initiative aimed at promoting a wider awareness of the opportunities offered by the advent of exponential technologies in reshaping the way business is conducted and society is governed.

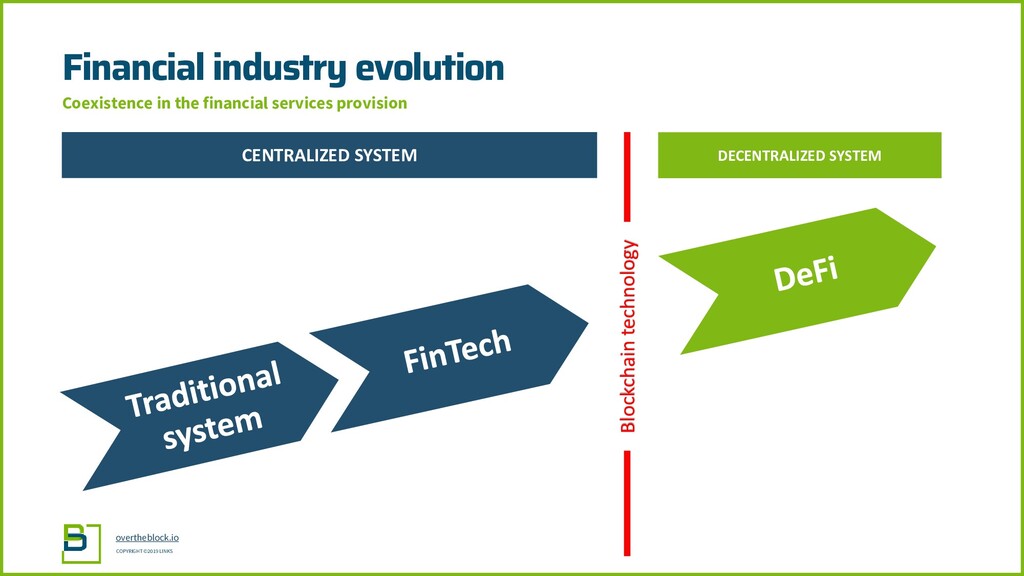

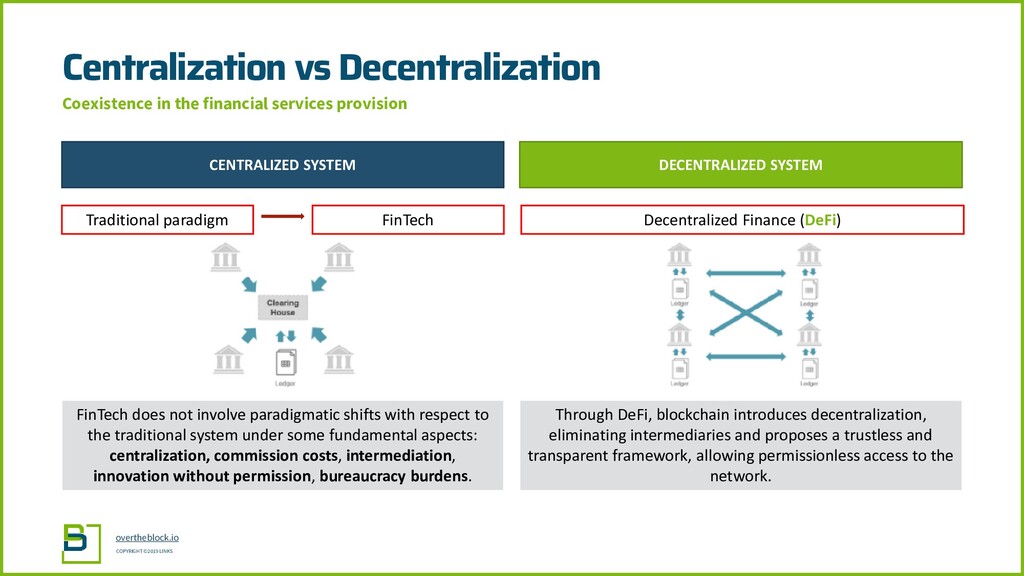

financial services provision CENTRALIZED SYSTEM DECENTRALIZED SYSTEM FinTech does not involve paradigmatic shifts with respect to the traditional system under some fundamental aspects: centralization, commission costs, intermediation, innovation without permission, bureaucracy burdens. Through DeFi, blockchain introduces decentralization, eliminating intermediaries and proposes a trustless and transparent framework, allowing permissionless access to the network. Decentralized Finance (DeFi) Traditional paradigm FinTech

et mi tincidunt, ornare ornare nisl. Quisque dapibus dolor eget lectus mollis, quis porttitor nisl maximus 1. What is DeFi? 2. How does DeFi differ from the standard paradigm?

