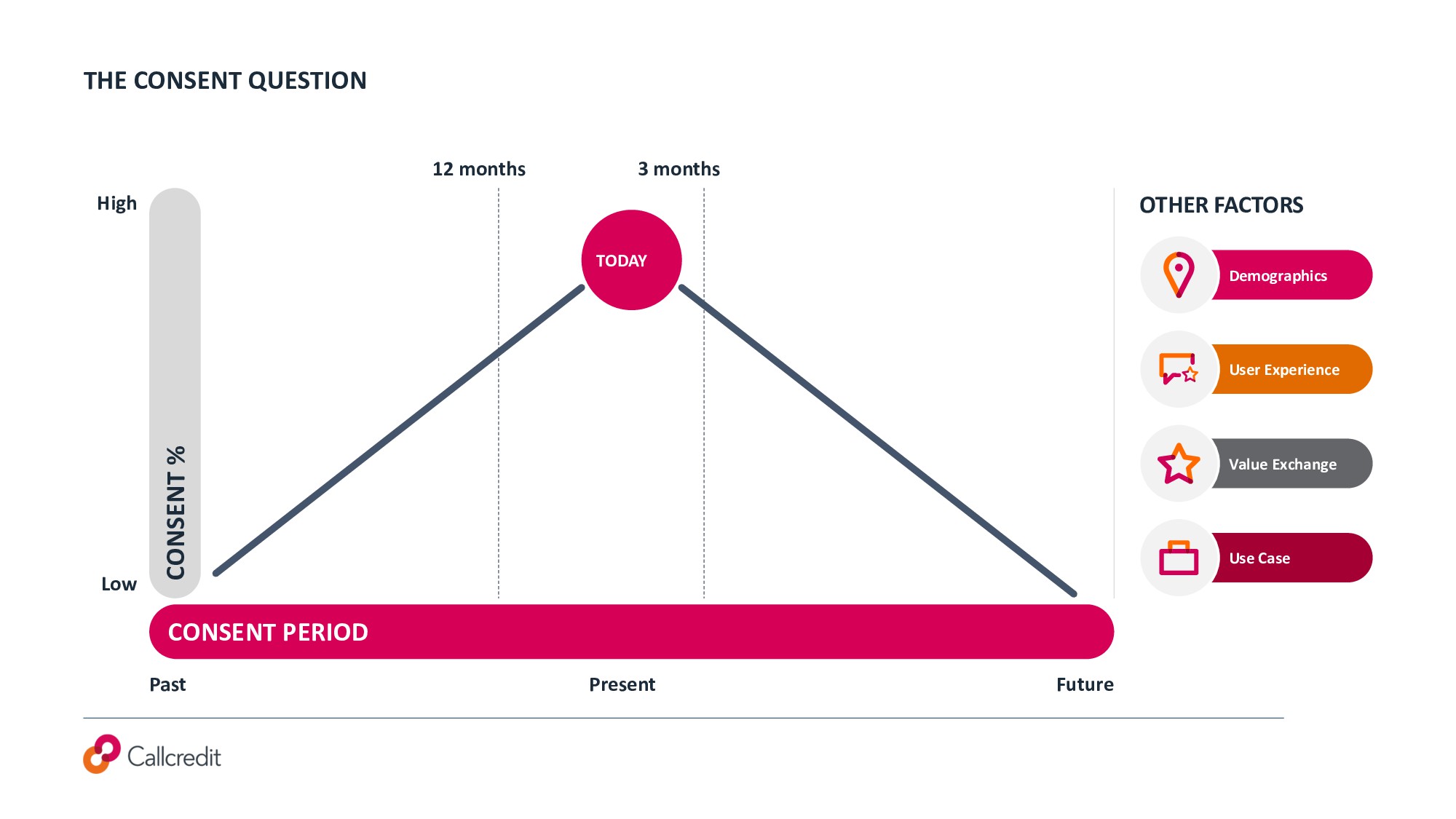

is driven by the consumer, therefore more onerous The consumer must be given a compelling reason to consent, this can either be driven by the outcome of why the data is required (i.e. lending) or a reward In credit terms, this is typically either saving the consumer a lengthier journey, or allowing access to the credit product The consent must be requested at the right time in the consumer journey, once the consumer gets bought into the process, rather than up front. Customer journey Data hunger Open Banking is all based on explicit consumer consent, third party services must create enough of a compelling reason for the consumer to consent and must ask for consent at the right point in the consumer journey

