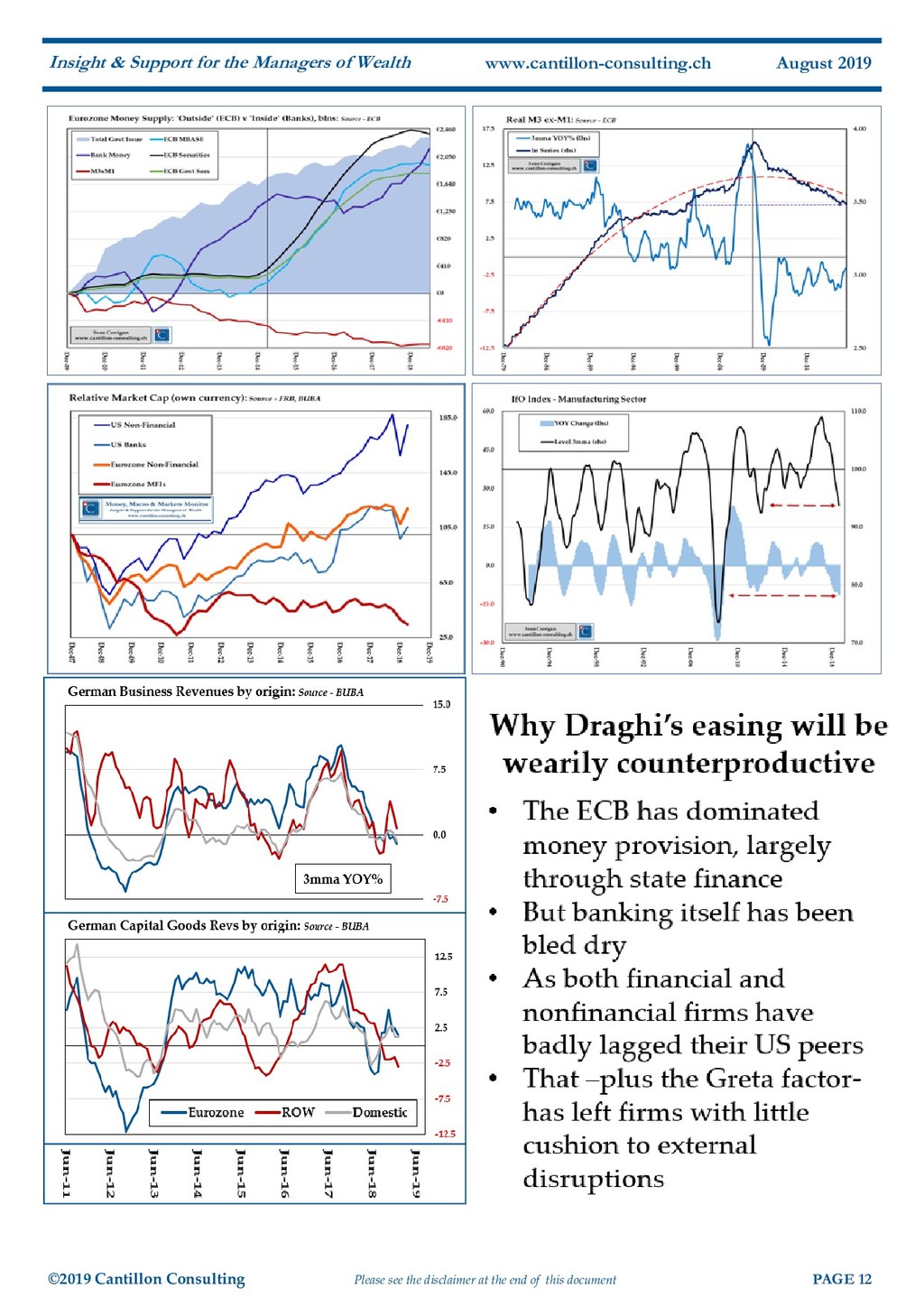

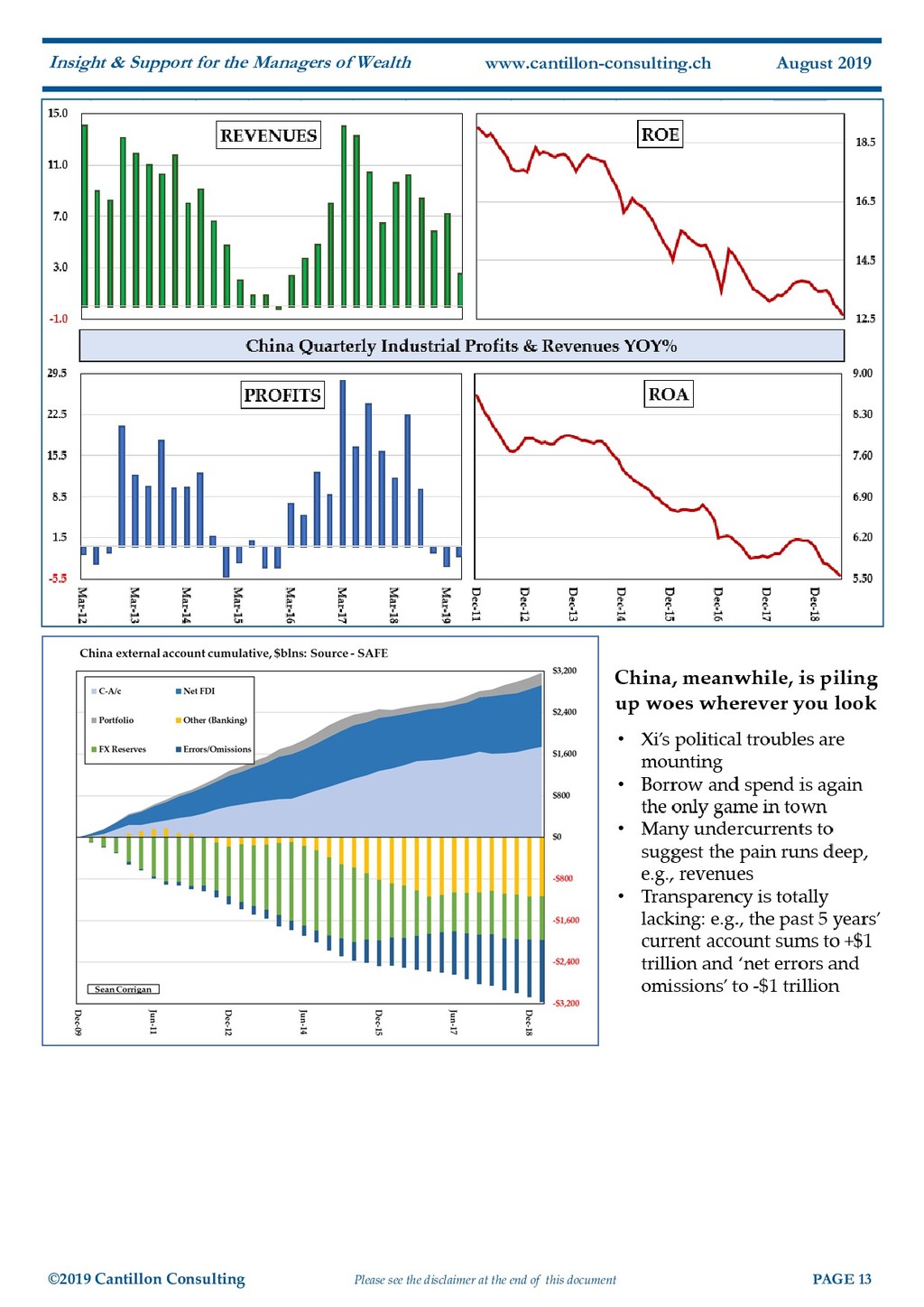

of this document PAGE 4 Insight & Support for the Managers of Wealth www.cantillon-consulting.ch August 2019 fretting about the harm being done to commercial banks; the Fed engaging in a little cheap, CYA by delivering homilies on leveraged lending; the Bank of England’s chief economist laughably expressing belated fears of the ‘culture of low-rate dependency’ in whose seductive poisons he has long been an ac- tive, street-corner trafficker. But principally the attitude is ‘Flucht nach vorne’ - forward flight – with the major central banks gear- ing up to make a Passchendaele-style ‘one more heave’ and force people to pay at least that magic two percent more for their daily bread or else shatter the financial and political machinery in the attempt to do so. Grandpa - through a combination of negative inter- est rates and often binding ceilings on his tax-free accumulations – has been unconstitutionally expro- priated - robbed, even – to finance a Mos Eisley can- tina cast of Zombies, Unicorns, PE Vampires, pub- lic sector drones, and condo flippers. And they wonder why productivity is low, real wages unre- markable, and capital formation anaemic. No real surprise then that Draghi emerged from the ECB’s Unholy Conclave at Sintra, a few weeks back, to deliver a fait accompli with which to tie the hands of his successor (not that the crude political cypher who was later chosen for that role will need much in the way of restraining). A crafty mix of in- sinuation and artful wish-listing sparked the de- sired change in the financial markets, driving the Bund yield to new, negative depths, that on the no- torious Austrian 100-years to sub-unity, and the Greek 10-year to – and briefly through – parity with that of the good ole US of A. Cementing his triumph, the subsequent policy meeting delivered the verdict that rates would re- main at or - crucially - below their current levels for another year, at least, and that among the “options being examined” were “the design of a tiered