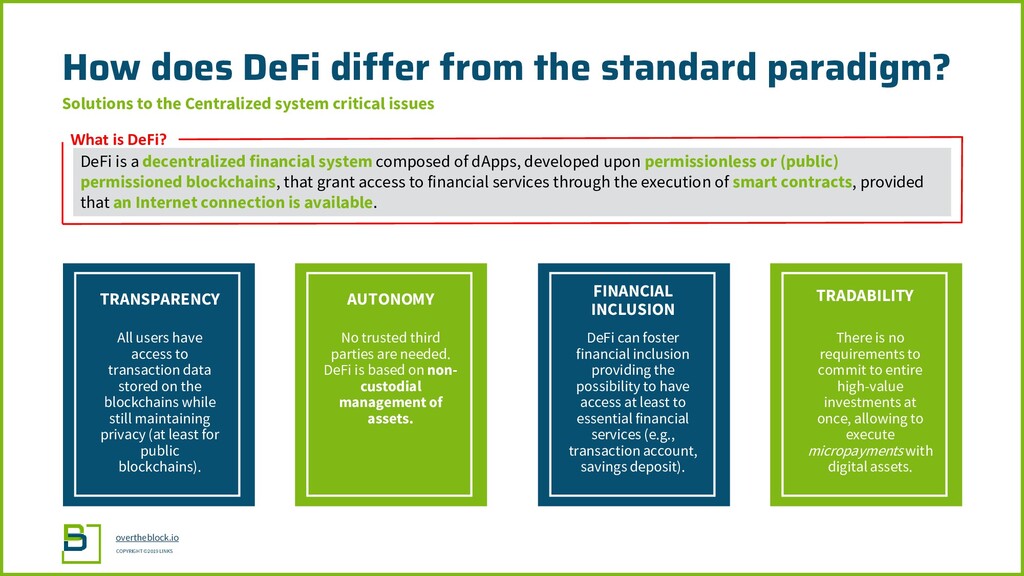

transaction data stored on the blockchains while still maintaining privacy (at least for public blockchains). How does DeFi differ from the standard paradigm? Solutions to the Centralized system critical issues AUTONOMY FINANCIAL INCLUSION No trusted third parties are needed. DeFi is based on non- custodial management of assets. DeFi can foster financial inclusion providing the possibility to have access at least to essential financial services (e.g., transaction account, savings deposit). DeFi is a decentralized financial system composed of dApps, developed upon permissionless or (public) permissioned blockchains, that grant access to financial services through the execution of smart contracts, provided that an Internet connection is available. What is DeFi? TRADABILITY There is no requirements to commit to entire high-value investments at once, allowing to execute micropaymentswith digital assets.

