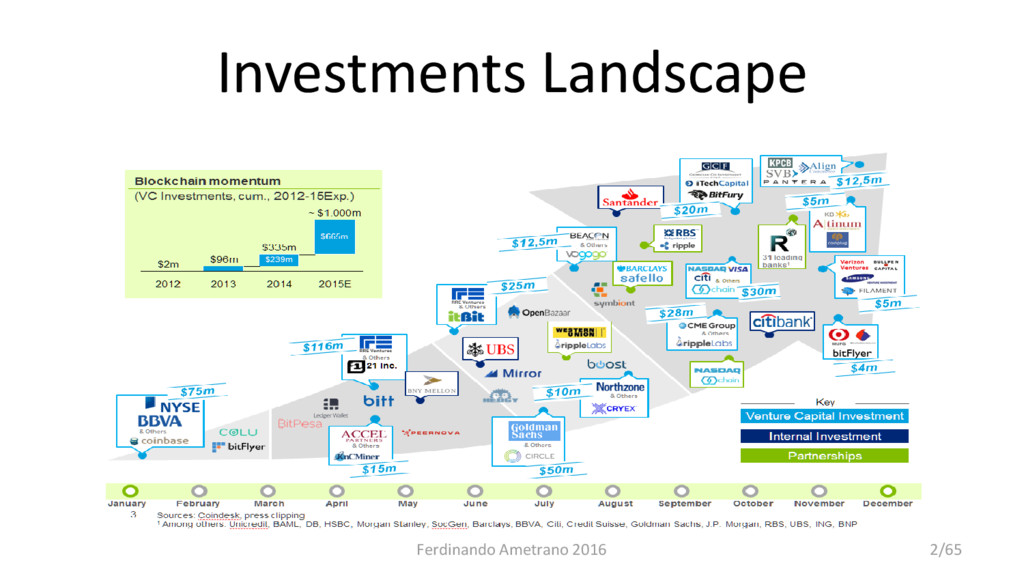

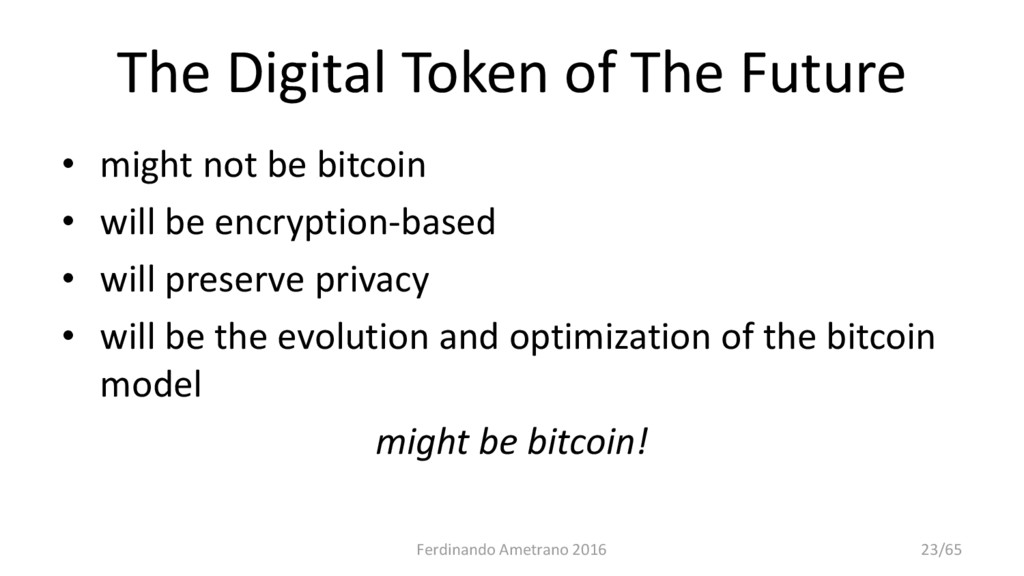

Blockchain needs a native digital asset;

