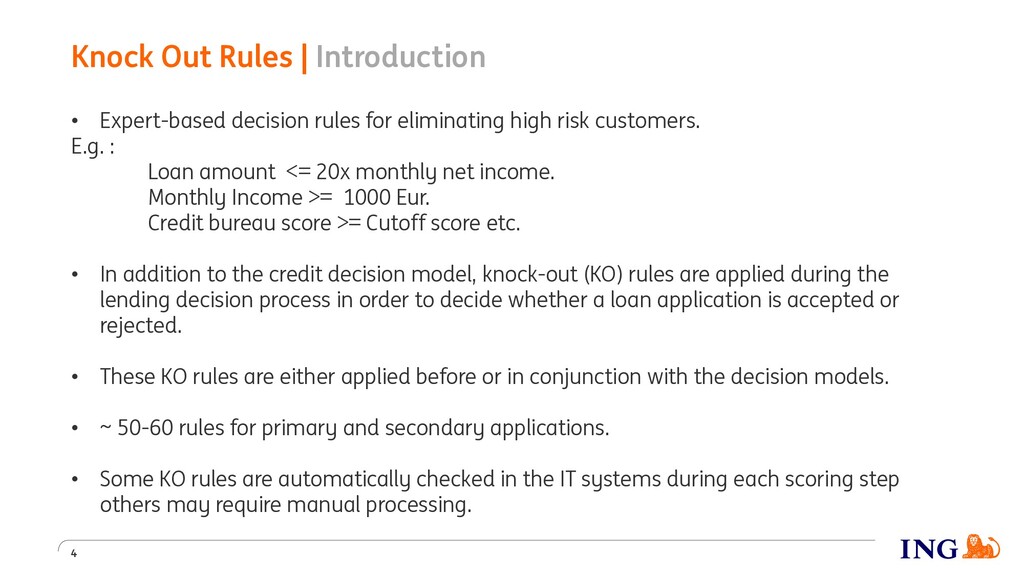

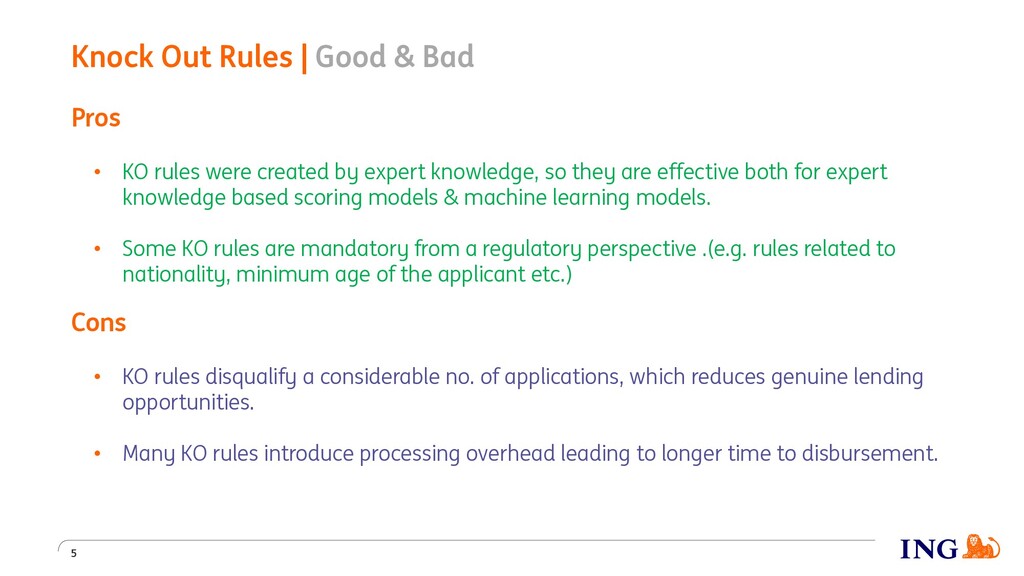

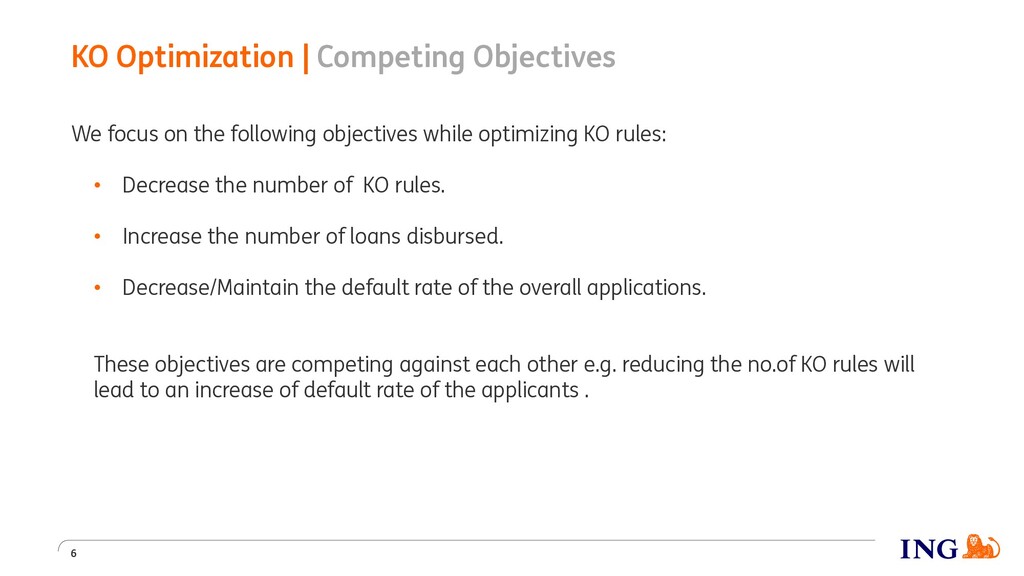

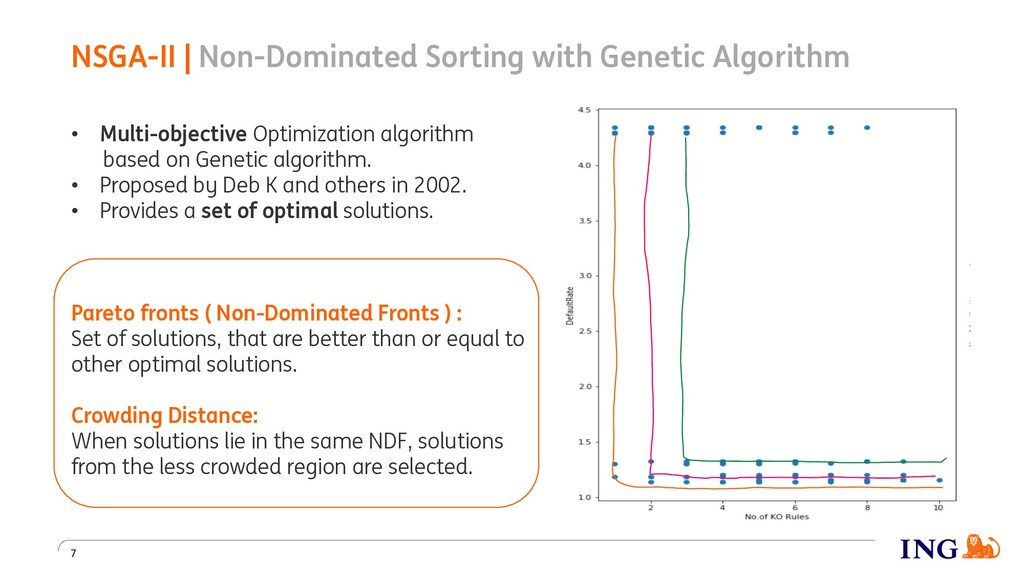

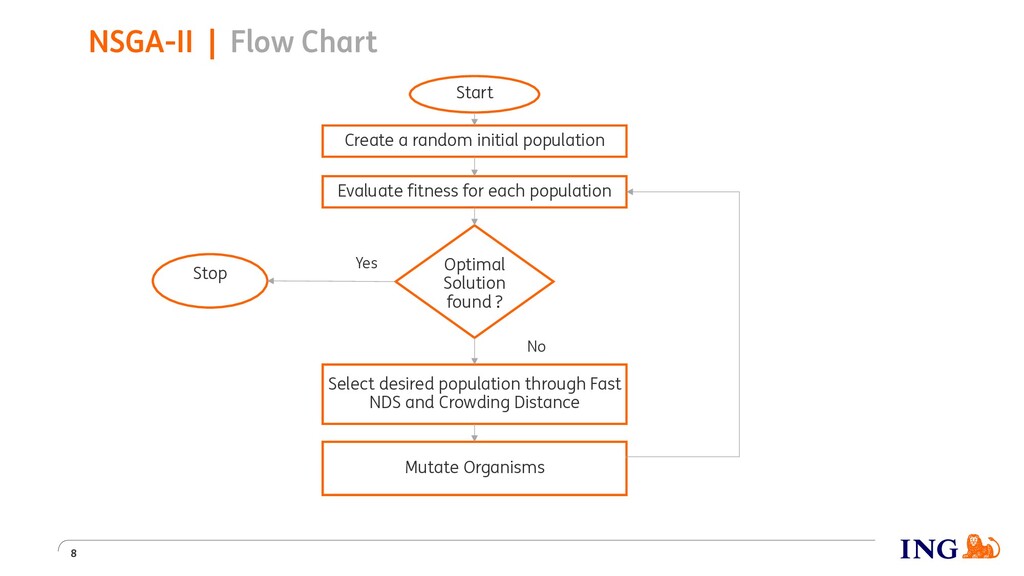

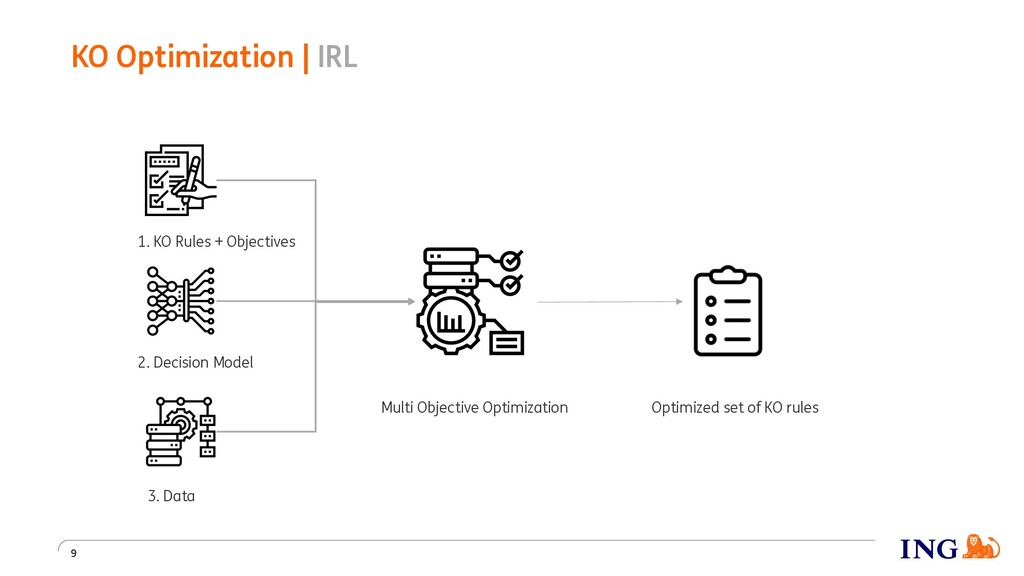

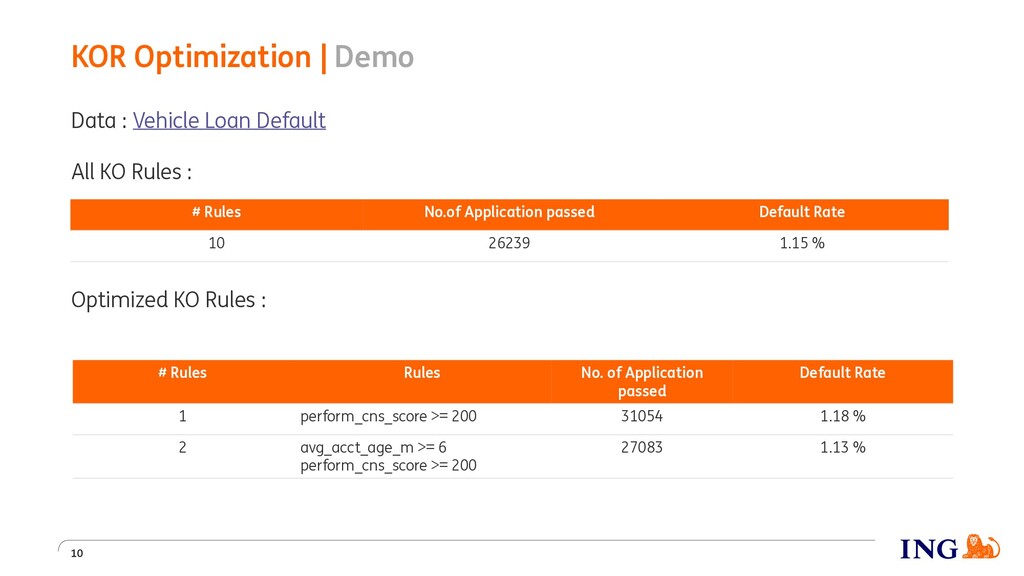

Historically banks have relied on expert scorecards for scoring their credit applications. This meant setting up of knock-out(KO) rules (e.g. age of the applicant > X years, applicant should be employed etc.). However for efficiency reasons there is a requirement to reduce the no.of KO rules applied, while keeping the default rate low. In this talk we will see, how a Multi-objective Optimisation method (NSGA-II) can be used to reduce the no.of KO rules while keeping the default rate as low as possible.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}