Learn the basics of electronic payment processing. A recent Tech Talk at Pivotal Labs in NYC presented by Robert Brodie, Head of Technology Experience at SUMO heavy Industries.

the cardholder’s account for an amount specified by the merchant. • This authorization is held for 1-5 days. (Some banks allow 30) • Once authorized, the merchant can capture at any time prior to the expiration of the authorization.

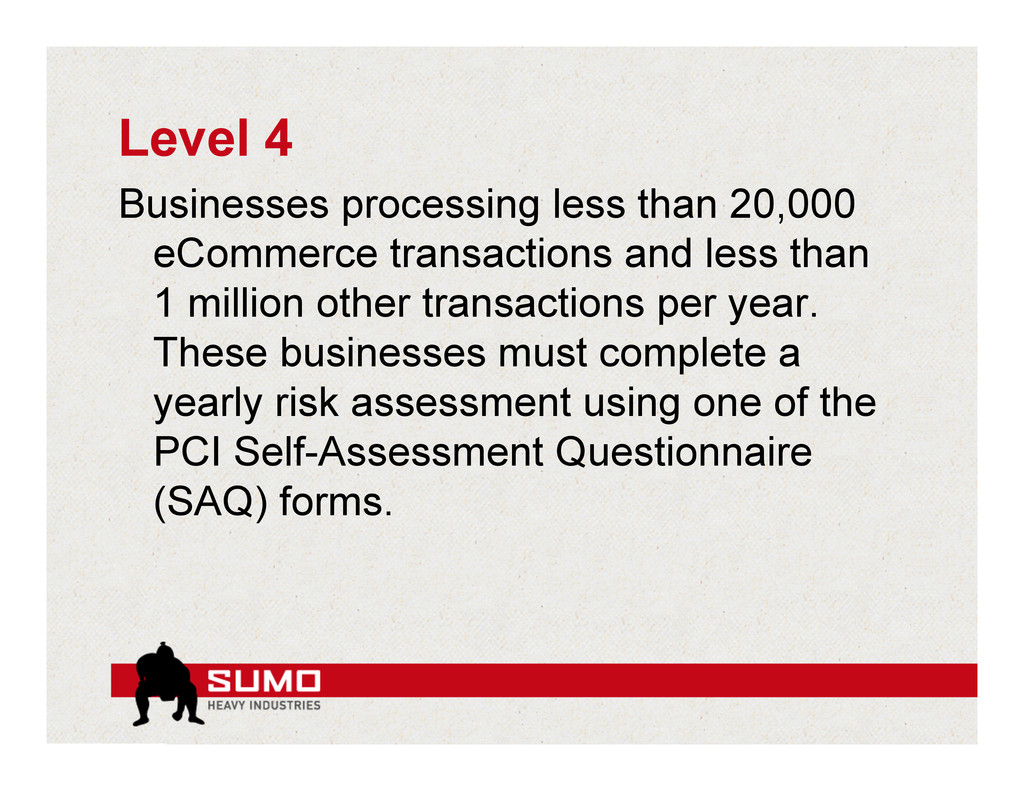

less than 1 million other transactions per year. These businesses must complete a yearly risk assessment using one of the PCI Self-Assessment Questionnaire (SAQ) forms.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}