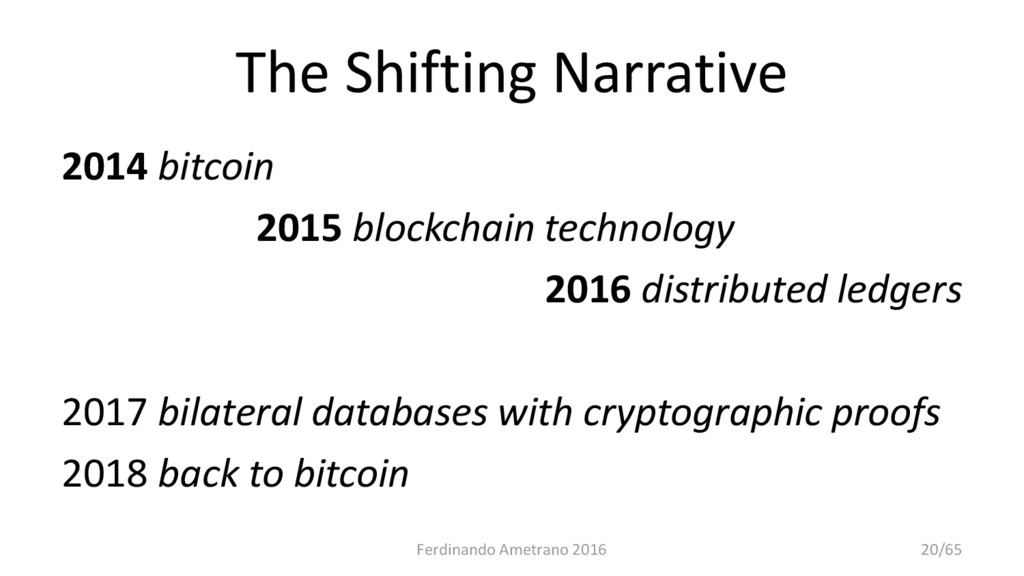

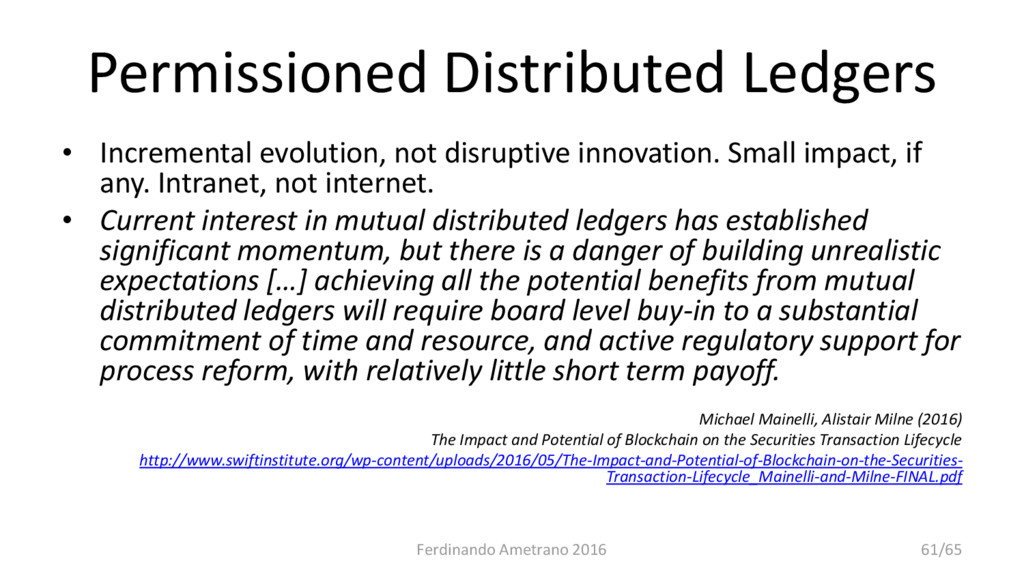

Unrealistic expectations arise from distributed ledger hype;

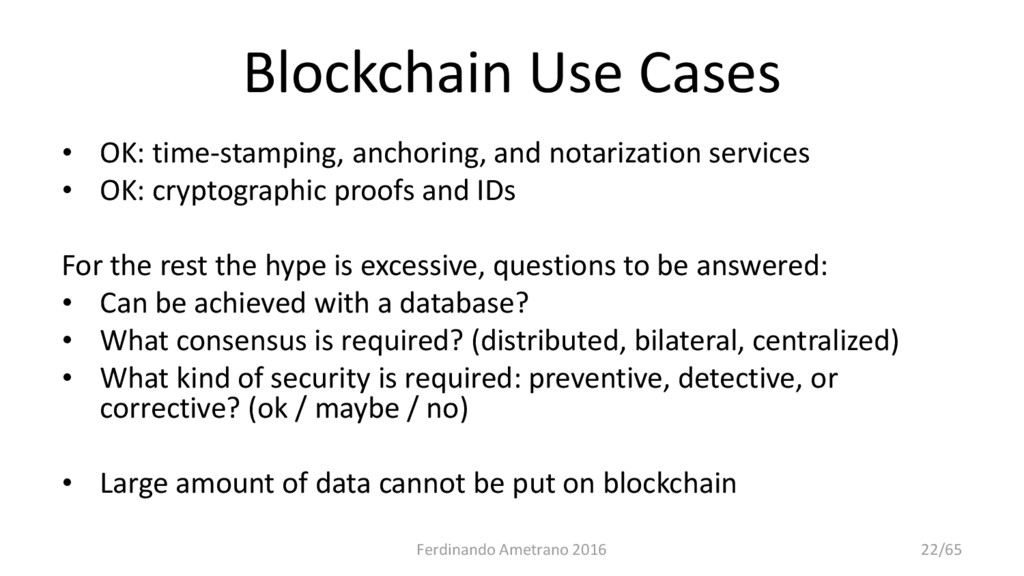

Decentralized transactional network are permissionless;

