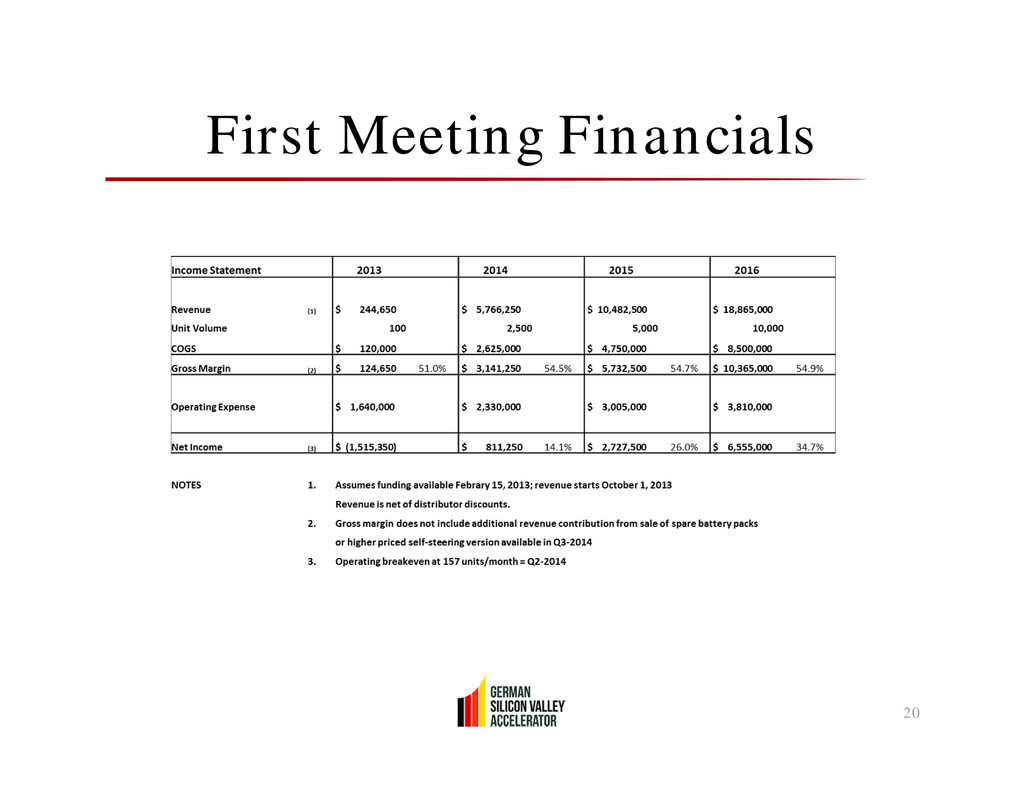

– 2-years by month, 3rd year by quarter • Income statement – Revenue, COGS, warranty cost >> net income – Expenses (partial list): • Headcount (salaries, taxes, benefits) • Commissions, travel, marketing • Contractors, outsourcing, services • Facilities, telecom, hosting, non-capital expenses • Monthly depreciation of capital expenses • Cash flow statement – Financing assumptions (Cash-In: equity, debt, NRE) – Uses of cash (operations, capital expenses) – Cash balance (each month or quarter)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}