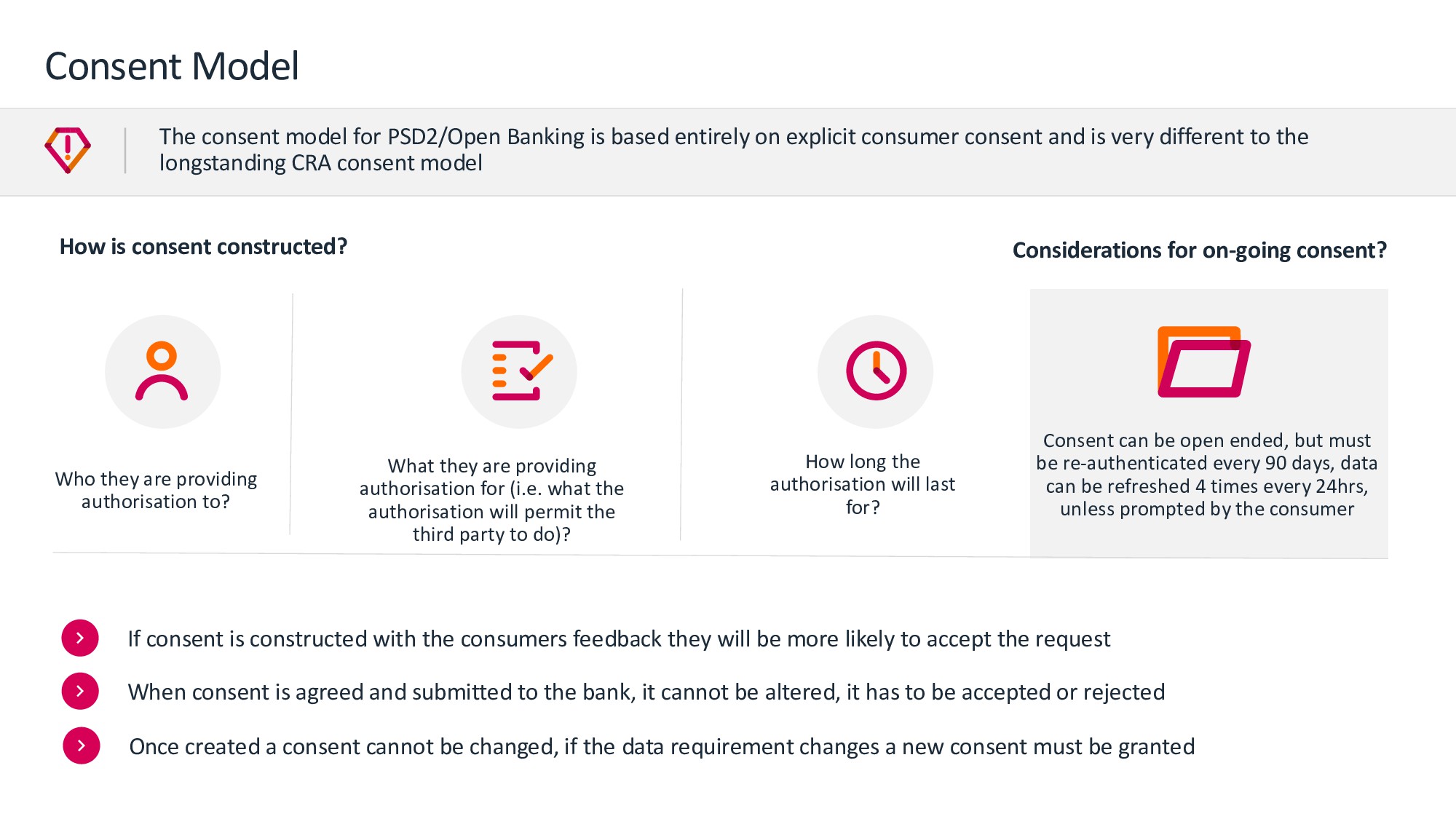

entirely on explicit consumer consent and is very different to the longstanding CRA consent model Who they are providing authorisation to? What they are providing authorisation for (i.e. what the authorisation will permit the third party to do)? How long the authorisation will last for? Consent can be open ended, but must be re-authenticated every 90 days, data can be refreshed 4 times every 24hrs, unless prompted by the consumer How is consent constructed? Considerations for on-going consent? If consent is constructed with the consumers feedback they will be more likely to accept the request When consent is agreed and submitted to the bank, it cannot be altered, it has to be accepted or rejected Once created a consent cannot be changed, if the data requirement changes a new consent must be granted

