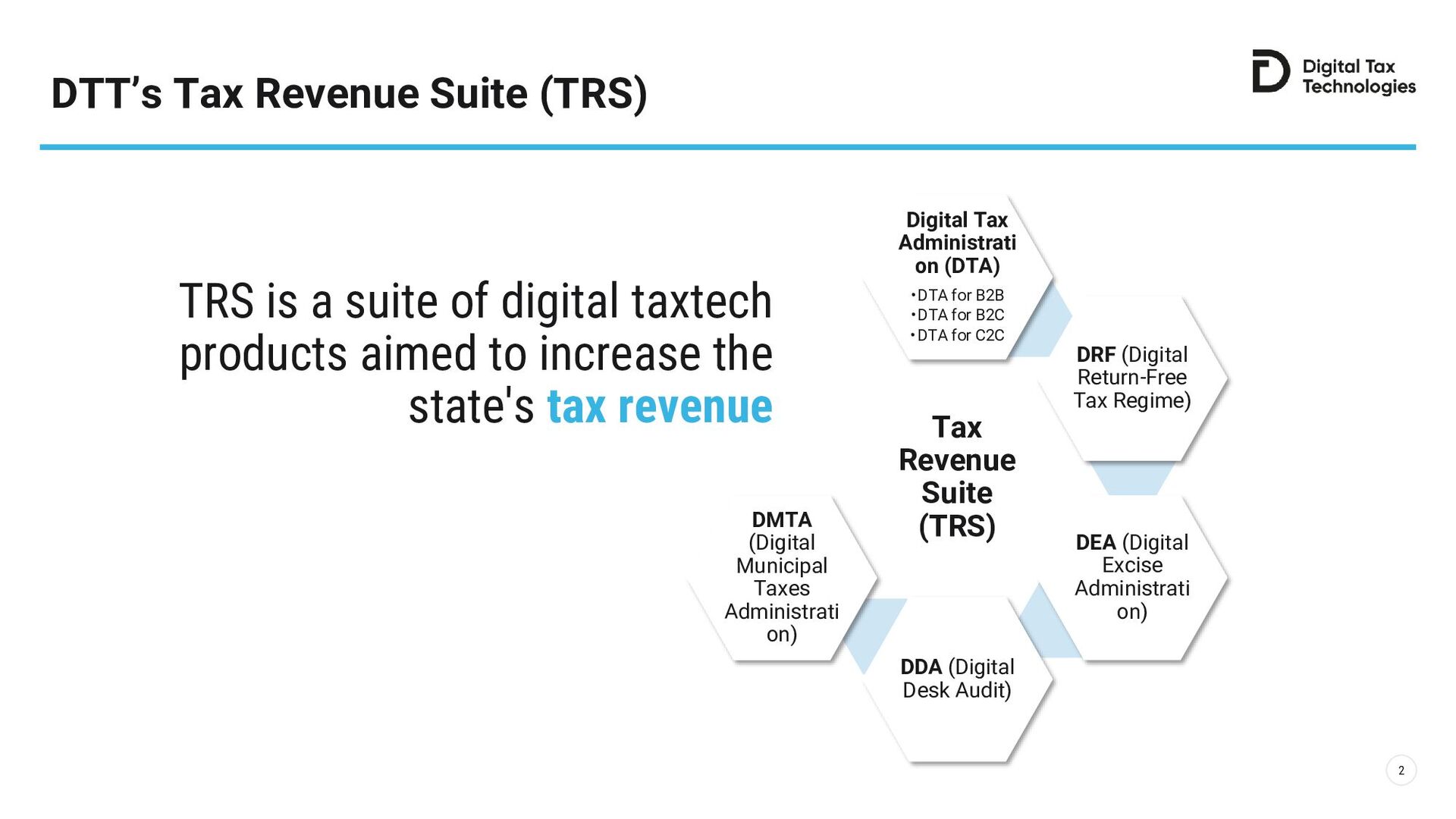

TRS is a suite of digital taxtech products aimed to increase the state's tax revenue.

