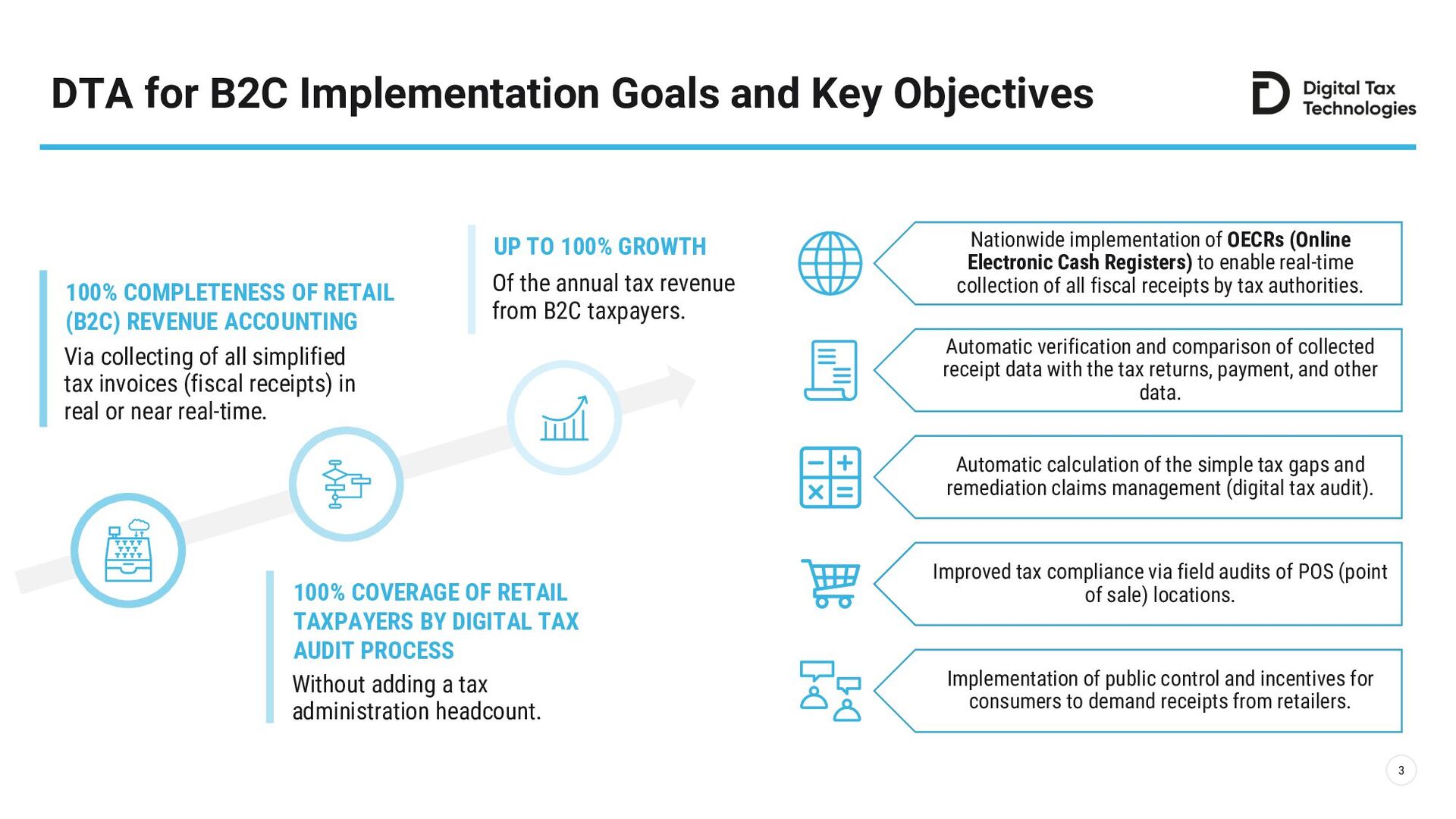

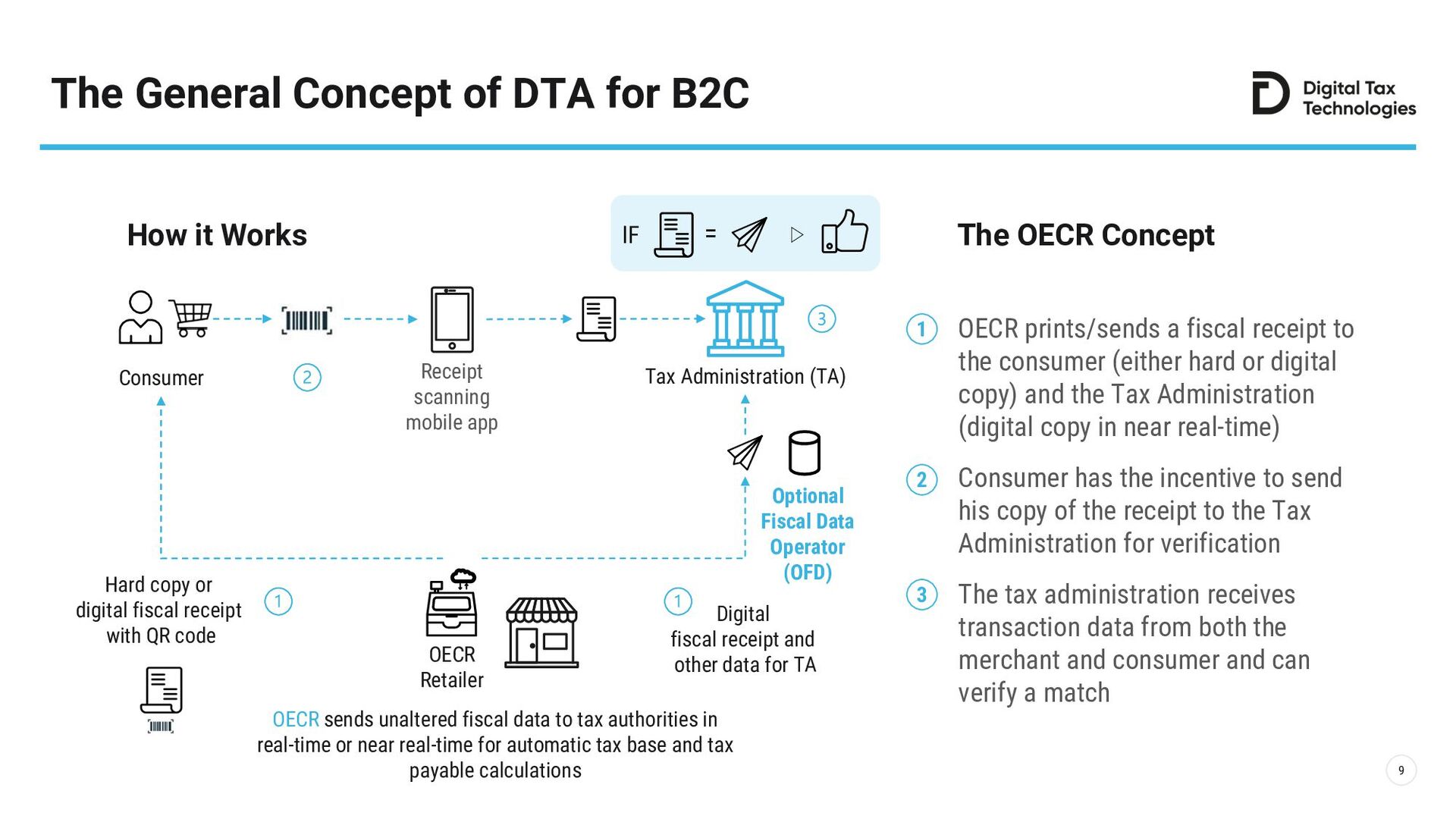

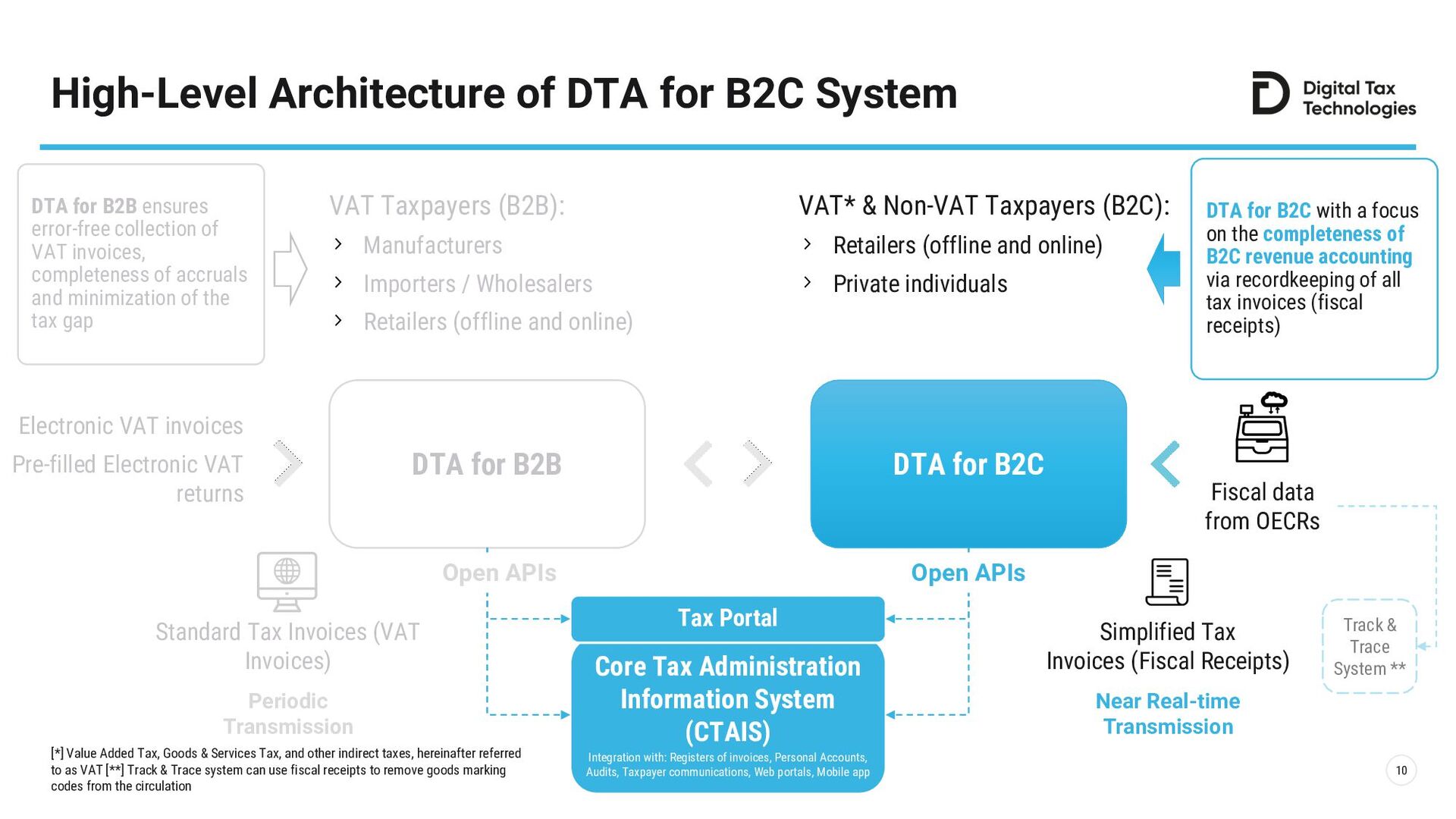