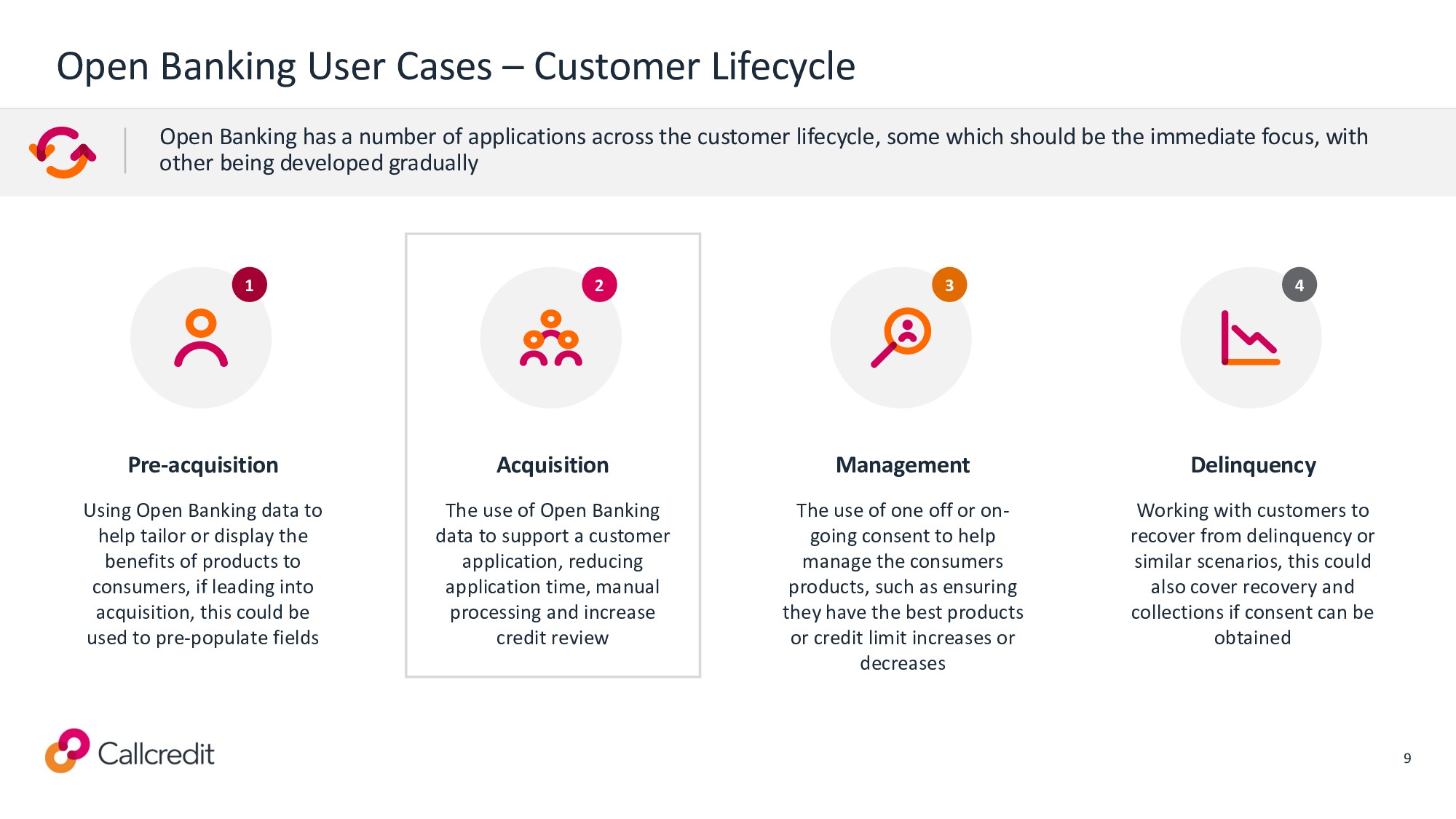

Banking data to help tailor or display the benefits of products to consumers, if leading into acquisition, this could be used to pre-populate fields The use of Open Banking data to support a customer application, reducing application time, manual processing and increase credit review The use of one off or on- going consent to help manage the consumers products, such as ensuring they have the best products or credit limit increases or decreases Working with customers to recover from delinquency or similar scenarios, this could also cover recovery and collections if consent can be obtained Pre-acquisition Acquisition Management Delinquency 1 2 3 4 Open Banking has a number of applications across the customer lifecycle, some which should be the immediate focus, with other being developed gradually

