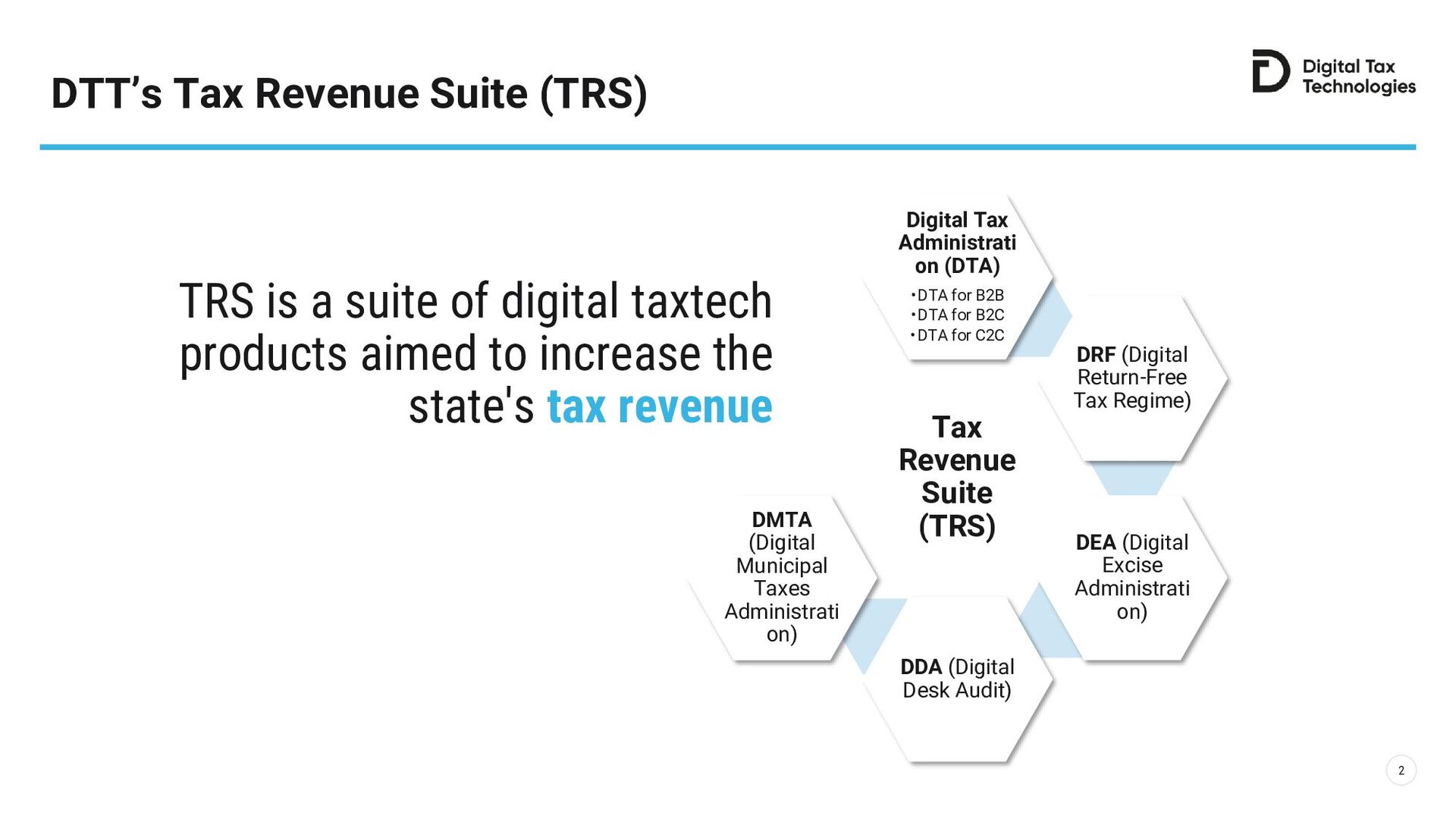

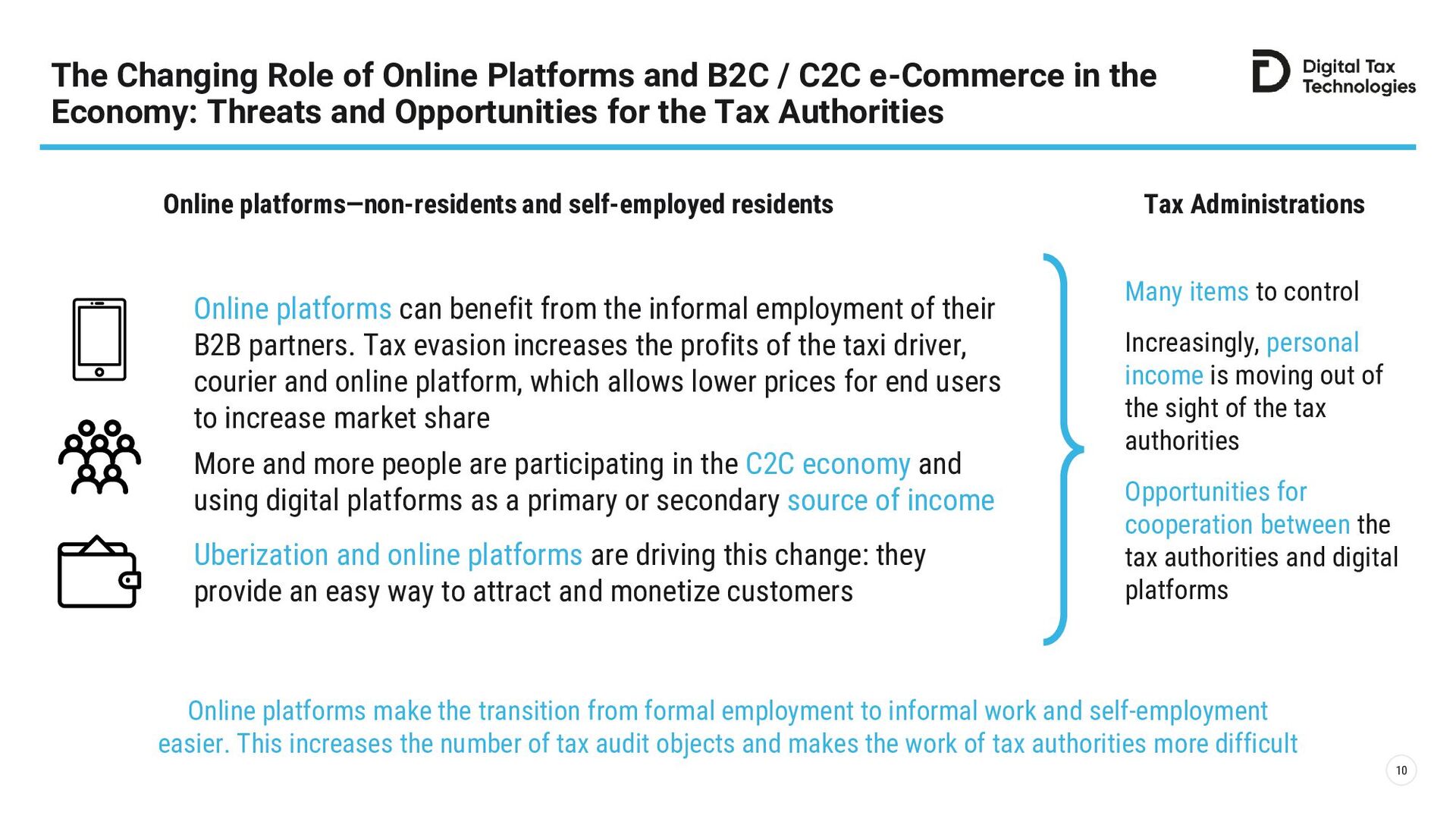