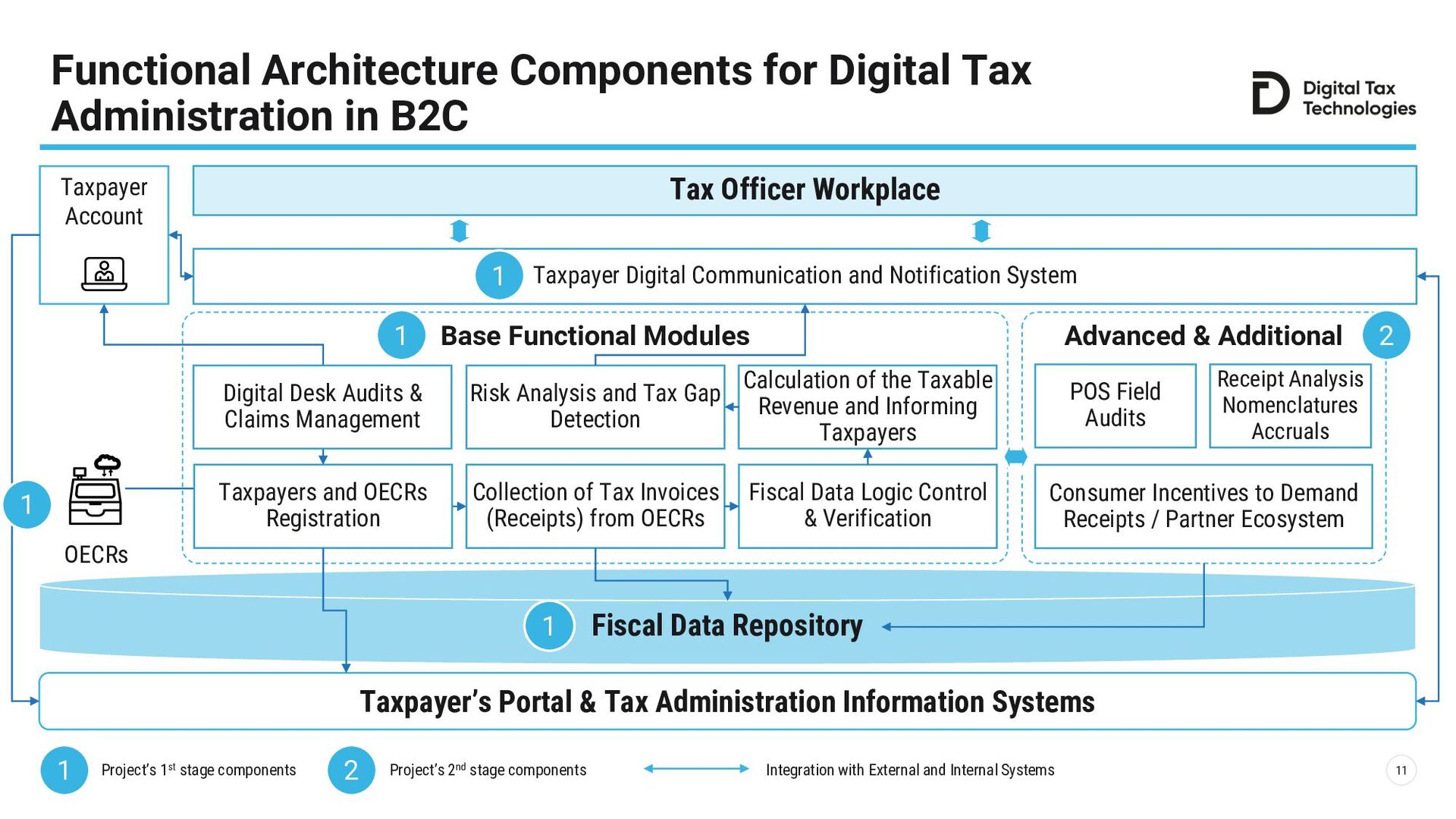

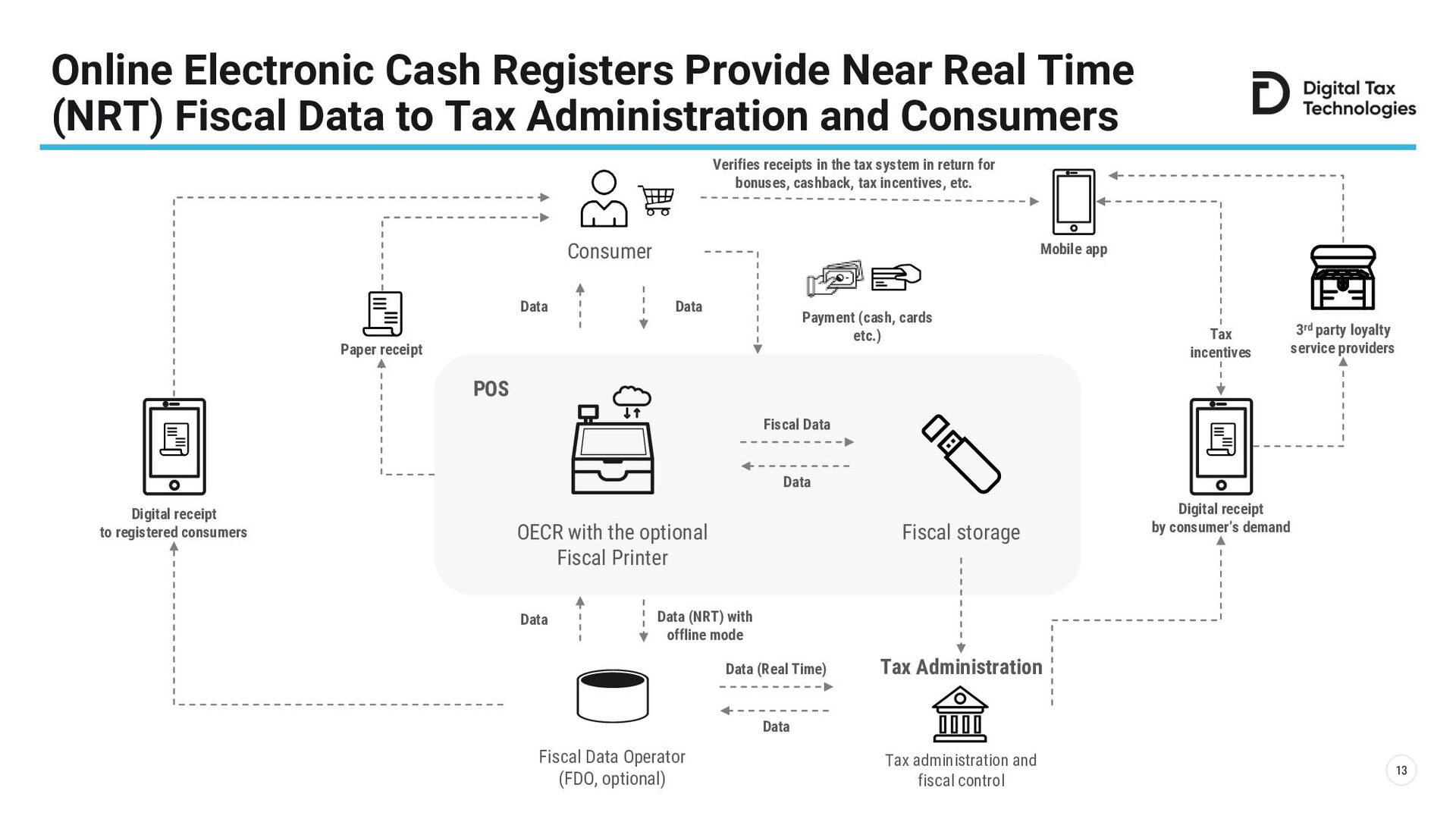

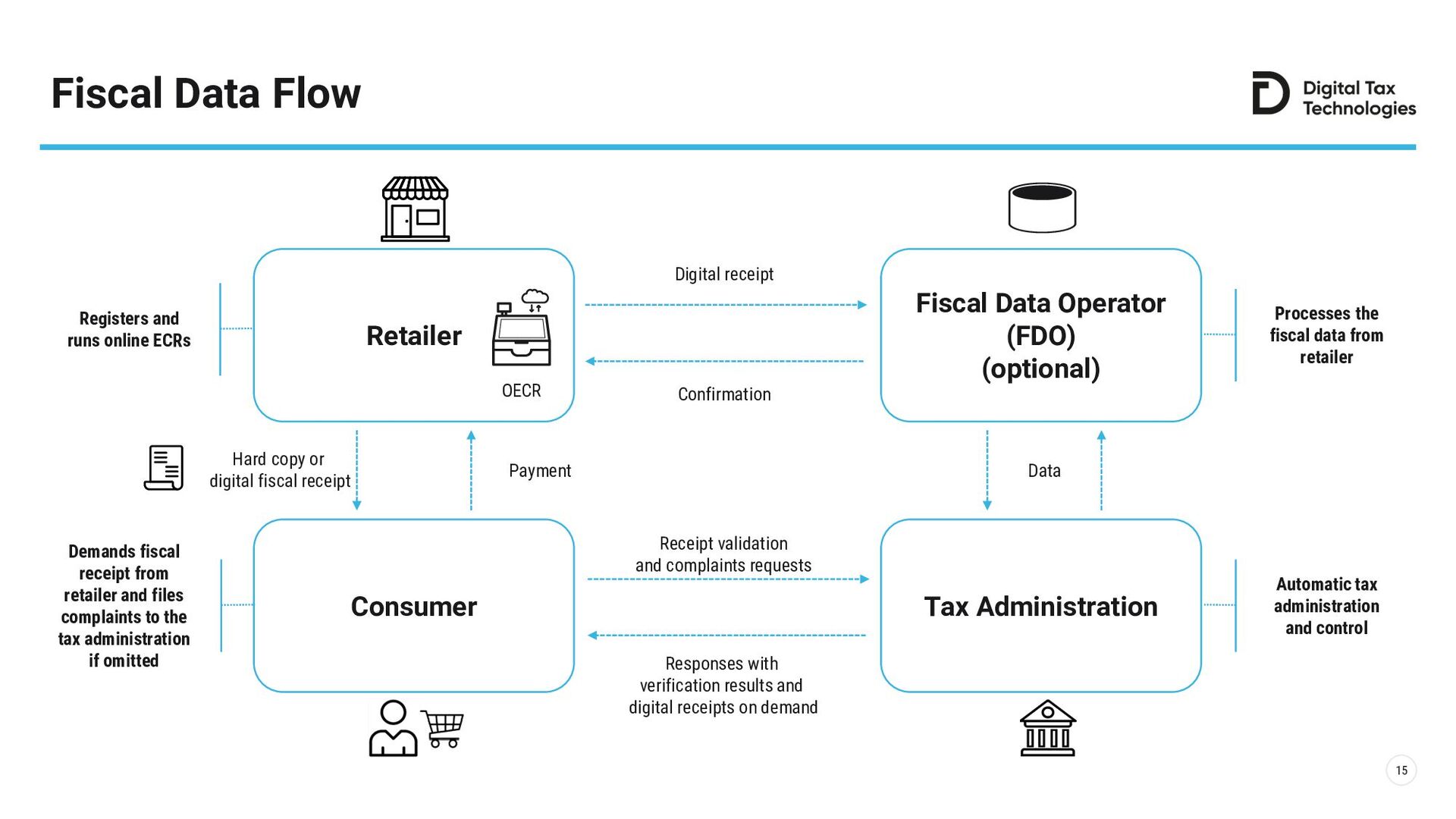

