Presented at the QuantLib User Meeting 2015 in Düsseldorf

http://ssrn.com/abstract=2696743

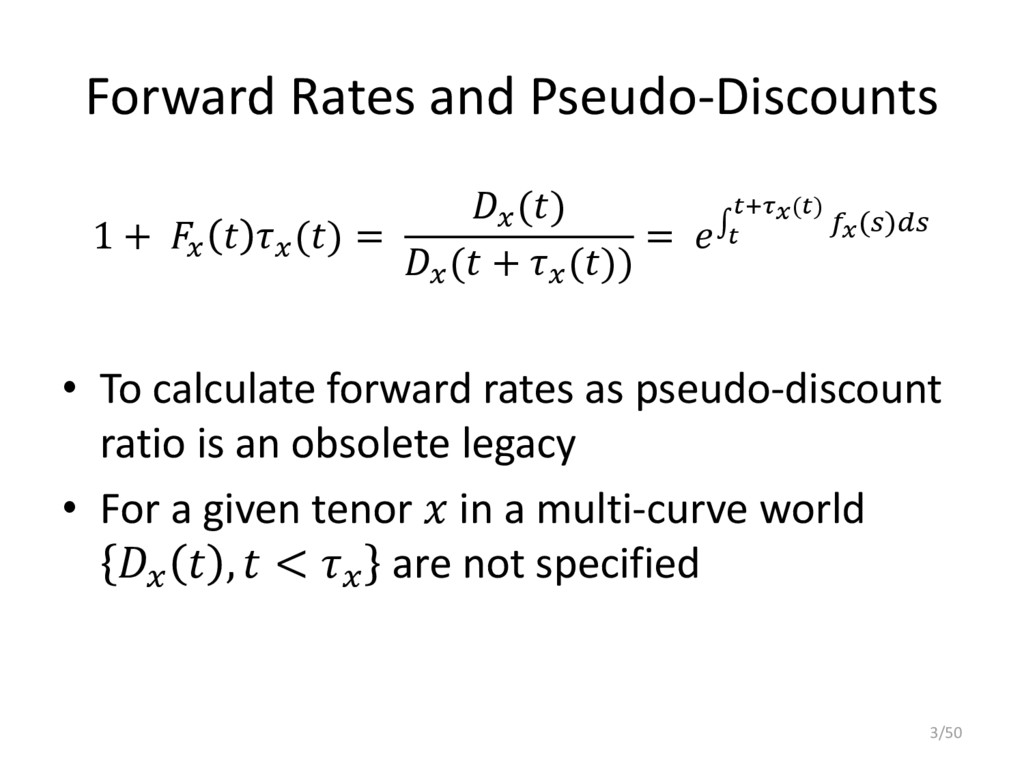

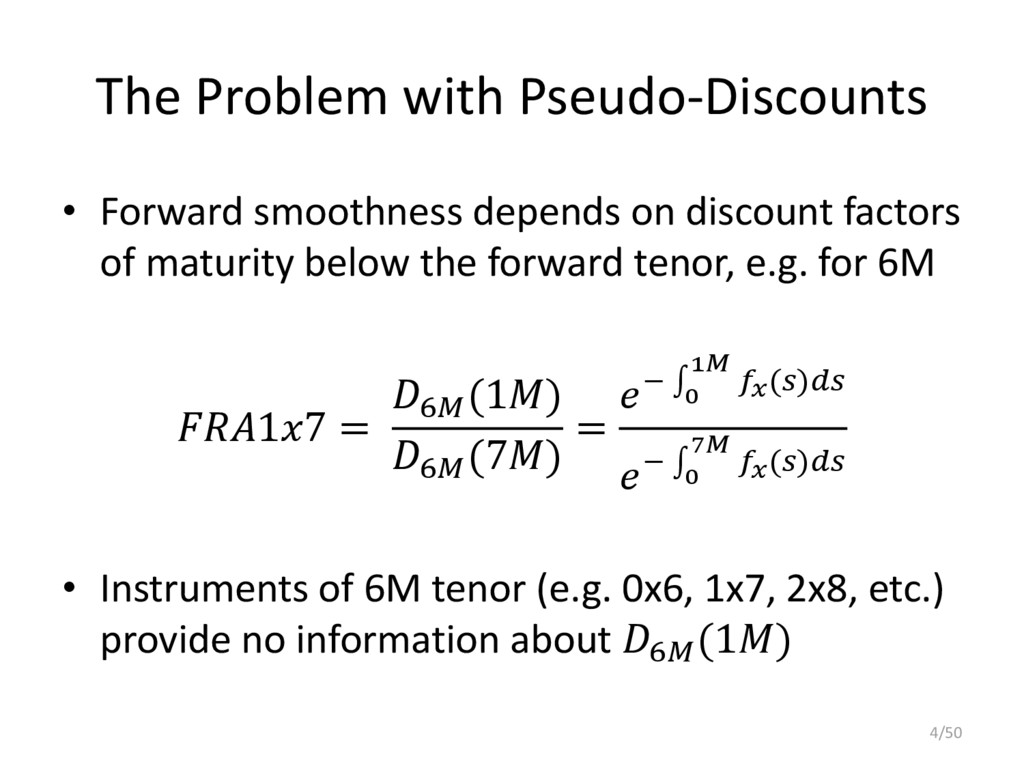

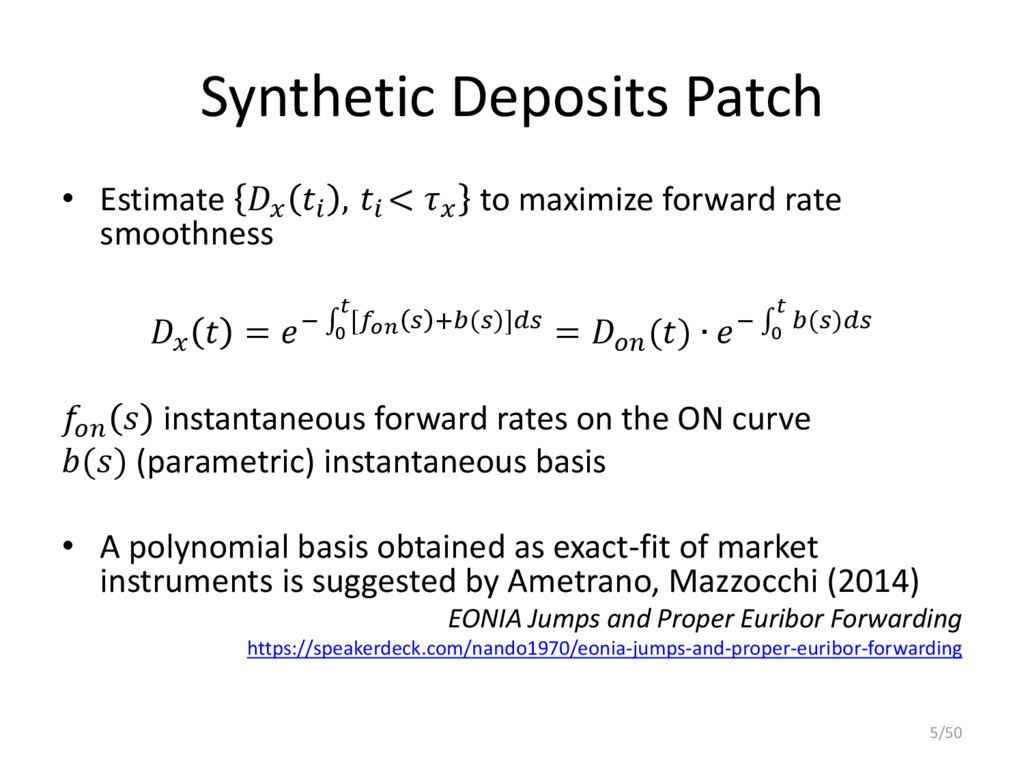

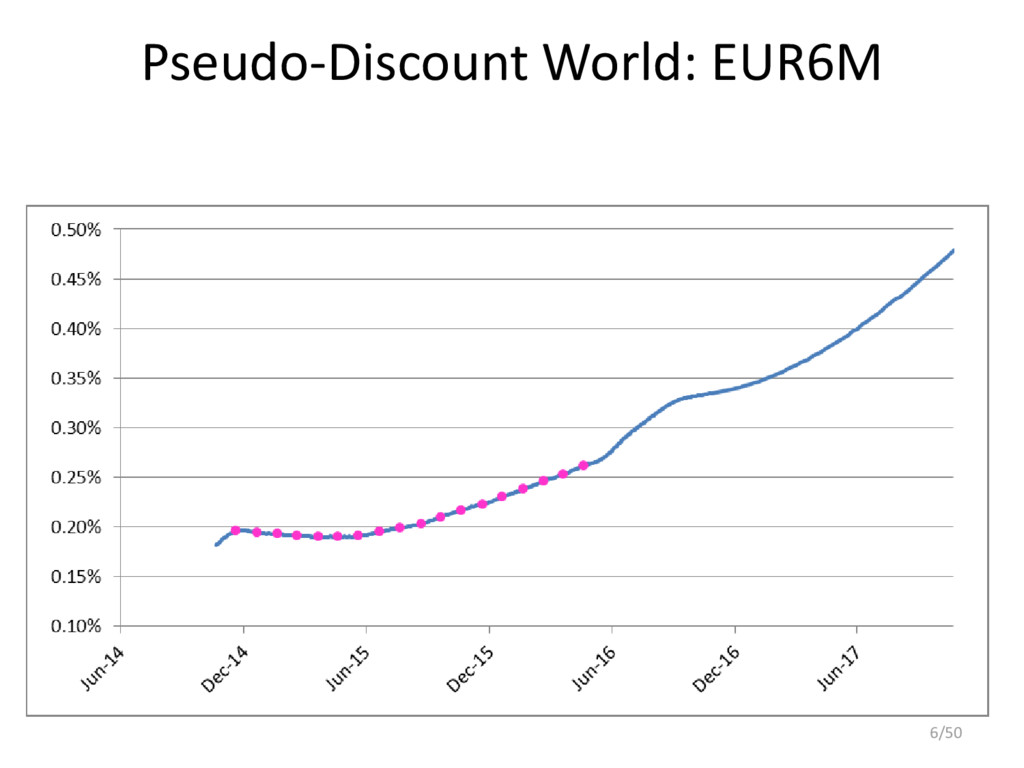

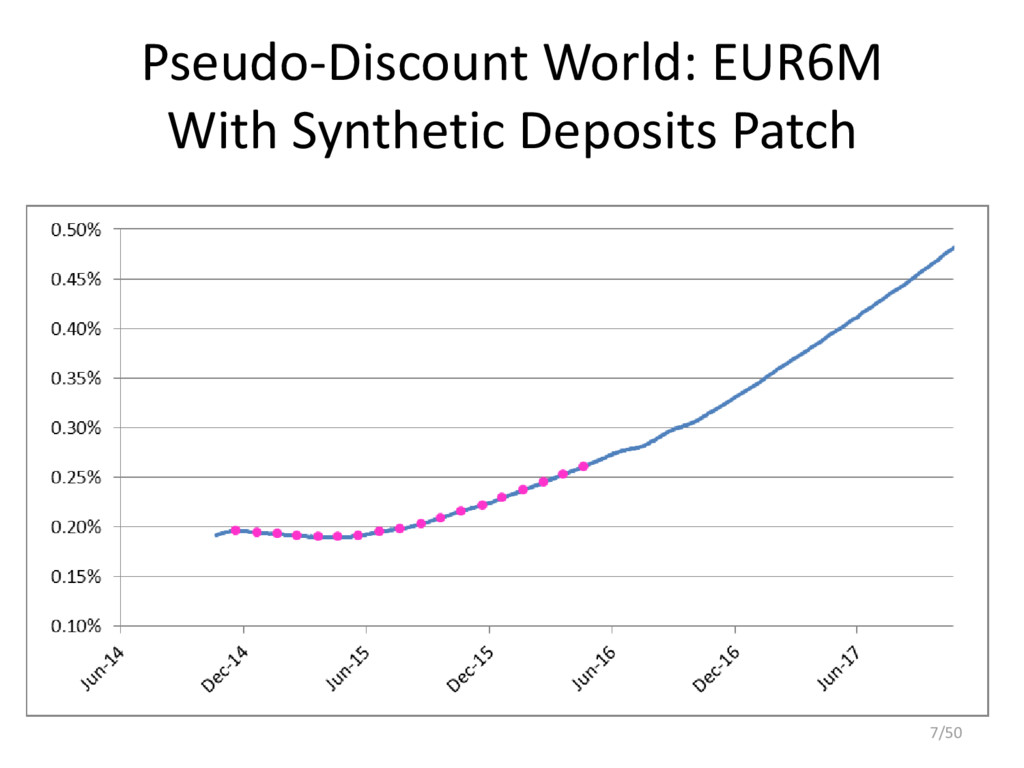

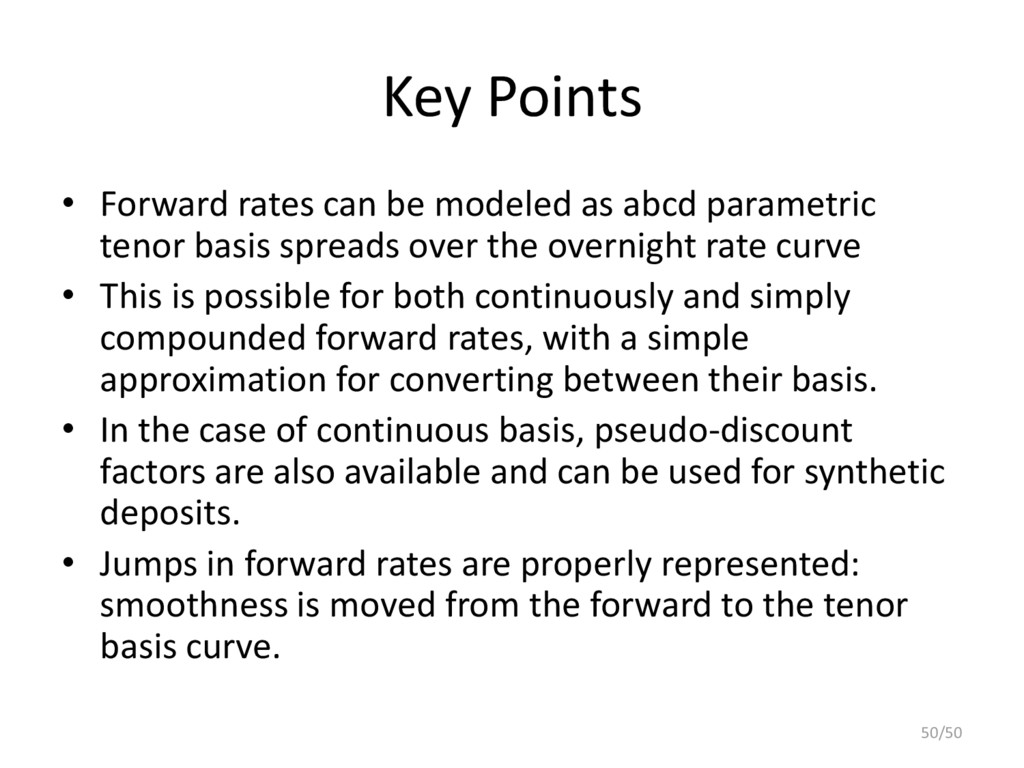

We show that forward rates can be modeled as abcd parametric tenor basis spreads over the underlying overnight rate curve. This is possible