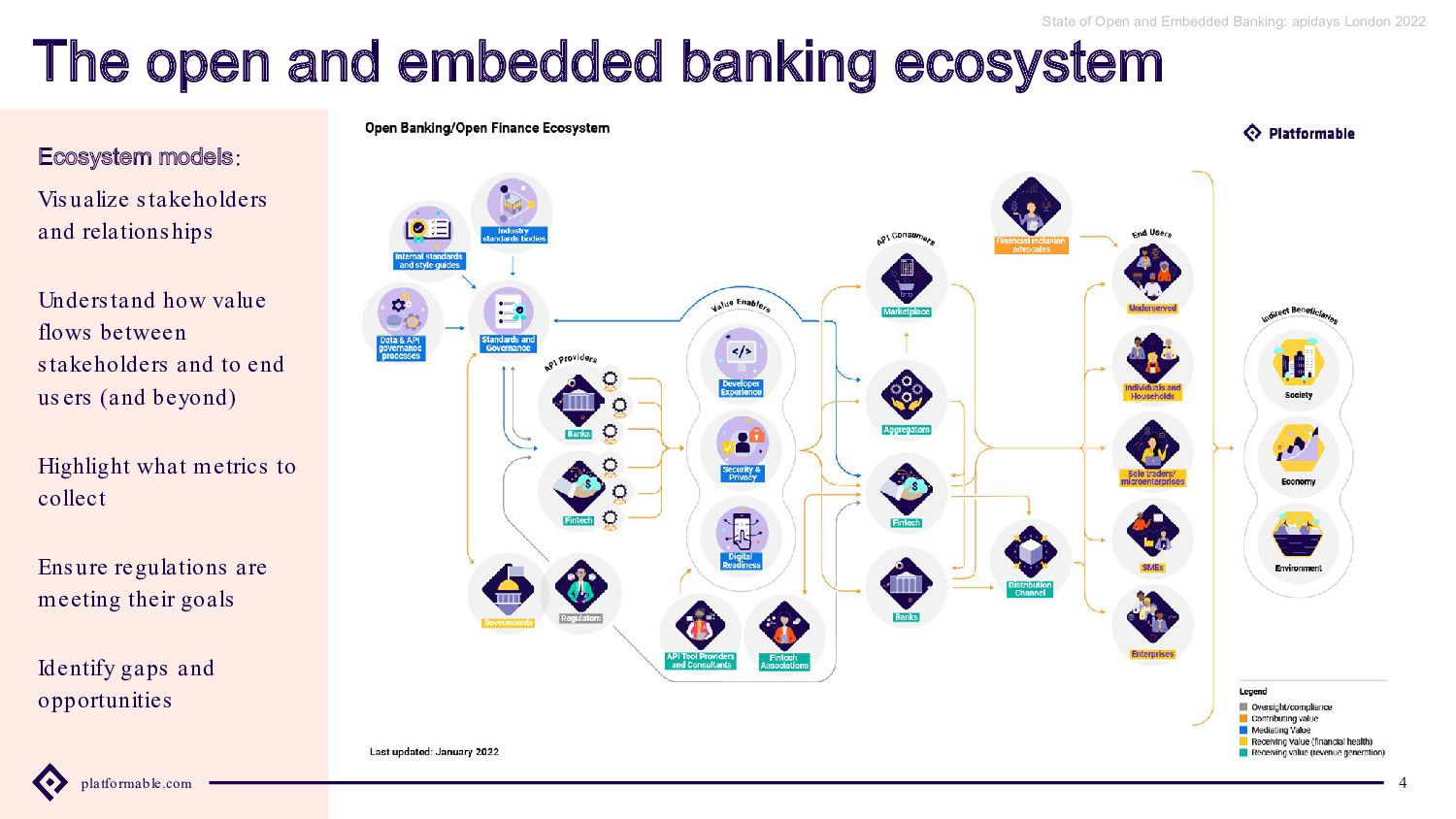

apidays London 2022 - The Path from Open Banking to Embedded Finance

October 26 & 27, 2022

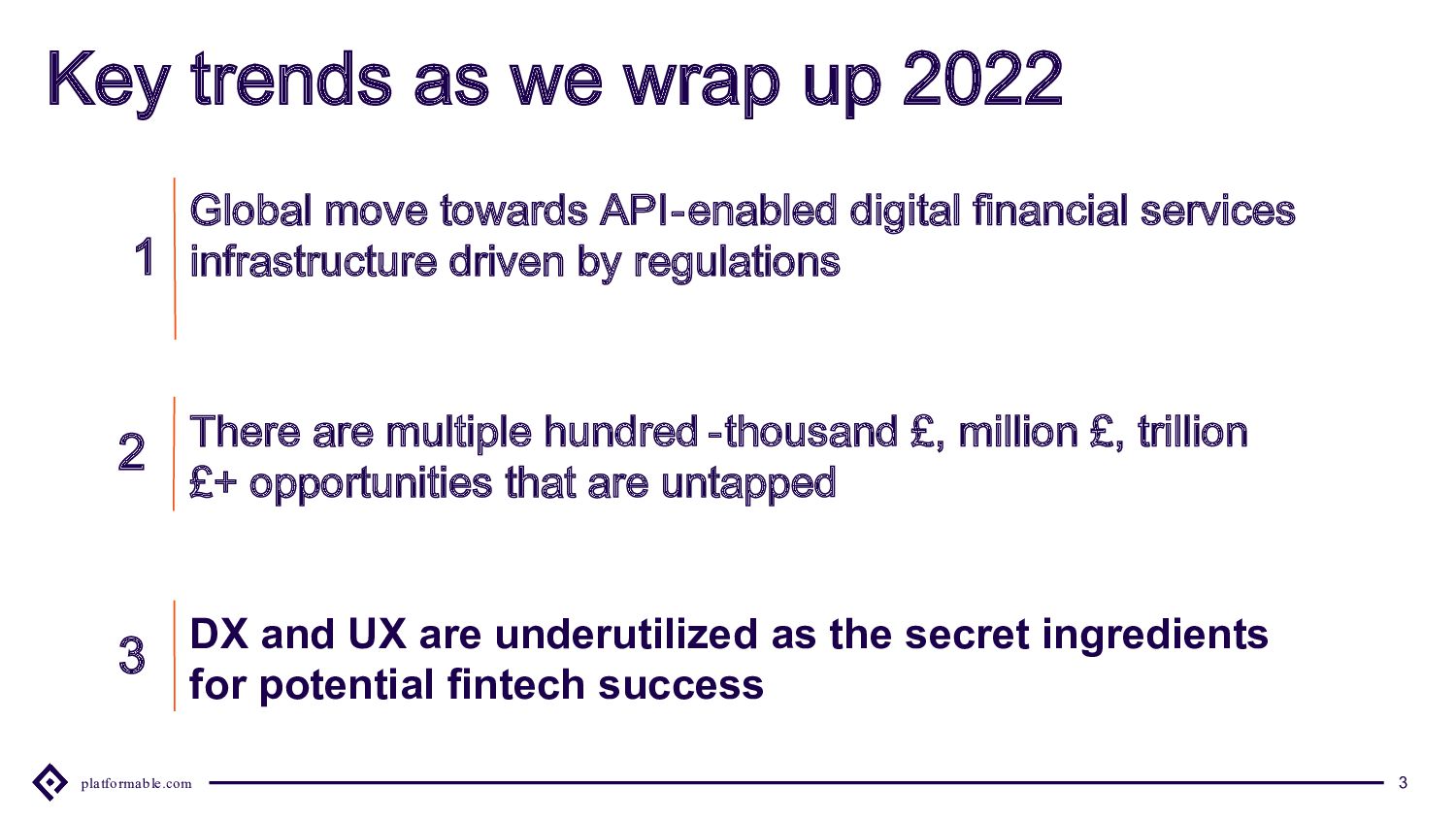

The State of Banking APIs 2022

Mark Boyd, Director at Platformable

------

Check out our conferences at https://www.apidays.global/

Do you want to sponsor or talk at one of our conferences?

https://apidays.typeform.com/to/ILJeAaV8

Learn more on APIscene, the global media made by the community for the community:

https://www.apiscene.io

Explore the API ecosystem with the API Landscape:

https://apilandscape.apiscene.io/

Deep dive into the API industry with our reports:

https://www.apidays.global/industry-reports/

Subscribe to our global newsletter:

https://apidays.typeform.com/to/i1MPEW

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![platformable.com [email protected] @mgboydcom https://www.linkedin.com/company/platformable Contact us](https://files.speakerdeck.com/presentations/6850a7999fba462b9bd0456b6eaedec8/slide_39.jpg){kind=link}