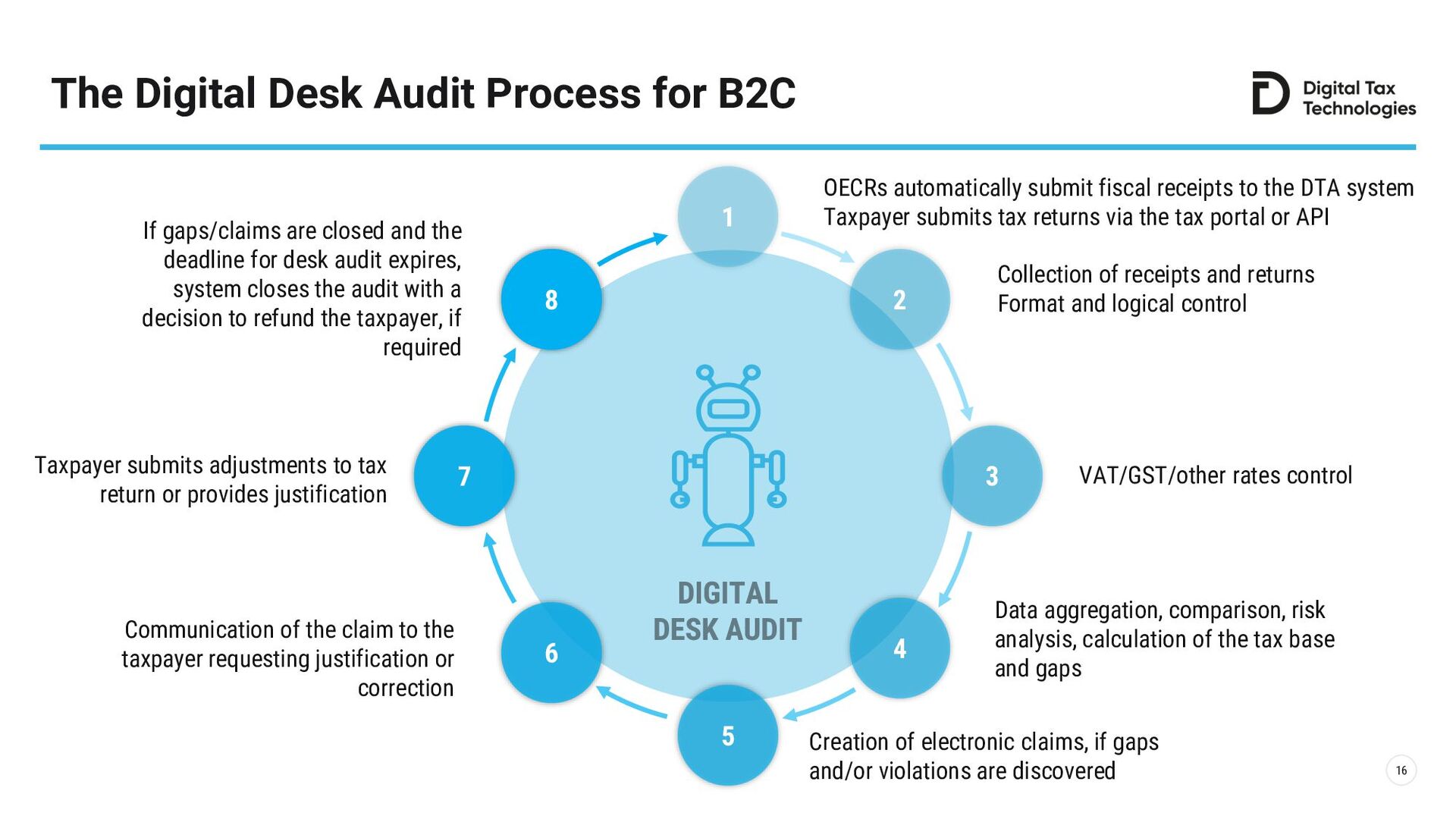

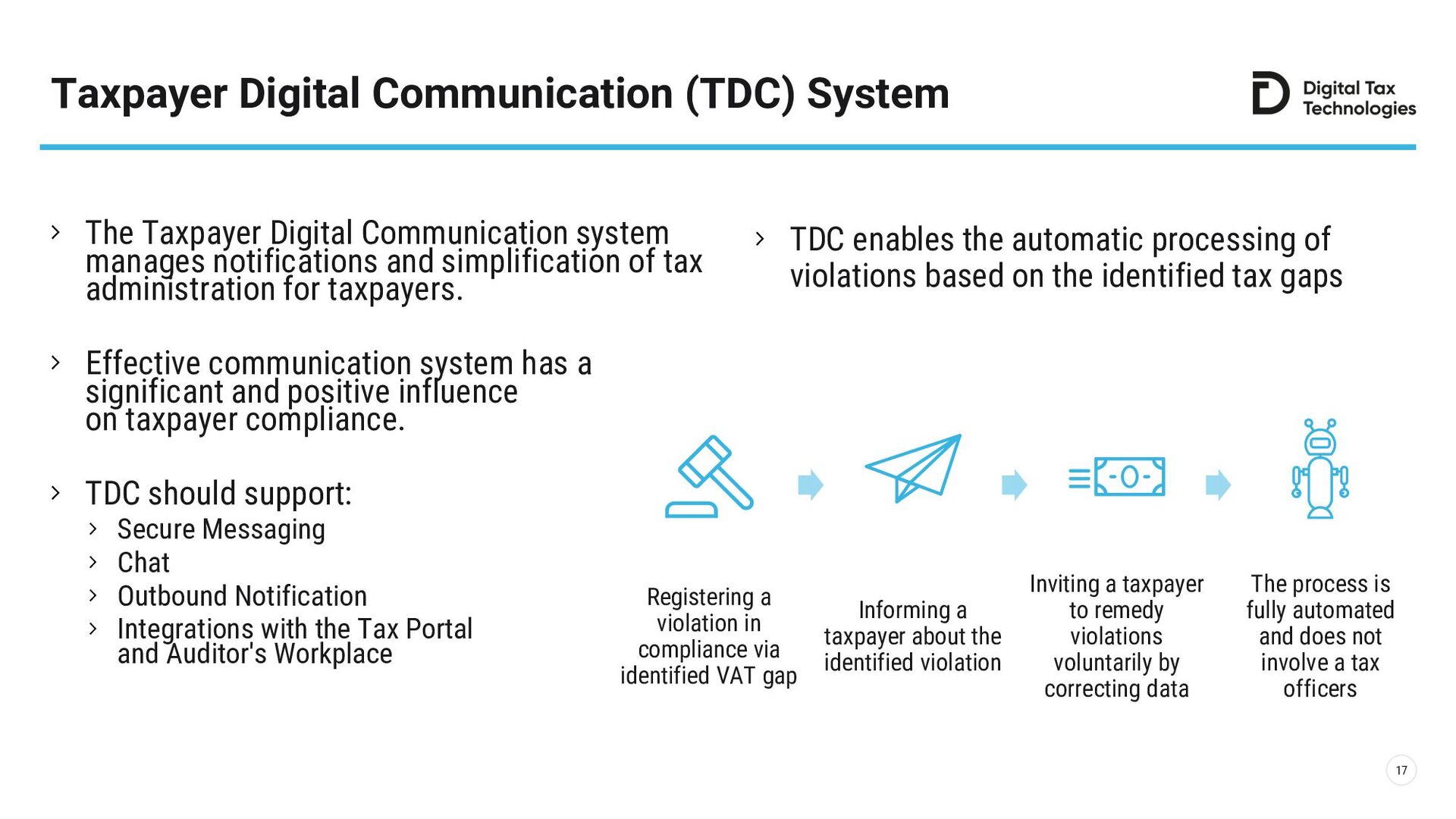

