Was the Fed justified in ending its rate hike cycle? Possibly.

Is it justified in reversing those hikes? Probably not.

Are the one-trick ponies at the other central banks likely to succeed?

What do YOU think?

hikes • Trade –and supply chains- are in flux • Wage growth has fallen sharply below the historic ~5% Fed hike threshold • Business Revenues have slowed well below their ~6% trigger rate • Private construction spending is notably weak

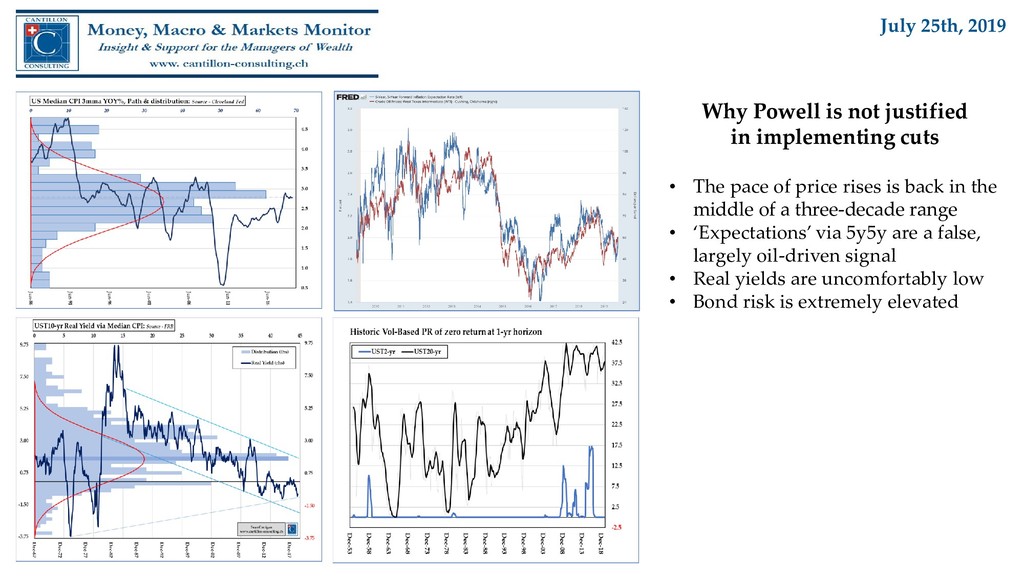

cuts • The pace of price rises is back in the middle of a three-decade range • ‘Expectations’ via 5y5y are a false, largely oil-driven signal • Real yields are uncomfortably low • Bond risk is extremely elevated

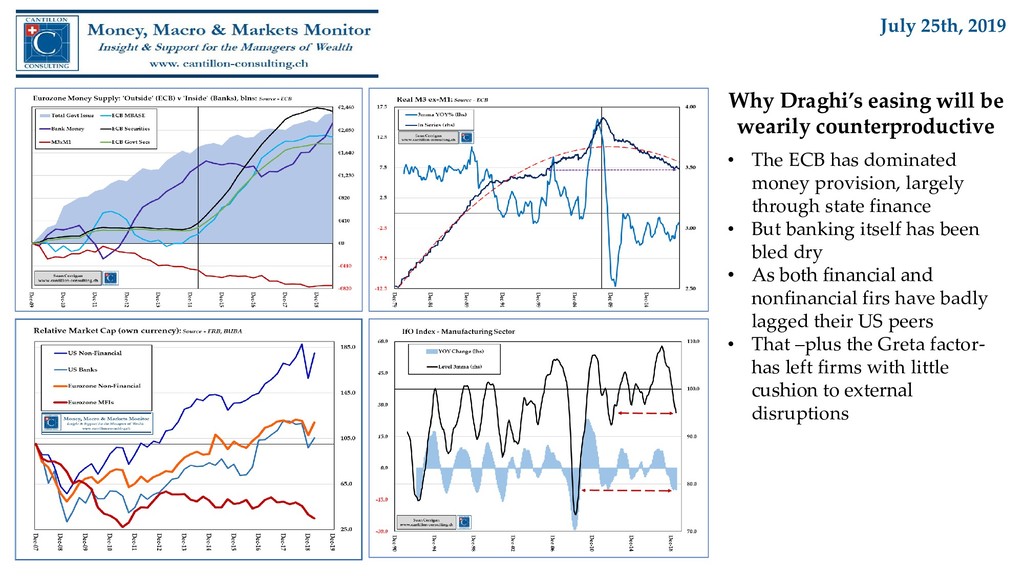

largely through state finance • But banking itself has been bled dry • As both financial and nonfinancial firs have badly lagged their US peers • That –plus the Greta factor- has left firms with little cushion to external disruptions Why Draghi’s easing will be wearily counterproductive

you look • Xi’s political troubles are mounting • Borrow and spend is again the only game in town • Many undercurrents to suggest the pain runs deep • Transparency is totally lacking: e.g., the past 5 years’ current account sums to +$1 trillion and ‘net errors and omissions’ to -$1 trillion

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}