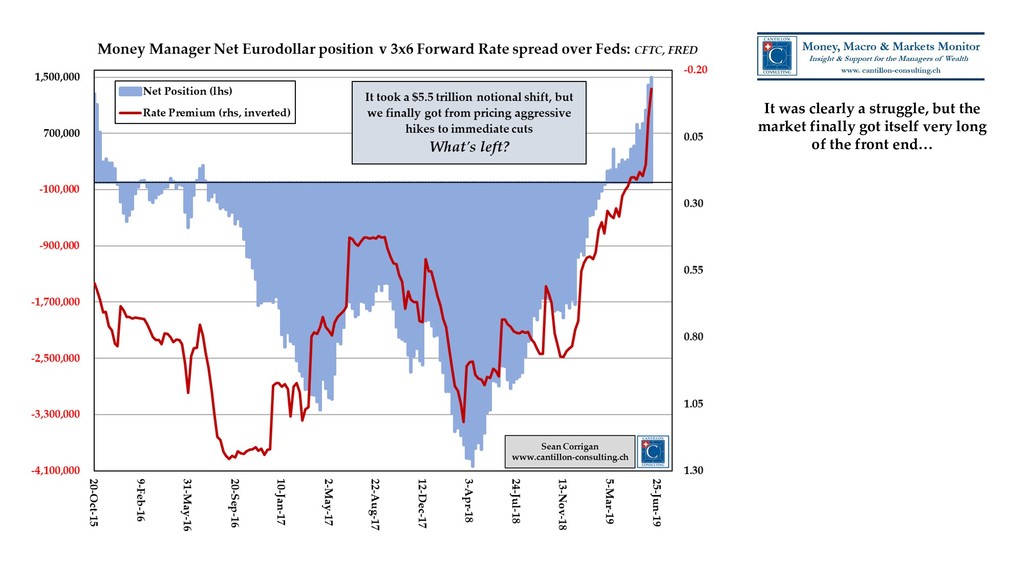

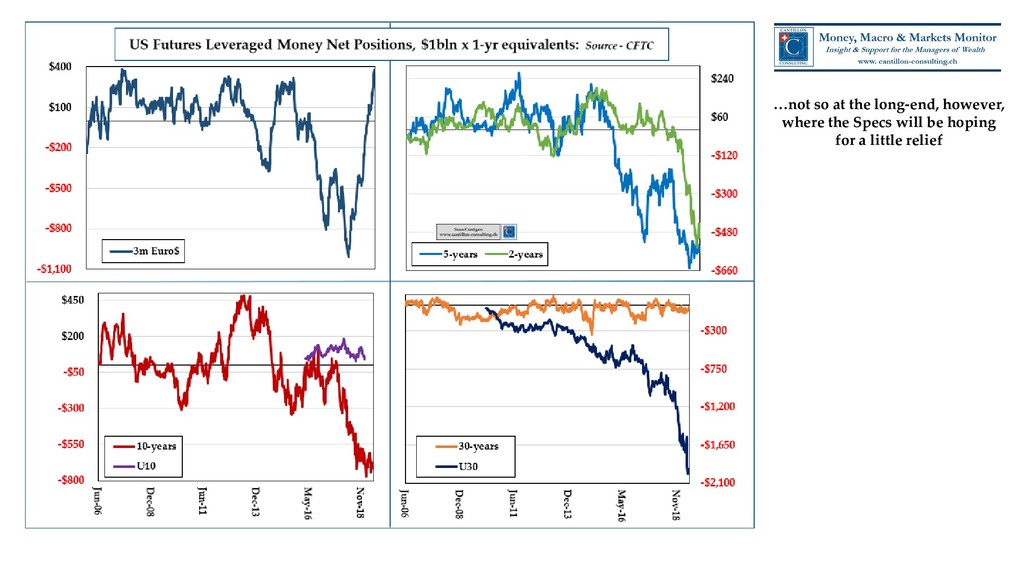

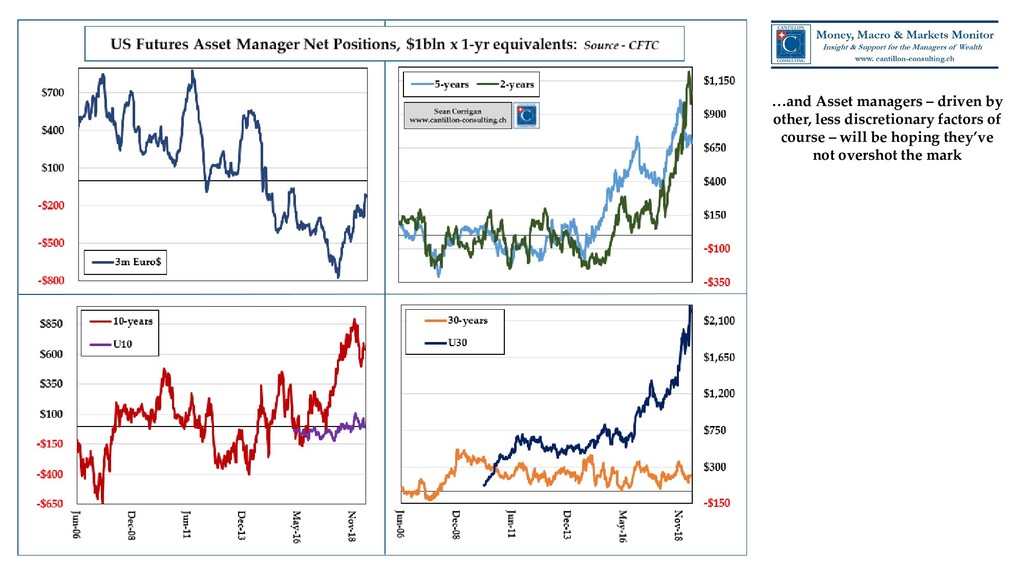

Markets go into the meeting with everything staked on black. Record eurodollar longs for the spec crowd; record long-end position for asset managers. Bond yields at Lehman Crisis lows; 5y5y helpfully declining. Oil and base metals weak; gold testing resistance.

Stock markets and high-yield at or near record highs are the only dissonant factors.

Powell & Co are going to have to disappoint SOMEBODY, here - and we don't mean the man in the Oval Office!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}