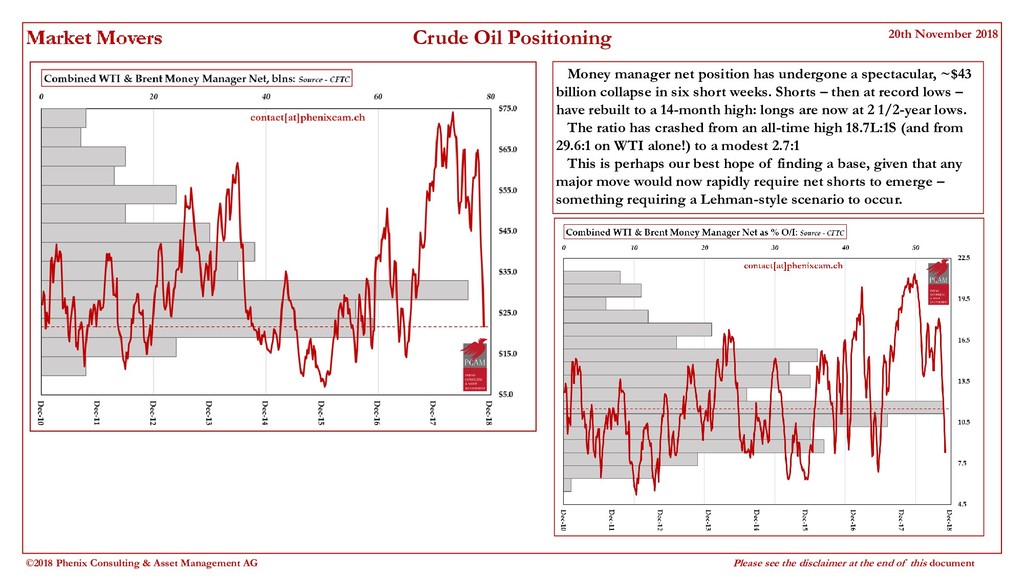

The one way (one timeframe) sell-off in oil continues, threatening to leave a majority of hot money types leaning out of the SHORT side of the boat for the first time since Lehman and hence possibly over-extended on the OTHER side of the ledger.

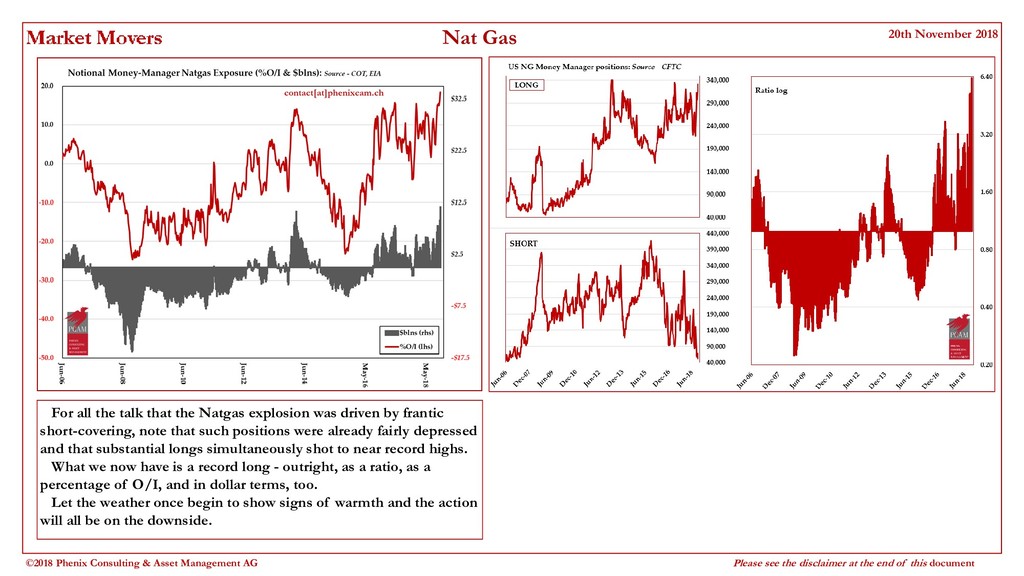

We suggest a couple of key areas to watch both here and also in a Natgas contract driven violently higher by low storage, cold weather and a scramble by the Herd to get long. If those icy weather patterns break after Thanksgiving, it could be cold turkey all round...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}