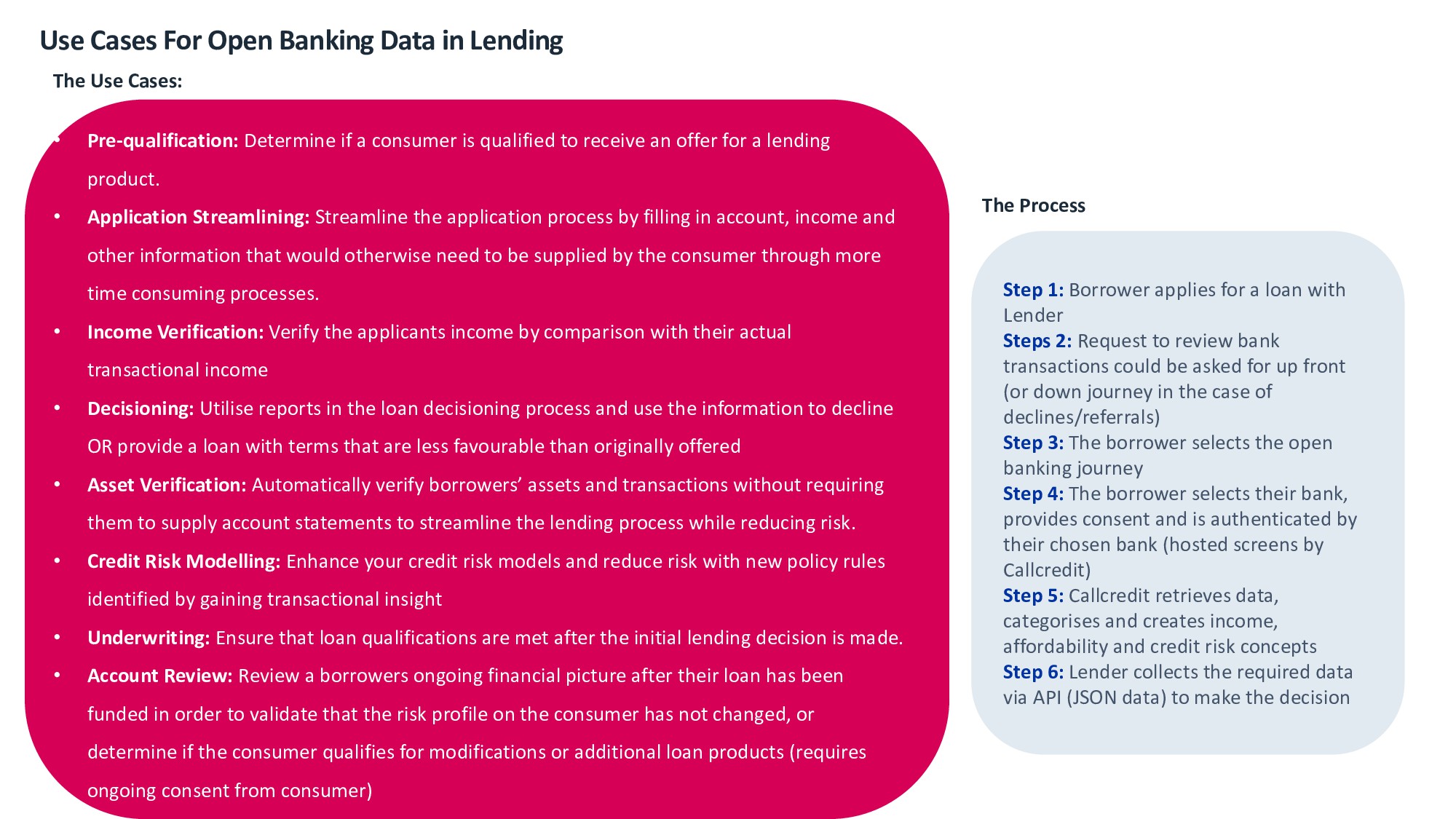

2: Request to review bank transactions could be asked for up front (or down journey in the case of declines/referrals) Step 3: The borrower selects the open banking journey Step 4: The borrower selects their bank, provides consent and is authenticated by their chosen bank (hosted screens by Callcredit) Step 5: Callcredit retrieves data, categorises and creates income, affordability and credit risk concepts Step 6: Lender collects the required data via API (JSON data) to make the decision The Use Cases: • Pre-qualification: Determine if a consumer is qualified to receive an offer for a lending product. • Application Streamlining: Streamline the application process by filling in account, income and other information that would otherwise need to be supplied by the consumer through more time consuming processes. • Income Verification: Verify the applicants income by comparison with their actual transactional income • Decisioning: Utilise reports in the loan decisioning process and use the information to decline OR provide a loan with terms that are less favourable than originally offered • Asset Verification: Automatically verify borrowers’ assets and transactions without requiring them to supply account statements to streamline the lending process while reducing risk. • Credit Risk Modelling: Enhance your credit risk models and reduce risk with new policy rules identified by gaining transactional insight • Underwriting: Ensure that loan qualifications are met after the initial lending decision is made. • Account Review: Review a borrowers ongoing financial picture after their loan has been funded in order to validate that the risk profile on the consumer has not changed, or determine if the consumer qualifies for modifications or additional loan products (requires ongoing consent from consumer) Use Cases For Open Banking Data in Lending The Process