system for reserve remuneration, and for the size and composition of potential new net asset purchases.” Blackrock’s Mr. Fink helpfully responded by offering to unload a bunch of stock upon him – which may tell you all you need to know about that worthy’s view of the equity market’s near-term prospects and of his wish for a liquidity backstop (c.f., Thomson Hankey, above). Ominously, Draghi mused about the ‘symmetry’ of the Bank’s 2% target which is to say that, whenever price rises do next choose to accelerate, the ECB will not be in any hurry to rein them in, once more, hav- ing thus added a wholly subjective, desired path for prices to the existing, equally fabulous, instantane- ous rate of climb. That, as a moment’s reflection will surely reveal, is a far from innocent addendum. We need look no further than Germany for evi- dence of the slowdown underway in the Eurozone which has prompted such anxiety on carissimo Mari- o’s behalf. Its mighty industrial sector is suffering flat to negative sales at home for the first time in three years; its Eurozone customers are also on strike, registering the first declines in purchases since autumn 2013; and while the count for the rest of the world is just positive overall, its key capital goods exports are off by nearly 3%, also the worst showing since the global, commodity-driven, ‘Hidden Recession’ of 2016. The IfO has dropped like a stone, from post-Unification highs to six-year lows, the sharpest descent since the GFC itself. Over at the Fed, meanwhile, the racing certainty is that cuts are on the way with the only token protes- tation of virtue (“Oooh! Sir Jasper!”) being over the rather trivial issue of whether to deliver one cut of half a point in one go , or two rapid instalments of a quarter. We shall shortly turn to the wisdom of this decision, below. In China, meanwhile, the problems are of a different order. Although rumours abound that a good deal of unsubtle censorship is being exercised (scuttlebutt lent a good deal of credence by the re-

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}