for both continuously and simply compounded forward rates, with a simple approximation for converting between the corresponding basis. In the case of continuously compounded tenor basis, pseudo-discount factors are also available for use in legacy systems. Unlike established practices, this approach properly represents the market evidence of jumps in forward rates: smoothness as quality metric is moved from the forward to the tenor basis curve.

![The abcd of Forward Rate Bootstrapping Ferdinando M. Ametrano [email protected]](https://files.speakerdeck.com/presentations/d826ac1ea4c540fdbc5212615360b595/slide_0.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![EUR6M abcd Errors Exact-Fit with ∈ [0.9984, 1.0005] 30/50](https://files.speakerdeck.com/presentations/d826ac1ea4c540fdbc5212615360b595/slide_29.jpg){kind=link}

{kind=link}

{kind=link}

![EUR3M abcd Errors Exact-Fit with ∈ [0.9980, 1.0026] 33/50](https://files.speakerdeck.com/presentations/d826ac1ea4c540fdbc5212615360b595/slide_32.jpg){kind=link}

{kind=link}

{kind=link}

![EUR1M abcd Errors Exact-Fit with ∈ [0.9994, 1.0020] • 36/50](https://files.speakerdeck.com/presentations/d826ac1ea4c540fdbc5212615360b595/slide_35.jpg){kind=link}

{kind=link}

{kind=link}

![EUR1Y abcd Errors Exact-Fit with ∈ [0.9998, 1.0019] • 39/50](https://files.speakerdeck.com/presentations/d826ac1ea4c540fdbc5212615360b595/slide_38.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}