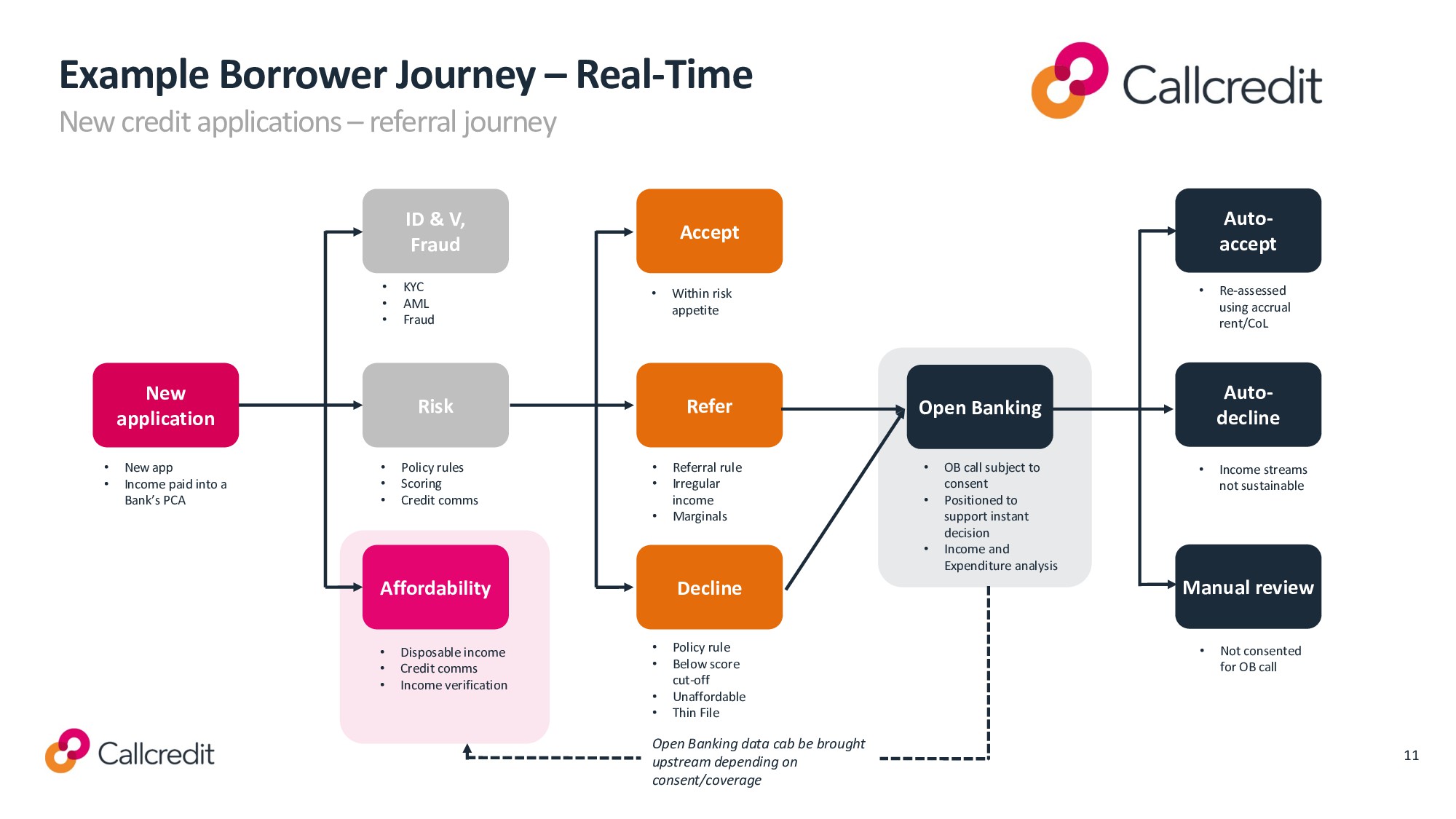

journey New application ID & V, Fraud Risk Affordability Accept Refer Decline Auto- accept Auto- decline Manual review Open Banking • KYC • AML • Fraud • Policy rules • Scoring • Credit comms • Disposable income • Credit comms • Income verification • Within risk appetite • Referral rule • Irregular income • Marginals • Policy rule • Below score cut-off • Unaffordable • Thin File • OB call subject to consent • Positioned to support instant decision • Income and Expenditure analysis • Re-assessed using accrual rent/CoL • Income streams not sustainable • Not consented for OB call • New app • Income paid into a Bank’s PCA Open Banking data cab be brought upstream depending on consent/coverage 11