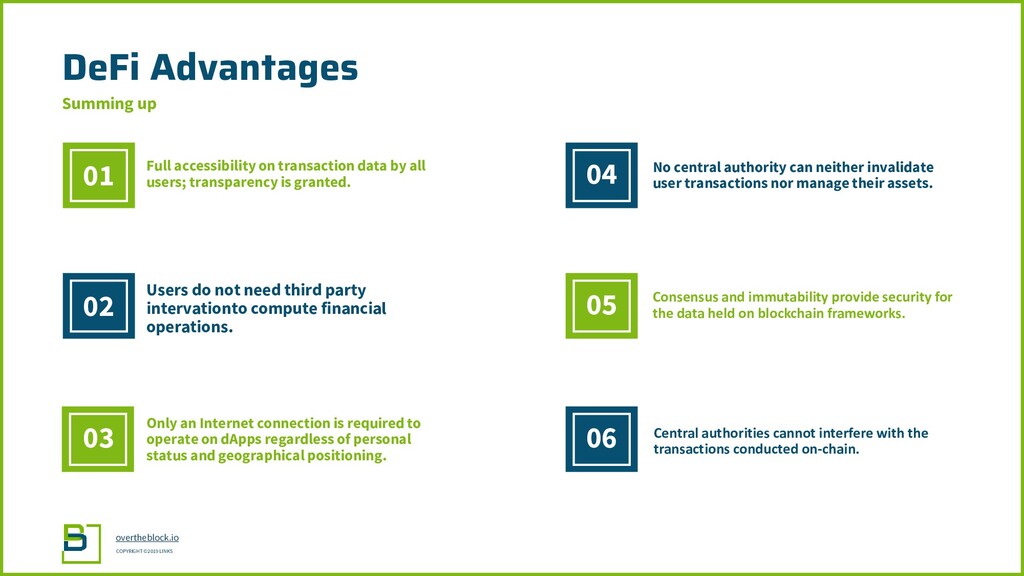

on transaction data by all users; transparency is granted. 01 02 03 04 05 Users do not need third party intervationto compute financial operations. Only an Internet connection is required to operate on dApps regardless of personal status and geographical positioning. No central authority can neither invalidate user transactions nor manage their assets. 06 Central authorities cannot interfere with the transactions conducted on-chain. Consensus and immutability provide security for the data held on blockchain frameworks.

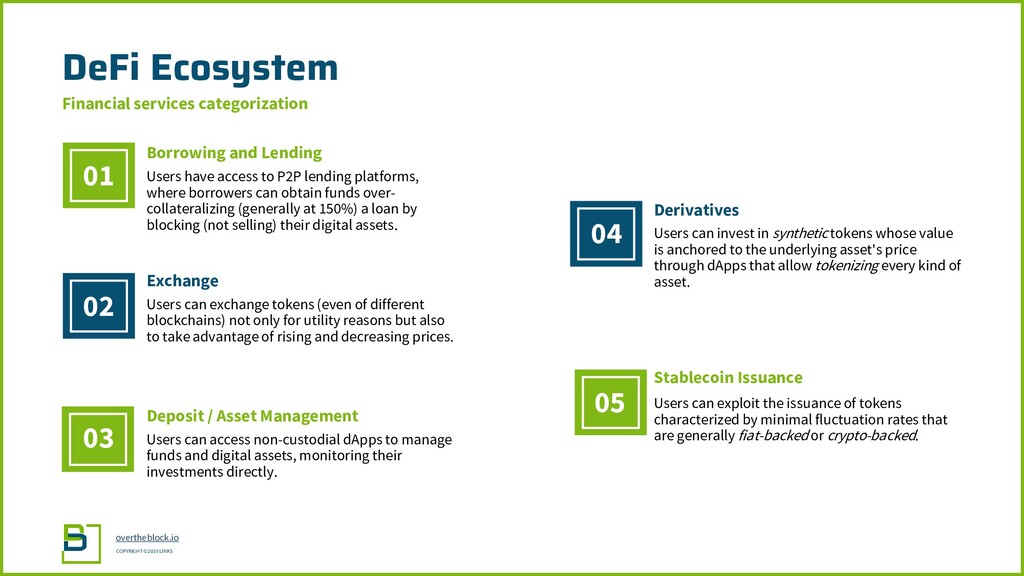

and Lending 01 02 03 04 05 Exchange Deposit / Asset Management Derivatives Stablecoin Issuance Users can exchange tokens (even of different blockchains) not only for utility reasons but also to take advantage of rising and decreasing prices. Users can access non-custodial dApps to manage funds and digital assets, monitoring their investments directly. Users can invest in synthetic tokens whose value is anchored to the underlying asset's price through dApps that allow tokenizing every kind of asset. Users can exploit the issuance of tokens characterized by minimal fluctuation rates that are generally fiat-backedor crypto-backed. Users have access to P2P lending platforms, where borrowers can obtain funds over- collateralizing (generally at 150%) a loan by blocking (not selling) their digital assets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}