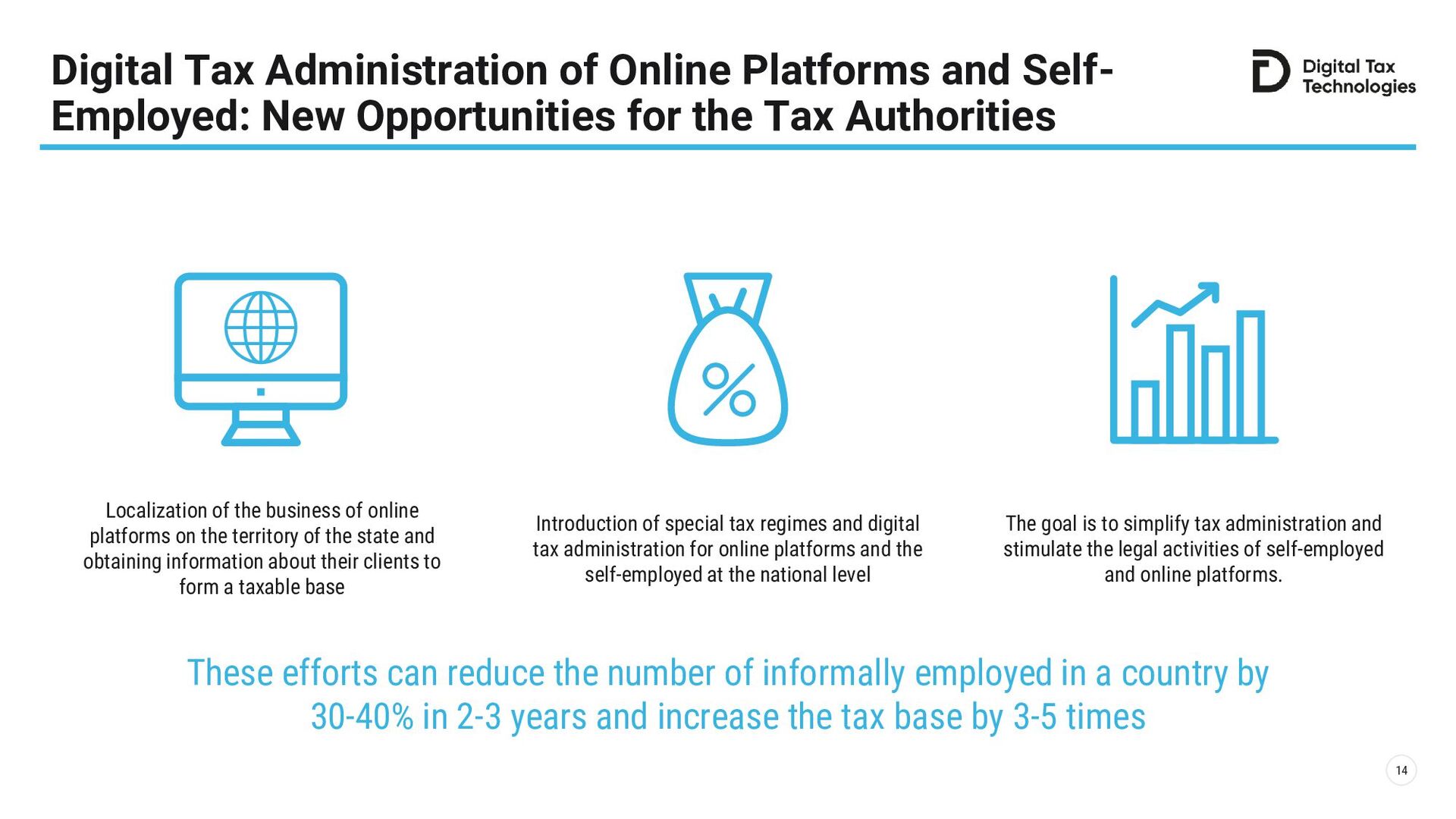

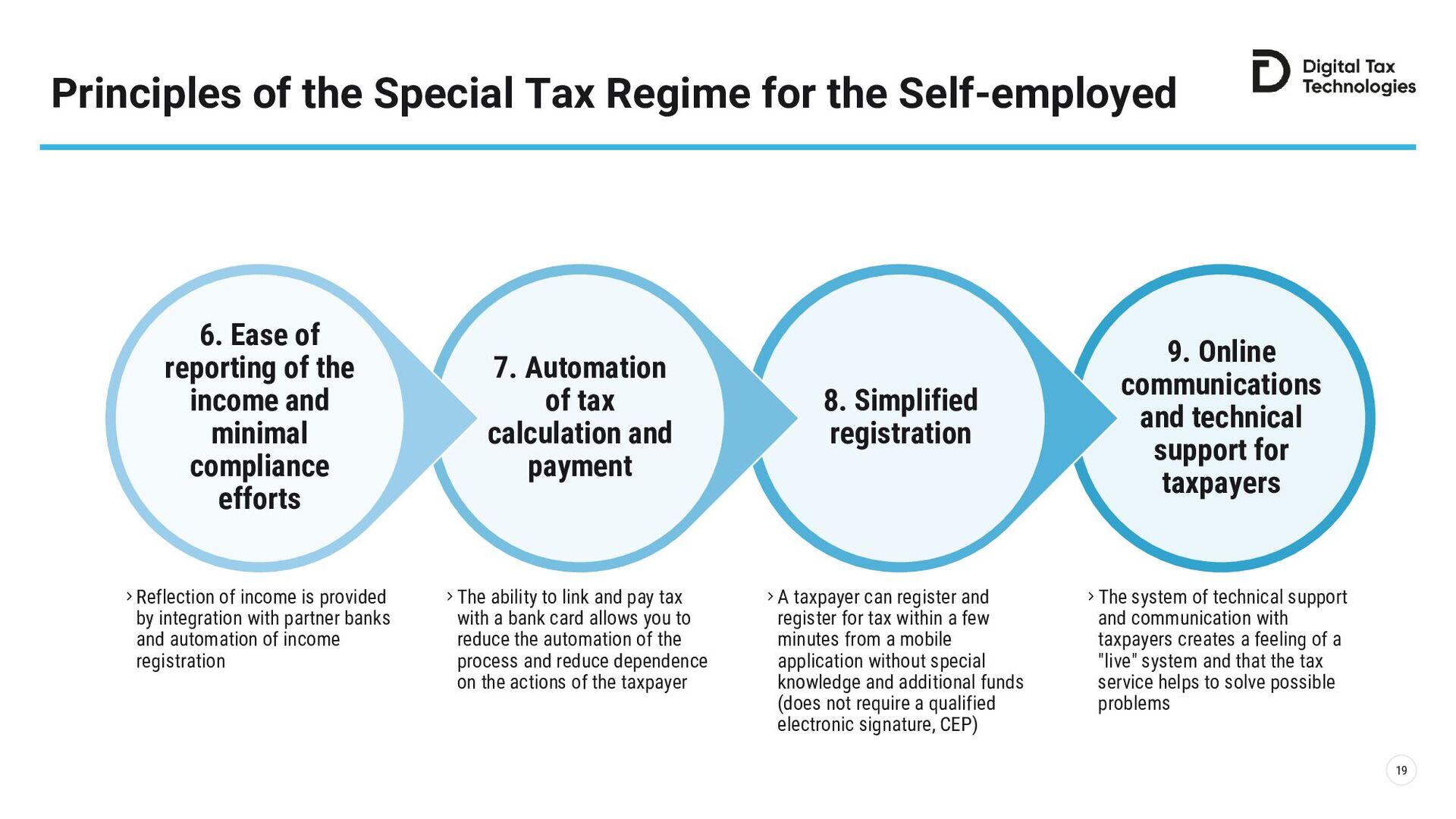

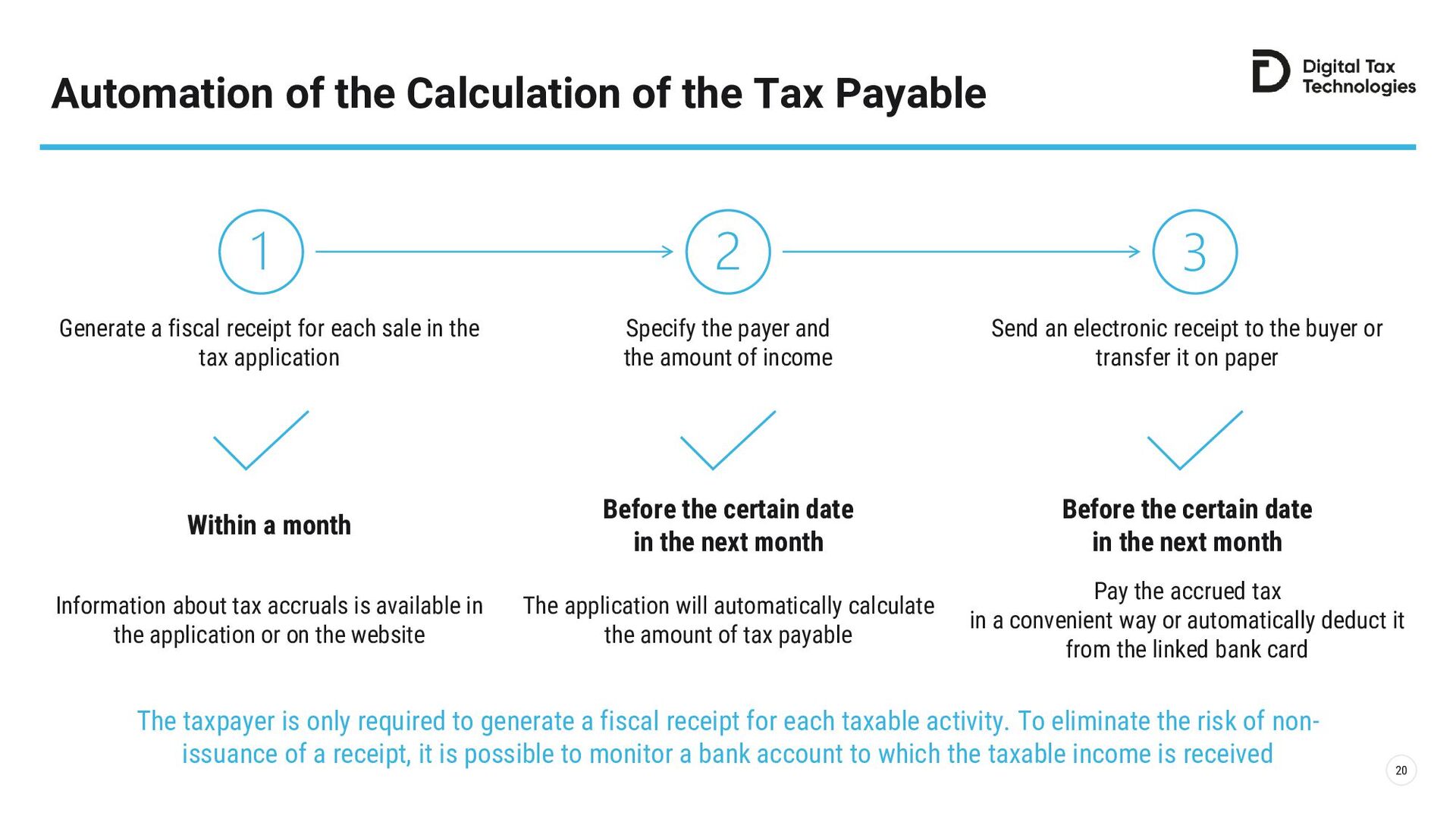

