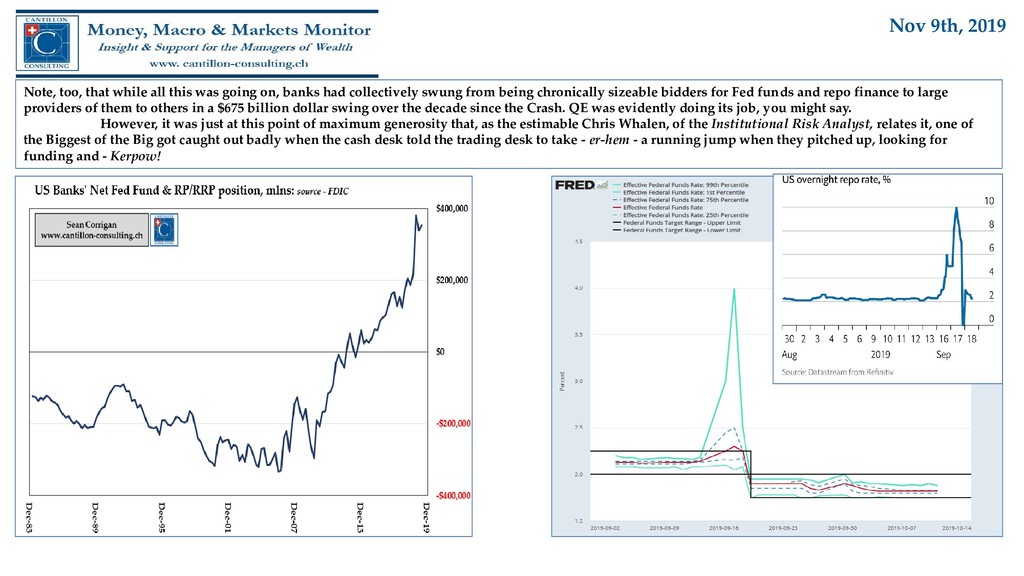

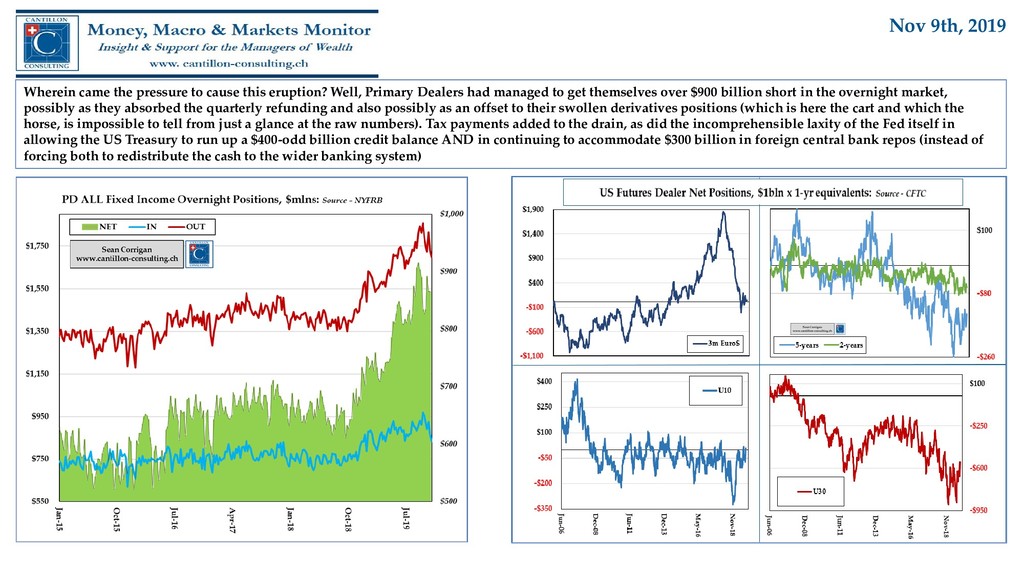

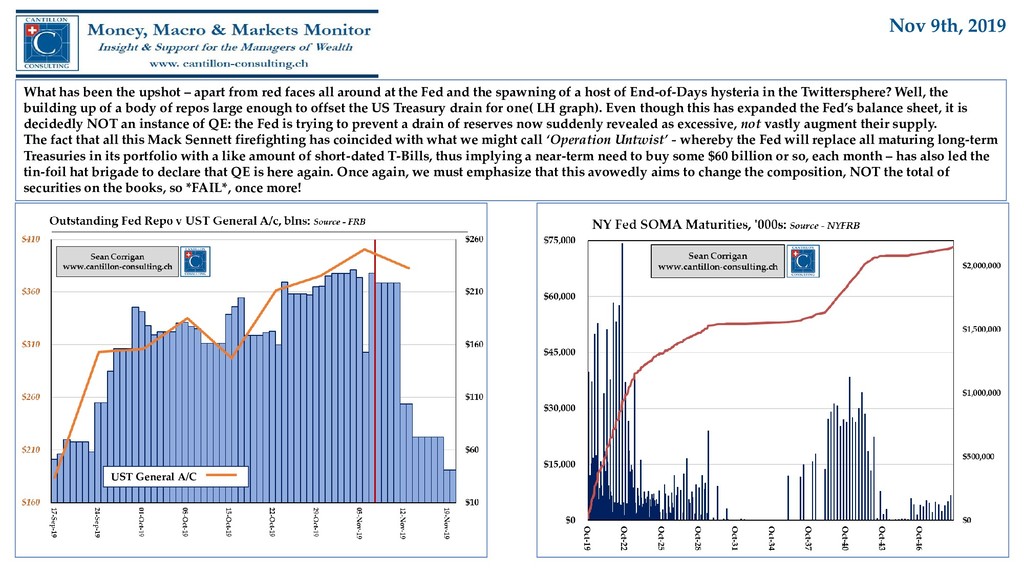

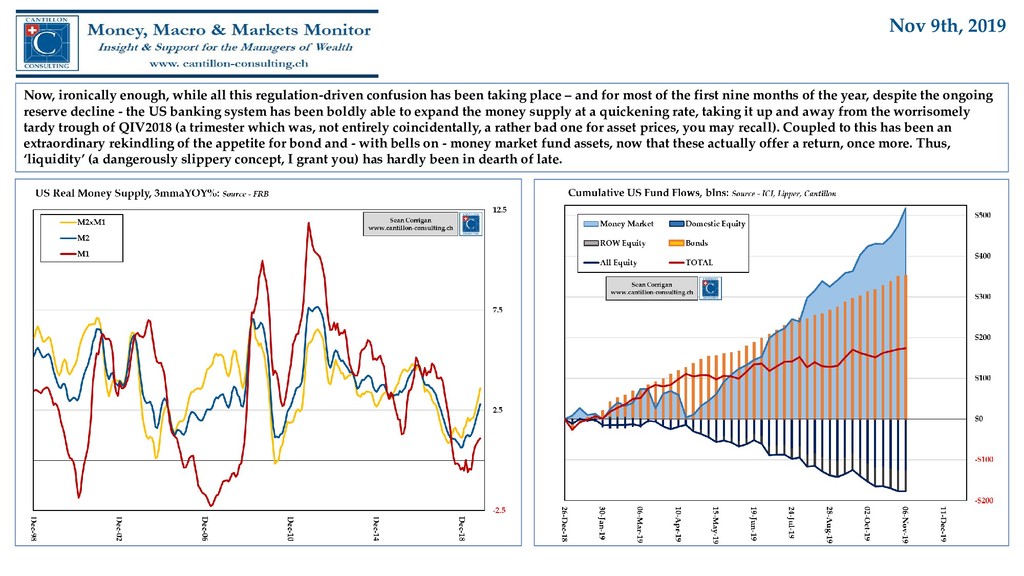

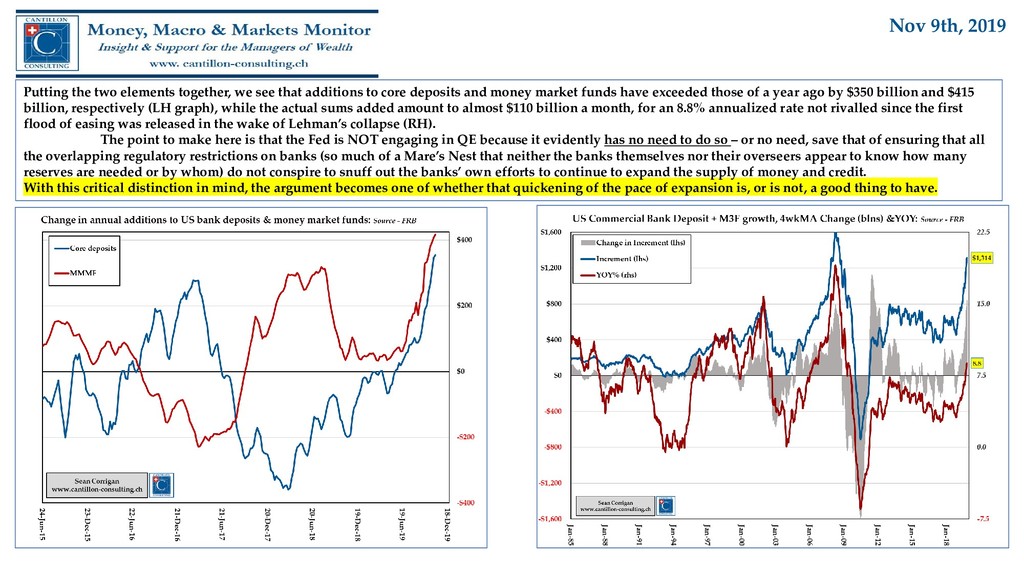

Ever since the repo market shuddered almost to a halt in mid-September, a wrong-footed Fed has been scrambling to try to ensure the seizure does not recur, with its actions leading many commentators to wail that it has re-launched QE. We explain why this is NOT the case - and also point out that such a drastic move would be largely superfluous anyway, given how the banks and money markets were already behaving.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}