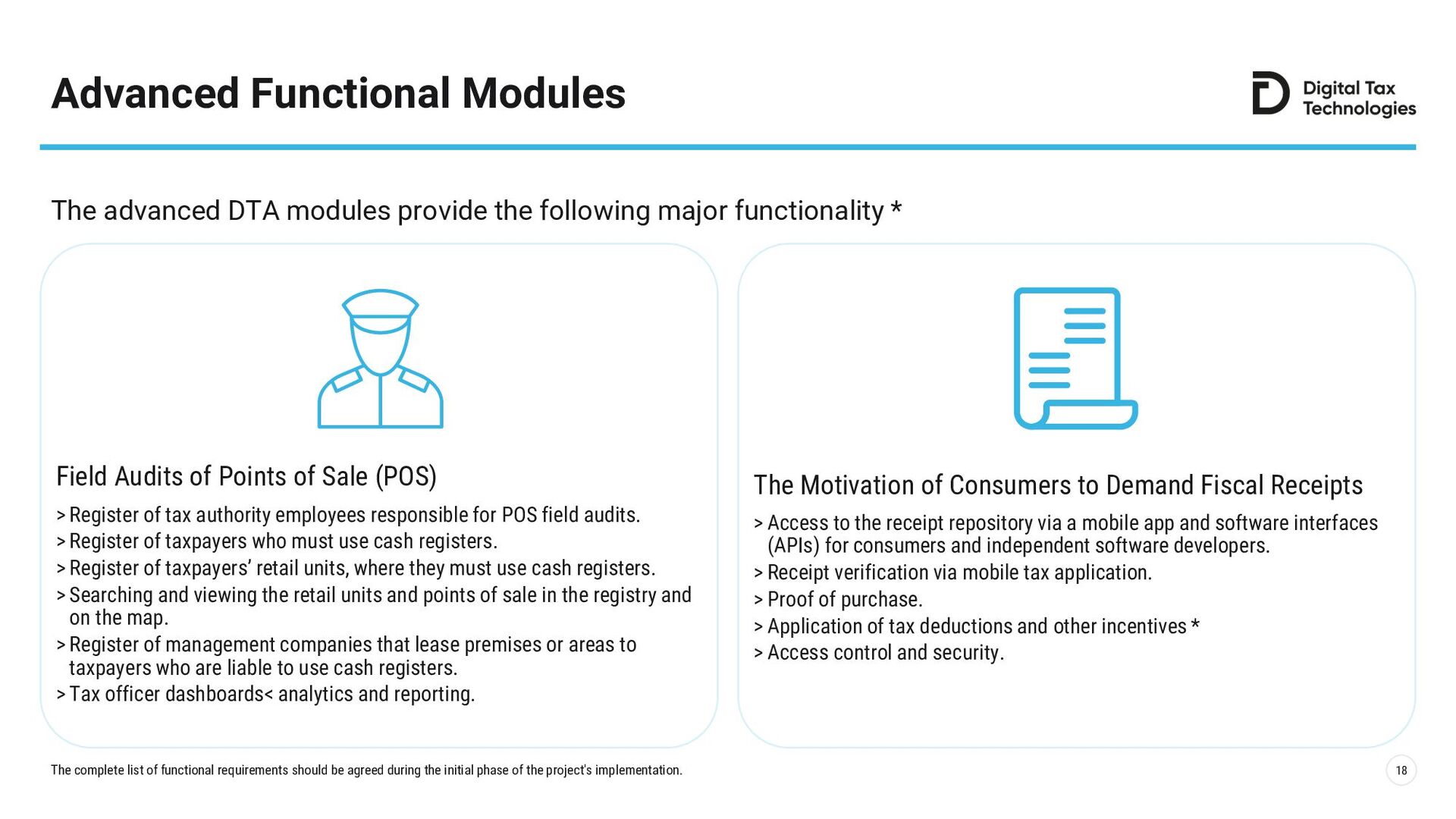

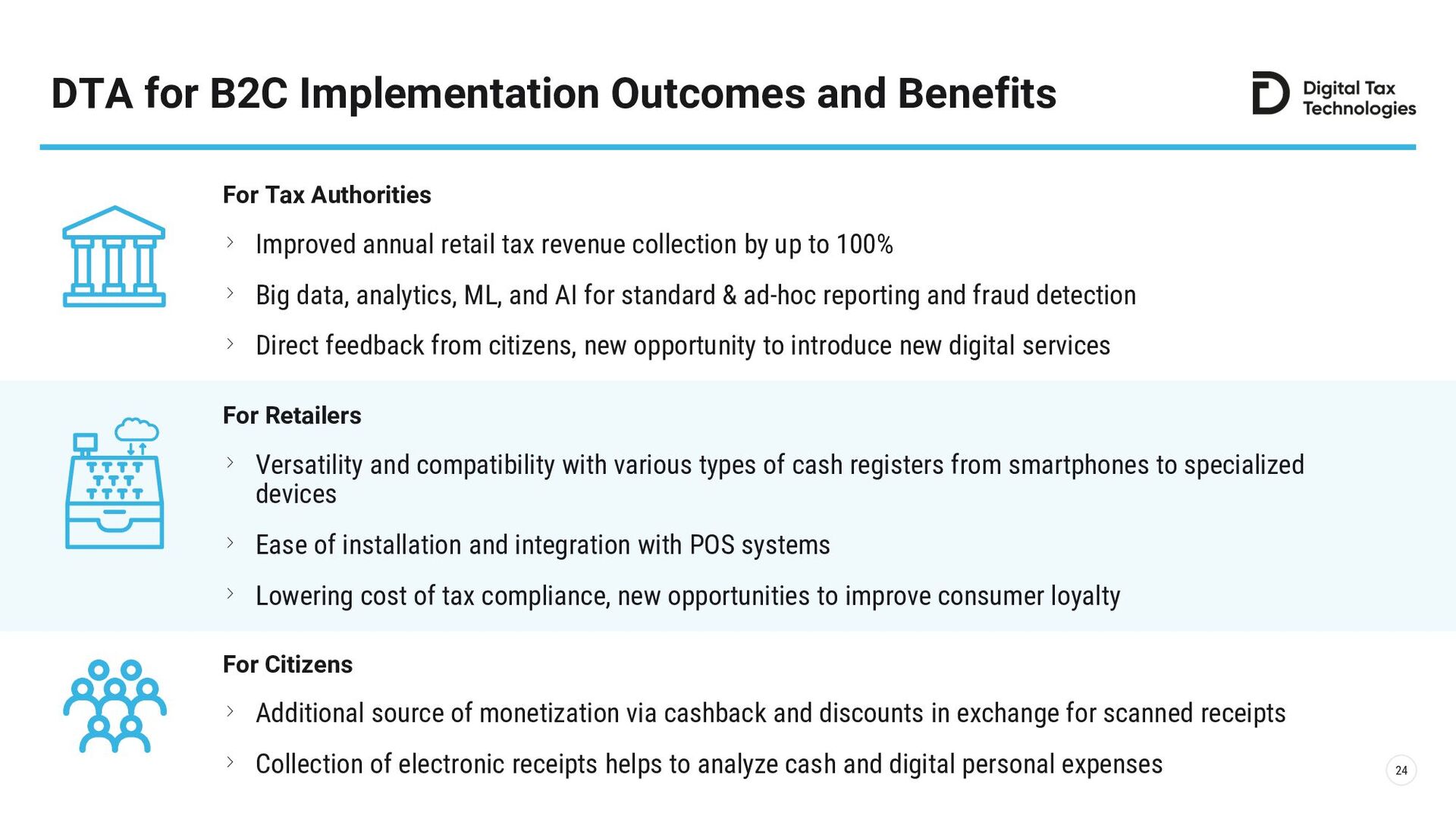

Digital tax administration of B2C taxpayers ensures completeness of revenue account-ing and taxation of retailers through real-time collection of fiscal receipts.

