Talk Summary:

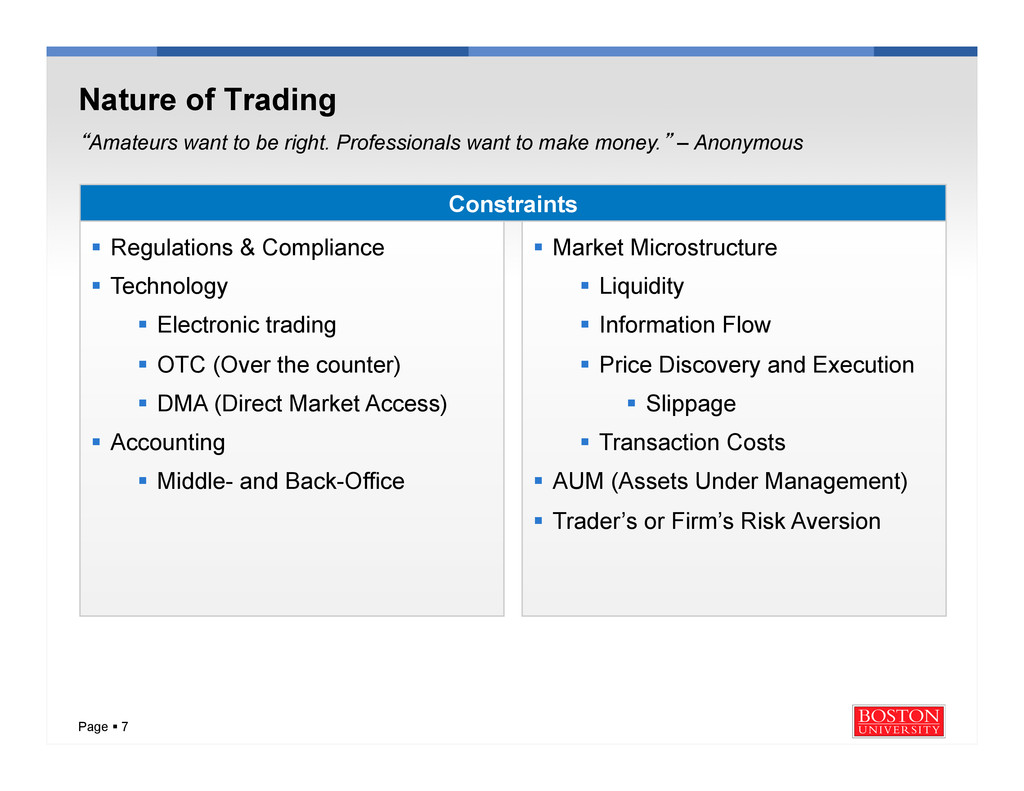

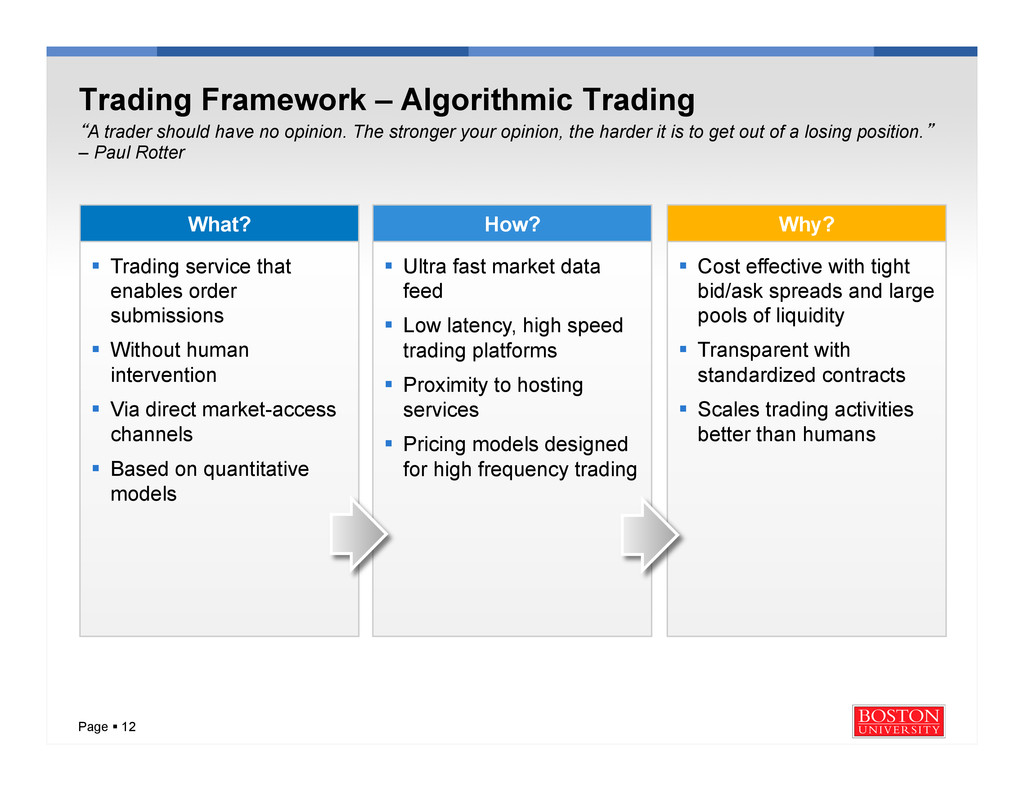

In an increasing era of electronic trading, algorithmic trading is responsible for an ever greater share of market trading. This talk will present introductory information required for traders, quants, and risk managers to understand the fundamental framework required for successful algorithmic trading. The fields of market microstructure (order book, market impact, liquidity, price discovery), high performance computing, and the evolution of trading styles will also be discussed. Finally, the computational skills and hardware frameworks needed for implementation will be presented.

Bio:

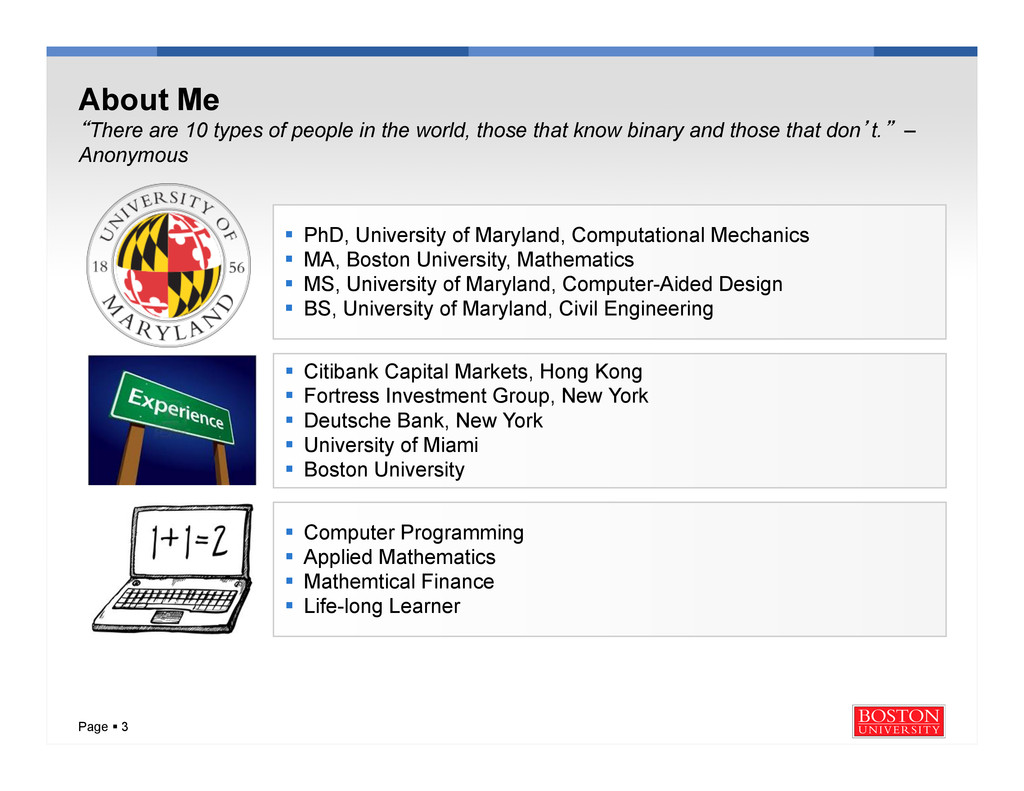

Ahmad Namini is the Executive Director and Adjunct Professor of Boston University’s Mathematical Finance Program. Dr. Namini has served as a quantitative analyst/developer, desk strategist, and analytics head for a hedge fund (Fortress Investment Group) and investment banks (Deutsche Bank and Citigroup Capital Markets). He is an experienced builder, manager, and teacher of trading modes and applications, with models spanning the credit derivative, rates, and equity markets. He built Deutsche Bank’s first fixed income algorithmic trading platform. He currently teaches the course “Quantitative Strategies and Algorithmic Trading” at Boston University which has been featured in the Wall Street Journal. He also teaches a course entitled “C++ for Mathematical Finance, ” and is involved in research and publication in the mathematical finance field. Dr. Namini earned a PhD in computational mechanics from the University of Maryland and then served as a faculty member at the University of Miami for ten years where he developed a research program in computational aerodynamics and parallel computing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}