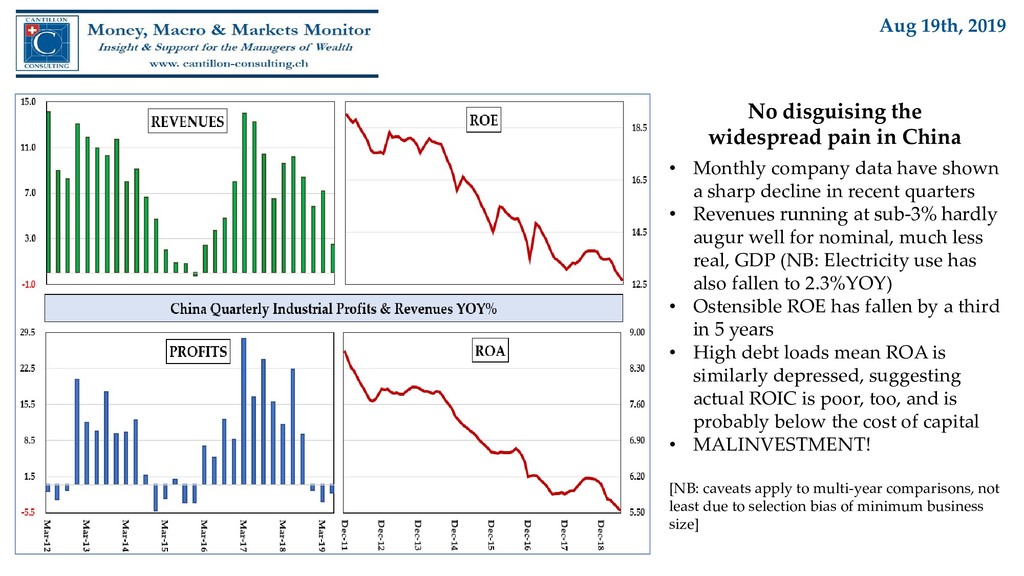

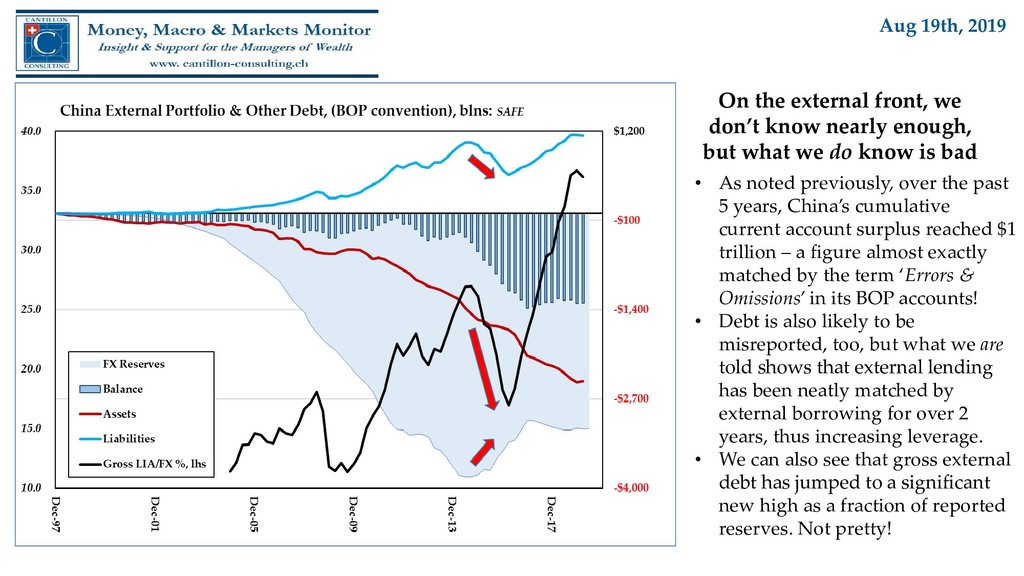

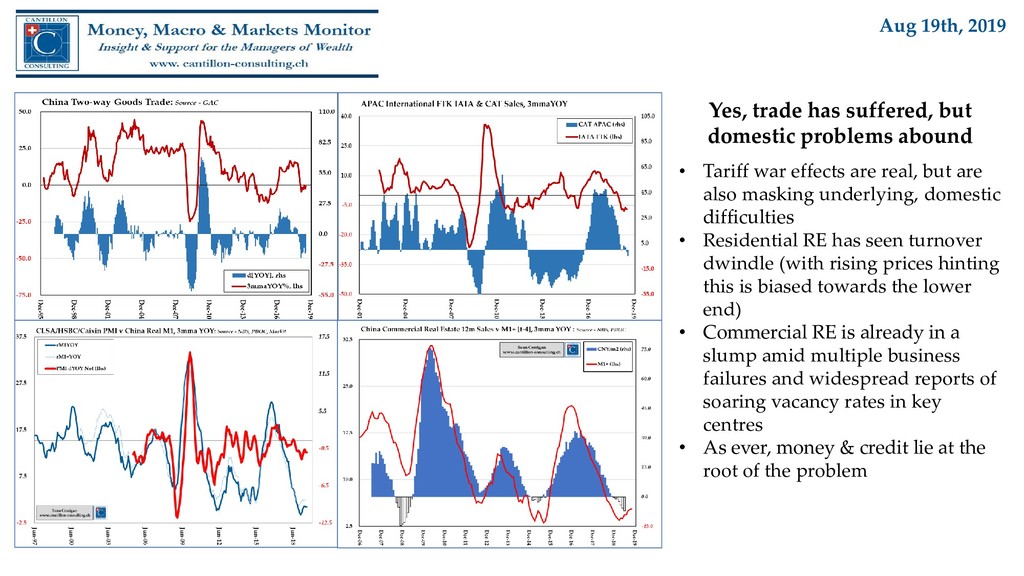

In line with the trends - both real and monetary - whose development we have long been documenting, China's economic situation continues its sharp deterioration, much of it principally domestic in origin, even if being aggravated by President Trump's 'Trade Wars'.

In light of the PBOC's latest parlour trick, hopefully aimed (once more) at easing financing conditions for struggling businesses, we present a short, but concentrated overview of the nation's woes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}