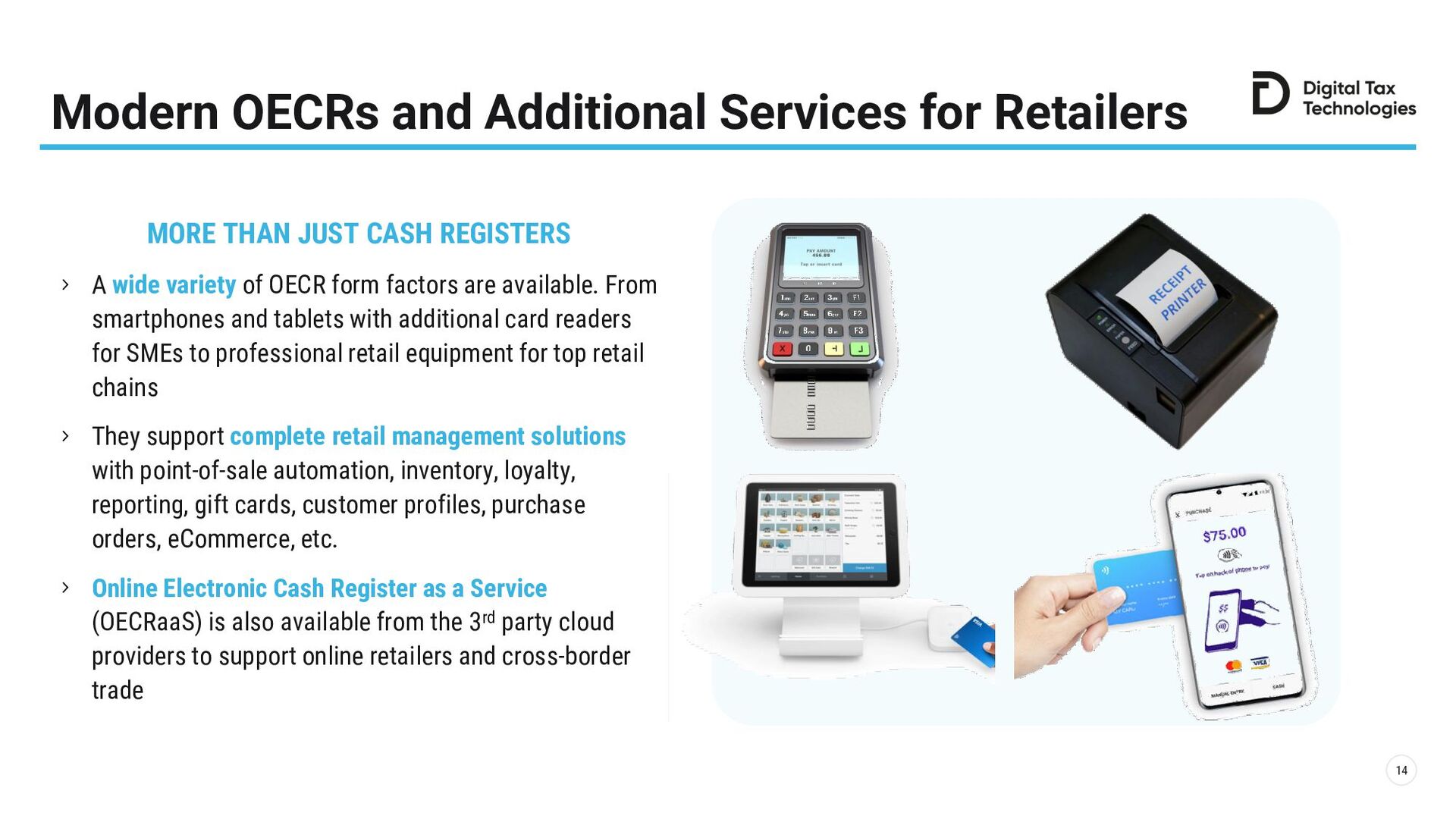

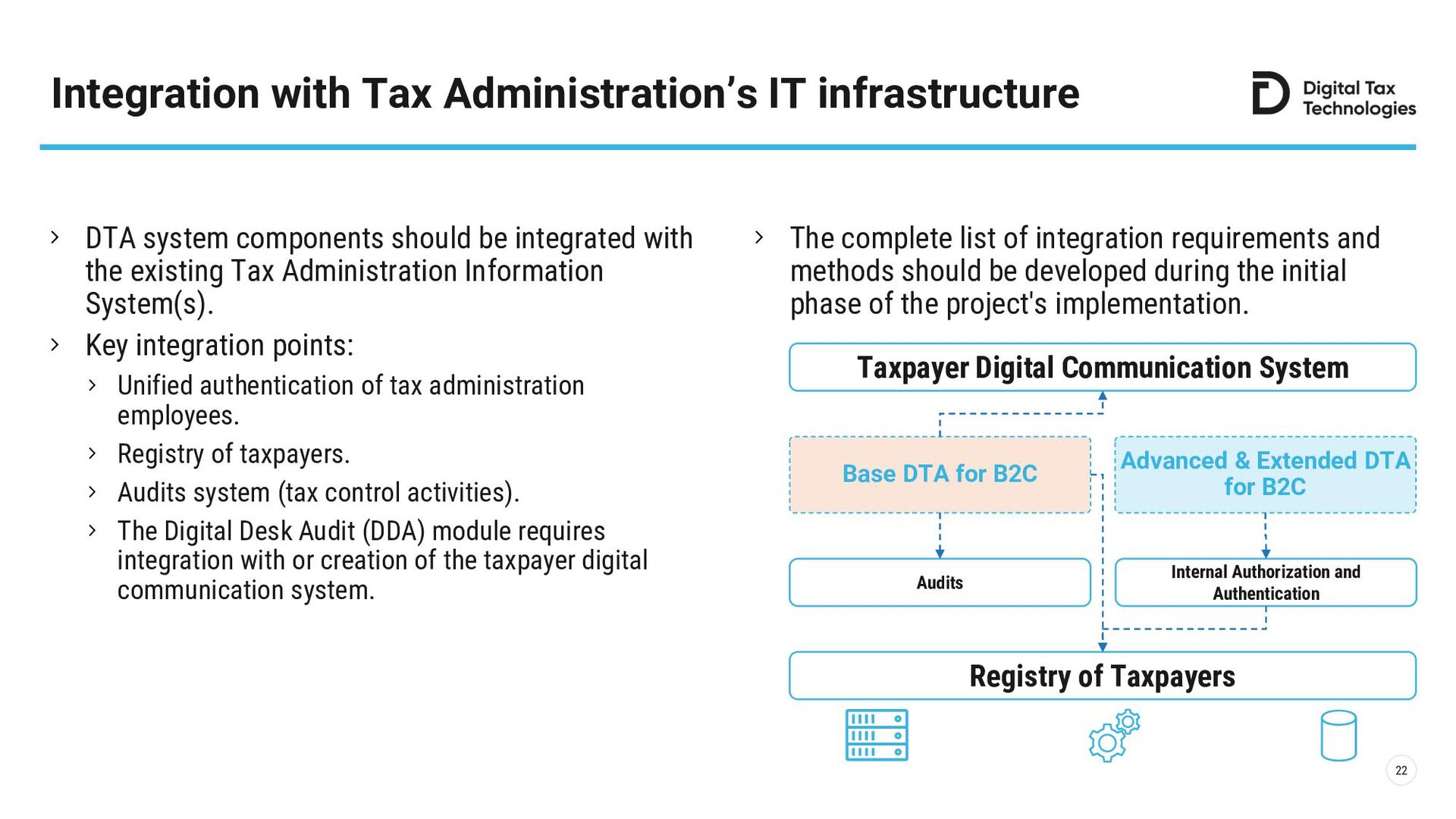

→ Supports hardware and software online electronic cash registers (OECRs).