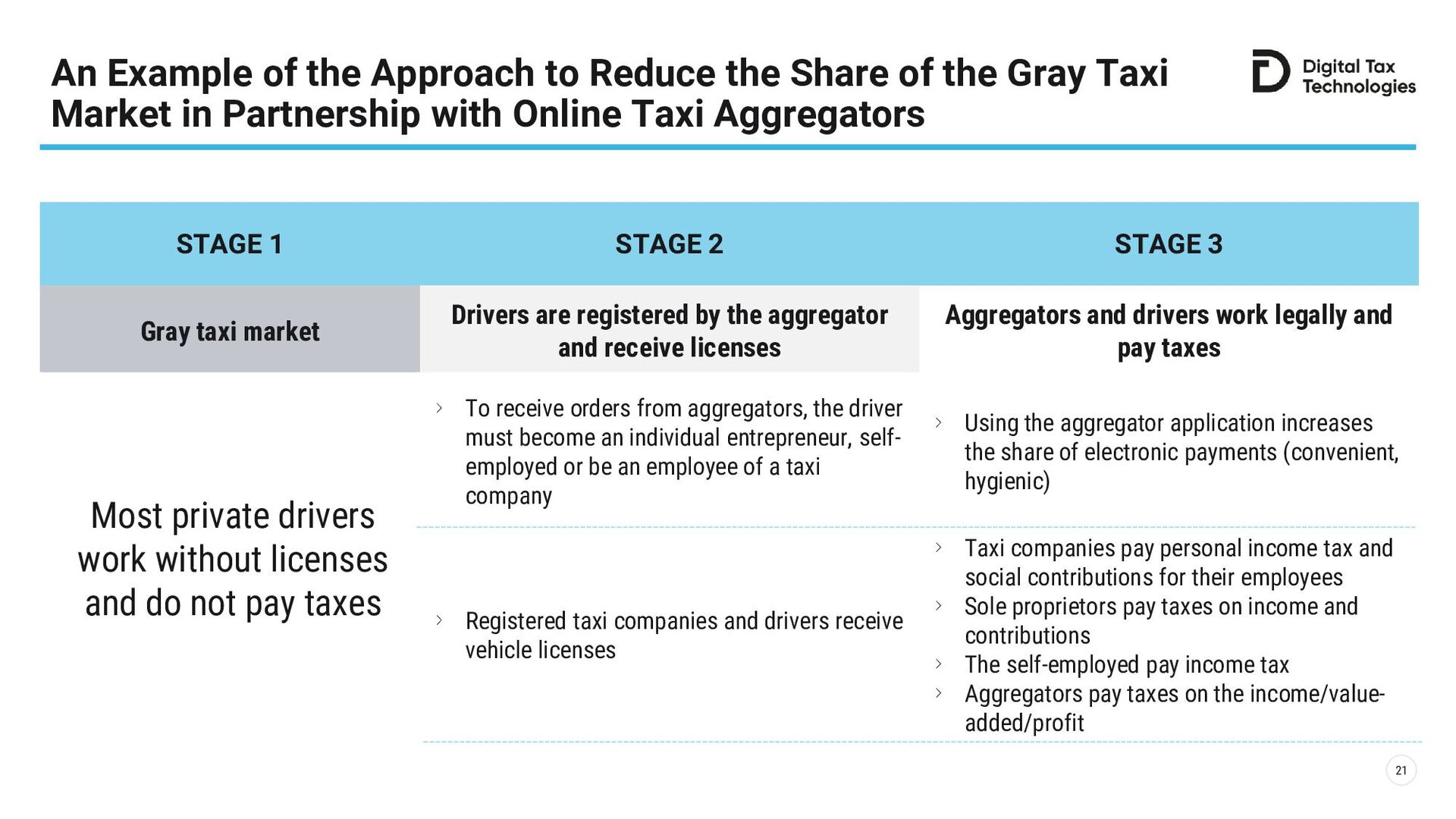

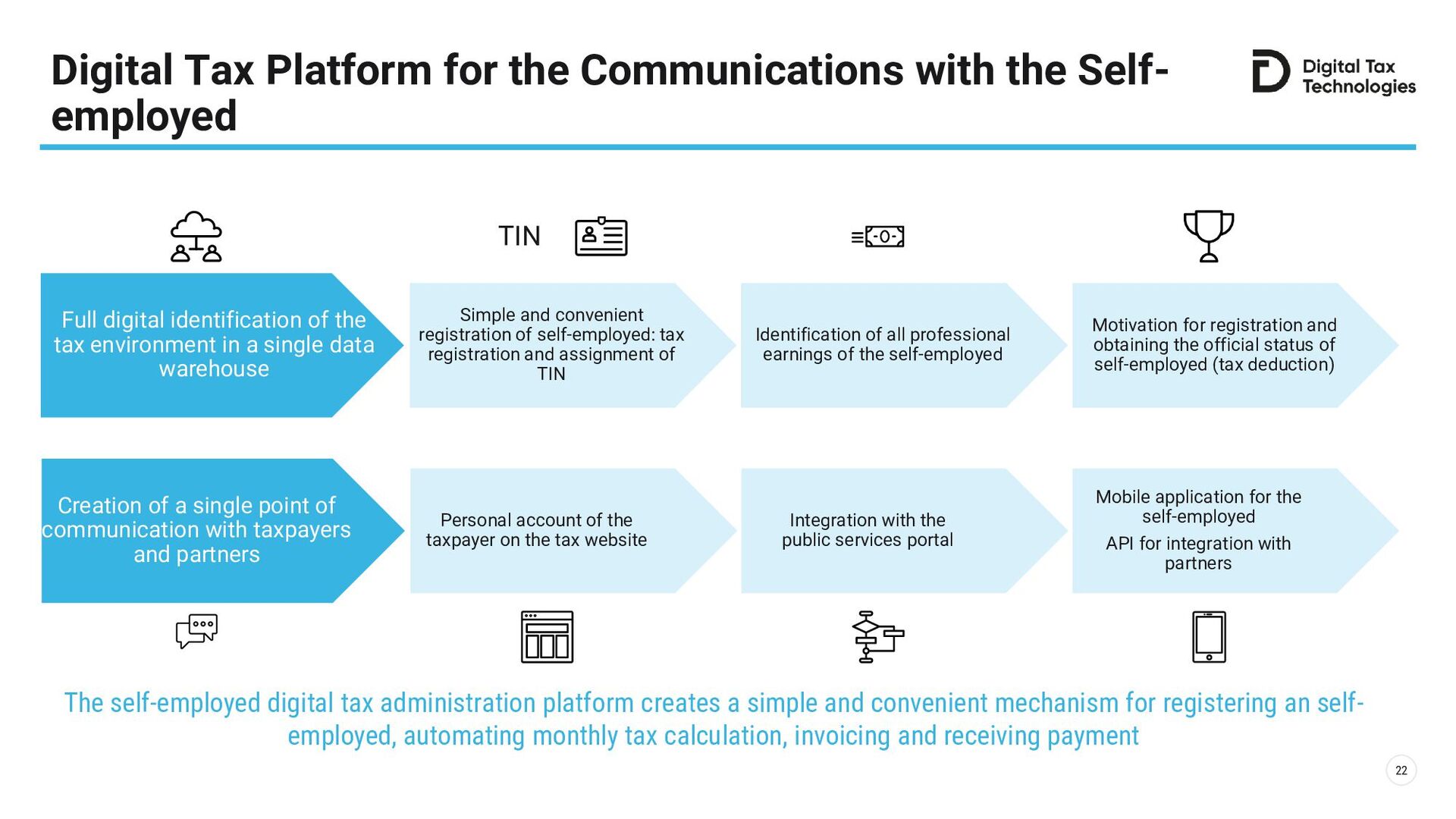