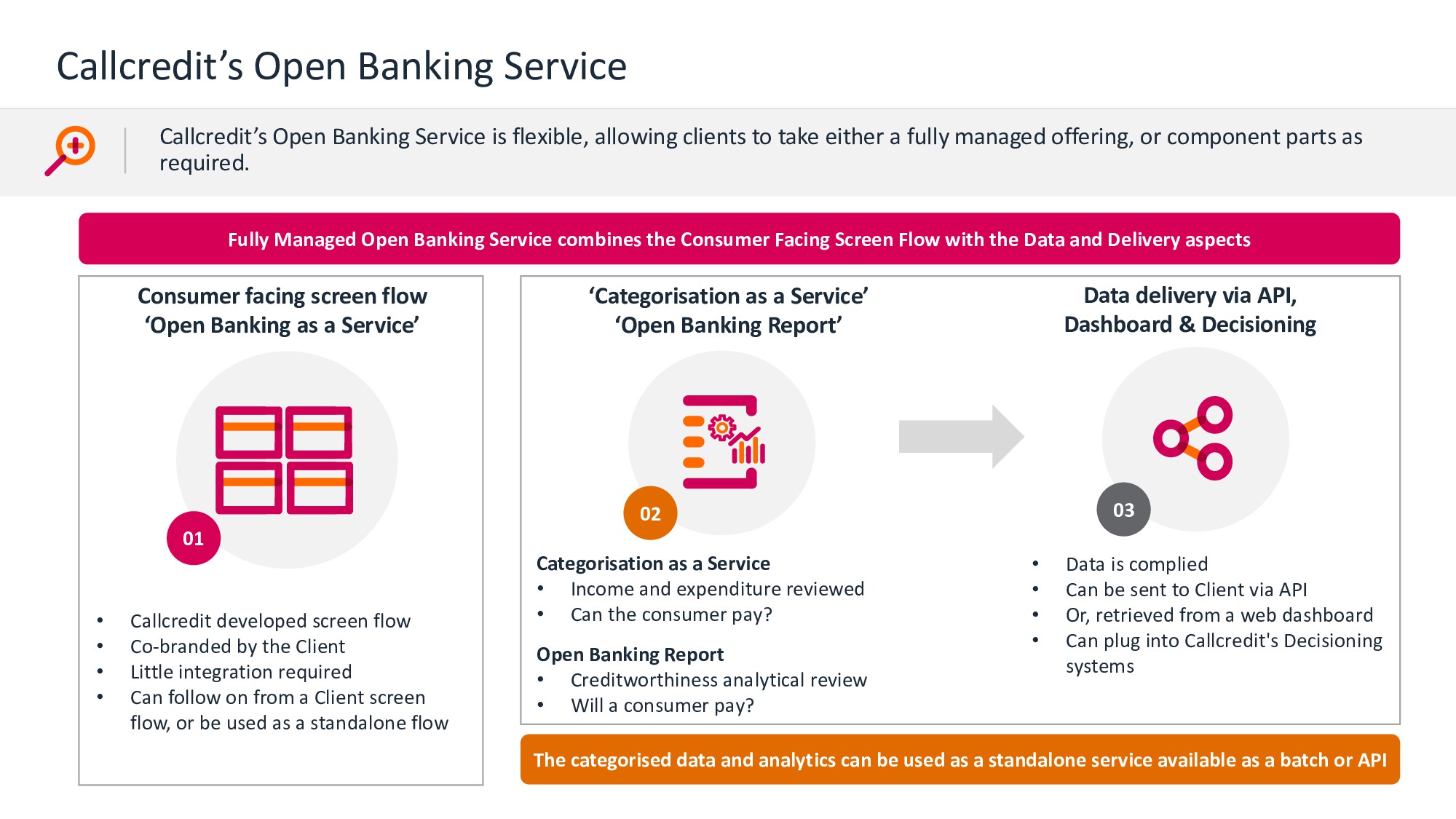

allowing clients to take either a fully managed offering, or component parts as required. Consumer facing screen flow ‘Open Banking as a Service’ 01 ‘Categorisation as a Service’ ‘Open Banking Report’ 02 Data delivery via API, Dashboard & Decisioning 03 • Callcredit developed screen flow • Co-branded by the Client • Little integration required • Can follow on from a Client screen flow, or be used as a standalone flow Categorisation as a Service • Income and expenditure reviewed • Can the consumer pay? Open Banking Report • Creditworthiness analytical review • Will a consumer pay? • Data is complied • Can be sent to Client via API • Or, retrieved from a web dashboard • Can plug into Callcredit's Decisioning systems Fully Managed Open Banking Service combines the Consumer Facing Screen Flow with the Data and Delivery aspects The categorised data and analytics can be used as a standalone service available as a batch or API