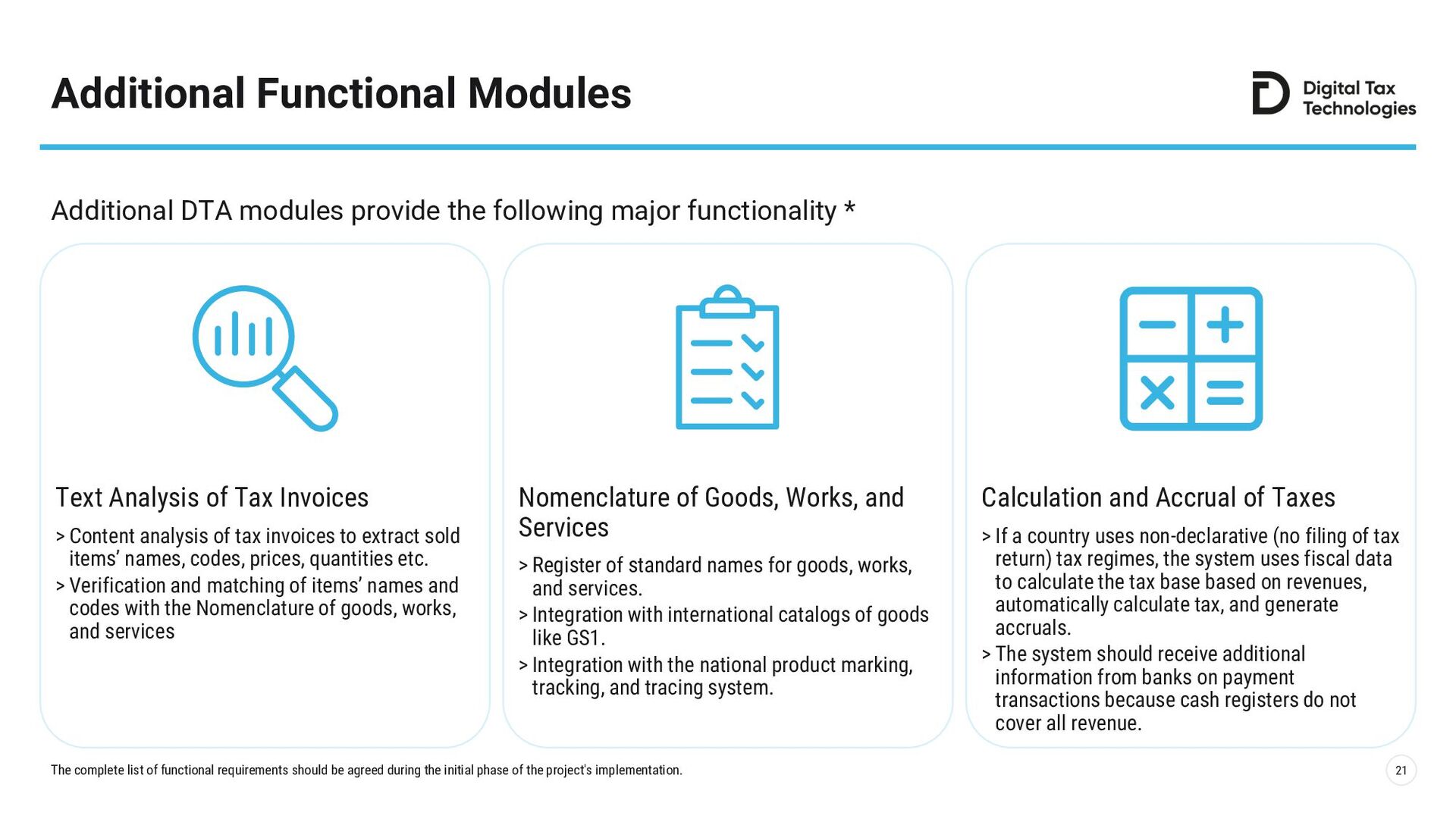

→ Fiscalization of mortar & bricks and e-commerce retailers, real-time collection of fis-cal receipts, taxable revenue, and tax payable calculation.