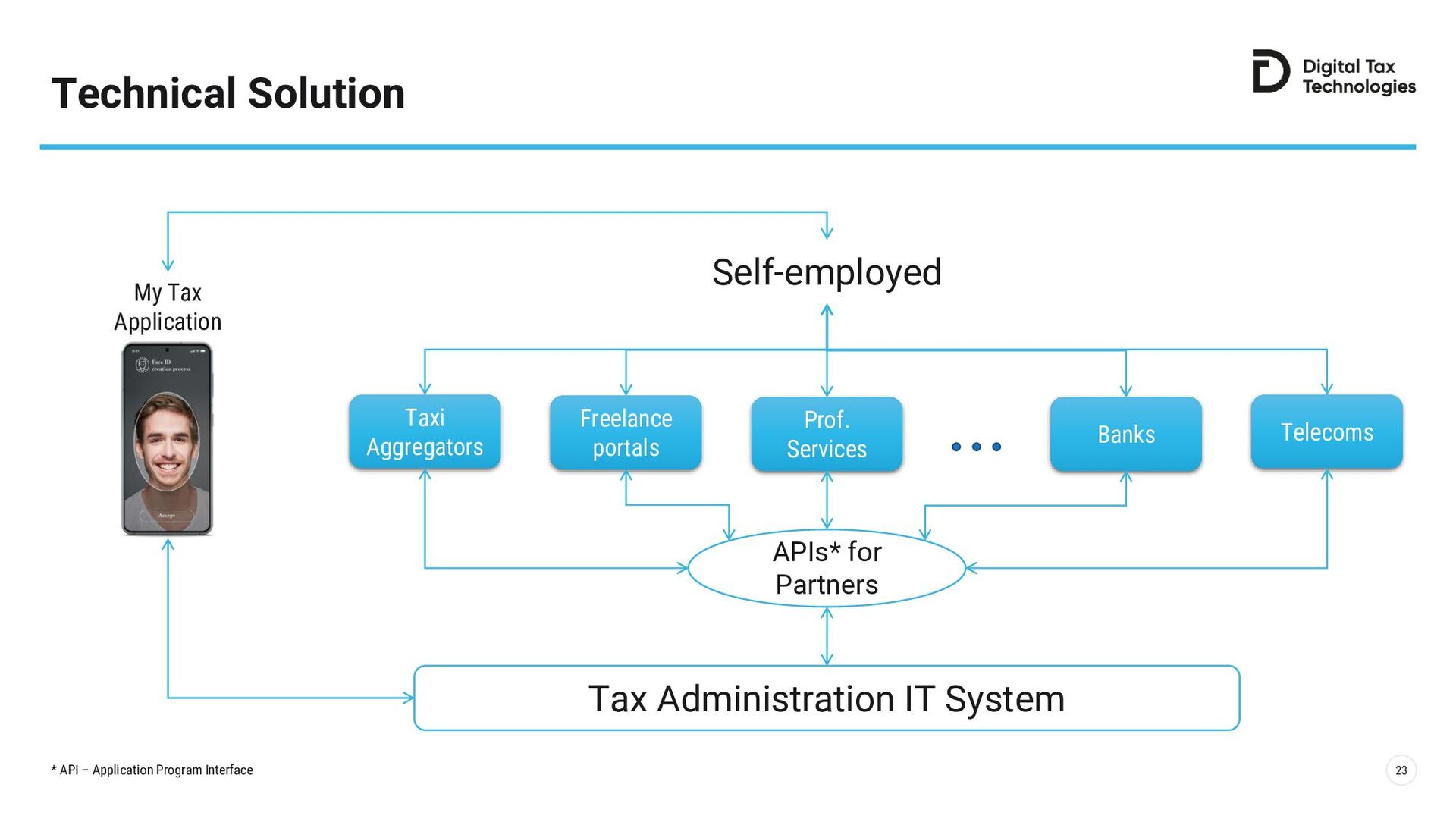

Digital tax administration of C2C taxpayers applies revenue accounting and taxation for direct sales between consumers and through online platforms.