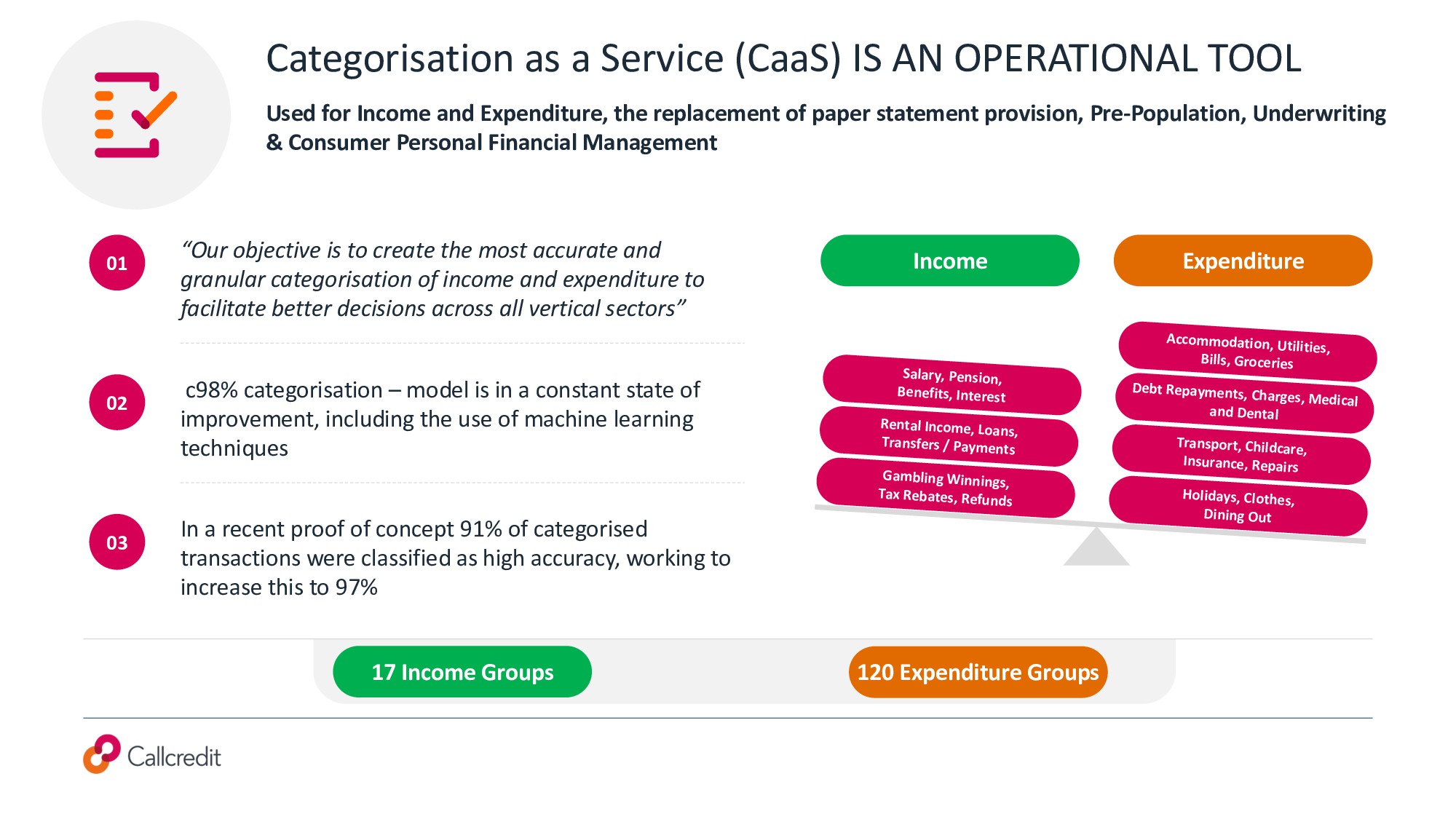

for Income and Expenditure, the replacement of paper statement provision, Pre-Population, Underwriting & Consumer Personal Financial Management 01 “Our objective is to create the most accurate and granular categorisation of income and expenditure to facilitate better decisions across all vertical sectors” 02 c98% categorisation – model is in a constant state of improvement, including the use of machine learning techniques 03 In a recent proof of concept 91% of categorised transactions were classified as high accuracy, working to increase this to 97% Income Expenditure Salary, Pension, Benefits, Interest Rental Income, Loans, Transfers / Payments Gambling Winnings, Tax Rebates, Refunds Accommodation, Utilities, Bills, Groceries Debt Repayments, Charges, Medical and Dental Transport, Childcare, Insurance, Repairs Holidays, Clothes, Dining Out 17 Income Groups 120 Expenditure Groups

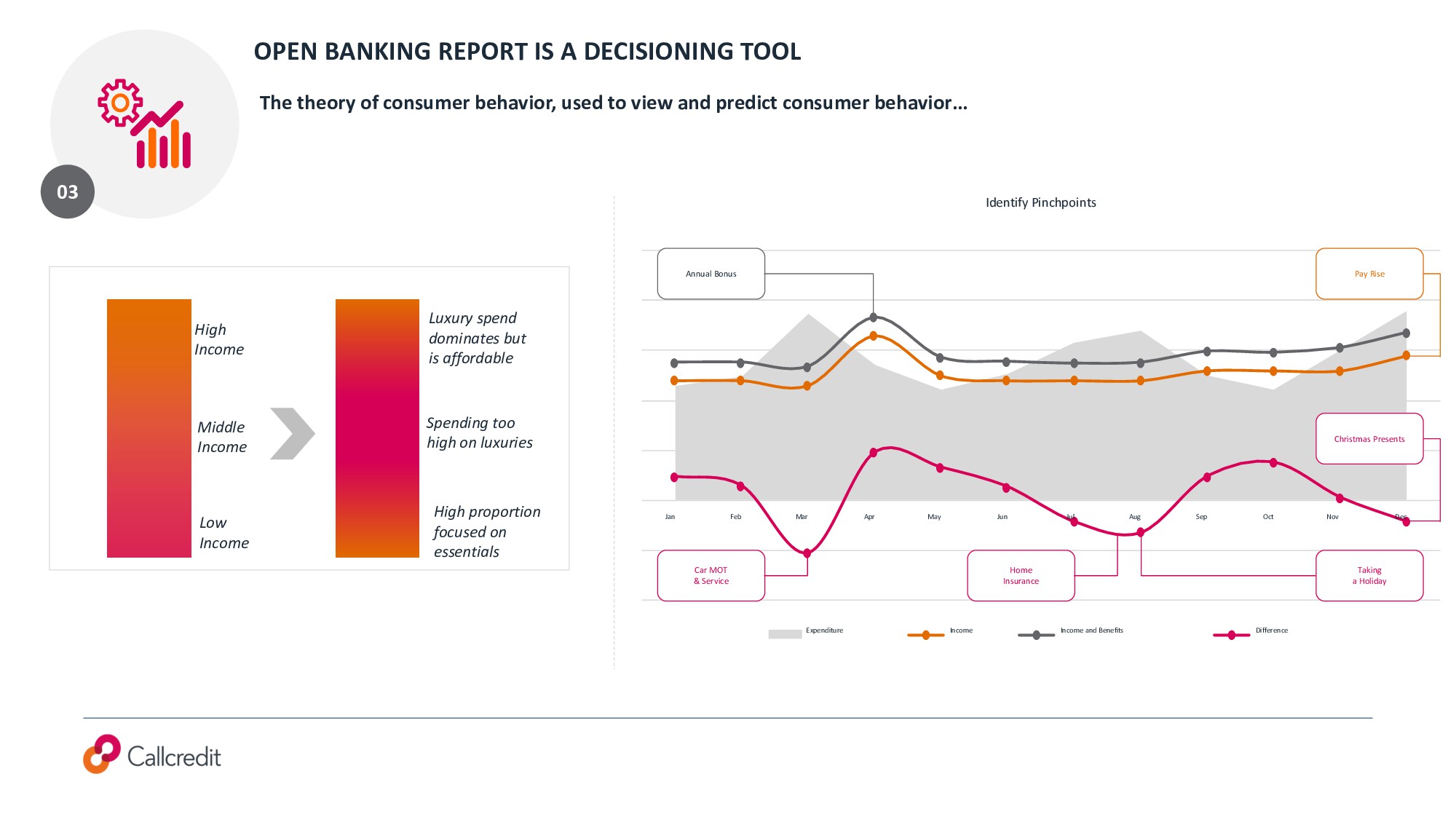

of consumer behavior, used to view and predict consumer behavior… High Income Middle Income Low Income Luxury spend dominates but is affordable Spending too high on luxuries High proportion focused on essentials Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Identify Pinchpoints Expenditure Income Income and Benefits Difference Pay Rise Christmas Presents Dec Taking a Holiday Home Insurance Car MOT & Service Annual Bonus