TRS offers digital tax administration solutions for B2B, B2C, C2C, return-free tax regimes, excise administration, digital desk audit, and municipal taxes administration, enabling efficient tax collection and enforcement while preventing tax evasion and errors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

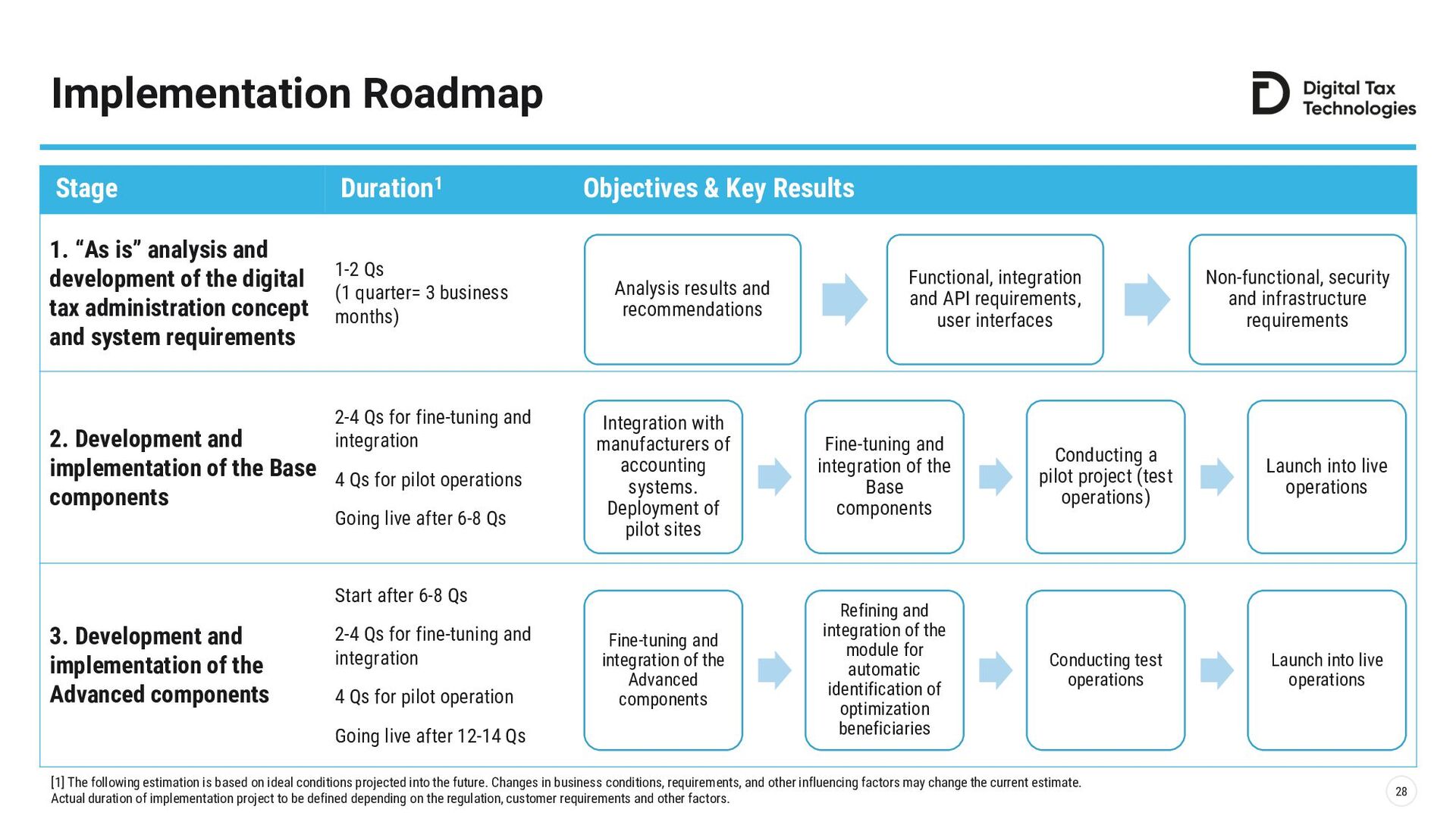

![Timeline 1 [1] The following estimation is based on ideal](https://files.speakerdeck.com/presentations/82dd72a2be534a78a1aed0bad641b112/slide_28.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}