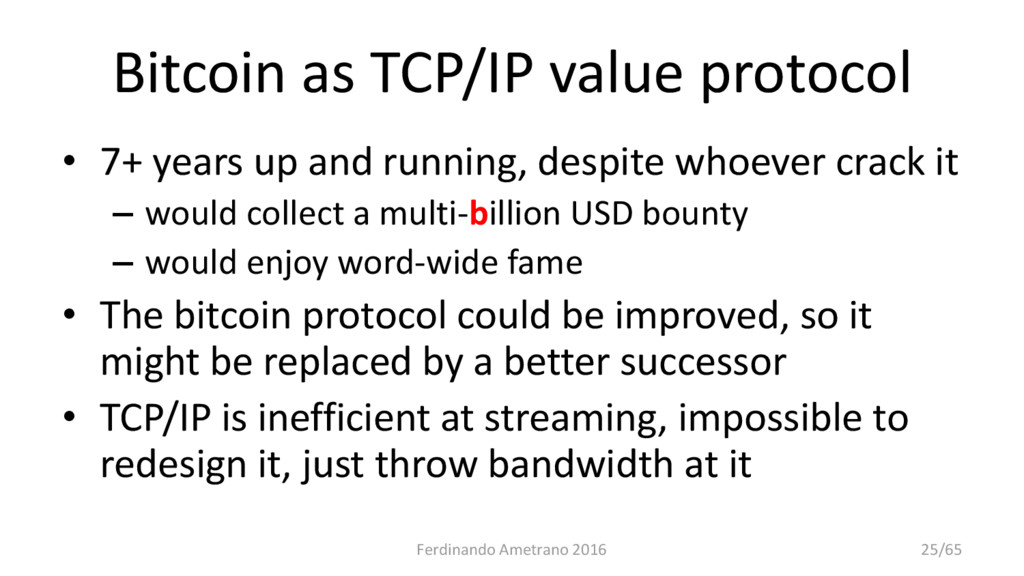

We are at a turning point in the history of money;

Do not slow down banking innovation with regulation;

A level playing field for incumbents and fintechs is needed;

Customer/investor protection should be the highest priority;

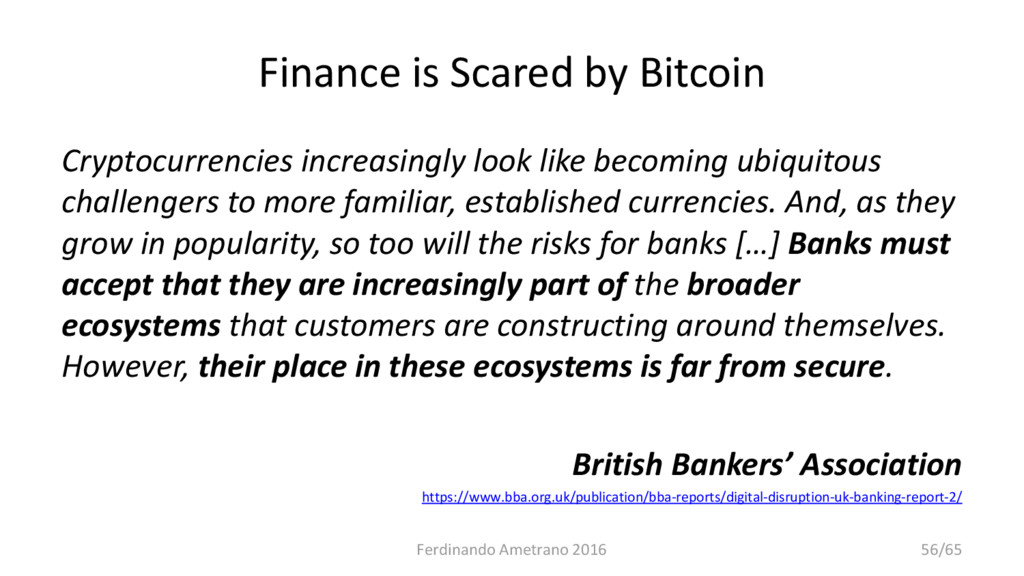

Banks: understand and ride innovation, do not fight it;

Cash digitization is urgent and crucial.

Presented at the Università della Calabria

{kind=link}

{kind=link}

![Opinions • Ben Bernanke: [the virtual currency] may hold long-term](https://files.speakerdeck.com/presentations/655f852ff67f4285917153ad63e16f57/slide_2.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![What is Blockchain? [A hash pointer linked list of blocks]](https://files.speakerdeck.com/presentations/655f852ff67f4285917153ad63e16f57/slide_7.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}