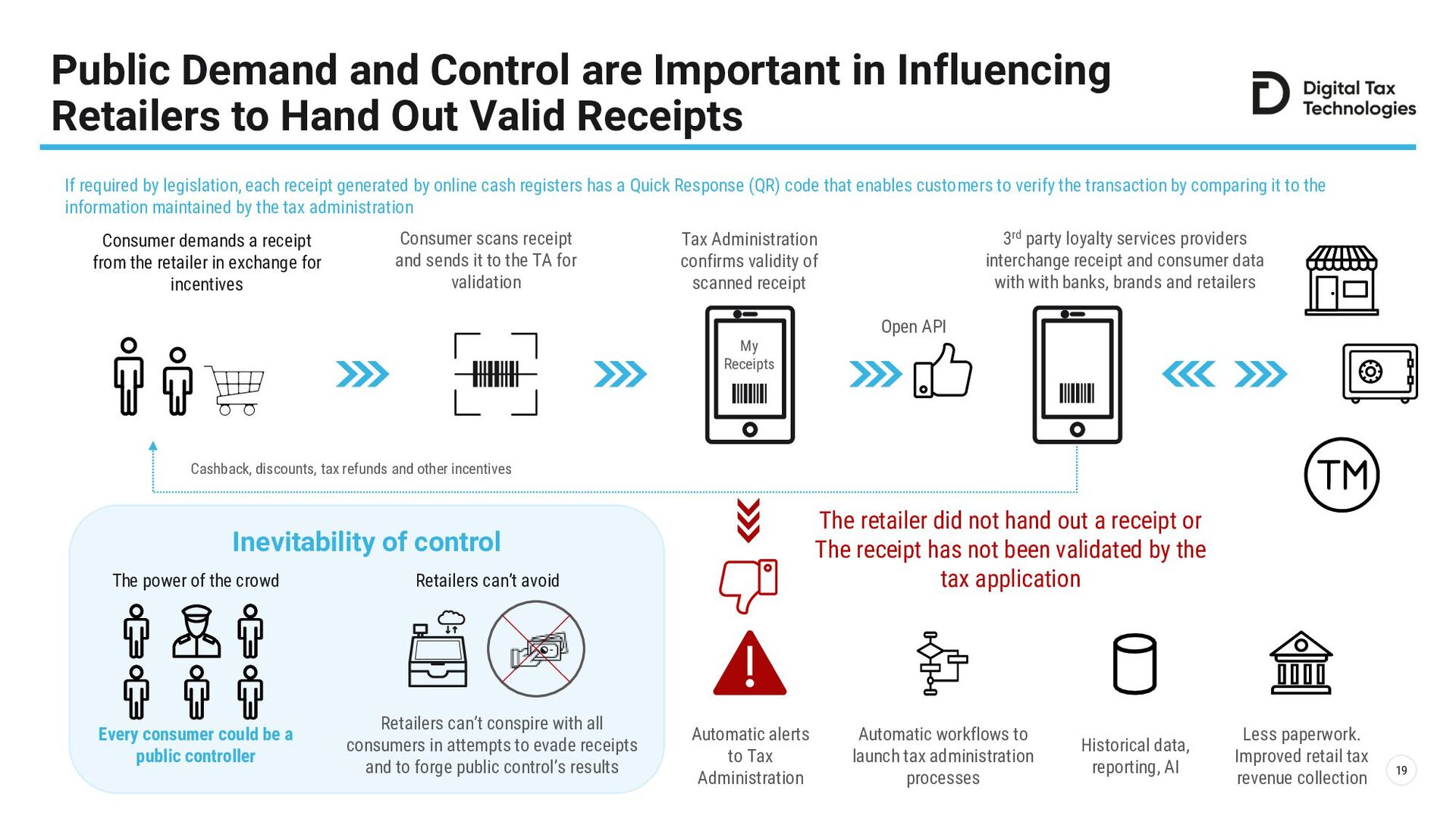

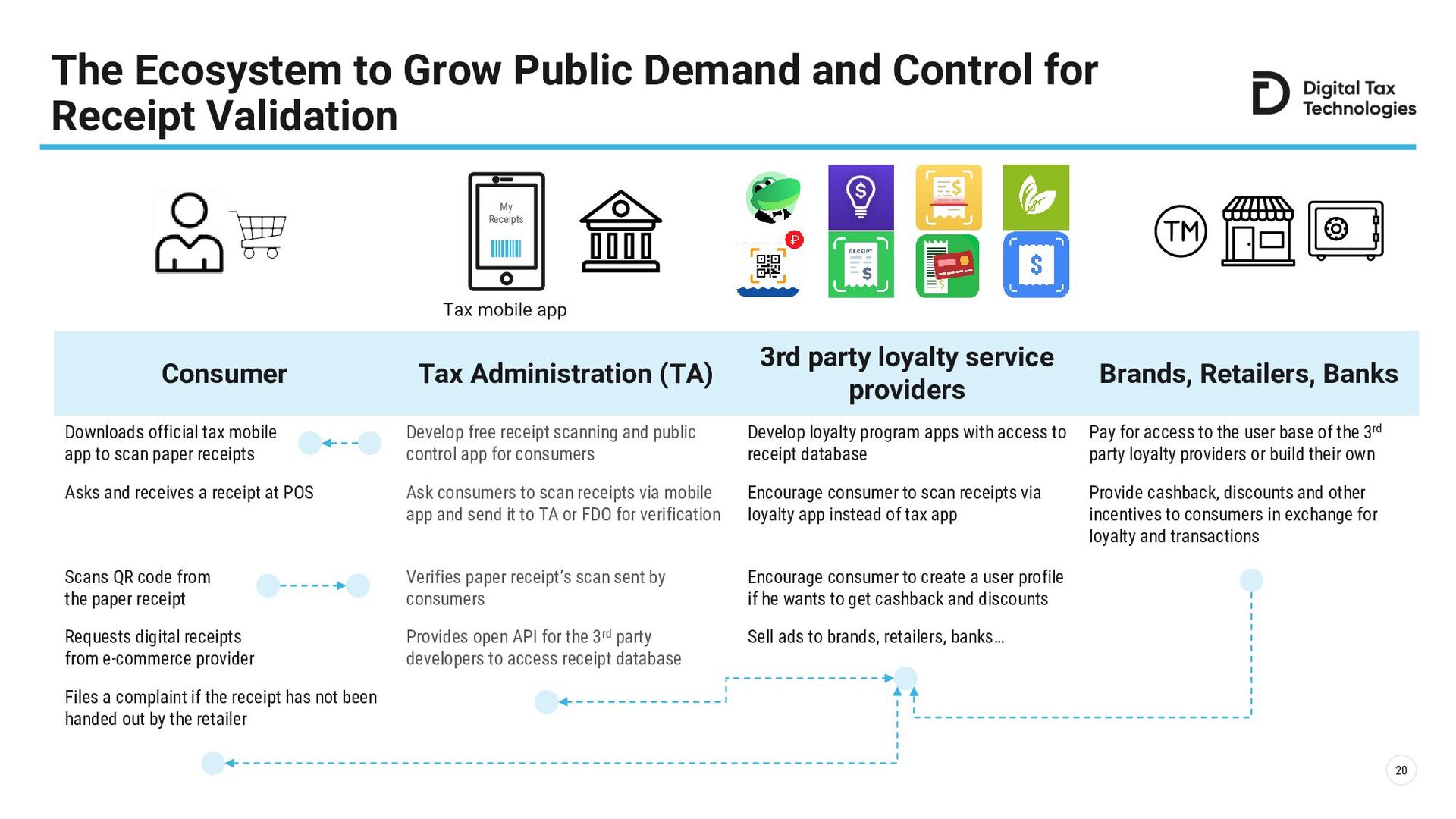

→ Consumer motivation to demand receipts and the field work of tax officers to control retail point of sales.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[*] The complete list of functional requirements should be created](https://files.speakerdeck.com/presentations/38bc6769ba1e4ebfa2eabb935e135f3b/slide_11.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}