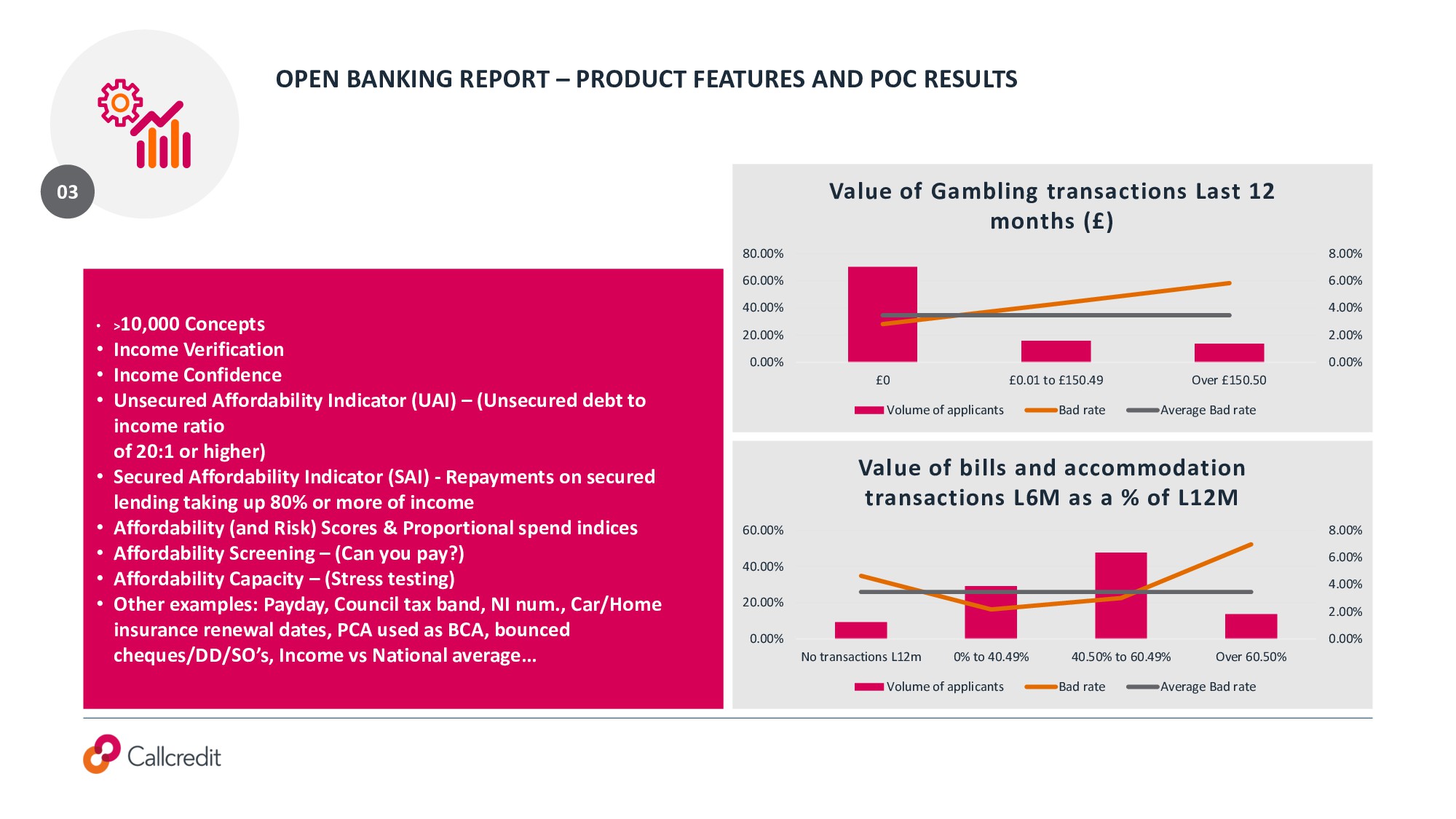

2.00% 4.00% 6.00% 8.00% 0.00% 20.00% 40.00% 60.00% 80.00% £0 £0.01 to £150.49 Over £150.50 Value of Gambling transactions Last 12 months (£) Volume of applicants Bad rate Average Bad rate 0.00% 2.00% 4.00% 6.00% 8.00% 0.00% 20.00% 40.00% 60.00% No transactions L12m 0% to 40.49% 40.50% to 60.49% Over 60.50% Value of bills and accommodation transactions L6M as a % of L12M Volume of applicants Bad rate Average Bad rate • >10,000 Concepts • Income Verification • Income Confidence • Unsecured Affordability Indicator (UAI) – (Unsecured debt to income ratio of 20:1 or higher) • Secured Affordability Indicator (SAI) - Repayments on secured lending taking up 80% or more of income • Affordability (and Risk) Scores & Proportional spend indices • Affordability Screening – (Can you pay?) • Affordability Capacity – (Stress testing) • Other examples: Payday, Council tax band, NI num., Car/Home insurance renewal dates, PCA used as BCA, bounced cheques/DD/SO’s, Income vs National average… 03

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}