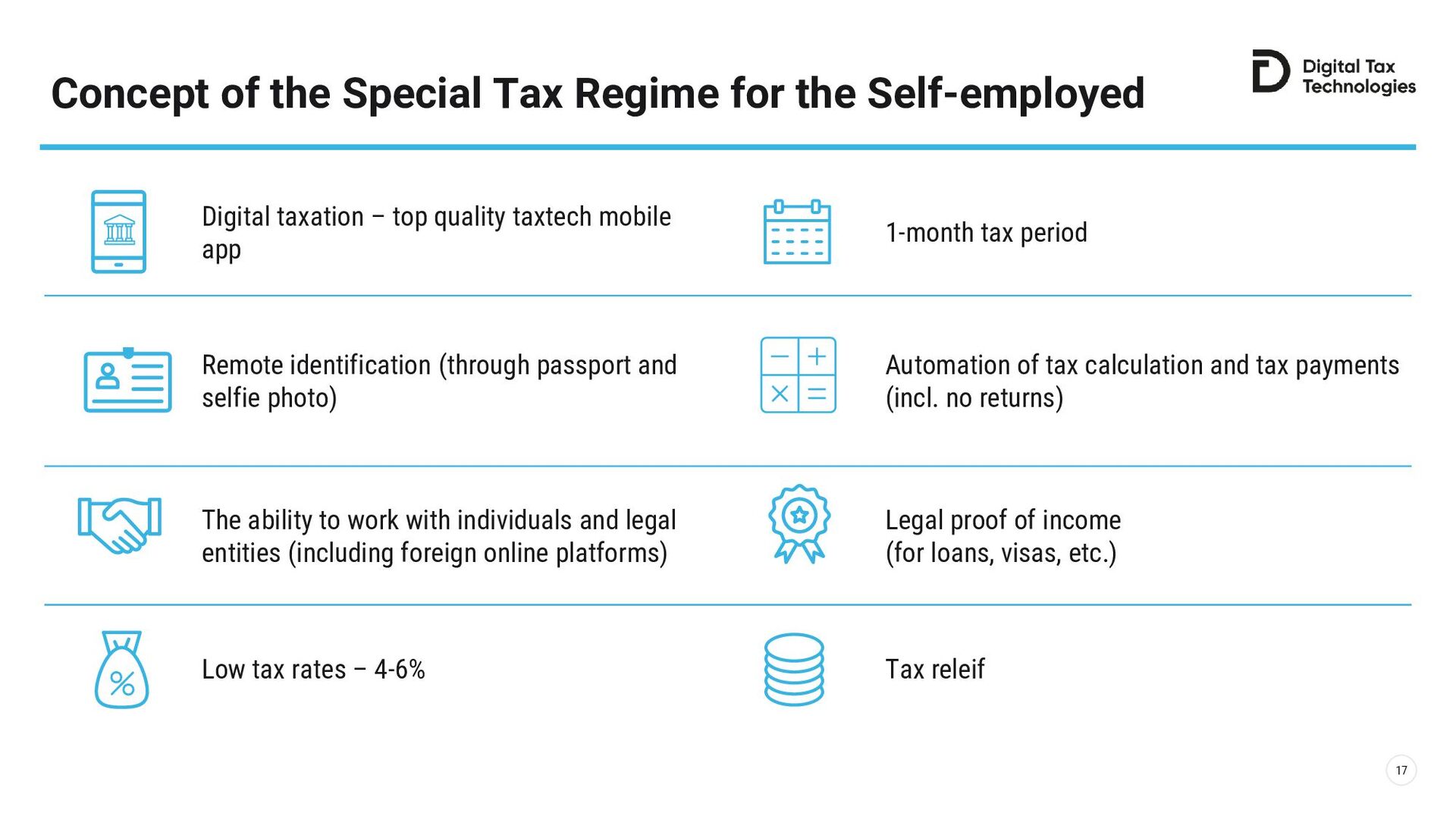

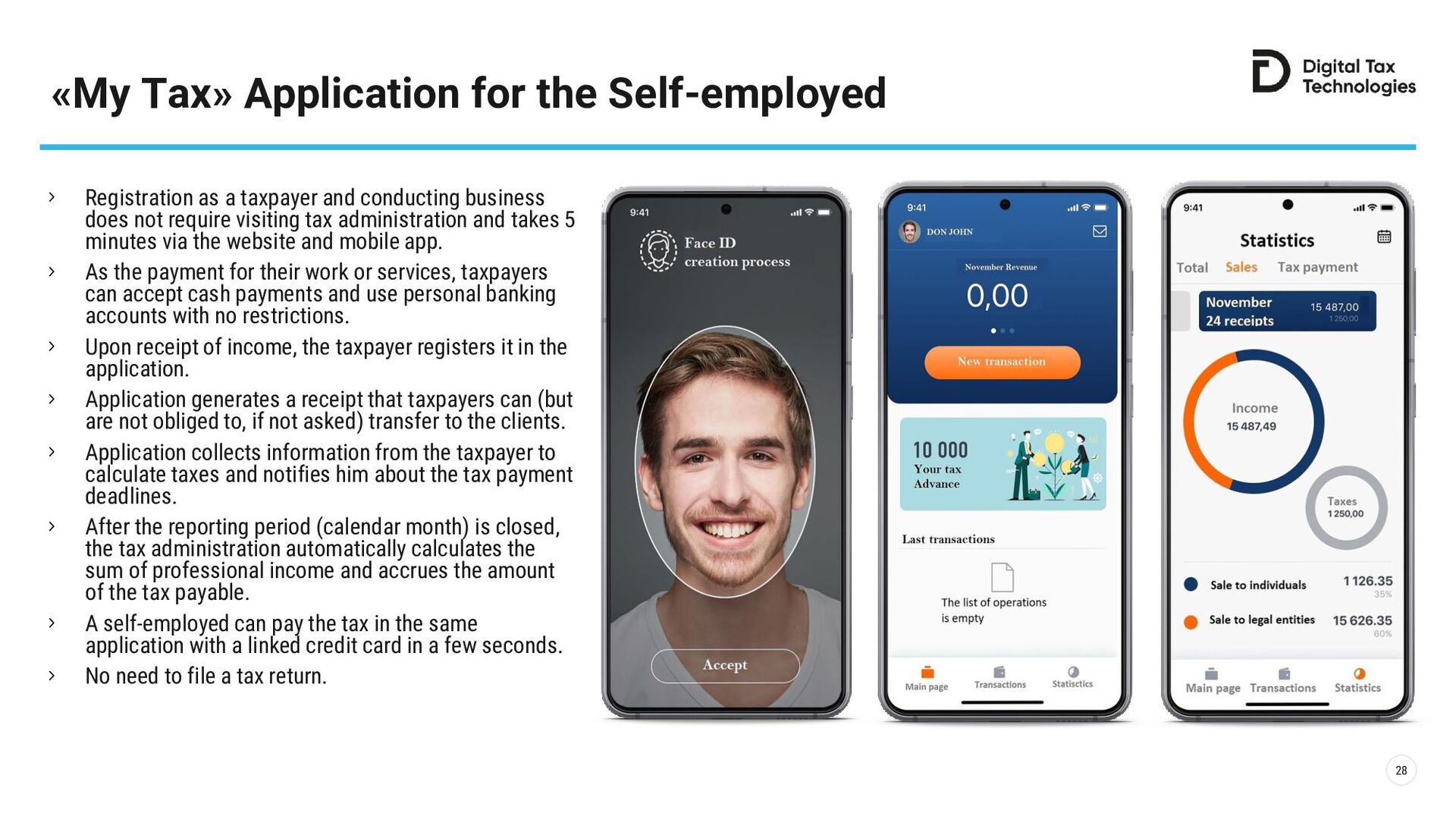

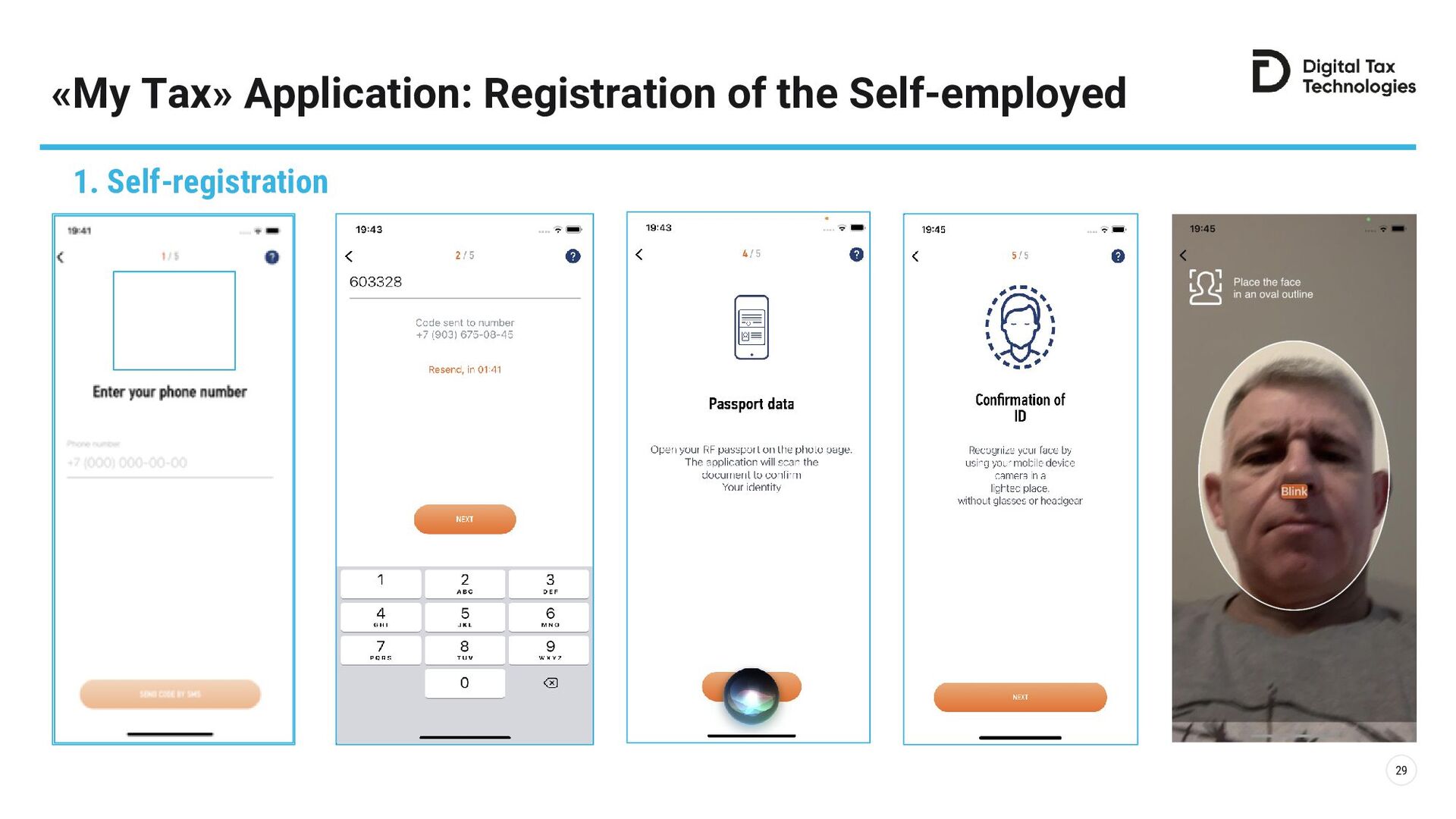

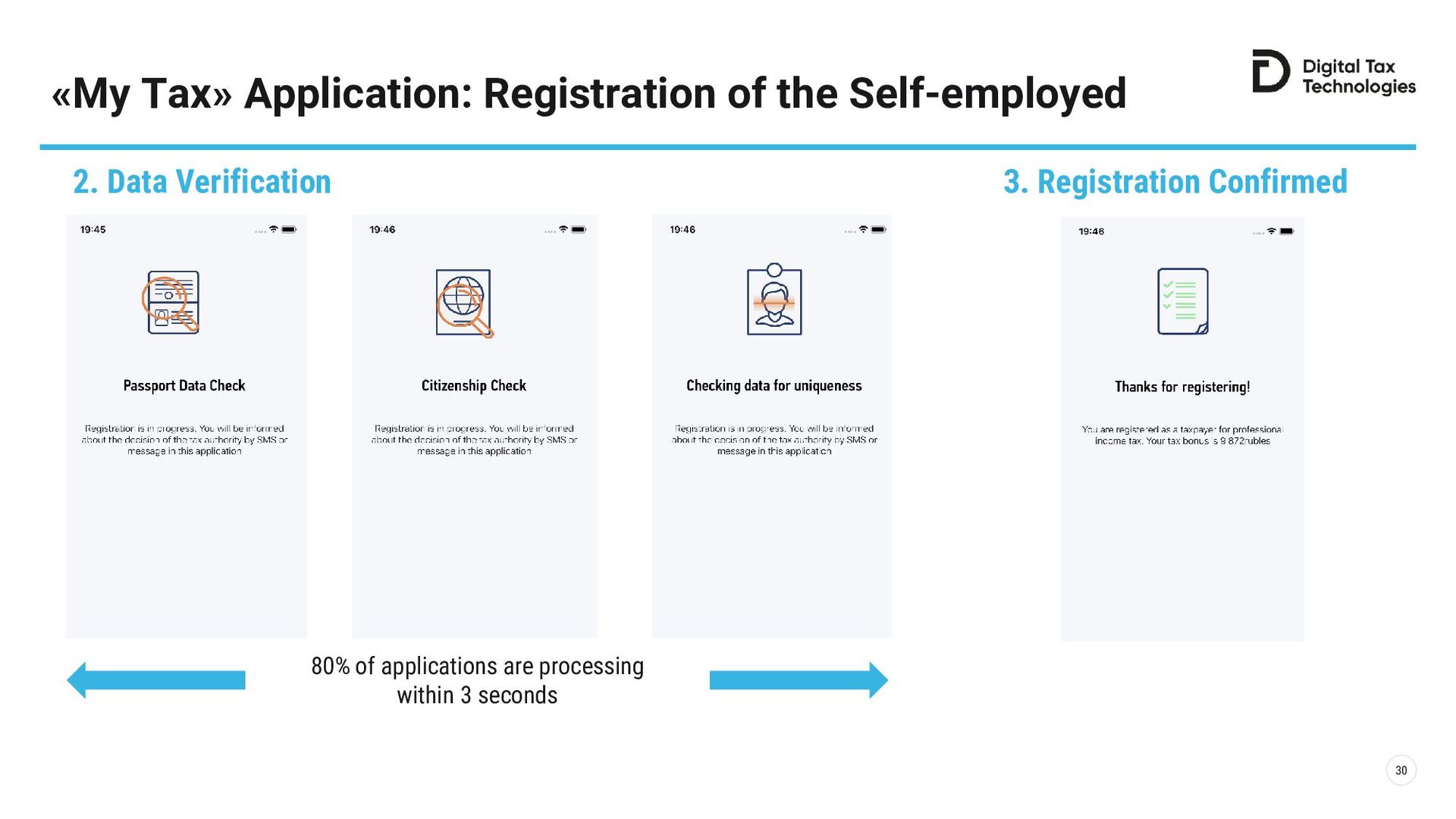

→ Mobile app for the remote online registration of self-employed without visiting tax administration offices.

→ Integration with online platforms and banks; income, tax base and tax payable calculation.

→ Automatic mobile payment of taxes.

{kind=link}

{kind=link}

{kind=link}

![[1] International Labour Organization (ILO). Resolution I. Resolution concerning statistics](https://files.speakerdeck.com/presentations/0359fab98c3143ff93a351a6708a8386/slide_3.jpg){kind=link}

![[1] International Labour Organization ( ILO ). SMALL MATTERS. Global](https://files.speakerdeck.com/presentations/0359fab98c3143ff93a351a6708a8386/slide_4.jpg){kind=link}

![[1] As a share of the working population. Statista, International](https://files.speakerdeck.com/presentations/0359fab98c3143ff93a351a6708a8386/slide_5.jpg){kind=link}

{kind=link}

{kind=link}

![[1] C2C stand for “Consumer 2 Consumer” - doing business](https://files.speakerdeck.com/presentations/0359fab98c3143ff93a351a6708a8386/slide_8.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}